| TROVIEW INTELLIGENCE | Australia Agricultural Land and Farmland Market | Q2 2026 |

| TROVIEW INTELLIGENCE · COUNTRY INTELLIGENCE REPORT |

By State · By Land Type · By Investor Class · By Commodity System

State Profiles: New South Wales · Victoria · Queensland · Western Australia · South Australia

ABARES forecasts Australia's combined agriculture, fisheries, and forestry sectors to reach AUD 94.3 billion in 2024 to 2025 with the agriculture sector alone valued at AUD 88.4 billion, up AUD 6 billion from the prior year, driven by higher livestock prices and winter crop production volumes rising 16% to 55.1 million tonnes, Australian median farmland prices declining 6% in 2024 after an extraordinary 79% appreciation from 2020 to 2023 per RaboResearch 2025 farmland outlook analysis of 1,200 sampled sales, South Australia and New South Wales recording growth in H1 2025 with NSW prices at AUD 9,815 per hectare, Agriculture and Natural Solutions Acquisition Corporation purchasing the Australian Food and Agriculture Company portfolio for AUD 780 million across 225,405 hectares in New South Wales in 2024, Warakirri Asset Management purchasing the 26,855-hectare Worral Creek Aggregation in Queensland for AUD 350 million, and RaboResearch forecasting a return to modest growth in 2025 supported by anticipated cash rate declines and a positive commodity price outlook confirming Australia's position as one of the world's most sought-after cross-border institutional agricultural land investment destinations despite the post-boom valuation correction.

| Standard License: USD 6,500 | Enterprise License: USD 9,500 |

MARKET SYNOPSIS

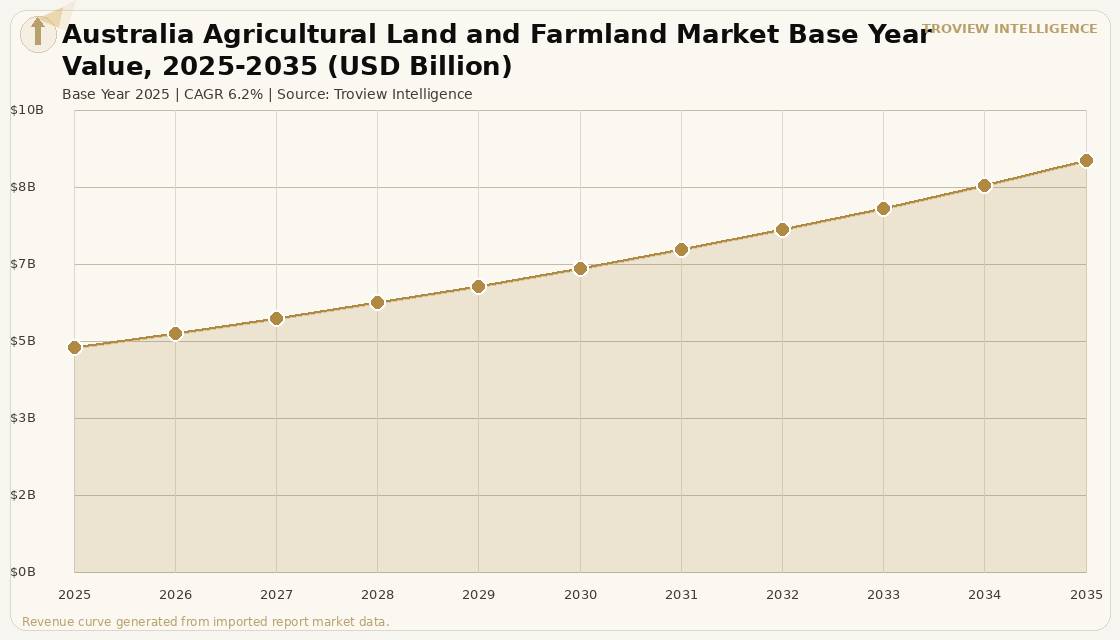

The Australia agricultural land and farmland market size was USD 4.76 Billion in 2025 and is expected to register a revenue CAGR of 6.2% during the forecast period, reaching USD 8.71 Billion by 2035. The 2025 market estimate is grounded in verified industry data: ABARES forecasts Australia's agriculture sector alone to be worth AUD 88.4 billion in 2024 to 2025, up AUD 6 billion from the prior year, as higher livestock prices and favourable grain production conditions drive the sector's highest nominal output value in recent years per ABARES December 2024 outlook report; Australian median farmland prices declined 6% in 2024 across all land types per RaboResearch Australian Farmland Price Outlook 2025 based on a sample of 1,200 agricultural land sales nationwide, following an extraordinary 79% appreciation from 2020 to 2023 that elevated Australian farmland valuations to levels that required a period of consolidation before resuming growth; and South Australia and New South Wales were the only states to record growth in H1 2025, with NSW prices at AUD 9,815 per hectare, up 1.3%, and South Australia prices at AUD 9,214 per hectare, up 15.8%, per Bendigo Bank Agribusiness 2025 Farmland Values Report. Market revenue growth is anchored in Australia's structural position as one of the world's premier agricultural land investment destinations, combining food production quality and diversity from Murray-Darling Basin irrigated horticulture to Queensland beef cattle pastoral stations and Western Australian grain belt broadacre properties with institutional-grade property rights, transparent title systems, and a Foreign Investment Review Board oversight framework that provides the regulatory clarity required for sovereign wealth and pension fund capital to make large-scale agricultural land commitments. For instance, in 2024, Agriculture and Natural Solutions Acquisition Corporation, United States, Nasdaq-listed, purchased the Australian Food and Agriculture Company portfolio for AUD 780 million encompassing 13 New South Wales farms totalling 225,405 hectares including the high-profile Wanganella and Poll Boonoke Merino studs the highest-value agricultural land transaction in Australia in 2024 confirming that US institutional capital at scale continues to pursue prime Australian broadacre and Merino station assets despite the post-boom valuation correction per Raine and Horne Rural reporting. These are some of the key factors driving revenue growth of the market.

Warakirri Asset Management, Australia, on behalf of US-headquartered Alkira Farms, purchased the 26,855-hectare Worral Creek Aggregation in Queensland for AUD 350 million in 2024, divested as part of succession planning by its long-time owners and marking one of Queensland's highest-value single agricultural land transactions per Raine and Horne Rural reporting, confirming that cross-border capital continues to target scale pastoral and broadacre beef production aggregations in Queensland where the combination of land size, beef cattle production capacity, and the northern Australian beef export corridor to Asia generates the long-term production and appreciation returns that institutional agricultural investors require. RaboResearch's Australian Farmland Price Outlook 2025 forecasts a return to modest growth in 2025, with lead author Paul Joules noting that a favourable outlook for commodity prices particularly dairy and beef prices per the Australian commodity price index alongside an anticipated decline in the Reserve Bank of Australia cash rate support the thesis of a recovery, with neutral ENSO conditions pointing towards rainfall closer to average through much of 2025 reducing the drought risk that suppressed land values in Victoria and Queensland through 2024. Australian agricultural sector output growth of 16% in winter crop production volumes to 55.1 million tonnes in 2024 to 2025 per ABARES, driven by favourable growing conditions in New South Wales, Queensland, and Western Australia, provides the commodity income foundation that supports buyer confidence in farmland acquisition for 2025 and 2026 per Travis Wentriro of Raine and Horne Rural who noted demand for rural property will likely strengthen further if rainfall forecasts prove accurate and the Reserve Bank cuts rates. These are some of the key factors driving revenue growth of the market.

However, the Australia agricultural land and farmland market faces structural constraints that temper the pace of land value recovery and institutional capital deployment in the current cycle. The sharp 13% decline in Australian grazing land prices in 2024 per RaboResearch analysis, driven by the combination of higher interest rates, lower commodity prices, and elevated fertiliser input costs, reflects the operational margin pressure on livestock producers whose pastoral land valuations are most directly tied to cattle and sheep profitability with the pullback in overseas corporate investment particularly notable in the dairy space where returns have begun to normalise after a period of high profitability, suggesting that foreign institutional capital is taking a more selective approach to Australian farmland acquisition as margins compress. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, affect Australian agricultural land operating costs through fertiliser price transmission, as Australia's grain and oilseed producers are direct consumers of nitrogen fertiliser whose production economics are linked to international natural gas and LNG prices, creating operating cost exposure that reduces the net farm income available to support land purchase price expectations. The Foreign Investment Review Board's AUD 15 million threshold for foreign investment review of agricultural land reduced from prior higher thresholds by amendments to the Foreign Acquisitions and Takeovers Act increases regulatory complexity and approval timeline risk for the large-scale cross-border farmland acquisitions that characterised the 2020 to 2023 boom period. These factors substantially limit Australia agricultural land and farmland market growth over the forecast period.

The Australian agricultural land market in 2025 is at the most interesting entry point for institutional capital in a decade. The 79% appreciation from 2020 to 2023 has corrected 6% nationally in 2024. Interest rates are starting to fall. ABARES is forecasting AUD 88.4 billion in agricultural output for 2024 to 2025. Rabobank is calling a return to modest growth. The buyers who bought at the peak in 2022 are sitting on paper losses in grazing land, which was down 13%. The buyers who are looking at 2025 to 2026 as a vintage are buying at a 6% to 13% discount to those peak buyers, with the commodity cycle and interest rate cycle both turning in their favour. That is the structural case for Australian farmland investment at the current point in the cycle. Whether cross-border institutional capital is willing to navigate the FIRB review process at AUD 15 million thresholds, the time it takes to complete a quality due diligence on a 200,000-hectare broadacre portfolio, and the concentration risk of any single Australian state's climate and commodity exposure those are the deal-by-deal variables. The structural case is sound. The execution is what separates the institutional managers who generate returns from those who generate paperwork." Troview Intelligence Head of Australia Agricultural Land and Farmland Research

SEGMENT INSIGHTS

| 03 | STATE PROFILE ANALYSIS |

Five States Defining Australia's Agricultural Land Market

| H1 2025 Median Price | H1 2025 Sales Volume | Key 2024 Transaction | Primary Land Types |

| AUD 9,815/ha (+1.3% H1 2025) | 1,163 sales (-23.8% YoY) | AUD 780M ANSA Corp 225,405ha Merino stud portfolio | Murray-Darling irrigated, Riverina grain, northern beef, Merino studs |

New South Wales recorded a median farmland price of AUD 9,815 per hectare in H1 2025, up 1.3% year-on-year, making it one of only two Australian states to record price growth in the first half of 2025 alongside South Australia per Bendigo Bank Agribusiness 2025 Farmland Values Report, despite the sharpest sales volume decline of any state at 23.8% to 1,163 sales a reduction partly attributed to the increasing prevalence of off-market sales as vendors pursue expression-of-interest processes that bypass traditional listed sale formats. The highest-value agricultural land transaction in Australia in 2024 was the purchase of the Australian Food and Agriculture Company portfolio for AUD 780 million by the US Nasdaq-listed Agriculture and Natural Solutions Acquisition Corporation, encompassing 13 New South Wales farms totalling 225,405 hectares including the Wanganella and Poll Boonoke Merino studs historic bloodline properties that command premiums above pure land and production value that reflect the genetic capital accumulated across decades of stud management. The diversity of New South Wales agricultural land types spanning the Murray-Darling Basin's irrigated horticulture and viticulture, the Riverina's dryland grain and rice production, the central west's wheat-sheep mix, and the northern tablelands' beef cattle and Merino country provides the broadest within-state agricultural land investment diversification of any Australian state per ABARES agricultural zone mapping.

| H1 2025 Sales Volume | Key 2024 Transaction | Primary Export | Outlook |

| 713 sales (-22.4% YoY) | AUD 350M Worral Creek Aggregation (26,855ha) | Northern Australian beef to Asia via Darwin and Townsville | Victoria and Queensland return to growth H2 2025-2026 (Bendigo) |

Queensland is Australia's largest-area farmland state by total agricultural land extent, encompassing the northern tropical beef cattle pastoral stations in the Gulf Country and Cape York, the mixed farming grain and cattle regions of the Darling Downs and Maranoa, and the sugar cane coastal belt from Bundaberg to Cairns that generates export value from global sugar markets. The 26,855-hectare Worral Creek Aggregation in Queensland, purchased by Warakirri Asset Management on behalf of US-headquartered Alkira Farms for AUD 350 million in 2024 as part of succession planning by its long-time owners, represents the scale of aggregated beef cattle pastoral property that international institutional investors target in Queensland as a platform for Asian beef export supply chain integration. Queensland farmland sales volumes declined 22.4% in H1 2025 to 713 sales per Bendigo Bank analysis, reflecting the same off-market transaction trend and buyer selectivity seen in New South Wales, with Bendigo Bank's Sean Hickey forecasting that Victoria and Queensland should see a return to growth in the remainder of 2025 and into 2026 as interest rates fall and commodity conditions improve per Bendigo Bank Agribusiness 2025 Farmland Values Report.

WESTERN AUSTRALIA FASTEST-GROWING FARMLAND PRICES +12% IN 2024, GRAIN BELT LEADER

| 2024 Median Price Change | Primary Production | Export Gateway | Land Scale |

| +12% YoY bucking national -6% trend (Rabobank) | Wheat, barley, canola dryland grain belt | Fremantle and Kwinana Asian grain market access | Largest dryland grain belt farmland parcels in Australia |

Western Australia's agricultural land market stands apart from the national trend, recording a 12% increase in median farmland prices in 2024 against the national 6% decline per RaboResearch Australian Farmland Price Outlook 2025, driven by the Western Australian grain belt's cost-competitive broadacre grain and oilseed production economics and the state's favourable growing season conditions in 2023 to 2024 that generated above-average crop yields at a time when WA's established export relationships with Japan, South Korea, and Indonesia sustained demand for the state's wheat, barley, and canola shipments through Fremantle and Kwinana port facilities. Western Australian grain belt properties offer the largest individual dryland grain farm parcel sizes of any Australian state, with properties spanning 5,000 to 50,000 hectares enabling the scale economies required for competitive broadacre grain production against global price benchmarks, making Western Australian farmland attractive to institutional agricultural investors seeking exposure to the low-cost production end of the global grain supply chain rather than the premium irrigated horticulture assets of the Murray-Darling Basin.

| SA H1 2025 Price | SA 2024 Full Year | Victoria Focus | Almond Orchards |

| AUD 9,214/ha (+15.8% H1 2025) | +18pc partly higher-quality property weighting effect | Murray-Darling Basin irrigation, dairy restructuring | Riverland SA almond orchards premium permanent crop |

South Australia recorded the strongest farmland price performance in H1 2025 at AUD 9,214 per hectare, up 15.8% year-on-year, and was up 18.4% for the full year to H1 2025 per Bendigo Bank Agribusiness reporting, though Bendigo Bank's Sean Hickey cautioned that the statewide price appreciation partially reflects a higher proportion of sales in premium regions skewing the statewide median upward, with five of the state's seven regions recording year-on-year price declines at the regional level amid persistent drought conditions and record rainfall deficits. South Australia's Riverland and Sunraysia districts are home to Australia's largest almond and citrus orchard concentrations, with water entitlement values from the Murray-Darling Basin allocation system adding a traded water asset component to irrigated horticulture land value that is unique to the South Australian and Victorian irrigation districts. Victoria's dairy farmland, concentrated in the Gippsland, Northern, and Western districts, has been undergoing structural ownership change as foreign institutional dairy investment from China and Japan normalised following the dairy profitability cycle peak of 2022 to 2023, creating acquisition opportunities for domestic operators and domestic institutional managers in a segment where the pullback in overseas corporate investment has, per RaboResearch analysis, taken the steam out of dairy farmland investment and created more attractive entry valuations.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from ABARES official data, RaboResearch farmland research, Bendigo Bank Agribusiness reports, Raine and Horne Rural market reporting, and verified trade press.