By Zone - By Operator - By Facility Type - By Demand Driver

Zones: Central Congestion Zone - Inner London - Heathrow Corridor - Canary Wharf - Outer Borough Hubs

London's Congestion Charge rose to GBP 18 per day from 2 January 2026 with the Cleaner Vehicle Discount ending 25 December 2025 and EVs now paying GBP 13.50 via Auto Pay, TfL estimates the changes reduce approximately 2,200 vehicles daily entering the CCZ, the ULEZ operates 24/7 across all 33 London boroughs with EVs permanently exempt, NCP operates the largest London car park network with EV charging on a first-come-first-served basis, EV registrations for the CVD grew from 20,000 in 2019 to over 112,000 by June 2024 a 460% increase, Westminster's car park charging shifted to emissions-based pricing in 2024, and APCOA installed 1,000 EV chargers across Network Rail car parks serving London commuters.

MARKET SYNOPSIS

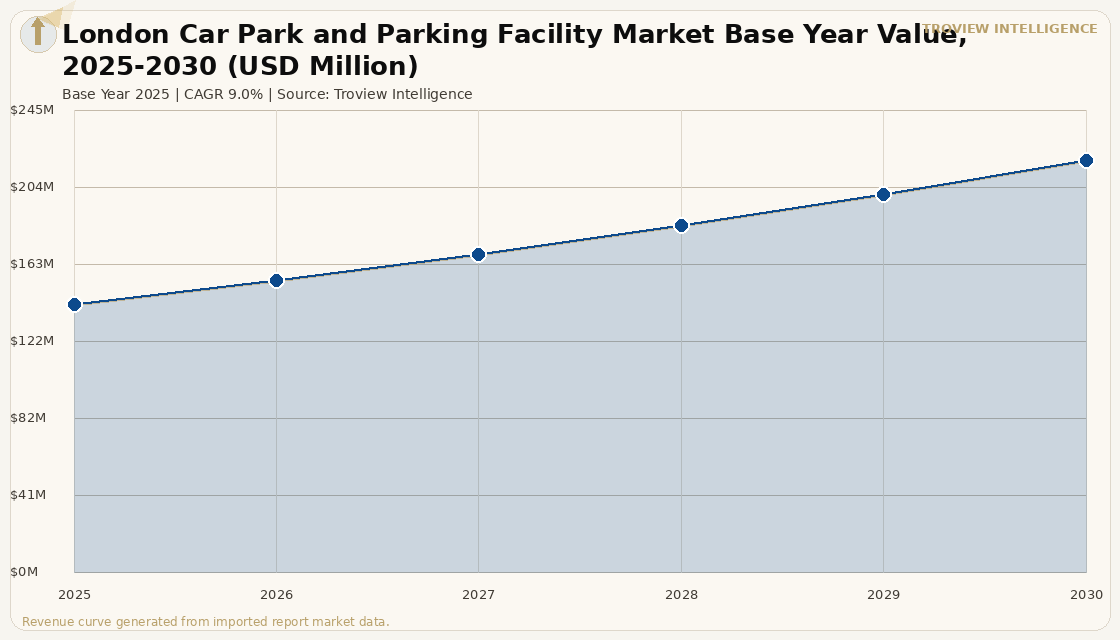

The London car park and parking facility market size was USD 142.18 Million in 2025 and is expected to register a revenue CAGR of 9.0% during the forecast period, reaching USD 218.64 Million by 2030. London is the UK's dominant car park and parking facility market, hosting the greatest concentration of managed multi-storey car parks, high-tariff central area surface car parks, on-street parking management zones, transport hub parking, and airport parking complexes in the country, generating the highest absolute parking revenue per capita of any UK city through the combination of scarcity-driven pricing, high transient demand from business and leisure visitors, and the regulatory cost architecture Congestion Charge and ULEZ that concentrates vehicle demand into managed off-street facilities rather than unmanaged on-street kerb space. The Congestion Charge in central London rose from GBP 15 to GBP 18 per day from 2 January 2026, simultaneously ending the Cleaner Vehicle Discount for electric vehicles on 25 December 2025 with EVs now paying a reduced charge of GBP 13.50 per day when registered on Auto Pay (a 25% reduction against the full GBP 18 charge for petrol and diesel vehicles) per The Electric Car Scheme verified guidance. Transport for London estimated that the combined changes would reduce approximately 2,200 vehicles per day from entering the Congestion Charge Zone, a volume reduction that partially offsets the average daily tariff increase for the remaining vehicle population and has net revenue implications for car park operators within the CCZ catchment. For instance, the Cleaner Vehicle Discount registrations grew from approximately 20,000 vehicles in 2019 to over 112,000 by June 2024 a more than 460% increase over five years confirming the rapid growth of EV penetration in the London vehicle fleet that has made the CVD revision both financially necessary for TfL and operationally significant for NCP, APCOA, Q-Park, and other London car park operators whose EV-specific charging bays and pricing policies must now be adjusted to reflect the changed cost calculus for EV drivers. These are some of the key factors driving revenue growth of the market.

London's car park market is defined by extreme geographic and tariff stratification: central London Congestion Charge Zone car parks in Westminster, the City of London, and Southbank command the highest per-hour and per-day tariff rates of any UK car park geography, with premium locations in Mayfair, Covent Garden, and the City generating revenue yields that justify significant capital investment in EV charging infrastructure and smart parking technology upgrades. The ULEZ expansion across all 33 London boroughs in August 2023 which operates 24 hours a day and seven days a week with electric vehicles permanently exempt from ULEZ charges per TfL and Pod Point verified guidance has reshaped the demand profile of car parks in outer London boroughs, where pre-ULEZ expansion non-compliant vehicle owners who previously drove to inner London car parks are now electing to park at outer-borough park-and-ride interchanges to avoid the GBP 12.50 daily ULEZ charge that applies to non-compliant petrol and diesel vehicles across the expanded zone. Westminster Council's transition to emissions-based parking pricing in 2024 replacing the zero-cost or reduced-cost EV kerbside parking that had previously applied creates an additional pricing rationalisation in London's most valuable on-street parking geography that removes the last remaining cost advantage for EV drivers using surface-level Westminster parking space.

However, the London car park and parking facility market faces structural constraints that limit revenue growth and capacity investment. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy cost inflation that increases the operating costs of London multi-storey car parks whose electricity consumption for continuous LED lighting in enclosed structures, mechanical ventilation systems required by building regulations, lift and escalator systems, ANPR camera and sensor networks, and the rapidly expanding EV charging point networks is significantly higher per square metre than equivalent surface-level commercial properties. The sustained transition toward hybrid working patterns among London's office worker population which concentrated 5-day-per-week commuter parking demand into London city centre car parks has structurally reduced the reliability and volume of Monday-to-Friday weekday car park utilisation, with operators unable to recover the season ticket revenue base that was lost when employers shifted to 2-to-3-day office attendance patterns following the pandemic. The end of the EV Cleaner Vehicle Discount on 25 December 2025 while broadly expected and given 7.5 years of advance notice per TfL removes an incentive structure that had been directing EV drivers into central London car parks at zero-cost charge entry, and may modestly reduce the fastest-growing segment of London's driving population from entering the Congestion Charge Zone, with secondary effects on car park demand within the CCZ footprint. These factors substantially limit London car park and parking facility market growth over the forecast period.

TROVIEW ANALYST PERSPECTIVE "London's car park market in 2026 is navigating four simultaneous regime changes. First, the Congestion Charge increase to GBP 18 and CVD removal: this will modestly reduce CCZ vehicle entry volume, but London's car parks will capture a larger share of a pricing-inelastic demand base the workers, shoppers, and visitors who will pay GBP 18 to enter because their purpose-of-journey requires central London presence. Second, the ULEZ's 33-borough expansion is a structural demand redistribution toward outer London park-and-ride rather than inner London car parks. Third, the hybrid working shift has permanently impaired the weekday season ticket revenue that historically subsidised night and weekend underutilisation. Fourth, EV charging infrastructure is creating a genuine second revenue stream for car park operators who have the capital to install it NCP and APCOA are leading this but the charging revenue economics only become compelling at scale with smart load management and eventually V2G capability. The operators who come through this period strongest are those with diversified revenue across zones, good EV charging penetration across their estate, and dynamic pricing capability to respond to the daily volatility of London's demand environment." Troview Intelligence Senior Analyst, London Car Park and Parking Facility Markets

SEGMENT INSIGHTS

Zone Deep-Dives

| Congestion Charge (Jan 2026) | EV Rate (Auto Pay) | Primary Operators | Daily Car Park Tariff Range |

| GBP 18/day (GBP 15 until Dec 2025) | GBP 13.50 (25% discount) | NCP, Q-Park, APCOA, Euro Car Parks | GBP 25-60/day (Westminster, City, WC1/WC2) |

The Central Congestion Charge Zone covering Westminster, the City of London, Southwark, and the West End is London's highest-tariff car park geography, hosting the most intensively managed and highest-revenue car parks in the UK, with NCP operating the most extensive central London network and Q-Park and Euro Car Parks providing competing managed off-street car park capacity across major retail and office districts. Daily car park tariff rates in prime central London locations including the West End, Mayfair, and the City range from GBP 25 to GBP 60 per day depending on location, facility quality, and advance booking discount, generating the revenue intensity that justifies EV charging infrastructure investment and the sophisticated dynamic pricing software that adjusts rates in response to real-time occupancy and event-driven demand spikes. The Congestion Charge increase to GBP 18 per day from 2 January 2026 following the end of the Cleaner Vehicle Discount on 25 December 2025 with EVs retaining a 25% Auto Pay discount at GBP 13.50 per day per The Electric Car Scheme verified guidance adds a fixed cost of entry that discourages discretionary vehicle journeys into the CCZ but leaves the purpose-of-journey inelastic demand from workers, scheduled deliveries, and committed visitors largely unaffected, sustaining CCZ car park occupancy at levels that operators had managed through the prior GBP 15 regime with steady demand.

Heathrow Corridor and Surrounding Airports UK'S BUSIEST AIRPORT, MULTI-DAY PARKING, NCP AND APCOA, MEET-AND-GREET

| Heathrow Annual Passengers | Key Operators | Revenue Characteristic | Zone Coverage |

| ~79 million annually UK's busiest airport | NCP, APCOA, JustPark, independent M&G | Multi-day premium highest revenue/transaction | Heathrow Terminals 2-5 + off-airport Hounslow |

The Heathrow Corridor is London's highest-revenue-per-parking-transaction car park zone, with the airport's approximately 79 million annual passengers generating multi-day pre-booked parking demand at official terminal car parks and competing off-airport facilities that creates the most visible dynamic pricing environment in the London parking market, where official NCP-managed terminal parking and third-party off-airport competitors including JustPark, APCOA, and independent meet-and-greet operators compete on price, convenience, and shuttle frequency. Official terminal car parks at Heathrow command significant daily premiums for guaranteed covered proximity parking, while off-airport facilities in Hounslow, West Drayton, and Slough offer price-competitive alternatives with shuttle transfers that serve the cost-sensitive leisure traveller segment who prioritise parking cost savings over terminal proximity. The shift in Heathrow passenger profile toward higher proportions of international long-haul travellers who park for 7 to 14 days on average generates significantly higher revenue per parking event than short-haul European travellers who park for 1 to 3 days, creating an ongoing revenue mix management challenge for operators who must yield-manage across very different duration profiles within the same multi-storey facility.

Canary Wharf and East London FINANCIAL DISTRICT, CROSSRAIL IMPACT, EV CHARGING, HYBRID WORKING IMPACT

| Key Demand Base | Crossrail (Elizabeth Line) Effect | EV Charging Provision | Hybrid Working Impact |

| Financial services professionals, Canary Wharf Group | Reduced weekday car demand since 2022 opening | Q-Park and NCP Canary Wharf with EV points | 2-3 day office attendance reduces season ticket base |

Canary Wharf and East London constitute London's financial district car park market, serving the major banking, financial services, and professional services employer base concentrated in the Canary Wharf estate Barclays, HSBC, Citi, JP Morgan, and Clifford Chance as well as the emerging technology and creative sector concentration in Shoreditch, Whitechapel, and the Olympic Park. Canary Wharf Group operates its own car park estate within the Canary Wharf development, supplemented by Q-Park and NCP facilities that serve both estate tenants and visitors. The opening of the Crossrail Elizabeth Line in 2022 connecting Canary Wharf to central London Paddington in approximately 7 minutes and to Heathrow in approximately 45 minutes has fundamentally shifted the modal choice calculus for Canary Wharf commuters who previously drove and parked, with the improved public transport connectivity reducing weekday car park demand at a time when hybrid working had already reduced the frequency of office attendance. Q-Park and NCP Canary Wharf facilities have responded by installing EV charging points to serve the growing fleet of EVs among the high-income financial services workforce, creating incremental charging revenue alongside the reduced parking tariff revenue from the lower weekday occupancy environment.