| TROVIEW INTELLIGENCE | Timberland and Forestry Real Estate Market | Q2 2026 |

By Geography - By Asset Class - By Investment Vehicle - By Revenue Stream

The global forestry market size was valued at USD 14,786 Million in 2025, FAO confirms forests cover approximately 4.06 Billion hectares representing 31% of Earth's total land area, Weyerhaeuser acquired 117,000 acres of timberland in North Carolina and Virginia for USD 375 Million in May 2025 bringing its total timberland acquisitions since early 2022 to over USD 1.10 Billion, Weyerhaeuser generated USD 7.10 Billion in net sales and manages approximately 10.4 Million acres of forest worldwide in 2024, NCREIF Timberland Index values have increased at a CAGR of 6.8% since 2021, the global timber construction market was valued at USD 16.13 Billion in 2024 growing at a CAGR of 9.6% to USD 36.49 Billion by 2033, and the Government of Canada launched USD 500 Million in support for retooling Canada's forest sector in February 2026.

MARKET SYNOPSIS

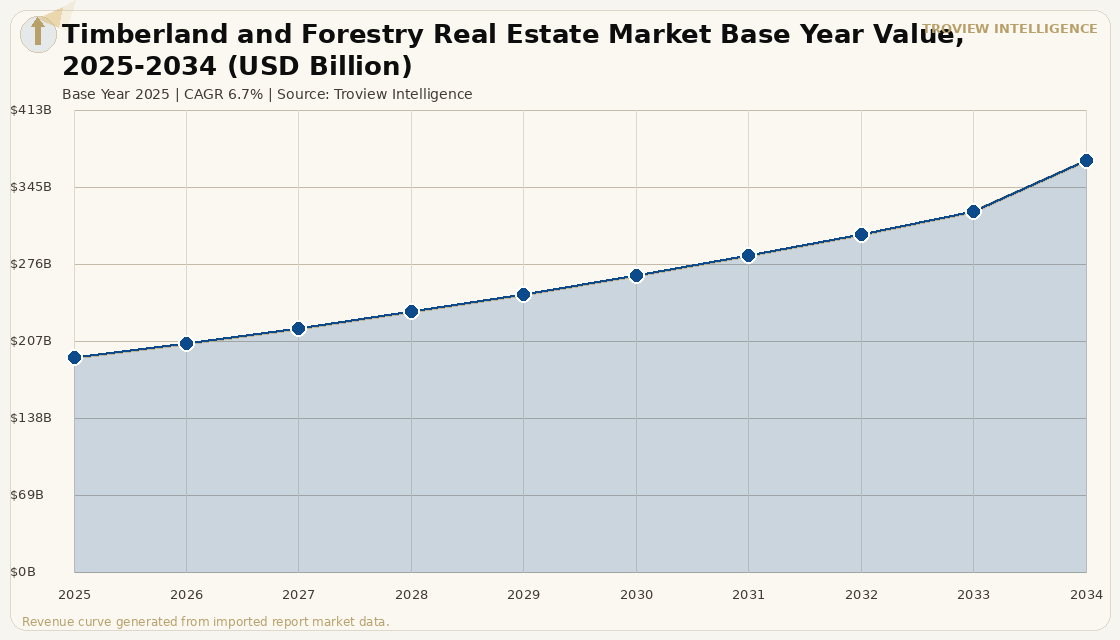

The global timberland and forestry real estate market size was USD 192.46 Billion in 2025 and is expected to register a revenue CAGR of 6.7% during the forecast period, reaching USD 369.14 Billion by 2034. The timberland and forestry real estate market encompasses the ownership, acquisition, management, and investment in forested land assets for timber production, carbon credit generation, conservation easements, mass timber supply chain development, and biological value accretion from ongoing forest growth. FAO confirms that forests cover approximately 4.06 Billion hectares representing 31% of Earth's total land area, with the area of certified forest worldwide expanding globally as institutional investors demand responsible sourcing certification as a prerequisite for acquisition. NCREIF Timberland Index values have increased at a compound annual rate of 6.8% since 2021 per Forisk verified data, confirming timberland's sustained per-acre value appreciation through the post-pandemic interest rate cycle a cycle that impaired commercial real estate values broadly but left timberland largely insulated due to its biological growth characteristics, carbon revenue optionality, and the inelastic demand from pension funds and endowments seeking hard asset inflation protection. The global timber construction market was valued at USD 16.13 Billion in 2024 and is projected to reach USD 36.49 Billion by 2033 at a CAGR of 9.6% per verified timber construction market data, with engineered wood growing at 10.1% CAGR as cross-laminated timber, glued-laminated timber, and nail-laminated timber increasingly replace concrete and steel in mid-rise and high-rise construction across North America, Europe, and Oceania. The 2025 market estimate is grounded in verified operator revenues and transactions: Weyerhaeuser Company, United States, generated USD 7.10 Billion in net sales in 2024 and manages approximately 10.4 Million acres of forest worldwide, and in May 2025 acquired 117,000 acres of timberland in North Carolina and Virginia for USD 375 Million at a 5.1% free cash flow yield, bringing its total timberland acquisitions since early 2022 to over USD 1.10 Billion per Weyerhaeuser investor relations press release of 22 May 2025. These are some of the key factors driving revenue growth of the market.

North America dominated the global timberland and forestry real estate market in 2024 with a 40.4% share of the global forestry market per Market Data Forecast verified data, driven by the United States' and Canada's extensive forest resources which support the most mature institutional timberland investment market globally. Close to half of all capital placed in timberland globally has come from non-US investors per TimberLink investment consulting survey data, with three-quarters of all timberland valued on a market-weighted basis located in the United States, confirming the country as the world's primary timberland investment destination by both capital allocation and asset quality. Timberland has limited correlations with the performance of stocks, bonds, and real estate per Timberland Investment Resources Europe verified investment attribute data, establishing it as a genuine portfolio diversifier that generates ongoing value accretion through biological tree growth that functions as a warehouse for increasing asset value on the stump until supply, demand, and pricing conditions favour harvest realisation. The carbon credit market is adding a third revenue stream beyond timber sales and biological land appreciation: Weyerhaeuser sold its second issuance of carbon credits from its Maine project in 2024 at a per-credit price slightly above the USD 29.00 per credit received in 2023, with the company's carbon credit pipeline expected to generate a significant increase in credit sales in 2025 per Weyerhaeuser Nareit reporting, while firms including Acadian Timber are monetising carbon sequestration with planned credits totalling 390,000 by mid-2025 at USD 20.00 to USD 30.00 per tonne.

However, the global timberland and forestry real estate market faces structural constraints that limit the pace of institutional investment deployment and revenue realisation. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy and logistics cost inflation that increases timber harvesting, transport, and processing costs in markets where log haul distances are long and diesel-dependent logging and transport equipment represents a significant share of total stumpage-to-mill operating cost. Labour shortages across the global logging and forestry workforce represent a structural constraint on harvest capacity utilisation: the growing scarcity of skilled loggers and machine operators in mature timberland markets including the United States, Canada, and Scandinavia drives up harvesting cost per tonne and limits operators' ability to increase harvest volumes in response to favourable timber pricing, reducing the revenue capture from invested timberland assets during timber price up-cycles. New trade policies and tariffs affecting the global timber supply chain including US lumber tariffs on Canadian softwood lumber that have created persistent trade friction between the world's two largest timber-trading partners introduce pricing volatility into timberland investment return calculations that depends on cross-border lumber trade economics remaining accessible to Canadian and US timberland owners. These factors substantially limit global timberland and forestry real estate market growth over the forecast period.

Timberland is the only real asset class where the asset grows in value while you wait. Trees add biological mass every year regardless of interest rates, capital markets conditions, or macroeconomic cycles. That biological growth means the timberland owner who does not harvest during a poor pricing cycle is not simply waiting the trees are becoming more valuable. Weyerhaeuser's USD 1.10 Billion in strategic timberland acquisitions since 2022 while simultaneously divesting USD 1.10 Billion in non-strategic land is the most sophisticated articulation of this thesis at institutional scale: assembling a portfolio of higher-quality, higher-yield timberland by recycling lower-quality assets, exactly as a core office REIT might recycle secondary buildings to buy trophy assets. The carbon credit layer is now material. Weyerhaeuser's Maine credits clearing USD 29.00 per tonne confirms that carbon monetisation is no longer a theoretical upside it is a current cash flow. And the engineered wood demand driver is multi-decade: the global timber construction market growing at 9.6% CAGR through 2033, with mass timber buildings generating 40% to 70% lower embodied carbon than concrete, is creating structural demand for certified softwood that the timberland asset class is uniquely positioned to supply." Troview Intelligence Head of Global Timberland and Forestry Real Estate Research

SEGMENT INSIGHTS

By Asset Class

Timber tract operations and natural forest management asset class is expected to account for a significantly large revenue share in the global timberland and forestry real estate market during the forecast period.

Based on asset class, the global timberland and forestry real estate market is segmented into timber tract operations and natural forest management, plantation forestry and silviculture-intensive managed forests, mass timber and engineered wood supply chain forestlands, carbon forestry and conservation easements, and mixed-use forestland with energy and natural resource optionality. Timber tract operations dominate the market, with the segment estimated to register a CAGR of 12.6% during the forecast period per Market Data Forecast forestry market data, as institutional investors including pension funds, endowments, and TIMOs focus their capital on long-rotation managed forestlands in the US South, Pacific Northwest, Canada, and Northern Europe where certified sustainable forest management practices and established log marketing infrastructure provide reliable revenue realisation. Carbon forestry and conservation easements are expected to register a rapid revenue growth rate in the global market over the forecast period, as the voluntary carbon credit market for forest-based sequestration scales with per-credit prices at USD 20.00 to USD 30.00 per tonne and climbing as corporate net-zero commitments drive demand for high-quality forest carbon offsets converting previously non-monetised conservation forestlands into income-generating assets that can deliver comparable or superior returns to harvested timberland on a risk-adjusted basis.

By Investment Vehicle

Timberland Investment Management Organisation direct ownership vehicle is expected to account for a significantly large revenue share in the global timberland and forestry real estate market during the forecast period.

Based on investment vehicle, the global timberland and forestry real estate market is segmented into Timberland Investment Management Organisations managing private institutional capital, timber-focused REITs including Weyerhaeuser and Rayonier-PotlatchDeltic, private equity timber funds with defined holding periods, endowment and pension direct ownership programmes, and retail-accessible ETFs and exchange-traded vehicles providing indirect timber exposure. TIMOs dominate institutional timberland capital deployment, as they offer pension funds and endowments the specialist forestry management, log marketing access, and sustainable certification infrastructure that direct ownership programmes cannot replicate without prohibitive internal investment in operational capability. Timber REITs are expected to register a rapid revenue growth rate in the global market over the forecast period, combining the tax efficiency of the REIT structure with the biological growth and carbon credit revenue streams of large-scale timberland portfolios, with the Rayonier and PotlatchDeltic merger completed on 30 January 2026 creating an expanded combined entity with 0.9 million acres including 0.6 million acres in Idaho per Weyerhaeuser public filing data.

By Revenue Stream

Timber harvest and stumpage sales revenue stream is expected to account for a significantly large revenue share in the global timberland and forestry real estate market during the forecast period.

Based on revenue stream, the global timberland and forestry real estate market is segmented into timber harvest and stumpage sales, biological land value appreciation, carbon credit and ecosystem services monetisation, real estate and higher-and-better-use land sales, energy and mineral rights licensing, and recreational and hunting lease income. Timber harvest and stumpage sales dominate near-term timberland cash flows, with well-managed US South pine plantations generating 7.4 tonnes per acre annually at premium productivity levels per Weyerhaeuser verified acquisition data, producing predictable cash flows that institutional investors value for their inflation-tracking and biological growth characteristics. Carbon credit and ecosystem services monetisation is expected to register a rapid revenue growth rate over the forecast period as the voluntary carbon market matures, with forestry-based credits qualifying for corporate Scope 1 and 3 emissions reporting programmes under verified standard registries, and the combination of timber production income and carbon credit income creating a dual-revenue model that improves the risk-adjusted return of timberland investment by reducing dependence on timber price cycles alone.

REGIONAL ANALYSIS

NORTH AMERICA

| North America Forestry Share (2024) | Weyerhaeuser Acquisitions Since 2022 | Weyerhaeuser 2024 Sales | NCREIF Timberland CAGR (Since 2021) |

| 40.4% of global forestry market | Over USD 1.10 Billion / 252,000+ acres | USD 7.10 Billion net sales | 6.8% per-acre value appreciation |

North America is the global timberland and forestry real estate market leader, with the United States hosting the world's most mature institutional timberland investment ecosystem anchored by Weyerhaeuser Company, Rayonier-PotlatchDeltic, and a network of TIMOs including Manulife Investment Management that collectively manage tens of millions of acres of US and Canadian timberland on behalf of pension funds, endowments, and sovereign wealth funds. Weyerhaeuser, operating as a REIT on NYSE under symbol WY, generated USD 7.10 Billion in net sales and employed approximately 9,400 people in 2024 while managing approximately 10.4 Million acres of forest globally per Weyerhaeuser 22 May 2025 press release. The company executed a disciplined portfolio optimisation strategy: acquiring USD 1.10 Billion in strategic timberland purchases across over 252,000 acres primarily in the Carolinas, Mississippi, and Alabama since 2022, while simultaneously divesting approximately USD 1.10 Billion in non-strategic forest land for a net reduction of 680,000 acres improving portfolio quality, productivity, and per-acre cash flow by concentrating holdings in the high-productivity US South per Nareit reporting. Canada contributes substantially to North American market leadership through British Columbia's established coastal and interior timberland base, Ontario's 66% forest cover contributing CAD 5.20 Billion to provincial GDP in 2024, and the ongoing Government of Canada investment of USD 500 Million in retooling Canada's forest sector announced in February 2026 per Natural Resources Canada Investments in Forest Industry Transformation programme data.

EUROPE

| Europe Timber Construction Share (2024) | EU EUDR Status | French Timber CAGR (to 2035) | EU Investment in Transport Infrastructure |

| 34.35% of global timber construction | Enforcement delayed to December 2025 (Dec 2024) | 10% CAGR government mandates for timber in public buildings | EUR 7 Billion committed for smart transport |

Europe is the world's largest timber construction market by revenue share, with 34.35% of global timber construction market revenue in 2024 per verified timber construction market data, driven by the most advanced regulatory ecosystem favouring timber and bio-based construction materials of any global region. France's timber construction market is growing at a 10% CAGR through 2035, supported by government regulations mandating timber use in public buildings and requiring minimum bio-based material content in new construction, with regional initiatives strengthening domestic timber supply chains per verified timber construction market data. The European Union's Deforestation Regulation which bans imports of commodities linked to deforestation and would have affected timber and forest product supply chains across all EU importing nations was delayed by one year in December 2024, with the revised enforcement date set at 30 December 2025, per verified EU regulatory reporting. This delay provides a transitional window for timber supply chain operators to establish the geographic tracking and certification systems required for EUDR compliance. Stora Enso, Metsä Group, Mayr-Melnhof Holz, and Binderholz dominate European timberland and forestry real estate, operating vertically integrated forest-to-building supply chains across Finland, Sweden, Austria, and Germany that demonstrate the full value chain potential of forestry real estate assets.

ASIA PACIFIC

| Asia Pacific Wood Market (2024) | China Timber Status | India and SE Asia Driver | Japan Export Importance |

| USD 916 Billion 31.8% of global market | World's largest importer and processor | Urbanisation driving construction demand | Weyerhaeuser: multi-decade Japan export relationships |

Asia Pacific dominates the global wood and timber products market with a 31.8% share valued at USD 916 Billion in 2024 per verified market analysis wood and timber products market data, with China as the world's largest consumer and importer of wood and timber products, relying on international sources including Canada, Russia, and New Zealand for raw material supply across its construction, furniture, and paper manufacturing industries. China's construction sector, particularly in urban housing and infrastructure, drives massive demand for softwood lumber, plywood, and engineered wood, with China's passenger car and construction industry expansion creating a sustained appetite for forest product imports that positions Canadian, US, and New Zealand timberland owners as long-term beneficiaries of Chinese timber demand. Japan is a strategically important export market for US Pacific Northwest timberland owners, with Weyerhaeuser maintaining multi-decade export relationships supplying high-value Douglas Fir to Japanese housing and construction markets from its Pacific Northwest timberland estate, with approximately 24% of its western log sales volumes directed to high-value export markets per Weyerhaeuser 2026 investor day data.