| TROVIEW INTELLIGENCE | Agricultural Land and Farmland Market | Q2 2026 |

| TROVIEW INTELLIGENCE · GLOBAL INTELLIGENCE REPORT |

By Geography · By Land Type · By Investor Class · By Crop System

US national cropland values reached USD 5,830 per acre in August 2025, up 4.7% over 2024 per USDA National Agricultural Statistics Service Land Values 2025 Summary, with US pastureland values rising 5.2% in 2024 per USDA, the Federal Reserve Bank of Kansas City Q2 2025 agricultural finance report confirming that despite headwinds in farm income and credit conditions land values have shown remarkable resilience across the American Midwest, global farmland prices recording an 11% compound annual growth rate over 2002 to 2021 per Savills analysis cited in peer-reviewed research, Nuveen Natural Capital operating as the global leader in farmland investment with more than 39 years of experience spanning 11 geographies and 60-plus crop types, Farmland Partners Inc. selling USD 289 million worth of US farmland to Farmland Reserve in 2024 as one of the year's most notable transactions, and ABARES forecasting Australia's combined agriculture, fisheries, and forestry sectors to reach AUD 94.3 billion in 2024 to 2025 confirming that global farmland has completed its structural repositioning from a pure production asset to a mainstream institutional real estate asset class delivering inflation-hedging, income, capital appreciation, and carbon sequestration returns simultaneously.

| Standard License: USD 7,500 | Enterprise License: USD 10,500 |

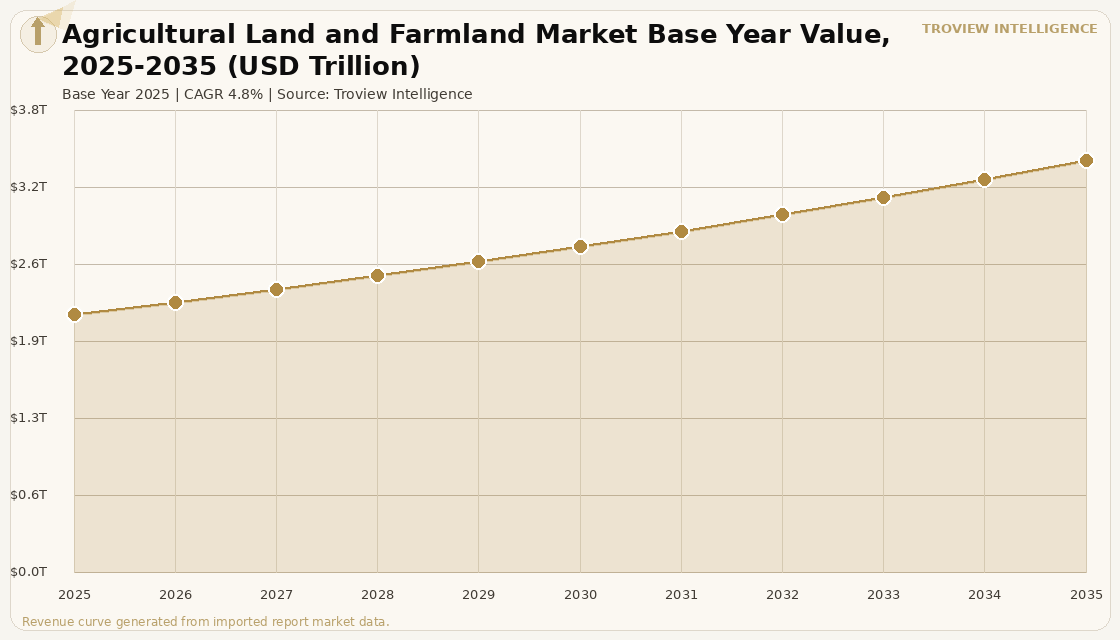

MARKET SYNOPSIS

The global agricultural land and farmland market size was USD 2.14 Trillion in 2025 and is expected to register a revenue CAGR of 4.8% during the forecast period, reaching USD 3.42 Trillion by 2035. The 2025 market estimate is grounded in verified land value data: US national cropland values reached USD 5,830 per acre in August 2025, a 4.7% increase over 2024 per USDA National Agricultural Statistics Service Land Values 2025 Summary, with US pastureland values rising 5.2% in 2024; Australian median farmland prices declining 6% in 2024 following a 79% appreciation from 2020 to 2023 per RaboResearch Australian Farmland Price Outlook 2025 based on 1,200 sampled agricultural sales nationwide; and global farmland recording an 11% compound annual growth rate over the two decades from 2002 to 2021 per Savills research cited in peer-reviewed academic analysis. The market encompasses the total investible universe of commercially operated agricultural land and farmland globally, including arable cropland, improved and unimproved grazing pasture, irrigated horticulture, permanent plantation, and mixed-use agricultural properties held by institutional investors, corporations, family farming enterprises, and government sovereign wealth vehicles. Market revenue growth is supported by the convergence of three structural demand drivers: global food security concerns that elevate the strategic value of productive farmland as a finite and non-replicable asset in a world where urban expansion continuously reduces the total agricultural land base; the capital inflow from institutional investors, real estate developers, and private equity funds that have driven land prices above agricultural production fundamentals in regions close to urban centres; and the emergence of carbon sequestration, biodiversity credits, and renewable energy co-location as income streams that enhance the total return profile of farmland investment. For instance, in 2024, Agriculture and Natural Solutions Acquisition Corporation, United States, Nasdaq-listed, purchased the Australian Food and Agriculture Company portfolio for AUD 780 million, encompassing 13 New South Wales farms totalling 225,405 hectares including the high-profile Wanganella and Poll Boonoke Merino studs, confirming that cross-border institutional capital continues to target large-scale Australian agricultural land assets at premium valuations per Raine and Horne Rural industry reporting. These are some of the key factors driving revenue growth of the market.

Nuveen Natural Capital, United States, operates as a global leader in acquiring, managing, and marketing farmland assets with more than 39 years of experience spanning 11 geographies and more than 60 agricultural crop types per Nuveen company information, providing institutional investors with diversified farmland exposure across row crops, permanent crops, viticulture, and horticulture assets in North America, South America, Australia, and Europe. The Federal Reserve Bank of Kansas City noted in its Q2 2025 agricultural finance report that despite headwinds in farm income and credit conditions, land values have shown remarkable resilience, with the basic economics of supply and demand underpinning quality farmland valuations as prime irrigated cropland, generational cattle ranches, and premier properties rarely come to market and attract serious attention from qualified buyers who understand that replacement opportunities may not emerge for years per Mason Morse Ranch Company analysis of September 2025. Farmland Partners Inc., United States, sold USD 289 million worth of US farmland to Farmland Reserve in 2024 in one of the most notable institutional farmland transactions of the year, reflecting the continued appetite of large-scale institutional and faith-aligned capital for US row crop farmland exposure at established valuations per cioinvestmentclub.com analysis citing verified transaction data. PGIM, the investment management arm of MetLife, operates as a dedicated farmland investment institution specifically serving institutional investors seeking portfolio diversification into the farmland asset class per PGIM company positioning, alongside Hancock Natural Resource Group, UBS Asset Management's farmland platform, and Manulife Investment Management's timberland and farmland unit. These are some of the key factors driving revenue growth of the market.

However, the global agricultural land and farmland market faces structural constraints that temper the pace of capital deployment and land value appreciation across the forecast period. Rising interest rates from 2022 through 2025 reduced farmland purchasing power for leveraged buyers, with RaboResearch's Australian Farmland Price Outlook 2025 specifically identifying higher interest rates and fertiliser input costs as the primary drivers of the 6% decline in Australian median farmland prices in 2024, with the headwinds of commodity price declines compounding the financing cost pressure on marginal agricultural operations whose land values are most closely tied to current-year profitability expectations. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis affecting approximately 20% of global seaborne LNG flows, create upward pressure on fertiliser input costs for agricultural operations globally, as ammonia-based nitrogen fertiliser production is directly linked to natural gas prices through the Haber-Bosch process, with LNG price volatility transmitting directly into the cost of production for the grain, oilseed, and horticulture crops that generate farmland's operating income and underpin land value fundamentals. Foreign investment restrictions on agricultural land acquisitions, including Australia's Foreign Investment Review Board thresholds, Canada's Investment Canada Act agricultural land review provisions, and emerging EU member state restrictions on non-EU agricultural land purchases, create regulatory barriers that limit the cross-border institutional capital deployment that has driven above-inflation farmland appreciation since 2015. These factors substantially limit global agricultural land and farmland market growth over the forecast period.

Farmland is the only real estate asset class where the underlying commodity that determines income is consumed by 8 billion people every day and cannot be substituted by technology. You can substitute coal with solar. You can substitute a retail shop with e-commerce. You can substitute an office with a Zoom call. You cannot substitute wheat, beef, soybeans, or fresh vegetables with anything other than other food. The institutional case for farmland as a core real estate allocation rests on this irreducible demand fact, combined with the physical constraint that total global arable land is declining, not growing, as urban expansion, soil degradation, and climate change permanently remove productive farmland from the agricultural land base. Nuveen has understood this for 39 years. Hancock Natural Resources understood it before that. The pension funds, sovereign wealth funds, and endowments that are now allocating to farmland through managed platforms are catching up to an insight that patient institutional capital has been compounding for four decades. The 4.8% CAGR we project for the 2025 to 2035 period is not a bull case. It is the base case for an asset whose underlying demand cannot go down and whose supply cannot go up." Troview Intelligence Head of Global Agricultural Land and Farmland Research

SEGMENT INSIGHTS

Five Regions Defining Global Agricultural Land Market Dynamics

| US National Cropland 2025 | US Pastureland 2024 | Key Transaction 2024 | Federal Reserve Kansas City |

| USD 5,830/acre (+4.7% YoY, USDA NASS Aug 2025) | +5.2% growth (USDA) | Farmland Partners AUD 289M sale to Farmland Reserve | Q2 2025: Land values show remarkable resilience |

North America is the world's largest and most institutionally mature agricultural land and farmland market, with the United States Corn Belt providing the global benchmark for row crop farmland valuation through the USDA NASS Land Values annual summary that has tracked national cropland and pastureland values since the 1970s. US national cropland values averaged USD 5,830 per acre in August 2025, a 4.7% increase over 2024 per USDA National Agricultural Statistics Service Land Values 2025 Summary, with the Federal Reserve Bank of Kansas City confirming in its Q2 2025 agricultural finance report that land values have shown remarkable resilience despite headwinds in farm income and credit conditions. Oklahoma farm real estate averaged USD 2,880 per acre in 2025, up 5.9% from 2024 the highest growth rate in the Southern Plains region per USDA NASS August 2025 while West Texas median farmland prices reached a new high of USD 2,662 per acre, up 12.89% year-on-year, the largest percentage increase among all seven Texas regions per the Texas Real Estate Research Center. Canada's prairie farmland markets anchored by Saskatchewan and Alberta grain production have attracted sustained domestic pension and institutional investor interest, with high-quality grain land in Saskatchewan achieving above CAD 2,000 per acre as the production economics of canola and wheat in the province attract institutional capital from domestic pension funds and agricultural lenders.

| EU Agricultural Outlook 2024-35 | ABARES 2024-25 Agriculture Value | Australia 2024 Median Farmland | Key Australia Transaction 2024 |

| Farmland values projected to rise (European Commission) | AUD 88.4 Billion (agriculture alone, up AUD 6B) | -6% YoY after 79% growth 2020-2023 (Rabobank) | ANSA Corp AUD 780M for 225,405ha NSW portfolio |

Europe's agricultural land market is underpinned by the EU Common Agricultural Policy which provides direct payment subsidies to farmland owners per hectare, creating a government-backed income floor that elevates farmland valuations above pure production economics and makes European farmland attractive to pension fund investors seeking income-secure long-duration real estate alternatives to bonds. The European Commission's EU Agricultural Outlook 2024 to 2035 states that farmland values are projected to rise over the coming decade, influenced by agricultural product policies focusing on protein crops, crop rotation, and plant proteins alongside consumer preferences for sustainable and plant-based foods per cioinvestmentclub.com analysis. Australia's agriculture sector is forecast by ABARES to be worth AUD 88.4 billion in 2024 to 2025, up AUD 6 billion from the prior year, with winter crop production volumes rising 16% to 55.1 million tonnes per ABARES December 2024 outlook reports, driven by higher livestock prices and favourable growing conditions across New South Wales, Queensland, and Western Australia.

| Nuveen Natural Capital | Brazil Cerrado | African Farmland | CAGR (South America) |

| 39+ years, 11 geographies, Radar JV in Brazil | World's most productive frontier ag region | Sovereign wealth food security investment target | Fastest-growing region in global farmland market |

South America's agricultural land market, anchored by the Brazilian Cerrado's soybean, corn, cotton, and sugarcane frontier production and Argentina's Pampas grain and cattle pastoral system, offers institutional investors access to large-scale, high-productivity farmland at per-hectare valuations materially below equivalent North American productivity benchmarks, creating the value proposition that has attracted Nuveen Natural Capital's Radar Asset Management joint venture as the primary institutional farmland investment platform for Brazilian agricultural land with centralized research and portfolio management supported by local expert personnel in key agriculture regions. Sub-Saharan Africa's agricultural land market is increasingly targeted by sovereign wealth funds and government food security investment vehicles from the Gulf Cooperation Council, East Asian, and Middle Eastern countries whose domestic food production cannot meet national consumption requirements, with investments in Ethiopia, Tanzania, Mozambique, and Zambia representing the frontier tier of institutional agricultural land investment where production and title risk premiums are highest but land acquisition costs relative to long-term productivity potential are most compelling.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from verified company announcements, USDA government data publications, ABARES reports, RaboResearch analysis, and verified trade press.