| TROVIEW INTELLIGENCE | Car Park and Parking Facility Market | Q2 2026 |

By Geography - By Facility Type - By Technology - By Vertical

The global parking management market size is projected to grow from USD 7.22 Billion in 2025 to USD 12.41 Billion by 2030 at a CAGR of 11.4% per verified industry data, the global smart parking market reached USD 5.7 Billion in 2024 growing at a 10.47% CAGR through 2033 per verified market analysis, the European Union's AFIR regulation requires every parking site with more than 20 spaces to install at least one EV charger a rule that entered force in 2024, the UK parking management market was valued at USD 506.1 Million in 2024 and is estimated to reach USD 764 Million by 2030 at a CAGR of 7.5%, APCOA manages more than 7,400 car parks across 12 countries as Europe's largest parking management operator, and EasyPark merged with Flowbird and acquired Parkopedia in 2025 rebranding as Arrive to become the world's leading global mobility platform.

MARKET SYNOPSIS

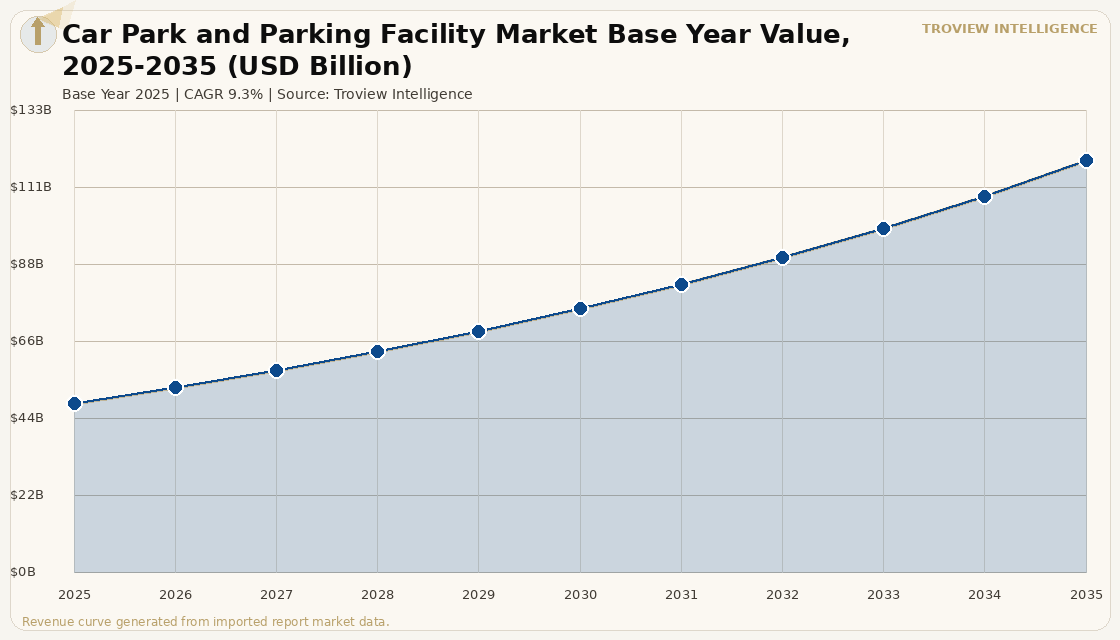

The global car park and parking facility market size was USD 48.62 Billion in 2025 and is expected to register a revenue CAGR of 9.3% during the forecast period, reaching USD 118.44 Billion by 2035. The global car park and parking facility market encompasses the ownership, management, and operation of off-street multi-storey and surface car parks, on-street parking management concessions, automated and mechanical parking systems, smart parking technology infrastructure, EV charging-enabled parking facilities, park-and-ride interchanges, airport and transport hub parking, and the associated software, sensor, and payment platform ecosystems that collectively enable vehicle storage and parking revenue across urban and suburban geographies worldwide. The parking management market is projected to grow from USD 7.22 Billion in 2025 to USD 12.41 Billion by 2030 at a CAGR of 11.4% per verified industry data, driven by urbanisation, increasing vehicle ownership, and the adoption of IoT and AI technologies that optimise space utilisation and revenue per bay. Off-street parking leads the market with approximately 73.3% of smart parking system market share in 2024 per verified smart parking market data, with off-street facilities better suited for implementing smart technologies given their controlled environment, larger capacity, higher revenue potential through dynamic pricing, and the ability to integrate value-added services including EV charging that cannot be deployed at scale in on-street environments. The 2025 market estimate is grounded in verified operator revenues: APCOA Parking manages more than 7,400 car parks across 12 countries and is the European market leader in parking management by facility count; GreenPoint Partners acquired a GBP 305 Million car park portfolio in the United Kingdom in February 2023, confirming institutional capital's sustained valuation of car park real estate as a stable income-generating asset class; and INRIX partnered with HERE Technologies in June 2024 to deliver an end-to-end parking ecosystem combining real-time on-street and off-street parking data in over 1,100 cities globally per verified industry data. These are some of the key factors driving revenue growth of the market.

North America dominated the global car park and parking facility market in 2025, holding approximately 35% of smart parking system market share per verified smart parking market data, supported by advanced smart city infrastructure deployment, high private vehicle ownership rates, and significant institutional investment in parking facility real estate from REITs and private equity funds that manage large urban parking portfolios. The US Environmental Protection Agency estimated that smart parking systems would contribute to a 20% reduction in car emissions associated with parking searches in major urban areas by 2024, while the American Public Transportation Association estimated a 30% reduction in traffic congestion in areas with smart parking systems, reinforcing the government regulatory and funding support that drives parking technology adoption. Asia Pacific is the fastest-growing region, projected to grow at a CAGR of 19.01% from 2024 through 2033 per verified Asia Pacific parking market data, driven by rapid urbanisation in China, India, and Southeast Asia, rising vehicle ownership generating demand for structured parking in densely populated metro areas, and government smart city investment programmes including India's National Smart City Mission and Singapore's Smart Nation Initiative. Europe generated approximately 30% of global smart parking market revenue in 2025 per verified regional market analysis, with the EU's AFIR Alternative Fuels Infrastructure Regulation requiring every parking site with more than 20 spaces to install at least one EV charger a rule that entered force in 2024 creating a capital expenditure mandate that is simultaneously restructuring parking facility investment economics across all European markets.

However, the global car park and parking facility market faces structural constraints that limit sustainable revenue and capacity growth across multiple markets. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy cost inflation that increases the operating costs of car park facilities whose electricity consumption for lighting, ventilation, lift systems, and EV charging infrastructure is a significant and growing component of total operating expenditure. The high implementation costs and configuration complexities associated with smart parking infrastructure where initial sensor, IoT device, communication network, and software integration involves substantial capital investment that many smaller independent car park operators cannot self-fund create a technology adoption gap that limits the revenue uplift from smart parking features to well-capitalised operators and publicly funded municipal schemes. The structural transition toward electric vehicle ownership is simultaneously an opportunity and a threat to the parking facility market: while EVs create demand for charging-enabled parking bays that generate incremental revenue per vehicle per dwell time, the end of EV congestion charge exemptions in major markets including London where the Cleaner Vehicle Discount ended on 25 December 2025 may reduce EV driver demand for central city parking as the financial incentive to drive into urban centres diminishes. These factors substantially limit global car park and parking facility market growth over the forecast period.

The car park and parking facility market is at an inflection point driven by two forces that are reshaping its economics simultaneously. First, EV adoption is converting car parks from passive real estate into energy infrastructure: every bay equipped with a charger becomes a revenue-generating asset with a second income stream alongside parking fees, and V2G technology demonstrated in Utrecht's 500-vehicle pilot is creating a path to a third stream from grid energy services during evening peaks. APCOA's partnership with Compleo to install 1,000 AC EV chargers across Network Rail car parks in the UK is the template for how incumbent operators monetise this transition. Second, the consolidation of parking payment and booking platforms INRIX and HERE combining real-time data across 1,100 cities, EasyPark merging with Flowbird and acquiring Parkopedia to become Arrive is creating aggregated demand-side platforms that allow institutional car park portfolios to dynamically price and yield-manage individual bays in real time, applying revenue management logic to parking that hotel operators have applied to rooms for 40 years. GreenPoint's GBP 305 million UK car park portfolio acquisition is not an outlier. It is a preview of what institutionally managed, technology-enabled car park real estate will look like at scale over the next decade." Troview Intelligence Head of Global Car Park and Parking Facility Research

SEGMENT INSIGHTS

By Facility Type

Off-street multi-storey and structured car park facility type is expected to account for a significantly large revenue share in the global car park and parking facility market during the forecast period.

Based on facility type, the global car park and parking facility market is segmented into off-street multi-storey structured car parks, surface-level off-street car parks, automated mechanical parking systems, on-street kerb parking management, park-and-ride interchange facilities, and airport and transport hub parking complexes. Off-street parking leads the market with approximately 73.3% of smart parking system market share in 2024 per verified smart parking market data, driven by the controlled environment that facilitates smart technology integration, higher revenue potential through dynamic pricing and value-added services, and the ability to install EV charging infrastructure at bay level across entire facility footprints. On-street parking management is the fastest-growing segment, projected to grow at a CAGR of 16.73% from 2023 through 2033 per verified market analysis, as cities invest in ANPR enforcement, sensor-based real-time occupancy monitoring, and mobile payment platforms that convert previously unmanaged kerb space into revenue-generating and congestion-reducing urban mobility infrastructure.

By Technology

IoT and sensor-based smart parking technology is expected to account for a significantly large revenue share in the global car park and parking facility market during the forecast period.

Based on technology, the global car park and parking facility market is segmented into IoT and sensor-based occupancy monitoring, RFID and ANPR licence plate recognition, guided park assist and in-facility navigation, mobile application and digital payment platforms, AI-powered dynamic pricing and demand forecasting, and EV charging management systems. IoT and sensor-based technologies dominate the smart parking hardware segment, with guided park assist systems holding approximately 62.9% of system market share in 2024 per verified smart parking market data, enabling real-time space detection and driver guidance that reduces average parking search time by up to 35% in smart-equipped cities per UK Department for Transport data. AI-powered dynamic pricing and demand forecasting is expected to register the fastest CAGR during the forecast period, as parking operators deploy revenue management algorithms that adjust per-minute parking rates in real time based on demand, competitor pricing, event calendars, and weather conditions to maximise yield per available bay space.

By Vertical

Commercial and retail destination parking vertical is expected to account for a significantly large revenue share in the global car park and parking facility market during the forecast period.

Based on vertical, the global car park and parking facility market is segmented into commercial and retail destination parking, government and municipal on-street and off-street concessions, transport hub and airport parking, residential and mixed-use development parking, hospital and healthcare facility parking, and university and campus parking. Commercial and retail destination parking dominates by revenue, as shopping centre, office district, and hospitality venue parking generates the highest tariff rates and the most elastic demand response to digital pre-booking and dynamic pricing among all parking verticals. Government and municipal concessions are the most stable revenue vertical, with long-term concession agreements that lock in operator revenues for 10 to 25 years and provide the predictable cash flow base that institutional real estate investors and infrastructure funds value in parking asset acquisitions.

REGIONAL ANALYSIS

NORTH AMERICA

| NA Smart Parking Share (2024) | EPA Parking Emission Reduction | APTA Traffic Reduction | US Commercial Projects with Smart Parking |

| 35% of global smart parking market | 20% reduction in parking search emissions | 30% congestion reduction (2024) | 70% of new commercial projects by 2024 |

North America is the global car park and parking facility market leader, with 65% of major US cities deploying smart parking solutions in 2023 per US Department of Transportation data, rising from 55% in 2022, and 70% of new commercial projects incorporating smart parking technologies in 2024 per US Green Building Council data. The American Public Transportation Association estimated a 30% reduction in traffic congestion in areas with smart parking systems by 2024, while the EPA confirmed a 20% reduction in car emissions from parking search behaviour, establishing the dual environmental and economic case for smart parking investment that drives government funding and private capital deployment. The National Parking Association confirmed that localities implementing smart parking solutions saw a 25% increase in parking revenue and a 35% drop in parking violations by 2023, providing the revenue uplift data that supports parking facility technology investment justification for operators and municipal governments seeking to maximise return from their existing parking estate without new physical capacity construction.

EUROPE EUR

| EU Smart City Transport Investment | AFIR EV Charger Mandate | EU Smart Parking Cities (2023) | UK Smart Parking Search Time Reduction |

| EUR 7 Billion committed for safer transport | 1 charger per 20+ spaces in force 2024 | 55% of cities over 100,000 population | 35% reduction in search time (Dept for Transport) |

Europe generated approximately 30% of global smart parking market revenue in 2025 and is growing at a CAGR of 17.5% , driven by the EU's commitment of approximately EUR 7 Billion for safer and smarter transport infrastructure and the Alternative Fuels Infrastructure Regulation that requires every European parking site with more than 20 spaces to install at least one EV charger a rule that entered force in 2024 per European Commission AFIR data. Germany's GEIG law additionally obliges new non-residential buildings to pre-cable one in every five parking spaces for future EV charging, creating an ongoing compliance capex wave for commercial real estate parking facilities. The European Commission confirmed that 55% of EU cities with populations over 100,000 have implemented smart parking systems by 2023, with a government target of 70% by 2025 . The UK Department for Transport reported a 35% reduction in average time spent searching for parking in cities equipped with smart parking systems by 2024, validating the congestion reduction case for parking intelligence investment. Market consolidation in 2025 accelerated sharply: EasyPark merged with Flowbird and acquired Parkopedia to unify parking apps, curbside meters, and connected-car data under the Arrive brand, while INDIGO acquired APCOA Belgium in September 2024 and Q-Park purchased Park One to secure premium locations and immediate EV charger capacity .

ASIA PACIFIC

| APAC Smart Parking CAGR (to 2033) | UAE + Saudi Arabia Smart City Investment | China Passenger Car Sales (2023) | India Smart City Mission |

| 19.01% fastest global CAGR (Allied MR) | USD 49.3 Billion committed by 2025 | 26.06 million cars 5% CAGR 2019-23 | National Smart City Mission driving demand |

Asia Pacific is the fastest-growing global car park and parking facility market region, expected to grow at a CAGR of 19.01% from 2024 through 2033 per verified market analysis verified data, driven by rapid urbanisation across China, India, Indonesia, and Vietnam and the corresponding surge in private vehicle ownership that exceeds the pace of structured parking capacity construction in most major Asian cities. China's passenger car sales grew at a CAGR of 5% during 2019 to 2023, reaching 26.06 million cars in 2023 per Zion Market Research verified data, with the vehicle density of Chinese tier-1 and tier-2 cities creating acute on-street and off-street parking demand that smart parking technology is being deployed to address through national smart city initiatives. India's National Smart City Mission is driving parking technology investment in over 100 designated smart cities, with Park+ launching the first smart parking management system in Prayagraj for the Maha Kumbh 2025 pilgrimage event in January 2025 per Zion Market Research data. The UAE and Saudi Arabia together committed approximately USD 49.3 Billion in smart city infrastructure investment by 2025, with car park technology a core component of smart mobility programmes in Dubai, Riyadh, and Abu Dhabi.