| TROVIEW INTELLIGENCE | Sydney Agricultural Land and Farmland Market | Q2 2026 |

| TROVIEW INTELLIGENCE · CITY INTELLIGENCE REPORT |

By Zone · By Land Use · By Buyer Segment · By Valuation Driver

Zone Profiles: Hawkesbury and Richmond · Camden and Macarthur · Sydney Basin Horticulture · Central Coast · Penrith and Blue Mountains Fringe

Sydney's peri-urban agricultural land market is defined by the intersection of the world's most expensive urban property market encroaching on some of Australia's most productive market gardening, turf, and horticultural land at the urban fringe the Hawkesbury-Richmond flood plain accommodating approximately 40% of New South Wales market garden vegetable production, the Camden-Macarthur corridor housing one of Australia's most productive dairy and equine agribusiness precincts in proximity to 5.3 million metropolitan residents, NSW recording the highest statewide farmland price per hectare at AUD 9,815 in H1 2025 per Bendigo Bank Agribusiness, the Greater Sydney Commission's Western Parkland City vision creating urban expansion pressure that simultaneously elevates peri-urban farmland scarcity value and threatens the viability of farming operations on land zoned for future residential and employment use, and carbon farming, water trading, and agri-tourism emerging as supplementary income streams for Sydney Basin farmers whose proximity to urban populations creates both competitive pressures and unique value propositions that inland agricultural properties cannot replicate.

| Standard License: USD 2,200 | Enterprise License: USD 9,500 |

MARKET SYNOPSIS

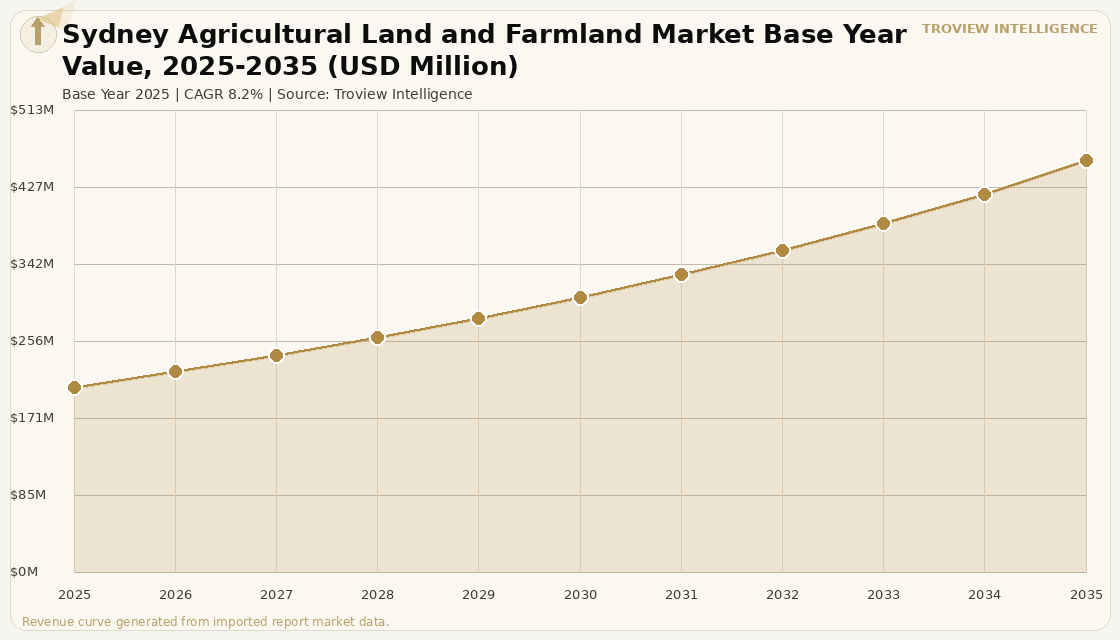

The Sydney agricultural land and farmland market size was USD 206.4 Million in 2025 and is expected to register a revenue CAGR of 8.2% during the forecast period, reaching USD 457.8 Million by 2035. The market encompasses peri-urban agricultural land across the Greater Sydney Basin including the Hawkesbury-Richmond flood plain, Camden-Macarthur corridor, Central Coast horticultural belt, Sydney Basin market garden and turf production zones, and the Penrith and Blue Mountains fringe agricultural holdings that together constitute the only large-scale productive agricultural land base within a major Australian metropolitan area, generating fresh produce supply, equine agribusiness, dairy production, turf and floriculture, and emerging carbon farming and agri-tourism revenue streams. Market revenue growth is anchored in the structural scarcity of peri-urban farmland within 80 kilometres of Australia's largest city, as urban expansion progressively converts former agricultural land to residential, commercial, and industrial uses while simultaneously elevating the capital value of remaining agricultural land through urban land value spillover that adds a development option premium to agricultural land valuations in the Greater Sydney Commission's Western Parkland City and North West growth precincts. NSW recorded the highest farmland price per hectare of any Australian state at AUD 9,815 per hectare in H1 2025 per Bendigo Bank Agribusiness 2025 Farmland Values Report, with the state's overall farmland prices rising 1.3% in H1 2025, confirming the resilience of NSW agricultural land values against the national correction that saw all other major states record declines. The Hawkesbury-Richmond flood plain accommodates approximately 40% of New South Wales market garden vegetable production per ABARES agricultural zone data, representing an irreplaceable peri-urban food production asset whose proximity to Sydney's 5.3 million population generates the fresh produce supply chain efficiency from field to Sydney market within hours that inland agricultural operations cannot replicate. For instance, the Camden area southwest of Sydney has been identified in multiple agricultural economics studies as housing one of Australia's highest-value peri-urban agricultural precincts, combining thoroughbred and standardbred equine agribusiness, intensive dairy production, premium market gardening, and heritage rural landscapes that generate the agri-tourism and rural residential amenity value that distinguishes peri-urban Sydney farmland from equivalent agricultural land at comparable distances from less affluent regional cities. These are some of the key factors driving revenue growth of the market.

The Greater Sydney Commission's Western Parkland City vision, encompassing the Western Sydney Airport precinct, the Aerotropolis employment and urban development zone, and the residential growth corridors extending from Penrith to Camden, creates the urban expansion dynamic that simultaneously elevates peri-urban farmland values through urban land price spillover and threatens the long-term viability of farming operations on land that is either already zoned for urban use or anticipated for future rezoning within the 30-year Metropolitan Strategic Plan horizon. Water entitlement values from the Sydney Basin and Hawkesbury-Nepean catchment system add a traded water asset component to irrigated horticultural land value in the Greater Sydney region, with Murray-Darling Basin water entitlement trading having established market prices for irrigation water that are now reflected in the total asset value of irrigated horticultural properties in the Hawkesbury-Richmond and Camden-Macarthur zones. Carbon farming and environmental plantings on peri-urban Sydney agricultural land are generating Australian Carbon Credit Units through the Emissions Reduction Fund, with the combination of carbon income, potential biodiversity credit registration, and agri-tourism revenue creating multi-income-stream farming models that generate above-agricultural-production returns from Sydney Basin farmland and attract non-farming institutional and private investors seeking portfolio diversification into agricultural real estate with income profiles that conventional grain or beef properties cannot offer. These are some of the key factors driving revenue growth of the market.

However, the Sydney agricultural land and farmland market faces structural constraints that temper the pace of agricultural productivity investment and long-term farmland value appreciation. Urban development pressure and the planning uncertainty associated with Western Parkland City, North West Growth Corridor, and South West Growth Corridor rezoning timelines creates a structural disincentive for multi-decade capital investment in agricultural improvement on land that may be rezoned for urban development before the investment has generated adequate agricultural return, resulting in underinvestment in irrigation infrastructure, soil improvement, and permanent plantings on farmland that is in the urban-rural land use transition zone. The Hawkesbury flood plain the most productive agricultural zone in Greater Sydney is subject to periodic flood events that damage crops, infrastructure, and soil structure at a frequency and scale that limits the insurance coverage and lending terms available to Hawkesbury farming operations, with the 2022 flood events having caused AUD hundreds of millions in agricultural losses across the Richmond-Windsor market garden precinct. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, affect Sydney Basin farmers through the fertiliser input cost transmission that increases the operating cost base of the intensive market gardening and horticultural operations that dominate peri-urban Sydney agricultural production, reducing the operating income available to support above-average land values at the urban fringe where land costs already compress farming margins relative to inland equivalent-productivity properties. These factors substantially limit Sydney agricultural land and farmland market growth over the forecast period.

Sydney's peri-urban farmland is the only agricultural land in Australia that is simultaneously a food production asset, a development option, a carbon farming platform, a water rights holding, and an agri-tourism business sitting within 90 minutes of 5 million consumers. The Hawkesbury flood plain market gardener who grows 40% of NSW's fresh vegetables is not competing with a grain farmer in Western Australia. They are competing with a Woolworths supply chain manager who wants fresh produce in a Sydney supermarket within four hours of harvest, and that competitive position is worth a location premium that does not exist anywhere else in Australian agriculture. The Camden dairy farmer is not a dairy farmer. They are operating an agribusiness in the most land-constrained premium market in Australia, on land that Stockland, Mirvac, or the NSW Land and Housing Corporation may be rezoning for residential development within 20 years. That optionality is priced into the land whether the farmer recognises it or not. Sydney peri-urban farmland is not valued on crop yields. It is valued on what the next highest-value use of the land is, and in Sydney, that is always urban development unless the land is permanently protected under an environmental or agricultural zone that removes the development option. Understanding which parcels are protected and which are not is the entire due diligence exercise for institutional peri-urban farmland investment in Greater Sydney." Troview Intelligence Head of Sydney Agricultural Land and Farmland Research

SEGMENT INSIGHTS

| 03 | ZONE ANALYSIS |

Five Zones Defining Sydney's Peri-Urban Agricultural Land Market

HAWKESBURY AND RICHMOND FLOOD PLAIN NSW'S MARKET GARDEN HEARTLAND ~40% OF NSW VEGETABLE PRODUCTION

| Production Share | Flood Risk | Land Use | Proximity |

| ~40% of NSW market garden vegetable production | 2022 floods AUD hundreds of millions agricultural damage | Intensive market gardening, floriculture, turf, citrus | ~60km from Sydney CBD same-day supply to Sydney markets |

The Hawkesbury-Richmond flood plain is the agricultural heartland of the Greater Sydney Basin, accommodating approximately 40% of New South Wales market garden vegetable production per ABARES agricultural zone data across a rich alluvial flood plain that has supported continuous intensive vegetable farming since the colonial period. The zone's proximity to Sydney's major wholesale and retail food distribution channels with produce reaching Sydney wholesale markets within 60 to 90 minutes of harvest compared to 12-plus hours for equivalent produce from the Riverina or Murray-Darling Basin generates the fresh produce supply chain premium that justifies above-inland land values for horticultural properties in the Hawkesbury-Richmond corridor. The zone faces a structural flood risk challenge from the Hawkesbury River system, with the March 2022 flood events causing major damage to vegetable crops, farm infrastructure, and soil structure across the Richmond and Windsor agricultural precincts, requiring soil rehabilitation and drainage investment that increases the operating cost base for Hawkesbury farmers while limiting the available lender and insurer appetite for agricultural finance in a flood-prone zone at Sydney land values. Despite the flood risk, the Hawkesbury-Richmond zone remains the Sydney Basin's most productive and highest-transaction agricultural land zone, as the alluvial soil fertility and irrigation water access from the Hawkesbury-Nepean river system are irreplaceable productive assets that cannot be relocated to flood-safe locations.

| Primary Uses | Urban Pressure | Key Feature | Valuation Driver |

| Thoroughbred / standardbred equine, dairy, market garden | Western Parkland City and South West Growth Corridor | Pastureland quality + proximity to racecourses/training | Urban development option premium alongside agricultural income |

The Camden-Macarthur corridor southwest of Sydney houses one of Australia's most productive and highest-value peri-urban agricultural precincts, combining thoroughbred and standardbred equine agribusiness anchored by proximity to Sydney's Thoroughbred Park at Menangle and the racing and training infrastructure of the Southern Highlands-Camden equine belt with intensive dairy production operations that supply the Greater Sydney fresh milk market, premium market gardening, and the rural lifestyle properties whose scenic pastureland and heritage rural character command residential premiums that complement agricultural income in the overall property valuation. The Greater Sydney Commission's Western Parkland City vision and South West Growth Corridor rezoning programme create the development option premium that elevates Camden-Macarthur agricultural land values above pure agricultural income capitalisation, as properties within the growth corridor planning envelope carry an embedded land bank value from future residential and employment land conversion that farmland in the Riverina or New England at equivalent soil quality productivity does not. Camden is one of Australia's fastest-growing Local Government Areas by residential population, with the urban expansion from Campbelltown and Narellan progressively converting former agricultural land to master-planned residential estates, raising the opportunity cost of continuing agricultural land use and elevating the value of remaining agricultural land that is either permanently protected in environmental or agricultural zones or is in the planning pipeline for future urban rezoning.

| Primary Uses | Solar Opportunity | Urban Encroachment | Key Characteristic |

| Market gardening, turf, floriculture | Flat topography + grid proximity agrivoltaic trials | North West and Western Sydney growth precincts | Small land parcels, high intensity production per hectare |

The Sydney Basin horticulture zone across the Western Sydney plains including St Marys, Llandilo, Berkshire Park, and the agricultural precincts of the Hawkesbury-Nepean corridor hosts the highest-intensity fresh produce, turf, and floriculture production in the Greater Sydney Basin, with agricultural operations typically producing multiple crop cycles annually from relatively small land parcels that generate per-hectare agricultural income that exceeds comparable-size rural properties through intensive production methods. The relatively flat topography of the Western Sydney plains and proximity to the Western Sydney electricity transmission network make peri-urban Sydney agricultural land increasingly attractive for utility-scale solar farm co-location, with agrivoltaic farming models that install solar panels above-ground at heights that allow continued vegetable or turf production beneath the solar array generating both renewable energy lease income and continued agricultural production from the same land area. The North West Growth Corridor's planned residential expansion from Rouse Hill toward Riverstone and Box Hill creates progressive urban land use conversion pressure on the northern fringe of the Western Sydney agricultural precinct, elevating residual agricultural land values through scarcity as zoned residential development absorbs the northern portions of the zone's agricultural land base.

| Distance from Sydney CBD | Primary Uses | Buyer Profile | Growth Driver |

| ~90 to 100km (1hr via M1 Pacific Motorway) | Blueberry, turf, small crops, equine, lifestyle rural | Sea-change and lifestyle buyers from Sydney + local farmers | Hybrid lifestyle-agricultural property market |

The Central Coast agricultural corridor north of Sydney including the Gosford, Wyong, and Mangrove Mountain horticulture and small farm precincts provides the outer boundary of the Greater Sydney Basin agricultural land market, where properties transition from intensive peri-urban market gardening toward the lifestyle-agriculture hybrid model that characterises the transitional zone between metropolitan Sydney and the Hunter Valley's established wine, thoroughbred, and mixed farming economy. The Central Coast's proximity to Sydney approximately 90 to 100 kilometres and one hour via the M1 Pacific Motorway generates the sea-change and lifestyle buyer demand that creates a residential premium component in agricultural land valuations across the zone, with rural residential properties offering acreage, privacy, and the aspiration of small-scale productive farming within commuting or occasional trip distance of Sydney CBD. Blueberry, turf, and small-crop horticulture operations on Central Coast agricultural land generate fresh produce revenue that supplements the lifestyle residential premium, creating the total return profile that attracts buyers who are not primarily agricultural operators but who value the farming income as a contribution to the overall property's investment economics.

| Urban Driver | Carbon Farming | Agri-Tourism | Land Value Driver |

| Western Sydney International Airport Aerotropolis | Blue Mountains fringe land ACCU eligible | Lavender farms, farm stays, food tourism | Development option from Aerotropolis precinct expansion |

The Penrith and Blue Mountains fringe agricultural zone is being transformed by the Western Sydney International Airport at Badgerys Creek and the surrounding Aerotropolis employment and urban development precinct, with the airport's planned opening having elevated peri-urban agricultural land values in the Penrith, Bringelly, and Luddenham corridors through the combination of development land option value from Aerotropolis precinct expansion and the improved transport connectivity that the airport infrastructure brings to the western Sydney agricultural zone. Carbon farming on Blue Mountains fringe agricultural and peri-agricultural land where native vegetation regeneration, environmental plantings, and savanna burning management on properties at the rural-conservation interface can generate Australian Carbon Credit Units through the Emissions Reduction Fund is emerging as a supplementary income stream for landholders in the Penrith and Blue Mountains western fringe whose land may be suitable for carbon project registration alongside residual agricultural or grazing use. Agri-tourism and farm-to-table hospitality on Blue Mountains fringe properties including lavender farms, strawberry picking operations, boutique vineyard estates, and farm stay accommodation generates visitor economy revenue from Sydney's recreational travel market that adds an income diversification layer to agricultural landholdings whose proximity to the Blue Mountains National Park tourism corridor positions them for visitor-facing agricultural business models that purely inland properties cannot access.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from ABARES official data, Greater Sydney Commission planning documents, Bendigo Bank Agribusiness reports, and verified trade press.