By Submarket · By Property Grade · By J-REIT Vehicle · By Occupier Sector

Tokyo Grade A office vacancy tightened to 1.0% in Q3 2025 the lowest in 18 years while Grade A rents spiked 3.4% quarter-on-quarter to JPY 39,750, the largest single-quarter increase since Q3 2007, and Grade A vacancy fell further to a historic low of 0.7% in February 2026 with prime rents reaching JPY 41,050 per tsubo, as new supply from the Nihonbashi, Toranomon, and Yaesu redevelopment corridors was absorbed faster than delivered across the world's tightest major office market.

MARKET SYNOPSIS

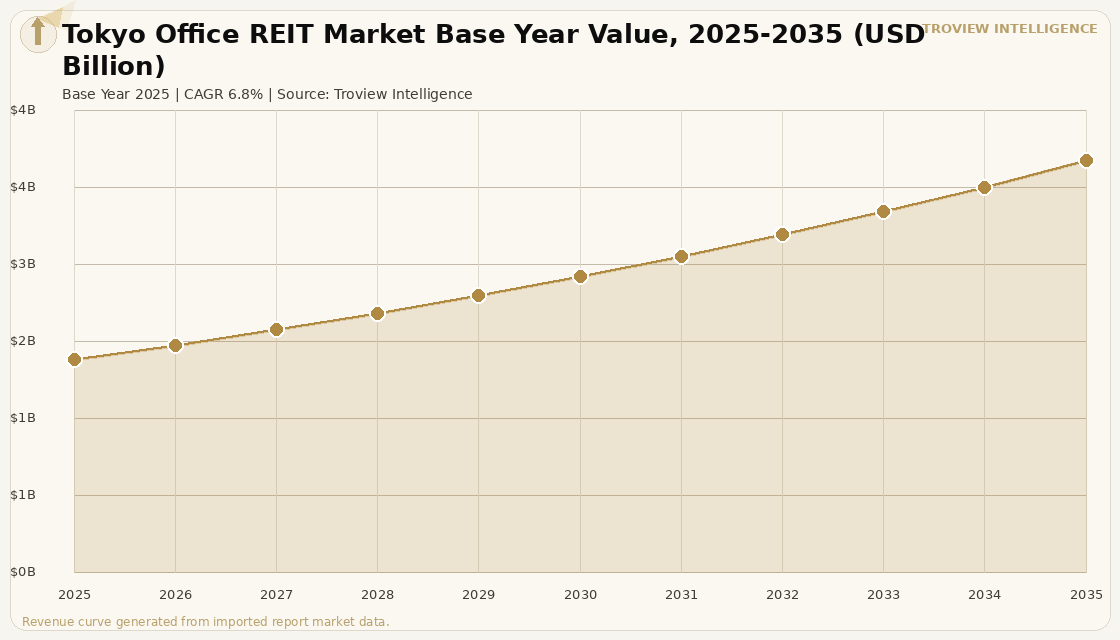

The Tokyo office REIT market size was USD 1.96 Billion in 2025 and is expected to register a revenue CAGR of 6.8% during the forecast period, reaching USD 3.79 Billion by 2035. Market revenue growth is supported by a structural tightening of office supply across Tokyo's five central wards Chiyoda, Chuo, Minato, Shibuya, and Shinjuku that has produced rental growth at the fastest pace since Q3 2007 and drawn foreign institutional capital into J-REIT vehicles at a pace not seen since the pre-global financial crisis cycle. Tokyo Grade A office vacancy fell to 1.0% in Q3 2025 per Ministry of Land, Infrastructure, Transport and Tourism property market data, and tightened further to 0.7% in February 2026 as verified by market data from Sanko Estate, with prime rents reaching JPY 41,050 per tsubo and Grade A rents in Q3 2025 at JPY 39,750 representing the highest level since Q1 2020. The five central wards vacancy rate for Grade A Tokyo offices dropped to 2.6% in 2025 per Miki-Shoji data, even as new office building supply increased to approximately 200,000 tsubo in 2025 from approximately 75,000 tsubo in 2024, as pre-leasing rates across new developments in the Nihonbashi Honcho, Toranomon Hills Business Tower, and Yaesu redevelopment districts absorbed new stock ahead of practical completion. The Japan Exchange Group confirmed that Nippon Building Fund Inc. became the first J-REIT to surpass the JPY 1 trillion mark in total assets, with the vehicle's portfolio concentrated in large-scale Grade A office towers in Tokyo's most liquid submarkets.

Tokyo's office REIT revenue growth is anchored by the convergence of three structural forces: a supply pipeline that has remained below historical averages for a decade following the post-2012 construction pause, corporate return-to-office adoption that has exceeded that of most other major Asian cities, and foreign institutional capital allocation to J-REIT vehicles as a liquid, transparent proxy for Tokyo Grade A office income. The Government Pension Investment Fund of Japan, the world's largest pension fund, held approximately JPY 2.1 trillion in domestic real estate and infrastructure assets as of March 2025 per its annual report, creating an institutional anchor that supports J-REIT market stability and borrowing costs. The Tokyo Metropolitan Government's urban redevelopment policies, specifically the strategic urban area designation that provides height relaxation and floor area bonuses for mixed-use developments meeting sustainability criteria, have concentrated next-generation office supply in the Toranomon, Nihonbashi, and Marunouchi corridors where J-REIT acquisition interest is greatest. For instance, in January 2026, Nippon Building Fund Inc., Japan, announced the acquisition of the newly delivered Nihonbashi Honcho M-SQUARE office building from Mitsui Fudosan Co., Ltd. and Kajima Corporation for approximately JPY 32.1 billion at a NOI yield of 3.3%, reflecting the premium pricing that Tokyo Grade A new supply commands from the J-REIT market and confirming that even at low cap rates the acquisition is accretive to distributable income given the all-grade vacancy backdrop. These are some of the key factors driving revenue growth of the market.

However, the Tokyo office REIT market faces structural constraints that moderate the pace of earnings growth for investors through the forecast period. The Bank of Japan's policy rate hike in January 2025, the first rate increase in decades, raised J-REIT borrowing costs and compressed the positive spread between Tokyo office cap rates and JPY funding costs that historically supported leveraged distribution growth for office-specialised J-REITs. The TSE REIT Index closed at 1,691.63 points as of March 31, 2025 per the Japan Exchange Group, reflecting investor caution toward J-REIT unit prices as rate expectations evolved upward, and representing a material discount to the historical high of 2,612.98. The significant increase in new office supply in 2025, with approximately 200,000 tsubo completing across Tokyo versus approximately 75,000 tsubo in 2024 per Miki-Shoji data, creates lease-up risk for developments that entered construction before pre-leasing was fully secured, potentially introducing localised vacancy in specific buildings even as the market-wide rate remains historically tight. A 2025 World Economic Forum survey found that 82.2% of Japanese workers wished to continue teleworking, creating long-term uncertainty about the quantum of office space that large Tokyo corporates will require at lease renewal relative to their current contracted footprints. These factors substantially limit Tokyo office REIT market growth over the forecast period.

Tokyo's Grade A vacancy at 0.7% in February 2026 is not a temporary post-pandemic bounce it is the product of a decade of below-average supply delivery colliding with a corporate sector that is committing to premium office space at unprecedented lease lengths and rent levels. The J-REIT vehicles that own the right buildings in the right corridors Nihonbashi, Toranomon, Shinjuku are sitting on an income stream that will compound at 4% to 6% annually through the end of the decade without any need for heroic assumptions. The rate environment is the conversation everyone is having. The vacancy is the reality that will drive returns." Troview Intelligence Senior Analyst, Tokyo Office Markets

SEGMENT INSIGHTS

By Property Grade

Grade A and newly delivered office assets in Tokyo are expected to account for a significantly large revenue share in the Tokyo office REIT market during the forecast period.

Based on property grade, the Tokyo office REIT market is segmented into Grade A, Grade B, and Grade C office assets. Grade A assets dominate J-REIT net operating income and distributable earnings in Tokyo, with vacancy at 1.0% in Q3 2025 per Ministry of Land, Infrastructure, Transport and Tourism data and rents spiking to JPY 39,750 per tsubo, the highest since Q1 2020. Newly delivered buildings targeting CASBEE S-rank sustainable building certification command rent premiums of 12% to 15% over legacy Grade A properties per investor disclosures from leading Tokyo developers, creating a sustainability stratification within the Grade A segment that J-REIT managers are actively exploiting through asset rejuvenation. Grade B assets within Tokyo J-REIT portfolios are expected to register declining NOI contributions over the forecast period as Nippon Building Fund's January 2026 disposal of the 34-year-old Sumitomo Densetsu Building at JPY 10.0 billion illustrates the active management of secondary asset exposure that defines leading J-REIT strategies.

By Submarket

Central five wards office assets, led by the Marunouchi, Toranomon, and Nihonbashi corridors, are expected to account for a significantly large revenue share in the Tokyo office REIT market during the forecast period.

Based on submarket, the Tokyo office REIT market is segmented into Marunouchi and Otemachi, Shinjuku, Toranomon and Minato, Nihonbashi and Chuo, Shibuya and Minami-Aoyama, Osaki and Shinagawa, and decentralised business districts. Marunouchi and the Otemachi-Marunouchi-Yurakucho district remains the largest J-REIT submarket by acquisition value, dominated by Mitsubishi Estate Co., Ltd.'s development pipeline and the concentration of domestic and foreign financial institution headquarters. The Toranomon-Azabudai corridor is the fastest-growing submarket by rent and acquisition pricing, anchored by Mori Building's Azabudai Hills complex, which opened in 2023 and expanded in 2025, delivering ZEB-standard office, residential, and retail space that is setting a new Tokyo rent benchmark. The Nihonbashi redevelopment corridor, supported by the Tokyo Metropolitan Government's strategic urban area designation, is attracting J-REIT acquisition interest at sub-3.5% cap rates on newly delivered buildings, reflecting the market consensus that central Tokyo Grade A supply will remain structurally undersupplied through the end of the decade.

By Occupier Sector

Financial services and technology sector occupiers of Tokyo office assets held by J-REITs are expected to account for a significantly large revenue share in the Tokyo office REIT market during the forecast period.

Based on occupier sector, the Tokyo office REIT market is segmented into financial services, technology and digital, professional and business services, manufacturing headquarters, government and quasi-government, and life sciences and healthcare. Financial services firms including domestic banks, securities companies, and the Japan headquarters of global investment banks and asset managers anchor the largest lease commitments in Marunouchi, Shinjuku, and Toranomon Grade A buildings. Technology and digital sector occupiers are the fastest-growing segment, with Sony, Fujitsu, and multiple global technology firms consolidating into high-specification Grade A headquarters that incorporate collaborative workspaces, AI-enabled building management systems, and activity-based working designs that support hybrid team structures. The Government Pension Investment Fund of Japan's JPY 2.1 trillion real estate and infrastructure allocation, confirmed in its March 2025 annual report, makes Japanese public institutional investors a structural anchor of demand for J-REIT investment units and a stabilising force in the Tokyo office REIT capital markets cycle.

Submarket Deep-Dives

MARUNOUCHI / OTEMACHI LARGEST SUBMARKET BY ACQUISITION VALUE

| Key Landlord | Mitsubishi Estate Co., Ltd. | Anchor Tenants | Global banks, domestic financial institutions |

| J-REIT Exposure | Japan Real Estate Investment Corp., Nippon Building Fund | Sustainability Standard | LEED Platinum, CASBEE S |

Marunouchi and Otemachi is the largest and most liquid office submarket in Tokyo by J-REIT acquisition value, anchored by Mitsubishi Estate Co., Ltd.'s ownership of the majority of the district's Grade A stock and by the concentration of domestic and foreign financial institution headquarters that occupy the ground floors through upper floors of Marunouchi's landmark towers. Japan Real Estate Investment Corporation and Nippon Building Fund Inc. both hold Marunouchi-adjacent assets, benefiting from the submarket's deep tenant base of investment banks, securities firms, and professional services companies that sign long-term leases with annual rent escalation provisions. The Marunouchi Smart City project, backed by the Tokyo Metropolitan Government and Mitsubishi Estate, has delivered digital infrastructure including 5G coverage, shared mobility hubs, and open data platforms that position the district as Tokyo's most technologically advanced commercial precinct, supporting premium rent levels above the central Tokyo average.

TORANOMON / AZABUDAI FASTEST-GROWING RENT SUBMARKET

| Anchor Development | Azabudai Hills (Mori Building, 2023-2025) | Sustainability Standard | ZEB (Zero Energy Building) |

| J-REIT Exposure | Mori Hills REIT Investment Corp. | Rent Premium vs Market | 12-15% for ZEB-certified assets |

The Toranomon and Azabudai corridor is the fastest-growing office submarket in Tokyo by rent level, driven by Mori Building's Azabudai Hills complex that expanded in 2025 with AI-optimised facades, geothermal cooling, and biodiversity roofs achieving Zero Energy Building status per the Ministry of Land, Infrastructure, Transport and Tourism's green building certification framework. Mori Hills REIT Investment Corporation, which holds 11 properties totalling 182,655 square metres of leasable floor area as of July 31, 2025 per its investor relations disclosures, is the primary J-REIT vehicle for investors seeking exposure to the Roppongi-Toranomon-Azabudai premium corridor. Tenants in Azabudai Hills and adjacent Toranomon Hills towers are paying rents above the market average for CASBEE S-rank and ZEB-certified space, establishing a sustainability premium that is attracting corporate occupiers whose ESG commitments require certified workplace environments. The Toranomon Hills Business Tower, which forms part of the Mori Building-led Toranomon redevelopment cluster, remains nearly fully occupied with technology and financial services tenants at rents that exceed the Marunouchi average for comparable floor plates.

NIHONBASHI / CHUO REDEVELOPMENT INVESTMENT CORRIDOR

| Key Development | Nihonbashi Honcho M-SQUARE (Oct 2025) | J-REIT Acquisition Price | JPY 32.1 Billion (Nippon Building Fund, Jan 2026) |

| NOI Yield | 3.3% | Government Framework | Tokyo Metro Strategic Urban Area designation |

Nihonbashi and the Chuo Ward redevelopment corridor is emerging as Tokyo's most active new Grade A office investment district for J-REITs, anchored by the Tokyo Metropolitan Government's strategic urban area designation that provides floor area bonuses and height relaxation for mixed-use developments meeting sustainability and cultural preservation criteria. Nippon Building Fund Inc.'s acquisition of Nihonbashi Honcho M-SQUARE for approximately JPY 32.1 billion at a 3.3% NOI yield, announced on January 7, 2026 per the company's Tokyo Stock Exchange filing, represents the market pricing benchmark for newly delivered Grade A assets in the district and confirms that J-REIT managers accept sub-3.5% cap rates for assets in prime Tokyo locations with strong sustainability credentials. Mitsui Fudosan completed Japan's first nearly Zero Energy Building timber rental office building in Nihonbashi in March 2026 per the company's press release, establishing the corridor as the national benchmark for sustainable office development and attracting corporate occupiers whose green building procurement policies require ZEB or CASBEE S-rank certification.

SHINJUKU / SHIBUYA TECHNOLOGY AND MEDIA CORRIDOR

| Key Tenants | Technology, media, advertising, gaming firms | J-REIT Exposure | NBF, Japan Metropolitan Fund |

| Vacancy Trend | Tightening with tech demand | Rent Trend | Steady growth, below Marunouchi premium |

Shinjuku and Shibuya form Tokyo's technology and media office corridor, hosting the headquarters of Japan's largest technology and entertainment companies including Sony, Recruit, and multiple gaming, advertising, and digital media firms that require modern collaborative office space designed for activity-based working. The Shinjuku Mitsui Building No. 2 within Nippon Building Fund's portfolio is a core CBD asset in the submarket, representing the kind of large-format, well-located Grade A tower that J-REIT investors target for long-term income stability in Tokyo's second-largest office district. Shibuya's Scramble Square and adjacent redevelopment projects have attracted global technology firm Asian headquarters, creating a demand base for Grade A office space that supports rent growth at rates slightly below the Marunouchi benchmark but above the all-grade Tokyo average. The planned Shibuya Station South Exit redevelopment, supported by the Tokyo Metropolitan Government's station area development fund, will deliver additional Grade A supply in the late 2020s that J-REIT managers are monitoring for potential acquisition at a post-completion stabilisation stage.