By Province - By Asset Class - By Investment Vehicle - By Revenue Stream

Province Spotlights: British Columbia - Ontario - Quebec

Canada's forest products industry employs hundreds of thousands of Canadians and generates tens of billions in annual export revenue, Ontario's forest sector contributed CAD 5.20 Billion to provincial GDP in 2024 with forest sector exports totalling CAD 8.30 Billion, 74% of Ontario's forest management units are certified representing 6% of the world's certified forests, the National Building Code of Canada expanded mass timber construction to twelve storeys in 2020, the Government of Canada launched USD 500 Million in forest sector support in February 2026, Element5 is investing USD 107 Million to expand mass timber operations in St. Thomas Ontario, and British Columbia is home to landmark projects including the 18-storey Brock Commons Tallwood House at the University of British Columbia.

MARKET SYNOPSIS

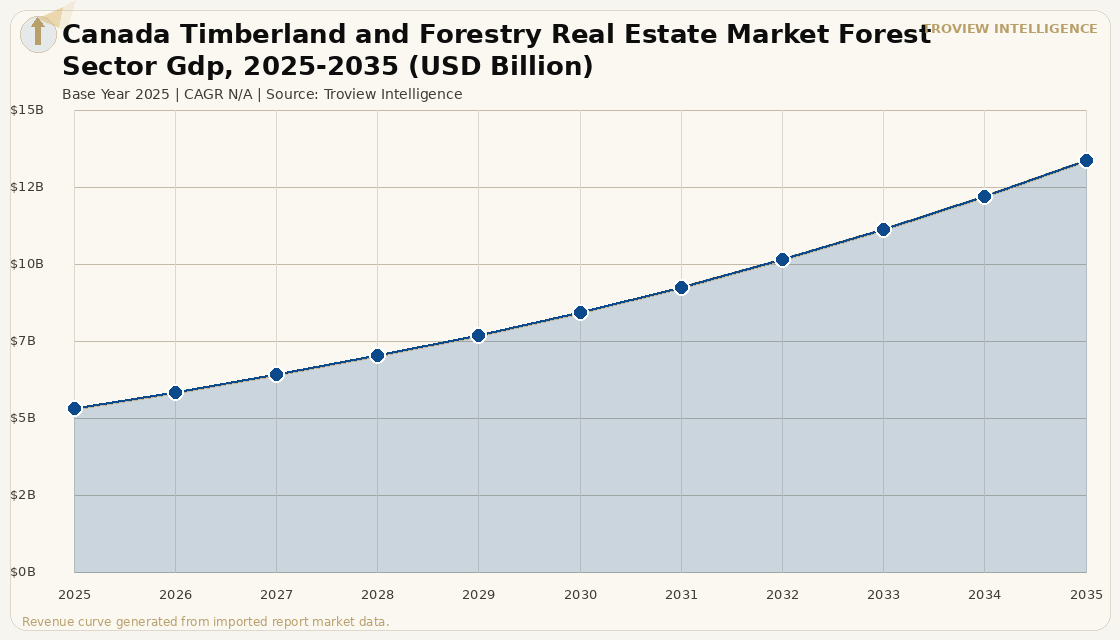

The Canada timberland and forestry real estate market is one of the world's most significant forestry investment and management jurisdictions, underpinned by the country's vast boreal and coastal forest estate which provides the raw material base for a forest products industry that employs hundreds of thousands of Canadians and generates tens of billions in annual export revenue per Morningstar verified March 2026 Canada mass timber construction reporting. Canada's forest sector produced CAD 8.30 Billion in Ontario forest sector exports alone in 2024, contributing CAD 5.20 Billion to Ontario's provincial GDP, with forests covering 66% of Ontario's land area and 74% of Ontario's forest management units certified as sustainably managed representing 6% of the world's total certified forest area per Invest Ontario verified forestry sector data. The national timberland and forestry real estate market is simultaneously a mature industrial forestry investment destination and an emerging mass timber construction supply chain investment opportunity, with the National Building Code of Canada's 2020 edition expanding permitted height of encapsulated mass timber construction to twelve storeys, provincial building codes across Ontario, Quebec, Alberta, and British Columbia aligning to reflect these changes, and regulatory conversations pointing toward further height increases in future code cycles per Morningstar Canada mass timber construction verified reporting of March 2026. For instance, in February 2026, the Government of Canada, Ottawa, launched USD 500 Million in support for retooling Canada's forest sector under the Investments in Forest Industry Transformation programme, simultaneously investing in Atlantic Canada's forest sector, supporting sustainable wood construction in Quebec, and investing in Nova Scotia's local mass timber industry per Natural Resources Canada IFIT programme data, confirming the federal government's commitment to the long-term capital modernisation and market development of Canada's forestry sector. These are some of the key factors driving revenue growth of the market.

Canada's timberland and forestry real estate investment market encompasses institutional forest land ownership by pension funds with Ontario Teachers' Pension Plan having executed an 870,000-acre redemption in 2022 confirming its long-standing large-scale timberland investment history per Forisk 2025 timberland transactions review TIMOs including Manulife Investment Management that manage Canadian and global timberland on behalf of institutional clients, publicly listed forest product companies including West Fraser Timber and Acadian Timber with significant Canadian forestland bases, and a rapidly developing mass timber and engineered wood manufacturing sector anchored by British Columbia's CLT and glulam industry infrastructure and Ontario's expanding mass timber production capacity. Acadian Timber Corp., a Canadian publicly traded timberland company, is monetising carbon sequestration with planned carbon credits totalling 390,000 by mid-2025 at USD 20.00 to USD 30.00 per tonne per verified analyst reporting, demonstrating that Canadian timberland assets are accessible to carbon credit programme registration under major voluntary carbon market standards. West Fraser Timber Co. Ltd. reported CAD 6.17 Billion in sales for 2024 with 11% EBITDA margin, investing in sawmill modernisation and renewable energy including solar panels to cut mill energy use as part of the company's green initiatives per verified wood industry statistics data.

However, the Canada timberland and forestry real estate market faces structural constraints that limit the pace of investment capital deployment and revenue growth. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating diesel cost inflation that increases logging equipment operation, log haul, and timber processing costs across British Columbia's interior and Ontario's boreal forest regions where logging and transport operations are heavily fuel-dependent. The US-Canada softwood lumber trade dispute which has resulted in sustained US countervailing and anti-dumping duties on Canadian softwood lumber imports creates pricing uncertainty for Canadian timberland owners whose logs and lumber are destined for US construction markets, as tariff rate changes and ongoing legal dispute proceedings under CUSMA create unpredictable revenue reductions that complicate the return modelling of timberland investments targeting US lumber market exposure. The shortage of skilled loggers, harvesting machine operators, and forestry technicians across Canadian provinces particularly in British Columbia and Ontario where the workforce demographic is aging and new entrant volumes are insufficient to replace retirements limits harvest volumes and increases per-tonne extraction cost, reducing the cash flow realisation from standing timber inventories at a time when timber pricing could otherwise support increased harvest activity. These factors substantially limit Canada timberland and forestry real estate market growth over the forecast period.

TROVIEW ANALYST PERSPECTIVE "Canada's timberland investment market in 2025 is defined by two intersecting opportunities: the traditional log and lumber production value chain that has made Canadian forest assets a cornerstone of institutional pension fund portfolios for three decades, and the emerging mass timber construction opportunity that is converting Canada's vast boreal and coastal softwood resource into a twenty-first century green building material with demand characteristics driven by building code reform, embodied carbon regulation, and ESG investment mandates rather than commodity housing cycle dynamics. Ontario Teachers' Pension's 870,000-acre redemption in 2022 was not a signal that Canadian timberland is being abandoned by institutional capital it was an asset rotation by one of the world's most sophisticated pension fund managers. The ongoing Government of Canada USD 500 million IFIT programme and Element5's USD 107 million mass timber expansion in St. Thomas are the signals of what the next decade looks like: a country investing in converting its standing timber advantage into a manufacturing advantage in the fastest-growing segment of global construction. The softwood lumber tariff dispute with the United States is the persistent headwind. Canadian timberland owners who are diversifying their log marketing toward domestic mass timber consumption and Pacific export markets to Japan and China are less exposed to US tariff volatility than those still primarily dependent on US lumber market realisation." Troview Intelligence Head of Canada Timberland and Forestry Real Estate Research

SEGMENT INSIGHTS

REGIONAL ANALYSIS

British Columbia

| Landmark Mass Timber Project | Manufacturing Capacity | Key Timber Species | Weyerhaeuser BC Transaction |

| Brock Commons Tallwood House, UBC 18 storeys (2017) | CLT and glulam facilities opened and expanded | Douglas Fir, Cedar premium Japan export species | Princeton Mill sold to Gorman Group for CAD 120M (2025) |

British Columbia is the epicentre of Canada's mass timber innovation and the country's most technically advanced timberland and forestry real estate market, with the Brock Commons Tallwood House at the University of British Columbia an 18-storey mass timber residence completed in 2017 that was among the tallest wood buildings in the world at the time demonstrating the structural capability of CLT construction and catalysing a wave of institutional and developer interest in mass timber as a viable high-rise building system. British Columbia's coastal and interior forests provide the foundation for a CLT and glulam manufacturing sector that has expanded rapidly in response to the National Building Code's 12-storey mass timber permission and the growing embodied carbon requirements of institutional real estate investors, with new manufacturing facilities opening across the Lower Mainland, the Okanagan, and the BC Interior that supply domestic and export mass timber demand. Weyerhaeuser's sale of its Princeton Mill in British Columbia to the Gorman Group for CAD 120 Million (USD 87 Million approximately) in 2025 confirmed the active market for British Columbia forestry assets among domestic purchasers with long-term BC market commitment, with Gorman's emphasis on sustainable forestry and BC market knowledge making it the preferred acquirer for Weyerhaeuser's non-core BC processing asset per verified analyst reporting. British Columbia's timberland also benefits from direct access to deep-water export terminals at Vancouver, Prince Rupert, and Port Alberni that enable log and lumber export to Japan, China, South Korea, and India export markets that command premium pricing for high-grade BC Douglas Fir and Hemlock relative to domestic Canadian construction grade pricing.

Ontario

| Forest Sector GDP (2024) | Forest Sector Exports (2024) | Forest Cover | Certification Rate |

| CAD 5.20 Billion | CAD 8.30 Billion | 66% of provincial land area | 74% of management units 6% of world certified forest |

Ontario is Canada's largest provincial forestry economy by export value, contributing CAD 5.20 Billion to provincial GDP and generating CAD 8.30 Billion in forest sector exports in 2024, with 66% of Ontario's land area covered by forest and 74% of forest management units certified under international sustainable forestry standards representing 6% of the world's total certified forest area per Invest Ontario verified forestry sector data. Ontario's certified forest proportion makes it a highly attractive destination for institutional timberland investment by ESG-mandated pension funds, endowments, and sovereign wealth funds that require certified sustainable forest management as a prerequisite for acquisition, as third-party certification provides documentary evidence of responsible harvesting practices, regeneration compliance, biodiversity protection, and Indigenous consultation that institutional investment policies increasingly mandate. Element5, a Canadian mass timber manufacturer, is investing USD 107 Million to expand its mass timber operations in St. Thomas, Ontario, creating a major increase in Ontario's CLT and glulam manufacturing capacity that will generate demand for certified Ontario softwood timber input and create a domestic end-use market for Ontario timberland owners who currently export significant volumes of lumber to US construction markets subject to softwood tariff headwinds. The Government of Canada's March 2025 investment in sustainable wood construction in partnership with Quebec, and the February 2026 USD 500 Million IFIT programme, both direct capital into the Ontario-Quebec forest products manufacturing sector that supplies mass timber developers building twelve-storey encapsulated mass timber structures under the 2020 National Building Code provisions.

Quebec

| Forest Resource | Federal-Provincial Collaboration | Carbon Opportunity | Key Advantage |

| Second-largest commercial forest province | CAD investment in sustainable wood construction (Mar 2025) | Boreal forest carbon sequestration registrations growing | First Nations partnership forestry model established |

Quebec is Canada's second-largest commercial forest province, hosting an extensive boreal softwood and mixed wood forest estate across the Laurentian Highlands, the Abitibi region, and the Outaouais that collectively form one of the world's largest contiguous managed forest areas and support a major pulp, paper, lumber, and emerging mass timber manufacturing sector. The Government of Canada and Quebec jointly invested in sustainable wood construction in March 2025, targeting the integration of Quebec-sourced CLT and glulam into public building programmes and supporting the domestic mass timber supply chain that reduces Quebec developers' dependence on British Columbia CLT imports for large-scale mass timber projects in Montreal, Quebec City, and the greater Montreal metropolitan area. Quebec's boreal forest is increasingly recognised as a significant carbon sequestration asset, with growing interest from voluntary carbon market programme operators in registering Quebec forest carbon projects that generate Verra VCS or Gold Standard credits marketable to corporate buyers pursuing Scope 1 and 3 net-zero commitments. First Nations communities in Quebec hold significant forestry tenure rights across the Cree territory in the James Bay region and the Anishinaabe territories in the Mauricie and Abitibi regions, and are increasingly participating in carbon credit programme development and sustainable forestry enterprise that generates economic development revenue alongside traditional forestry activities.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from verified company press releases, Natural Resources Canada, Invest Ontario, and verified trade press.