By District · By Format · By Operator · By Consumer Profile

Tokyo ranked 4th in the 2026 World's Best Cities Report as the Japan Commercial Real Estate Price Index for retail assets rose 2.9% in Q3 2025, Gaw Capital acquired Tokyu Plaza Ginza for its 50,093 square metre four-sided Ginza block frontage citing the Tokyo Sky Corridor High Line as a 2029 value catalyst, and teamLab Borderless at Azabudai Hills and teamLab Planets in Toyosu together attract a visitor base disproportionately drawn from the United States, Australia, Canada, and the United Kingdom confirming that Tokyo's experiential retail real estate is earning its position as the global benchmark format.

MARKET SYNOPSIS

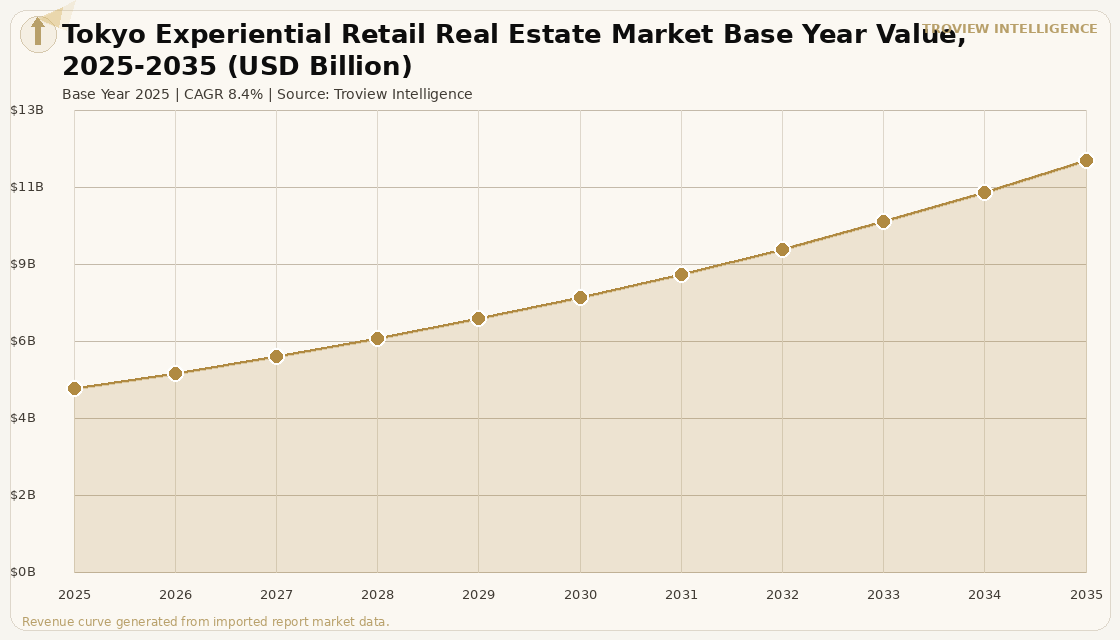

The Tokyo experiential retail real estate market size was USD 5.12 Billion in 2025 and is expected to register a revenue CAGR of 8.4% during the forecast period, reaching USD 11.47 Billion by 2035. Tokyo is the world's most advanced experiential retail real estate city, combining the globally recognised teamLab digital art ecosystem, the depachika food hall tradition that Isetan, Mitsukoshi, and Takashimaya have elevated to cultural institution status, and a concentration of luxury brand flagship concept stores in Ginza and Omotesando that defines the global standard for brand experience architecture. Tokyo ranked 4th in the 2026 World's Best Cities Report, with the city's commercial real estate market recording seven consecutive periods of land value appreciation across all major districts per Japan real estate market analysis. The Japan Commercial Real Estate Price Index for retail assets rose 2.9% in Q3 2025 per the Japan Ministry of Land, Infrastructure, Transport and Tourism composite data, outperforming every other commercial asset class and confirming that experiential and destination retail is among the strongest-performing segments in Tokyo's current investment cycle.

Tokyo's experiential retail real estate market is sustained by three structural demand drivers that operate simultaneously: inbound tourism at over 30 million annual visitors to Japan in 2025 per Japan National Tourism Organization data, with Tokyo capturing the largest share; the domestic consumer's deeply embedded gift-giving culture that generates repeat depachika visits across social occasions including Valentine's Day, White Day, Obon, and end-of-year gift-giving season; and global luxury brand investment in flagship concept stores across Ginza and Omotesando where brands treat physical retail as a media and experience channel rather than a transaction point. Large urban commercial facilities including Azabudai Hills, GINZA SIX, and Shibuya Scramble Square experienced strong leasing demand from domestic and international brands in 2025 with tight vacancies per Japan real estate market analysis. The Tokyo Sky Corridor, a planned conversion of the Shuto Expressway KK Line into a 4.8-kilometre elevated pedestrian park from Nihonbashi to Shiodome, is expected to partially open in 2029 and will enhance the value of Ginza commercial real estate along its route. For instance, in February 2025, Gaw Capital Partners and Patience Capital Group completed the acquisition of Tokyu Plaza Ginza, a 50,093 square metre retail facility spanning an entire block in Ginza with four-sided frontage and direct access to Ginza Station, with Gaw Capital holding a 91% stake and citing the Tokyo Sky Corridor as a forward value catalyst, per Gaw Capital Partners press release of February 2025. These are some of the key factors driving revenue growth of the market.

However, the Tokyo experiential retail real estate market faces structural constraints. Tax-free retail spending, which surged 231.2% year-on-year in 2024, softened 12.7% in 2025 and May 2025 recorded a 41% decline across more than 80 stores per Japan department store industry data, as the yen stabilised somewhat from its weakest levels and inbound tourism spending normalised after the post-pandemic surge. Premium immersive experience activations in Tokyo venues carry costs 20 to 30% above comparable activations in other Asian markets due to labour costs, quality standards, and real estate, with major named-artist installations starting at JPY 80 million to JPY 300 million and full floor experiential renovations at JPY 300 million or above per industry cost estimates, creating capital allocation challenges for department store operators managing multiple experiential programming cycles simultaneously. Tokyo's central commercial districts face constrained development land supply, with new experiential retail real estate delivered primarily through large mixed-use redevelopment projects rather than incremental expansion, limiting the pace of new supply. These factors substantially limit Tokyo experiential retail real estate market growth over the forecast period.

Tokyo has three things that no other city can fully replicate: the depachika, teamLab, and Ginza. The depachika is sixty years of commercial iteration by the world's most demanding food consumers. teamLab is the only company that has made immersive digital art commercially self-sustaining at venue scale globally. Ginza is the street where LVMH, Cartier, and Grand Seiko open their third flagship in the same three blocks. When Gaw Capital pays institutional real estate money for Tokyu Plaza Ginza and cites the Tokyo High Line as a future value driver, they are betting on a city that continues to generate the highest density of world-class experiential retail formats per commercial district of anywhere in the world. The tax-free spend softening in 2025 is a one-year data point against a sixty-year structural trend." Troview Intelligence Head of Tokyo Experiential Retail Research

SEGMENT INSIGHTS

By District

Ginza and Omotesando are expected to account for a significantly large revenue share in the Tokyo experiential retail real estate market during the forecast period.

Based on district, the Tokyo experiential retail real estate market is segmented into Ginza, Omotesando-Harajuku, Shibuya, Shinjuku, Azabudai Hills-Roppongi, and Toyosu-Odaiba. Ginza dominates by per-square-metre revenue and institutional transaction volume, with GINZA SIX, Tokyu Plaza Ginza, and Ginza Sony Park representing three distinct models of experiential retail real estate curated luxury vertical mall, iconic block-frontage multi-tenant centre, and brand-owned experiential public space. Omotesando serves the street-level luxury flagship brand experience market, where brands including Hermes, Louis Vuitton, Prada, and Dior operate architecturally iconic standalone buildings that function as brand museums with retail attached. Shibuya is the fastest-growing district by new experiential retail completions, with Shibuya Scramble Square, Shibuya Sakura Stage, and Miyashita Park collectively delivering a new generation of mixed-use experiential retail alongside Shibuya Crossing, the world's most photographed street intersection.

By Format

Department store experiential floors and premium immersive art venues are expected to account for a significantly large revenue share in the Tokyo experiential retail real estate market during the forecast period.

Based on format, the Tokyo experiential retail real estate market is segmented into department store depachika and experiential programming floors, standalone immersive digital art venues, luxury brand flagship concept stores, curated food market and dining destinations, and pop-up and seasonal activation spaces. Department stores with premium depachika and experiential event programming Isetan Shinjuku at JPY 421 billion annual sales, Mitsukoshi Ginza, Takashimaya Nihonbashi dominate market revenue by format. Standalone immersive digital art venues teamLab Borderless at Azabudai Hills spanning approximately 9,300 square metres and teamLab Planets in Toyosu are the fastest-growing format by visitor growth and international visitor share. Luxury brand flagship concept stores in Ginza and Omotesando represent the most concentrated per-square-metre rent market, with brands accepting premium lease costs in exchange for the locational prestige and visitor demographics that these districts deliver.

By Consumer Profile

International tourist visitors and high-income domestic consumers generate a significantly large revenue share in the Tokyo experiential retail real estate market during the forecast period.

Based on consumer profile, the Tokyo experiential retail real estate market is served by international tourists from the United States, Australia, China, South Korea, and Europe who specifically select Tokyo for its experiential retail distinctiveness; high-income domestic shoppers who use department stores and luxury flagships for regular gift-giving and personal luxury purchases embedded in Japan's social calendar; and youth and trend consumers in Harajuku and Shibuya who drive fashion and pop culture brand activation demand. teamLab venues attract a disproportionately US, Australian, Canadian, and British visitor base compared to Tokyo's overall inbound tourist profile per teamLab official ticket data covering 2025, confirming that immersive art experiences draw independently motivated visitors rather than simply capturing the general tourist flow. Konbini like FamilyMart have expanded into IP-centred experiential experiments, transforming convenience stores into entertainment hubs with character-themed limited-edition merchandise and in-store event activations, extending experiential retail formats down to the convenience store level.

DISTRICT DEEP-DIVES

Tokyo's Key Experiential Retail Districts

| Tokyu Plaza Ginza | 50,093 m², acquired by Gaw Capital Feb 2025, 4-sided block frontage | GINZA SIX | 46,000 m² GFA, luxury brand cluster, gallery, food hall |

| Ginza Sony Park | Branded public space: interactive, experiential, seasonal programming | Tokyo Sky Corridor 2029 | Adjacent elevated High Line will enhance Ginza retail value |

Ginza is Tokyo's primary luxury experiential retail district and one of the most commercially productive retail streets in the world by per-square-metre tenant sales productivity. Three distinct experiential formats coexist within a single square kilometre: GINZA SIX as the curated luxury vertical mall with gallery programming and a premium depachika; Tokyu Plaza Ginza as the large-format multi-brand centre that Gaw Capital acquired in February 2025 for its rare block-frontage position and future Tokyo Sky Corridor uplift; and Ginza Sony Park as a wholly brand-owned experiential public space that Sony uses for interactive product demonstrations, seasonal installations, and experimental events. Grand Seiko opened its third Ginza flagship, confirming that the district absorbs multiple flagship investments from single luxury brands at a density not achievable anywhere else in Japan. The pending Tokyo Sky Corridor, converting the elevated KK Line expressway into a pedestrian park partially opening in 2029, will fundamentally transform Ginza's street-level connectivity between Nihonbashi and Shiodome.

OMOTESANDO / HARAJUKU BRAND FLAGSHIP AND YOUTH CULTURE

| Flagship Brand Formats | Hermes, Louis Vuitton, Prada, Dior: architecturally iconic brand museums | Tokyu Plaza Omotesando Harajuku | Pop-up and concept store host, OH MY Cafe activations |

| Harajuku Energy | Youth culture, Jordan World of Flight, Diesel concept, Ambush Workshop | Azabudai Hills Proximity | Adjacent mixed-use development with teamLab Borderless anchor |

Omotesando and Harajuku serve two distinct but adjacent experiential retail functions within the same corridor: the tree-lined main street of Omotesando hosts the world's highest concentration of architecturally significant luxury brand flagship buildings, while Harajuku's Cat Street and Takeshita-dori serve as the global capital of youth fashion experiential retail. On Omotesando, brands including Hermes, Louis Vuitton, Prada, and Dior operate buildings designed by globally recognised architects that function primarily as brand experience destinations. Tokyu Plaza Omotesando Harajuku hosts OH MY Cafe and rotating pop-up experiential concepts, with Miyashita Park serving as a dedicated pop-up and art activation space for youth-oriented brands. Jordan's World of Flight flagship, Diesel's concept store, and Ambush Workshop represent the brand activation formats that Harajuku generates as a testing ground for global youth culture retail concepts before they scale to other markets.

| Shibuya Scramble Square | Global brand flagships, tech companies, creative industry tenants | Miyashita Park | Pop-up spaces for retail and art above Shibuya Station |

| Shibuya Crossing | Most photographed street intersection globally; amplifies visitor draw | New Completions | Shibuya Sakura Stage (2023), Scramble Square Phase 2 pipeline |

Shibuya is Tokyo's fastest-growing experiential retail real estate district, with Shibuya Scramble Square, Shibuya Sakura Stage, and the reimagined Tokyu Department Store Shibuya collectively delivering new mixed-use experiential retail capacity above Shibuya Station. Shibuya Crossing, the world's most photographed street intersection, ensures that Shibuya captures a disproportionate share of Tokyo's international tourist footfall, generating visit occasions that spill into the surrounding retail and dining ecosystem. The Tokyoesque analysis of pop-up culture in Japan identifies Miyashita Park above Shibuya Station as one of the city's primary locations for retail and art-combined pop-up spaces, hosting brand activations that bridge the seasonal calendar events embedded in Japanese consumer culture Halloween, Cherry Blossom, Valentine's Day, White Day with international brand storytelling. The concentration of youth-oriented fashion and technology brands in Shibuya confirms the district's role as Tokyo's laboratory for global youth culture experiential retail formats.

| teamLab Borderless | ~9,300 m², Azabudai Hills basement, Feb 2024 opening | teamLab Planets Toyosu | Expanded Jan 2025, 1.5x previous size, 20+ new artworks |

| Azabudai Hills Market | 30+ gourmet vendors in integrated food market | Luxury Tenants | Hermes, Cartier, Dior, Celine at Azabudai Hills (2024) |

Azabudai Hills and the adjacent Roppongi-Toyosu corridor house Tokyo's two most globally recognised immersive art venues, teamLab Borderless at Azabudai Hills and teamLab Planets TOKYO in Toyosu, which together attract a visitor base with an internationally disproportionate profile per teamLab official data covering 2025, drawing heavily from the United States, Australia, Canada, and the United Kingdom. teamLab Borderless occupies approximately 9,300 square metres in the basement of Azabudai Hills, Mori Building's newest and most ambitious mixed-use development, which also houses luxury brands including Hermes, Cartier, Dior, and Celine that opened in 2024 alongside the Azabudai Hills Market with 30 or more gourmet vendors. teamLab Planets expanded in January 2025 to 1.5 times its previous size, adding three new educational project areas and over 20 new artworks, sustaining its position as one of the most visited experiential attractions in Japan for international visitors who make it a primary purpose of their Tokyo visit.