| TROVIEW INTELLIGENCE | Film Studio and Media Production Real Estate Market | Q2 2026 |

| TROVIEW INTELLIGENCE · GLOBAL INTELLIGENCE REPORT |

By Geography · By Facility Type · By Ownership Model · By Production Technology

Los Angeles County maintains the world's largest concentration of soundstage space at 8.3 million square feet of certified and uncertified stages, but average occupancy held at 62% in H1 2025 per FilmLA's eighth annual Sound Stage Production Report released March 18 2026 down sharply from mid-90% utilisation rates of 2016 through 2022 while Warner Bros. Discovery reported 91% occupancy across its Burbank stages in 2025 and cut the ribbon on Ranch Lot Studios, a nearly 1-million-square-foot campus with 16 new soundstages, the UK film and high-end TV production spending rose 30% to GBP 5.6 billion in 2024 per British Film Institute reporting, Hackman Capital Partners defaulted on a USD 1.1 billion mortgage tied to the historic Radford Studio Center in Studio City ceding the 55-acre property to lenders led by Goldman Sachs in January 2026, Hudson Pacific Properties posted trailing 12-month studio occupancy of approximately 67% at year-end 2025 reporting nine-figure annual losses for three straight years, the global virtual production market valued at USD 2.84 billion in 2025 is projected to reach USD 12.25 billion by 2033 at a 20.4% CAGR per FilmLA Sound Stage Production Report 2026 and MESA, and Japan's anime market generated approximately ¥1.3 trillion (USD 8.7 billion) in 2024 with overseas revenue approaching 50% per the Association of Japanese Animations confirming that global film studio and media production real estate is undergoing the most structurally consequential supply-demand rebalancing in its modern history.

| Standard License: USD 7,500 | Enterprise License: USD 10,500 |

MARKET SYNOPSIS

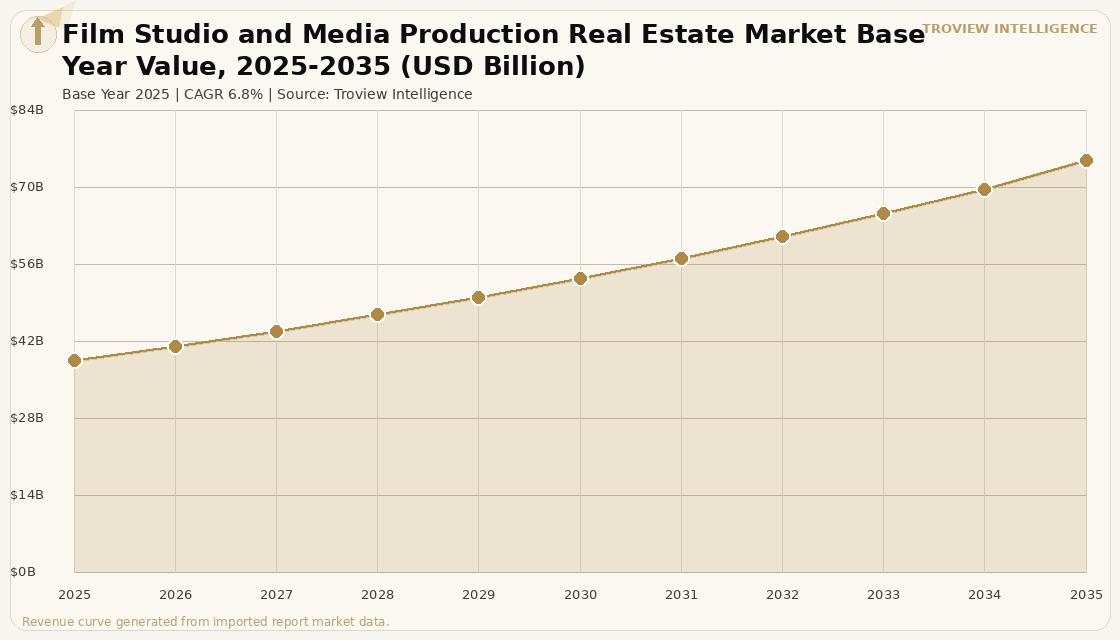

The global film studio and media production real estate market size was USD 38.47 Billion in 2025 and is expected to register a revenue CAGR of 6.8% during the forecast period, reaching USD 74.82 Billion by 2035. The 2025 market estimate is grounded in verified facility and transaction data: Los Angeles County maintains 8.3 million square feet of certified and uncertified soundstage space per FilmLA's eighth annual Sound Stage Production Report released March 18, 2026, with Warner Bros. Discovery's Ranch Lot Studios adding nearly 1 million square feet of new studio campus space in 2026 after reporting 91% occupancy across its Burbank stages in 2025; UK film and high-end TV production spending rose 30% to GBP 5.6 billion in 2024 per British Film Institute data, driving sustained investment in UK studio infrastructure at Pinewood, Shepperton, and NFTS-affiliated facilities; and Japan's anime market generating approximately JPY 1.3 trillion (USD 8.7 billion) in 2024 with overseas revenue approaching 50% per the Association of Japanese Animations, establishing dedicated anime studio real estate as one of the fastest-growing categories within the global media production facility market. The market encompasses the total investible real estate value of dedicated film and television production campuses, soundstage facilities, post-production and editing suites, virtual production LED volume stages, animation studio campuses, and associated production support infrastructure owned by major studios, independent operators, REITs, and institutional real estate investors. Market revenue growth is supported by the global proliferation of streaming platform content investment, with Netflix surpassing 301 million global subscribers and investing approximately USD 16 billion in original content production in 2024, generating sustained demand for production facility capacity across preferred shooting locations including the United States, United Kingdom, Canada, South Korea, Japan, and incentive-rich European jurisdictions. For instance, in 2026 year-to-date, Warner Bros. Discovery, United States, cut the ribbon on Ranch Lot Studios, a nearly 1-million-square-foot campus featuring 16 new soundstages, extensive production offices, a massive construction workshop, and high-end support facilities in the Los Angeles area, already locking in commitments from several tax-credit-qualified productions including Euphoria, Latitude, The Comeback, and I Love LA, demonstrating that vertically integrated studios with captive content pipelines can achieve near-full occupancy even in a broader Los Angeles market averaging only 62% per FilmLA. These are some of the key factors driving revenue growth of the market.

The virtual production market encompassing LED volume stages, real-time rendering infrastructure, in-camera visual effects studios, and associated technology infrastructure generated USD 2.84 billion in revenue in 2025 and is projected to reach USD 12.25 billion by 2033 at a CAGR of 20.4% per FilmLA Sound Stage Production Report 2026 virtual production studio data, representing the fastest-growing facility category within the broader film studio and media production real estate market as productions across streaming, theatrical, and advertising sectors invest in purpose-built virtual production infrastructure that combines the creative flexibility of computer-generated environments with the production quality of physical set photography. The UK film and television production spending increase of 30% to GBP 5.6 billion in 2024 per British Film Institute analysis reflects the sustained advantage of the UK's 25% Audio-Visual Expenditure Credit tax relief structure, the concentration of world-class studio infrastructure at Pinewood, Shepperton, and the Belfast and Welsh studio campuses, and the bilingual crew infrastructure that makes the UK the primary non-US English-language production destination for Hollywood studios and streaming platforms. South Korea's cultural exports including films, dramas, and music totalled USD 9.85 billion representing 1.4% of total goods exports per Korea Creative Content Agency (KOCCA) 2024 Export Statistics, establishing Korea as a major media production real estate investment destination for domestic and international streaming platforms including Netflix, which produces substantial Korean original content. These are some of the key factors driving revenue growth of the market.

However, the global film studio and media production real estate market faces structural constraints that temper revenue and occupancy growth across the forecast period. The post-2022 content spending correction by major streaming platforms with Netflix, Amazon, and Disney+ each reducing their content spend growth rates following the pandemic-era content arms race has created the most significant studio occupancy correction since the advent of streaming, with Los Angeles County average soundstage occupancy falling from mid-90% utilisation rates during 2016 through 2022 to 62% in H1 2025 per FilmLA, with independent and REIT-owned operators bearing a disproportionate share of the occupancy decline relative to vertically integrated studio majors with captive content pipelines. The Hackman Capital Partners default on a USD 1.1 billion mortgage tied to the Radford Studio Center in January 2026 in which revenue covered only approximately 21% of debt service amid below-average occupancy illustrates the severity of the leveraged independent studio real estate model's exposure to the content spending correction when operating income cannot service acquisition-era debt costs. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, affect film studio and media production real estate through their indirect impact on energy costs for 24-hour production facility operations, as large soundstage facilities, LED volume stages, and post-production server infrastructure require continuous power at energy intensities substantially above conventional commercial real estate, creating operating cost exposure that directly affects studio facility operators' net operating income and lender debt service coverage calculations. These factors substantially limit global film studio and media production real estate market growth over the forecast period.

The Los Angeles studio real estate market in 2025 is a story of two markets operating simultaneously in the same geography. Warner Bros. Discovery, running at 91% occupancy with 50 soundstages and a new nearly 1-million-square-foot campus already pre-committed to four productions, is not in the same market as a leveraged independent landlord defaulting on a USD 1.1 billion mortgage because revenue covers only 21% of debt service. They happen to be in the same city. They are not in the same business. The vertically integrated studios WBD, Universal, Disney, Sony, Paramount never needed the real estate markets to clear. They needed their own content pipelines to fill their own stages. Independent studio real estate worked only when the streaming platforms were expanding their content spend at 30% to 40% annually. When Netflix, Amazon, and Apple cut their production growth rates, independent studio landlords went from 95% utilisation to 62% without a single macro event triggering the change. The correction is structural. The recovery will be gradual. The winners over the next decade are the studios with the deepest IP libraries, the most captive content pipelines, and the most cost-effective facilities not the most highly leveraged independent stage operators." Troview Intelligence Head of Global Film Studio and Media Production Real Estate Research

SEGMENT INSIGHTS

Four Regions Defining Global Film Studio Real Estate Investment

| LA County Soundstage Space | LA Average Occupancy H1 2025 | WBD Burbank Occupancy 2025 | Hackman Default Jan 2026 |

| 8.3 million sqft (FilmLA Mar 2026) | 62% down from 95%+ in 2016-2022 | 91% captive pipeline outperforms market | USD 1.1 billion Radford Studio Center mortgage |

North America's film studio and media production real estate market is experiencing the most severe occupancy correction in its modern history, with Los Angeles County average soundstage occupancy at 62% in H1 2025 per FilmLA's eighth annual Sound Stage Production Report down from the mid-90% utilisation rates of 2016 through 2022 reflecting the simultaneous impact of the dual Hollywood writers' and actors' strikes of 2023, the post-pandemic streaming platform content spending correction, major studio consolidation activity, and intensifying international competition from the UK, Canadian, and European studio markets that have systematically expanded their stage inventories over the past five years while offering richer tax incentives and faster permitting. Warner Bros. Discovery's Ranch Lot Studios opening in early 2026 with 16 new soundstages and nearly 1 million square feet of studio campus space pre-committed across several tax-credit-qualified productions and WBD's 91% Burbank occupancy in 2025 confirm that the vertically integrated studio major model is structurally outperforming the independent studio landlord model that led to Hackman Capital Partners' USD 1.1 billion mortgage default on the Radford Studio Center in January 2026 per World Property Journal reporting.

EUROPE UK GBP 5.6B PRODUCTION SPENDING +30%, PINEWOOD, VIRTUAL PRODUCTION

| UK Film+HETV Production 2024 | UK Tax Relief | Key Facilities | Virtual Production |

| GBP 5.6 Billion (+30% YoY, British Film Institute) | 25% Audio-Visual Expenditure Credit | Pinewood, Shepperton, Belfast Titanic Studios, Wolf Studios Wales | Rapidly expanding LED volume stage capacity UK-wide |

Europe's film studio and media production real estate market, anchored by the United Kingdom's world-class production infrastructure and the 25% Audio-Visual Expenditure Credit tax relief structure, recorded GBP 5.6 billion in film and high-end TV production spending in 2024, up 30% year-on-year per British Film Institute analysis, confirming the UK as the primary destination for major studio and streaming platform production outside the United States. Pinewood Studios and Shepperton Studios consolidated under the Pinewood Group constitute the UK's most strategically important studio real estate, hosting productions from the James Bond franchise, Star Wars, and multiple major streaming platform series that require both traditional soundstage and increasingly virtual production LED volume infrastructure. Virtual production LED volume stage investment across the UK is expanding at rates significantly above the traditional soundstage market, with new virtual production facilities opening across London, the Midlands, and Scotland to serve the growing demand from productions that want the creative flexibility of virtual environments without the logistical complexity of building separate digital post-production pipelines.

| Japan Anime Market 2024 | Korea Cultural Exports 2024 | Streaming Anime Investment 2025 | India Films 2024 |

| JPY 1.3T (USD 8.7B), overseas ~50% (AJA) | USD 9.85 Billion 1.4% of total goods exports | USD 2.5 Billion+ (platforms including Netflix, Prime) | 1,800+ films released, 9,927 screens nationwide |

Asia Pacific's film studio and media production real estate market is the fastest-growing region globally, anchored by Japan's dominant anime studio infrastructure in Tokyo, South Korea's K-drama and film production ecosystem that generated USD 9.85 billion in cultural exports in 2024 representing 1.4% of total goods exports per KOCCA 2024 Export Statistics and South Korea Ministry of Culture, Sports and Tourism, and India's extraordinary production volume of 1,800-plus films in 2024 released across 9,927 screens nationwide per Producers Guild of India and Ministry of Information and Broadcasting 2024 data. Global streaming platforms invested over USD 2.5 billion in anime acquisition in 2025 per Vitrina.ai analysis of the Japanese anime studio landscape, creating unprecedented demand for the animation studio production real estate in Tokyo's Suginami, Nerima, Setagaya, and Musashino districts that houses MAPPA, Toei Animation, Wit Studio, Production I.G, and the other major anime studios whose facilities are committed 18 to 24 months in advance. South Korea's production infrastructure in Seoul's Sangam DMC (Digital Media City) and Gyeonggi Province studio complexes hosts the drama and film productions that have generated the global K-content phenomenon.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from FilmLA Sound Stage Production Report 2026, World Property Journal, British Film Institute, Association of Japanese Animations (AJA), FilmLA Sound Stage Production Report 2026, and verified trade press.