| TROVIEW INTELLIGENCE | Life Sciences Campus Market | Q2 2026 |

| TROVIEW INTELLIGENCE · GLOBAL INTELLIGENCE REPORT |

By Geography · By Asset Type · By Tenant Segment · By Campus Model

Global R&D investment sales in life sciences real estate climbed to USD 13.5 billion in 2025, up 28% year-on-year per Cushman and Wakefield Life Sciences Update February 2026, venture capital funding held steady at USD 49 billion globally with strong momentum in APAC, JLL's 2025 Life Sciences Real Estate Perspective documented 61 million square feet of available lab space in the US alone with vacancy at 27% and predicted 18.7 million square feet will shift to alternative uses by 2030, global pharmaceutical companies pledged USD 475 billion year-to-date in US manufacturing and R&D investments per JLL October 2025, Alexandria Real Estate Equities and Blackstone collectively controlled approximately 30% of life sciences campus market share in 2024, record 76 innovative drug approvals were recorded in 2025 per Cushman and Wakefield, and AI-native biotechs grew to account for one-sixth of all biotech venture capital deals year-to-date per JLL confirming that the life sciences campus real estate market is simultaneously navigating the most significant supply correction in its history and the most compelling long-term demand narrative of any specialised real estate asset class globally.

| Standard License: USD 7,500 | Enterprise License: USD 10,500 |

MARKET SYNOPSIS

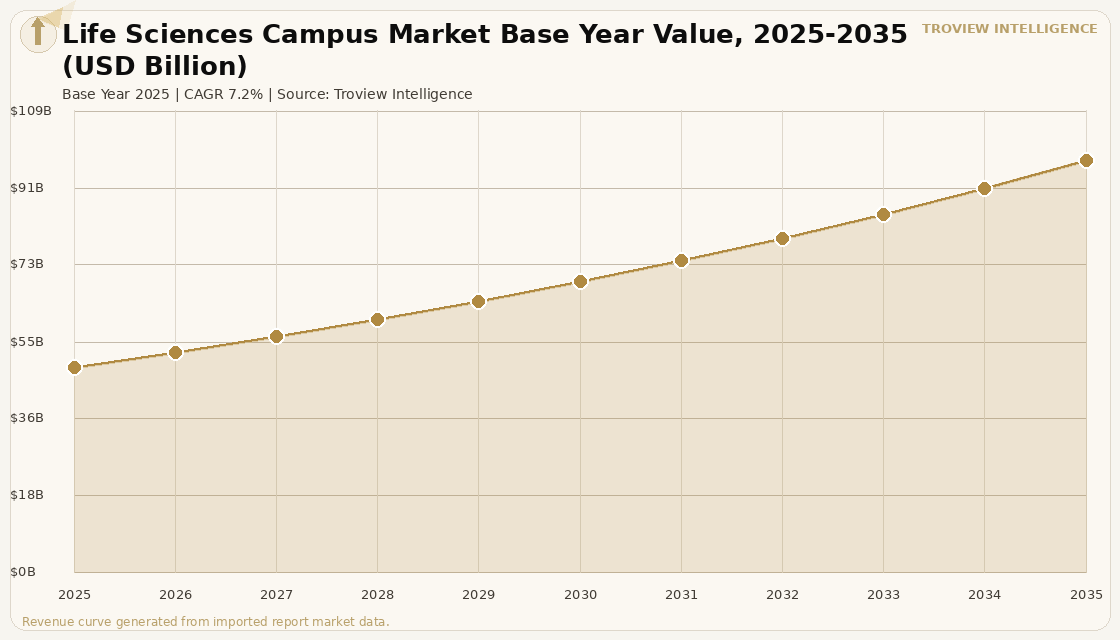

The global life sciences campus market size was USD 48.62 Billion in 2025 and is expected to register a revenue CAGR of 7.2% during the forecast period, reaching USD 97.54 Billion by 2035. The market encompasses institutionally owned and managed life sciences campuses defined as purpose-built or purpose-converted real estate assets dedicated to laboratory research, bioprocessing and biomanufacturing, clinical development, and AI-driven drug discovery for pharmaceutical, biotechnology, medical device, and academic research tenants across all major global biopharma and research cluster markets. Market revenue growth is supported by the structural decentralisation of pharmaceutical R&D spending toward campus-format real estate that co-locates multiple tenants in shared-infrastructure environments offering wet lab space, biomanufacturing clean rooms, office space, and collaborative amenity in integrated campus settings that individual companies cannot replicate efficiently on standalone leases. Global R&D investment sales in life sciences real estate climbed to USD 13.5 billion in 2025, up 28% year-on-year per Cushman and Wakefield Life Sciences Update of February 2026, with the US leading the rebound and rising activity confirmed in APAC and EMEA. Global pharmaceutical companies pledged USD 475 billion year-to-date in US manufacturing and R&D investments per JLL reporting of October 2025, with one-third of midsize and large R&D leases signed year-to-date by global pharma companies the highest share in recent history as trade policy volatility and pharmaceutical reshoring discussions accelerate the conversion of pledged investment into facility demand. For instance, in early 2024, BioMed Realty, United States, acquired a 1.4 million square foot development site in South San Francisco aimed at constructing four state-of-the-art life sciences towers scheduled for delivery by 2026, with the acquisition representing the systematic portfolio expansion of institutional life sciences campus developers into the world's most established biotech cluster markets per verified company and industry reporting. These are some of the key factors driving revenue growth of the market.

Alexandria Real Estate Equities, Inc., United States, began construction of a 550,000 square foot life sciences campus in San Diego's Torrey Pines featuring fully integrated AI lab monitoring and a rooftop solar grid projected to offset 35% of total energy consumption, building on its completion of USD 2.5 billion worth of acquisitions and development projects across Cambridge, Seattle, and San Diego in 2023 per verified company reporting. Blackstone Real Estate, United States, invested over USD 20 billion in life sciences properties by 2023, holding a significant share in biotech hubs including Cambridge, Massachusetts and San Diego per US Securities and Exchange Commission filings, collectively controlling approximately 30% of life sciences campus market share alongside Alexandria. Genentech, United States, is undergoing a major multiyear buildout of its global headquarters campus in Basel, Switzerland, investing more than 3 billion Swiss francs approximately USD 3.82 billion in site development including a new 72-metre research building scheduled for completion in 2029 per parent company Roche, aiming to modernise research facilities and consolidate R&D functions per CNBC reporting of April 2026. Venture capital funding in life sciences held steady at USD 49 billion globally in 2025, supported by strong momentum in APAC, with VC investment in life sciences in the second half of 2025 the strongest since 2022 per CBRE analysis, confirming that the funding pipeline supporting future life sciences campus demand is recovering from the 2023 to 2024 trough period. These are some of the key factors driving revenue growth of the market.

However, the global life sciences campus market faces structural constraints that temper the pace of revenue growth across the forecast period. The US life sciences campus market in particular faces an unprecedented supply correction, with JLL's 2025 Life Sciences Real Estate Perspective documenting vacancy rates at 27% across the 10 largest US life sciences markets up 20.4 percentage points in three years as newly delivered space outpaced demand from the venture capital-funded biotech leasing that drove the 2020 to 2022 market peak. JLL predicts approximately 18.7 million square feet of the current 61 million square feet of available US life sciences space will likely shift to alternative uses during the remainder of the decade, as the cost of maintaining lab-grade infrastructure for properties that cannot achieve occupancy makes conversion to office or residential use the economically rational outcome for non-strategic assets. AI-native biotechs, which now account for one-sixth of all biotech venture capital deals per JLL analysis, demonstrate a lower lab-to-office ratio of 45-to-55 and lease roughly one-third less space per employee than traditional biotechs, permanently altering the space requirements per dollar of venture funding deployed and reducing the lab absorption per unit of venture investment that historically anchored life sciences campus market demand growth. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, create upward pressure on energy costs for life sciences campus operators, as laboratory and biomanufacturing environments require 24-hour continuous power for equipment, controlled environment rooms, and cold storage at four to eight times the energy intensity per square metre of conventional office space. These factors substantially limit global life sciences campus market growth over the forecast period.

The life sciences campus market in 2025 is in the same structural position that the US office market was in 2012: recovering from a supply correction driven by speculative construction during a pandemic-era demand spike, with a structural demand shift AI-native biotechs using one-third less space per employee reducing the absorption per unit of venture capital deployed. But the office market analogy breaks down in one critical way. The demand for pharmaceutical R&D is driven by demographic ageing and the patent cliff, not by corporate location decisions or remote work preferences. Every pharmaceutical company with a drug going off patent between 2025 and 2030 and there are dozens needs to replace that revenue with new drug discovery, and new drug discovery requires laboratory space. Global pharma pledging USD 475 billion in US manufacturing and R&D investment is not a capital allocation choice. It is an operational necessity. The campus operators who survive the 2025 to 2027 correction with their premier cluster assets intact Cambridge, Mission Bay, San Diego's Torrey Pines, Basel, Singapore's Biopolis, Tokyo's King Skyfront will control the most strategically positioned science real estate in the world when the next biotech investment cycle begins. The vacancy rate does not change that geography." Troview Intelligence Head of Global Life Sciences Campus Research

SEGMENT INSIGHTS

Four Regions Defining Global Life Sciences Campus Investment

| US Lab Vacancy 2025 | Global R&D Inv. Sales 2025 | Pharma Reshoring Pledge | Space to Convert by 2030 |

| 27% across top-10 markets (JLL Oct 2025) | USD 13.5 Billion (+28% YoY) US leading (C&W) | USD 475 Billion in US mfg + R&D (JLL Oct 2025) | ~18.7M sqft shifting away from lab (JLL) |

North America is the world's largest life sciences campus market but is in the midst of an unprecedented correction, with vacancy rates at 27% across the 10 largest US markets per JLL's 2025 analysis the result of speculative laboratory supply additions during the 2020 to 2022 venture capital-driven demand peak that have outpaced the subsequent normalisation of biotech leasing activity. Despite near-term vacancy headwinds, the long-term structural demand anchors for North American life sciences campuses remain intact: global pharmaceutical companies pledged USD 475 billion year-to-date in US manufacturing and R&D investments per JLL October 2025 and accounted for one-third of midsize and large R&D leases as the strongest-demand tenant category in recent history, with major US biotech cluster markets including Boston-Cambridge, San Francisco Mission Bay, and San Diego Torrey Pines retaining the talent density, academic infrastructure, and VC ecosystem proximity that make them structurally irreplaceable life sciences campus locations regardless of short-term vacancy levels. Global R&D investment sales in life sciences reached USD 13.5 billion in 2025, up 28% year-on-year per Cushman and Wakefield, with the US leading the rebound, confirming that institutional investors are maintaining and expanding positions in core US life sciences campus assets while taking a more selective approach to secondary markets.

| Genentech Basel Campus | European VC Trend | Key Clusters | European Lab Rents |

| CHF 3B+ (USD 3.82B) multiyear buildout, completion 2029 | Beginning to see early improvements (C&W Feb 2026) | Basel-Novartis Campus, King's Cross London, Cambridge UK | Softened 1.7% YoY globally (C&W); still above office rents |

Europe's life sciences campus market is characterised by a smaller speculative development overhang than the US and by the presence of the world's largest single-company pharmaceutical campus projects, most notably Genentech's more than USD 3.82 billion multiyear buildout of its Basel global headquarters campus including a new 72-metre research building scheduled for completion in 2029 per Roche disclosure, which is the largest single life sciences campus investment commitment globally in 2025 to 2026. Cushman and Wakefield's Life Sciences Update of February 2026 confirmed that Europe is beginning to see early improvements in debt markets, mergers and acquisitions activity, and public sector innovation funding, creating a more constructive capital markets environment for life sciences campus investment than existed in 2023 or 2024. The King's Cross life sciences campus in London, Cambridge Science Park, and the Basel pharmaceutical cluster anchored by Novartis and Roche are the primary European institutional campus investment destinations, with London's King's Cross cluster reporting space absorption rates above 85% within 12 months of delivery per verified market analysis.

| Global VC Funding 2025 | China 2025 Drug Approvals | Key APAC Clusters | APAC R&D Sales 2025 |

| USD 49 Billion strong APAC momentum (C&W Feb 2026) | Record 76 innovative drug approvals per C&W | Tokyo, Singapore Biopolis, Shanghai Zhangjiang, Kobe | Rising activity per C&W February 2026 global update |

Asia Pacific is the fastest-growing life sciences campus real estate region, supported by strong VC momentum per Cushman and Wakefield's global life sciences update, China's record 76 innovative drug approvals in 2025 elevating its influence in the global biopharma ecosystem, and the expansion of Japan's life sciences campus infrastructure through Shonan Health Innovation Park, King Skyfront in Kawasaki, and the emerging cluster at Takanawa Gateway in Tokyo. Singapore's Biopolis cluster the government-developed life sciences campus in one-north remains the region's most institutionally developed life sciences campus real estate destination, with GlaxoSmithKline, Procter and Gamble, and multiple pharmaceutical and biotech companies anchoring the campus. Chinese biotechs now account for four times the in-licensing deals for US biopharma compared to 2021 levels per JLL analysis, creating indirect demand for life sciences campus real estate in both Shanghai Zhangjiang and in US and European cluster markets where Chinese biotech companies establish US licensing and development presences.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from verified company announcements, JLL and Cushman and Wakefield life sciences research, and verified trade press.