By Sector · By District · By Property Grade · By Tenure

Riyadh's property prices rose 10.6% year-on-year in September 2025 with rental yields averaging 8.89%, Grade A office rents climbed to SAR 2,750 per square metre at 98% occupancy, apartment prices rose 6.3% and villa prices 11.6% year-on-year in Q3 2025, and residential transaction values reached SAR 7.7 billion in Q3 2025 alone a city simultaneously absorbing 675 multinational regional headquarters under the Saudi Regional Headquarters Program, deploying a 176-kilometre metro system across six lines that became fully operational in early 2025, and executing the world's most ambitious single-city real estate transformation programme with over USD 500 billion in Vision 2030 megaproject allocations centred on the Saudi capital.

MARKET SYNOPSIS

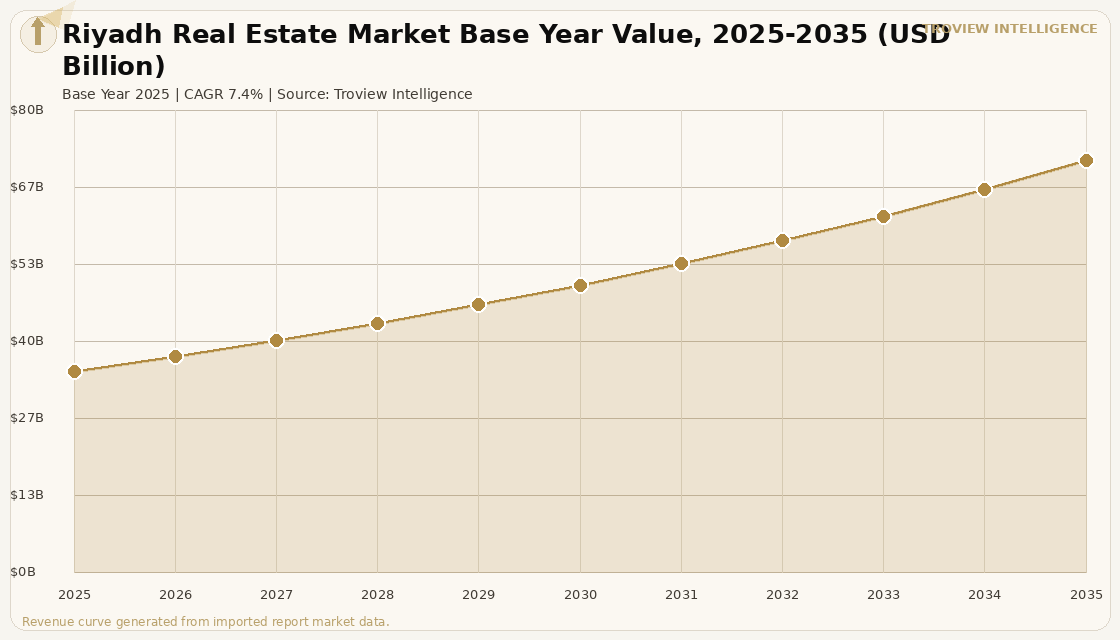

The Riyadh real estate market size was USD 34.82 Billion in 2025 and is expected to register a revenue CAGR of 7.4% during the forecast period, reaching USD 71.27 Billion by 2035. Market revenue growth is supported by the sustained convergence of Vision 2030's megaproject programme, the Regional Headquarters Program's corporate attraction mandate, the Riyadh Metro's full operational launch, and a foreign investment liberalisation agenda that is transforming Saudi Arabia's capital into one of the fastest-growing institutional real estate markets in the world. Riyadh contributed 41.5% of Saudi Arabia's total real estate market value in 2025 per the Saudi Real Estate General Authority, and property prices rose 10.6% year-on-year in September 2025 with rental yields averaging 8.89% per Saudi Central Bank property sector data. Residential transaction values in Riyadh reached SAR 7.7 billion in Q3 2025, representing 17.9% quarter-on-quarter growth per the Saudi Real Estate General Authority's Q3 2025 market review, with apartment prices rising 6.3% year-on-year and villa prices advancing 11.6% over the same period. Foreign investment in Saudi Arabia's real estate sector reached SAR 3 trillion in 2025, with Riyadh capturing the largest share per Saudi Real Estate General Authority investment flow data, as the new Law of Real Estate Ownership by Non-Saudis effective January 2026 opened designated zones to foreign institutional capital.

Riyadh's real estate market is driven by a uniquely concentrated combination of sovereign wealth deployment, government-mandated corporate occupation, and infrastructure-led value creation operating simultaneously in the same urban geography. The Saudi Real Estate Refinance Company plans to refinance SAR 170 billion by 2026, targeting 20% of the Kingdom's residential mortgage market per SRC company disclosures, while the government reduced the minimum down payment from 30% to 5% to expand mortgage accessibility for Saudi homebuyers. Districts near the Riyadh Metro recorded the strongest price appreciation, with Al Taawun recording 32% price growth to SAR 9,470 per square metre and King Abdullah District rising 17% to SAR 7,656 per square metre per Arriyadh Development Authority corridor data. Grade A office supply in Riyadh reached 6.4 million square metres per the General Authority for Statistics, with total office stock projected to rise to approximately 15 million square metres by 2028 as New Murabba, KAFD Phase 2, and private tower deliveries accelerate. For instance, in July 2025, the King Abdullah Financial District was awarded a Guinness World Record for the world's largest continuous pedestrian skyway network, with KAFD hosting more than 140 office tenants and over 75 multinational regional headquarters as of 2026 per KAFD Development and Management Company tenant roster disclosures, confirming Riyadh's emergence as the dominant Gulf commercial real estate market for institutional grade transactions. These are some of the key factors driving revenue growth of the market.

However, the Riyadh real estate market faces structural constraints that moderate the pace and sustainability of growth. The projected doubling of total office stock from approximately 9.7 million square metres across Saudi Arabia in 2025 to approximately 15 million square metres by 2028 creates near-term absorption risk that the Regional Headquarters Program must sustain through continued multinational expansion, and any slowdown in corporate licensing activity after the 2030 Vision deadline could introduce oversupply risk in the northern Riyadh Grade A districts. The Saudi government's 5% Real Estate Transaction Tax introduced in April 2025 per the Saudi Ministry of Finance adds financing friction for developers, increasing transaction costs and moderating the velocity of speculative investment activity in residential and commercial markets. Villa prices rising 11.6% year-on-year and apartment prices 6.3% against a backdrop of government-set affordable homeownership targets is creating affordability pressure that may constrain first-time buyer market conversion rates despite the mortgage down payment reduction to 5%. The government-backed Saudi Real Estate Refinance Company's SAR 170 billion target represents a concentration of financing risk in the sovereign balance sheet that creates a systemic dependency on oil revenue-linked government capital expenditure. These factors substantially limit Riyadh real estate market growth over the forecast period.

Riyadh in 2025 is the most policy-engineered real estate market on the planet. Every meaningful variable corporate tenant demand through the RHQ mandate, infrastructure supply through the metro, affordable housing through SRC mortgage refinancing, foreign investment through the January 2026 ownership law, and capital deployment through PIF's USD 700 billion-plus portfolio is being managed simultaneously by the Saudi government. That is not a criticism. It is an extraordinary statement of ambition and execution capability. The question every investor should ask is: what is the exit velocity of this market when the policy mandates run out? The 2030 deadline is not an endpoint it is the beginning of the test of whether Riyadh's real estate market can sustain organic demand independent of government-mandated corporate occupation." Troview Intelligence Head of Riyadh Real Estate Research

SEGMENT INSIGHTS

By Sector

The commercial office sector is expected to account for a significantly large revenue share in the Riyadh real estate market during the forecast period.

Based on sector, the Riyadh real estate market is segmented into commercial office, residential, retail, hospitality, industrial and logistics, and mixed-use developments. Commercial office dominates the market's institutional investment activity and per-square-metre revenue productivity, with Grade A office rents at SAR 2,750 per square metre at 98% occupancy in Q3 2025, generating the highest rental yields of any Riyadh property class per Saudi Central Bank sector data. Residential is the fastest-growing sector by transaction volume, with SAR 7.7 billion in Q3 2025 transaction values representing 17.9% quarter-on-quarter growth per Saudi Real Estate General Authority quarterly data, driven by the 5% down payment programme, SRC mortgage refinancing, and Saudi homeownership targets requiring 70% homeownership by 2030 under Vision 2030's housing strategy.

By District

King Abdullah Financial District and northern Riyadh districts are expected to account for a significantly large revenue share in the Riyadh real estate market during the forecast period.

Based on district, the Riyadh real estate market is segmented into King Abdullah Financial District, Olaya and Northern Business District, Al Malqa and Al Yasmin metro corridors, King Salman Park and New Murabba development zone, Diriyah Gate heritage district, Diplomatic Quarter and Suleimaniyah, and southern residential districts. KAFD dominates Grade A commercial revenue as the largest LEED Platinum-certified mixed-use district globally, spanning 1.6 million square metres with 95 buildings and hosting more than 140 office tenants per KAFD DMC records. Northern Riyadh metro corridor districts including Al Malqa and Al Yasmin are the fastest-growing residential markets, with Al Taawun recording 32% price growth to SAR 9,470 per square metre per Arriyadh Development Authority corridor data, driven by metro-enabled connectivity to KAFD and the Riyadh North employment districts.

By Property Grade

Grade A office and premium residential properties are expected to account for a significantly large revenue share in the Riyadh real estate market during the forecast period.

Based on property grade, the Riyadh real estate market is segmented into Grade A commercial and premium residential, Grade B mid-market commercial and residential, and Grade C affordable housing and secondary commercial. Grade A commercial dominates institutional investment and per-square-metre revenue, with KAFD's 95 LEED Platinum towers setting the benchmark and the PIF-backed 385-metre PIF Tower incorporating photovoltaic facades that lower energy intensity and command rent premiums above the KAFD average per Public Investment Fund portfolio disclosures. Grade B residential is the fastest-growing segment by new unit delivery, as government homeownership programmes target the middle-income Saudi buyer cohort that requires below-SAR 700,000 priced units in metro-connected northern and eastern Riyadh districts. The Saudi Real Estate General Authority confirmed that Grade A spaces hold 47.9% market share in Riyadh office demand, with rents up 23% year-on-year from the base established before the Regional Headquarters Program reached scale.

District Deep-Dives

KING ABDULLAH FINANCIAL DISTRICT (KAFD) RIYADH'S GLOBAL BUSINESS DISTRICT

| Total Area | 1.6M m², 95 buildings, 25 architectural firms | Certification | World's largest LEED Platinum mixed-use district |

| Office Tenants | 140+ (75+ multinational regional HQs as of 2026) | Guinness Record | World's largest continuous pedestrian skyway (Jul 2025) |

KAFD is Riyadh's premier commercial district and the anchor of Saudi Arabia's Regional Headquarters Program, owned and managed by the KAFD Development and Management Company, a wholly-owned subsidiary of the Public Investment Fund per PIF portfolio disclosures. The district spans 1.6 million square metres across 95 towers designed by 25 world-leading architectural firms including HOK, SOM, Gensler, Foster and Partners, and Omrania, and achieved designation as the world's largest LEED Platinum-certified mixed-use district per the US Green Building Council. As of 2026, KAFD hosts more than 140 office tenants and over 75 regional headquarters for multinational companies per KAFD DMC tenant roster data, with the September 2025 opening of EY's 11,691 square metre MENA headquarters the most recent major addition to the professional advisory tenant cluster. The KAFD metro station, designed by Zaha Hadid Architects and operational since late 2024, provides direct metro connectivity as part of the Riyadh Metro network, while the 3.6 kilometre driverless monorail with six stations is targeting 2027 public operation per KAFD infrastructure documentation. Expansion plans to double KAFD's footprint and accommodate 40,000 daily visitors represent the largest single pipeline of Grade A commercial real estate in the Gulf region.

OLAYA / NORTHERN BUSINESS DISTRICT PREMIUM CORPORATE AND RETAIL CORRIDOR

| Character | Corporate towers, luxury retail, hotel cluster | Key Assets | Faisaliyah Tower, Kingdom Centre Tower |

| Metro Access | Olaya Station, Line 4 and 5 interchange | Rent Trajectory | Rising with northward tenant migration |

The Olaya corridor and Northern Business District form Riyadh's established premium corporate and retail spine, anchored by the Faisaliyah Tower and the Kingdom Centre Tower, the city's most recognisable commercial landmarks, and extending north along King Fahd Road toward the KAFD district that has become the destination for multinational headquarters operations. Occupiers in Olaya and the northern corridor are increasingly choosing the submarket over southern Riyadh locations to avoid traffic congestion, a migration dynamic confirmed by the Saudi Real Estate General Authority's Q2 2025 occupier survey. The Riyadh Metro's Olaya Station, operational since early 2025 per the Arriyadh Development Authority, provides connectivity to KAFD, the airport, and southern residential districts, supporting the hybrid-working patterns of Saudi and expatriate employees who commute between northern employment corridors and southern residential zones. International luxury hotel operators including IHG, Marriott, and Hilton have concentrated their Riyadh flagship properties in the Olaya-King Fahd Road corridor, reflecting the district's status as Riyadh's primary destination for corporate travel and events.

AL MALQA / AL YASMIN (METRO CORRIDORS) FASTEST-GROWING RESIDENTIAL DISTRICTS

| Al Taawun Price Growth | 32% to SAR 9,470/m² | King Abdullah District Growth | 17% to SAR 7,656/m² |

| Price Growth Driver | Riyadh Metro Line 6 connectivity | Villa Sales 2025 | Q1 2025: +10.3% YoY |

The northern residential districts of Al Malqa, Al Yasmin, Al Taawun, and adjacent metro corridor communities are recording the strongest real estate price appreciation in Riyadh, driven by direct metro connectivity to the KAFD employment hub and the King Abdullah Financial District via the Riyadh Metro Line 6 that became fully operational in early 2025 per the Arriyadh Development Authority. Al Taawun recorded a 32% price increase to SAR 9,470 per square metre, the strongest single-district appreciation in Riyadh's residential market in 2025, per Saudi Real Estate General Authority property price indices, confirming the transit premium that metro connectivity creates in previously under-valued northern residential districts. Villa prices in metro-connected northern Riyadh districts rose 10.3% year-on-year in Q1 2025, substantially outpacing apartment price growth of 1.2% in the same period, as expatriate professional families and returning Saudis favour villa format housing with garden space in the northern corridors. King Salman Park, the 14 square kilometre royal park project under development in northern Riyadh per the King Salman Park Foundation, represents the most significant green infrastructure investment in Riyadh's history and is already generating substantial premiums for residential and commercial properties within its catchment.

| Total Investment | USD 50 Billion+ (Diriyah Gate Development Authority) | UNESCO Status | At-Turaif District, UNESCO World Heritage Site |

| Target Visitors | 27 million annually by 2030 | Asset Mix | Luxury hospitality, cultural, residential, commercial |

Diriyah Gate is Riyadh's most ambitious heritage regeneration project, developed by the Diriyah Gate Development Authority as a UNESCO World Heritage site transformation into a luxury cultural and lifestyle destination targeting 27 million annual visitors by 2030. The development centres on the At-Turaif district, the historic home of the Al Saud family and the original seat of the first Saudi state, which received UNESCO World Heritage designation in 2010 and is being complemented by purpose-built luxury hotels, cultural institutions, retail experiences, and premium residential products across the 14 square kilometre site adjacent to Riyadh's northern urban edge. The project's luxury positioning, targeting ultra-high-net-worth Saudi and international visitors through a curated hospitality programme, creates a distinct commercial real estate segment within the Riyadh market that operates at price points and with tenant profiles entirely different from the corporate and residential mainstream. Diriyah Gate residential units are expected to command the highest per-square-metre residential prices in Saudi Arabia upon delivery, establishing a benchmark for luxury real estate pricing in the Kingdom comparable to the premium commanded by comparable heritage-adjacent developments in Doha and Dubai.