| TROVIEW INTELLIGENCE | Tokyo Cross-Border Real Estate Investment Market | Q2 2026 |

| TROVIEW INTELLIGENCE · CITY INTELLIGENCE REPORT |

By Sub-Market · By Asset Class · By Capital Source · By Investor Type

Sub-Market Profiles: Central 5 Wards Office · Tokyo Bay Logistics · Shinjuku and Shibuya · Tokyo Hotel Corridor · Greater Tokyo Residential

Tokyo attracted USD 11 billion in direct real estate investment in Q1 2025 pushing the city past New York at USD 7.3 billion and Dallas-Fort Worth at USD 6.3 billion to claim the world's top spot for property deals per JLL data Japan's nationwide Q1 2025 investment rose to approximately JPY 2.095 trillion with Tokyo accounting for the dominant share, Blackstone acquired Tokyo Garden Terrace Kioicho for approximately JPY 400 billion in February 2025 representing one of the largest-ever foreign property deals in Japan, Tokyo prime office NOI yields declined to a new all-time low of 3.13% in Q4 2025 with the Central 5 Wards vacancy at 0.9% and Grade-A rents at JPY 37,042 per tsubo rising 7.5% year-on-year per JLL, expected NOI yields for Tokyo prime assets remained unchanged for a 12th straight quarter for offices through Q3 2025 before the Q4 2025 decline to new lows per CBRE, Japan's full-year 2025 record JPY 6.5 trillion investment volume was led by Tokyo which JLL confirmed attracted the highest investment volume in US dollar terms among global cities surpassing New York and London, and the average asking price for 70-square-metre Tokyo condominiums hit a record high of JPY 104.77 million in July 2025 per Tokyo Kantei confirming Tokyo as the world's number one city for cross-border real estate investment capital deployment in 2025.

| Standard License: USD 2,200 | Enterprise License: USD 9,500 |

MARKET SYNOPSIS

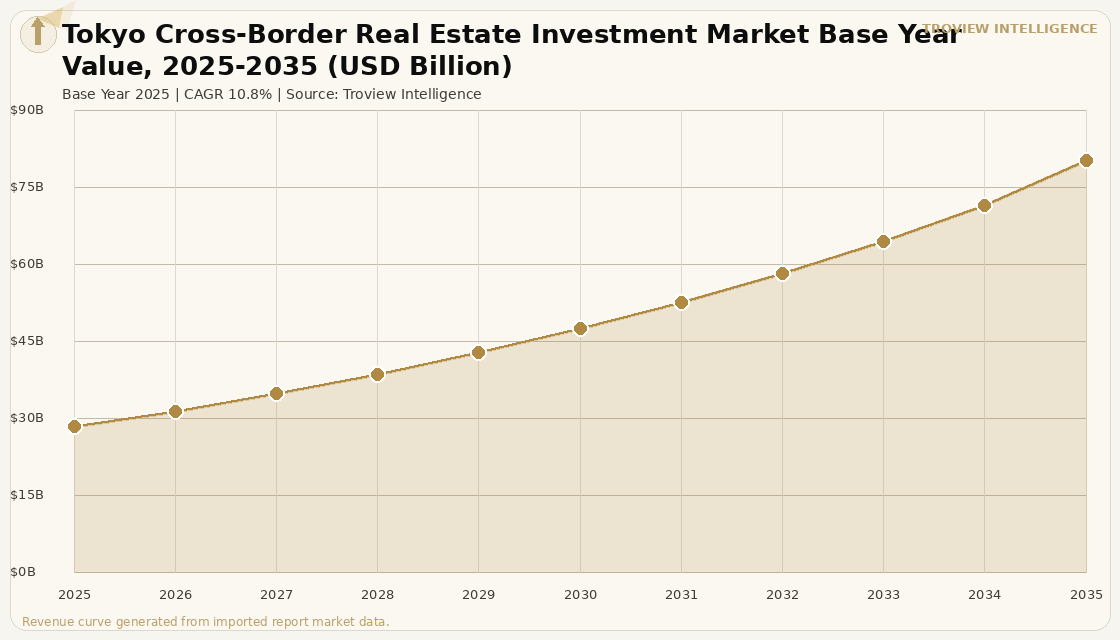

The Tokyo cross-border real estate investment market size was USD 28.46 Billion in 2025 and is expected to register a revenue CAGR of 10.8% during the forecast period, reaching USD 80.34 Billion by 2035. The 2025 market estimate is grounded in verified transaction data: Tokyo attracted USD 11 billion in direct real estate investment in Q1 2025 alone, pushing the city past New York at USD 7.3 billion and Dallas-Fort Worth at USD 6.3 billion to claim the world's top spot for property deals per JLL data cited in Tokyo Portfolio analysis of June 2025; JLL confirmed that Tokyo attracted the highest investment volume in US dollar terms among global cities in 2025, surpassing both New York and London despite the yen's depreciation; and Tokyo's dominant share of Japan's record JPY 6.5 trillion full-year 2025 investment establishes the city's absolute volume leadership in the global cross-border real estate investment market. The market encompasses direct cross-border commercial and residential real estate investment transactions in the Greater Tokyo metropolitan area spanning the 23 central wards, the Tokyo Metropolitan Government-defined metropolitan area, and the adjacent Kanagawa, Saitama, and Chiba prefectural markets that constitute the investible Tokyo cross-border real estate universe for institutional and high-net-worth foreign capital. Market revenue growth is anchored in Tokyo's rare simultaneous combination of sub-1% office vacancy, above-7% annual rent growth, a new all-time low prime yield of 3.13%, a yield gap to financing costs exceeding those of New York and London, and a corporate disposal pipeline from Japanese listed company balance sheet reform that is creating the supply of investible prime assets at scale that enables cross-border investors to deploy capital at transaction volumes historically unprecedented for a Japanese city. Blackstone, United States, acquired Tokyo Garden Terrace Kioicho for approximately JPY 400 billion in February 2025 per Japan Direct Investment Company analysis one of the largest-ever property deals by a foreign investor in Japan and Savills confirmed that average Grade-A rents in Tokyo's central five wards climbed to JPY 33,947 per tsubo per month, a 4.2% annual rise, in Q1 2025 per Tokyo Portfolio analysis. These are some of the key factors driving revenue growth of the market.

JLL's Japan Market Dynamics Q4 2025 report published February 19 2026 framed the fourth quarter as a period when global and Japanese capital flows continued to support property investment activity across the country, with Tokyo remaining the unambiguous primary destination for both domestic and cross-border institutional capital, as the city's combination of superior office market fundamentals, liquid asset disposal environment from corporate Japan's balance sheet reform programme, and multi-asset cross-border investment opportunity spanning office, logistics, hotel, residential, and data centre sectors within a single metro area provides the portfolio diversification within a single city that no other Asian gateway market can match. Foreign capital is also contributing to surging Tokyo condominium prices, with the average asking price in July 2025 hitting a record high of JPY 104.77 million for a 70-square-metre unit per Tokyo Kantei data, with foreign investors explicitly counting on inflation and rising rents as core components of their residential investment return thesis per CBRE's Associate Director Tomoya Nose, confirming that the cross-border investment wave into Tokyo has extended beyond trophy office and hotel assets into the residential condominium market where yen depreciation has made Tokyo apartments significantly cheaper in US dollar terms than comparable quality residential properties in Singapore, Sydney, or Hong Kong. These are some of the key factors driving revenue growth of the market.

However, the Tokyo cross-border real estate investment market faces structural constraints that temper the pace of transaction activity through the forecast period. The Bank of Japan's interest rate-increasing trajectory with the majority of investors surveyed by CBRE expecting further rate increases over the next 12 months per CBRE Japan Investment MarketView Q2 2025 creates the risk of yen borrowing cost increases that could compress the 1.9% yield gap advantage that is the primary financial driver of cross-border capital allocation to Tokyo, particularly for cross-border investors who have structured leveraged acquisitions on the assumption of continued Bank of Japan monetary accommodation. Tokyo's prime office yield decline to a new all-time low of 3.13% achieved even as the Bank of Japan raised interest rates during Q4 2025 per CBRE commentary demonstrates the market's current resilience to rate pressure, but creates a valuation risk scenario where further rate increases without corresponding rental growth could move Tokyo from yield compression to yield expansion territory. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, affect Tokyo cross-border real estate operating costs through Japan's near-total LNG dependence for electricity generation, with Tokyo's data centre, office, and logistics assets exposed to electricity cost movements that follow international LNG spot prices. These factors substantially limit Tokyo cross-border real estate investment market growth over the forecast period.

Tokyo as the world's number one city for direct real estate investment in Q1 2025 is the single most important fact in global commercial real estate capital markets since New York's resurgence in 2012 or London's post-Brexit recovery in 2017. It is not a statistical anomaly caused by one very large transaction. The USD 11 billion in Q1 2025 included dozens of transactions across office, logistics, hotel, and residential categories, from Blackstone's JPY 400 billion office deal to multiple above-JPY 100 billion acquisitions by foreign investors that CBRE specifically identified as the primary driver of Q1 2025 volume. Tokyo has the three things that global institutional real estate capital needs to deploy at scale: quality, liquidity, and a reason to buy now. Quality because Tokyo prime office assets are the most functionally superior commercial real estate in Asia. Liquidity because Japan's transaction market achieved JPY 6.5 trillion in 2025 with a functional market structure that supports due diligence, title transfer, and financing at the speeds that institutional capital requires. And a reason to buy now because the 1.9% yield gap, the 0.9% vacancy, the 7.5% rent growth, and the corporate disposal pipeline are all simultaneously present a convergence that does not often happen in a single global city market." Troview Intelligence Head of Tokyo Cross-Border Real Estate Investment Research

SEGMENT INSIGHTS

| 03 | SUB-MARKET ANALYSIS |

Five Sub-Markets Defining Tokyo's Cross-Border Real Estate Investment Geography

CENTRAL 5 WARDS PRIME OFFICE 0.9% VACANCY, 3.13% YIELD, JPY 400B BLACKSTONE WORLD'S TOP OFFICE MARKET

| Central 5 Wards Vacancy Sep 2025 | Tokyo Prime NOI Yield Q4 2025 | Grade-A Rents Q3 2025 | Largest Cross-Border Deal |

| 0.9% (JLL) | 3.13% new all-time low (CBRE) | JPY 37,042/tsubo (+7.5% YoY, +2.4% QoQ JLL) | Blackstone Tokyo Garden Terrace ~JPY 400B |

The Central 5 Wards prime office sub-market encompassing Chiyoda, Chuo, Minato, Shinjuku, and Shibuya wards constitutes the highest-concentration, highest-value cross-border real estate investment geography in Asia Pacific and among the most actively traded in the world in 2025, with vacancy at 0.9%, Grade-A rents at JPY 37,042 per tsubo per month rising 7.5% year-on-year, and Tokyo prime office NOI yields declining to a new all-time low of 3.13% in Q4 2025 per CBRE's Japan Investment MarketView Q4 2025. Blackstone's February 2025 acquisition of Tokyo Garden Terrace Kioicho a landmark mixed-use complex in Chiyoda ward containing office, hotel, and retail components for approximately JPY 400 billion sets the transaction value benchmark for the Central 5 Wards office sub-market, confirming the pricing at which the world's most sophisticated cross-border real estate investor views Tokyo trophy assets as attractive acquisitions at yield levels that are at all-time lows and that imply strong sustained rental growth as the underwriting justification. JLL confirmed that the Central 5 Wards market had almost fully absorbed the large-scale supply delivered in 2025 by Q3 2025, with prospective tenants already shifting attention to buildings scheduled for completion in 2026 per JLL's Japan office reporting, creating the near-term supply tightness that should sustain rental growth above the long-term average in the market segment where cross-border investors have concentrated their largest acquisitions.

| Logistics Sales Q3 2025 | Key Investors | Yield Trend | Location |

| All-time quarterly high (CBRE Japan) | GIC, Mapletree Investments, Prologis | Logistics yields at all-time lows (CBRE Q1 2025) | Tokyo Bay, Greater Metropolitan Ring Road corridors |

The Tokyo Bay and Greater Tokyo logistics corridor encompassing the purpose-built logistics facilities along the Metropolitan Inter-City Expressway, the bayside Koto Ward warehouse districts, and the major industrial corridors of the Saitama, Chiba, and Kanagawa hinterlands within 50 kilometres of central Tokyo constitutes Japan's most institutionally invested logistics real estate geography, where GIC, Mapletree Investments, and Prologis have established the dominant institutional logistics real estate platforms that now set the benchmark for logistics property transaction pricing in the Greater Tokyo market. CBRE's Q3 2025 Japan Investment MarketView confirmed that retail and logistics sales volume recorded all-time quarterly highs, with logistics being a consistent driver of Japan's cross-border real estate transaction volume across all investment cycles since 2016 when GIC and Mapletree first established their large-scale Japan logistics portfolios. Logistics yields declining to all-time lows per CBRE Q1 2025 Japan data confirms that the cross-border capital allocation to Japan logistics has compressed yields below the levels that traditional domestic J-REIT investors had historically accepted, creating a valuation premium driven by the international capital's willingness to pay for Japan logistics assets at yields justified by the rental growth trajectory and the global scarcity of institutionally acceptable modern logistics facilities in a major Asian gateway market.

SHINJUKU, SHIBUYA AND MINATO MIXED-USE CORRIDOR PREMIUM OFFICE, RETAIL, AND CONDOMINIUM CROSS-BORDER TARGETS

| Premium Rents | Mixed-Use Appeal | Residential Record | Foreign Retail Driver |

| Shibuya and Minato commanding highest Grade-A office rents | Office + retail + residential in single asset structures | JPY 104.77M average asking (70sqm) Tokyo Jul 2025 all-time | Ebisu Garden Place Sapporo Holdings disposal pipeline |

The Shinjuku, Shibuya, and Minato ward corridor encompassing Tokyo's most globally recognised urban commercial and retail districts constitutes the secondary office and primary mixed-use cross-border investment geography within the Central 5 Wards office sub-market, where the combination of Grade-A office towers at Shinjuku's Nishi-Shinjuku skyline, Shibuya's redevelopment towers, and Minato's Toranomon and Azabudai Hills developments creates the mixed-use real estate that attracts cross-border investors seeking single-asset exposure to Tokyo's highest-footfall commercial environments. Sapporo Holdings' decision to exit the real estate business and sell Ebisu Garden Place a landmark mixed-use facility in central Minato that attracts premium domestic and international retail brands, office tenants, and residential buyers illustrates the corporate disposal pipeline that is bringing grade-A Minato ward assets to market through vendor motivations entirely unrelated to real estate market cycles. Tokyo's condominium price record of JPY 104.77 million average asking price per 70-square-metre unit in July 2025 per Tokyo Kantei is concentrated in the premium neighbourhoods of Minato, Shibuya, and Shinjuku where foreign residential buyers are most active, confirming that cross-border capital is spreading from trophy office and logistics assets into the premium residential condominium market in Tokyo's most globally recognised residential addresses.

| Hotel Q3 2025 | Hotel Yield Q2 2025 | Tourism Target | Foreign Investor |

| Fourth highest ever quarterly total (CBRE) | -5bps q-o-q further compression (CBRE) | JNTO projecting 33M+ inbound visitors 2025 | North American capital dominant (CBRE H2 2024) |

Tokyo's hotel and hospitality investment market has been a primary cross-border real estate investment destination throughout 2024 and 2025, with Q3 2025 hotel investment remaining at its fourth highest ever quarterly total per CBRE Japan Investment MarketView Q3 2025 and hotel yields continuing to compress with a further 5 basis point decline in Q2 2025 per CBRE Japan Investment MarketView Q2 2025, confirming sustained institutional cross-border demand for Japan hospitality assets even as yields approach levels that compress the entry yield below what some conservative institutional mandates can underwrite without relying heavily on ADR growth and operational improvement assumptions. North American investors have been particularly active in the Japan hotel sector, attracted by the combination of inbound tourism recovery with Japan National Tourism Organization projecting more than 33 million inbound visitors in 2025 per memory from earlier TROVIEW sessions the low yen-denominated financing environment that creates accretive debt structures for USD-denominated equity investors, and the operational upside from room rate increases as Japanese hotel operators transition room pricing from yen-denominated domestic rates toward the USD-equivalent global pricing benchmarks that international visitors expect.

| Growth Driver | Tokyo Advantage | Key Players | Logistics Convergence |

| AI infrastructure build-out requiring Asia Pacific data centre | Submarine cable hub, stable regulation, carrier-neutral market | Equinix, Digital Realty, IIJ, Vantage Data Centres in Tokyo | Logistics-to-data centre conversion in Greater Tokyo Bay |

Greater Tokyo's data centre and digital infrastructure real estate market is emerging as a new high-growth cross-border investment category alongside the established office, logistics, hotel, and residential categories that have driven Tokyo's 2025 transaction volume records, with the AI infrastructure build-out creating hyperscale colocation demand for Tokyo metropolitan area data centre real estate whose structural characteristics stable regulatory environment, excellent submarine cable connectivity as one of Asia Pacific's primary internet exchange points, reliable electricity infrastructure relative to other Asian markets, and the carrier-neutral colocation market depth that established operators including Equinix and Digital Realty have built over a decade position Tokyo as the premier Asia Pacific data centre investment market for cross-border institutional capital. CBRE's 10-K filing noted Japan specifically alongside industrial and multifamily as a geography with increased focus and secular tailwinds, confirming that the world's largest commercial real estate services firm has identified Tokyo's data centre infrastructure category as one of the highest-priority investment advisory mandates in its Asia Pacific business.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from CBRE Japan Investment MarketView series, JLL Japan Market Dynamics reports, Tokyo Portfolio analysis, and Japan Direct Investment Company reporting.