By Zone - By Asset Type - By Investor Profile - By Revenue Driver

Zones: Ontario Boreal North - Ontario Mid-Boreal - Georgian Bay - Muskoka - Toronto Metropolitan Region Mass Timber

Toronto anchors Ontario's timberland and forestry real estate investment market as the primary institutional capital base for Ontario pension funds holding forest real assets, Element5's USD 107 Million mass timber expansion in St. Thomas Ontario creates direct Toronto-region mass timber supply chain infrastructure, Ontario's forest sector contributed CAD 5.20 Billion to provincial GDP and CAD 8.30 Billion in exports in 2024, 74% of Ontario forest management units are certified representing 6% of world certified forest, Ontario Teachers' Pension Plan is among the world's most significant timberland investors with demonstrated large-scale forest asset deployment, and the National Building Code of Canada's twelve-storey mass timber provision is being actively applied in Toronto mass timber residential and commercial development.

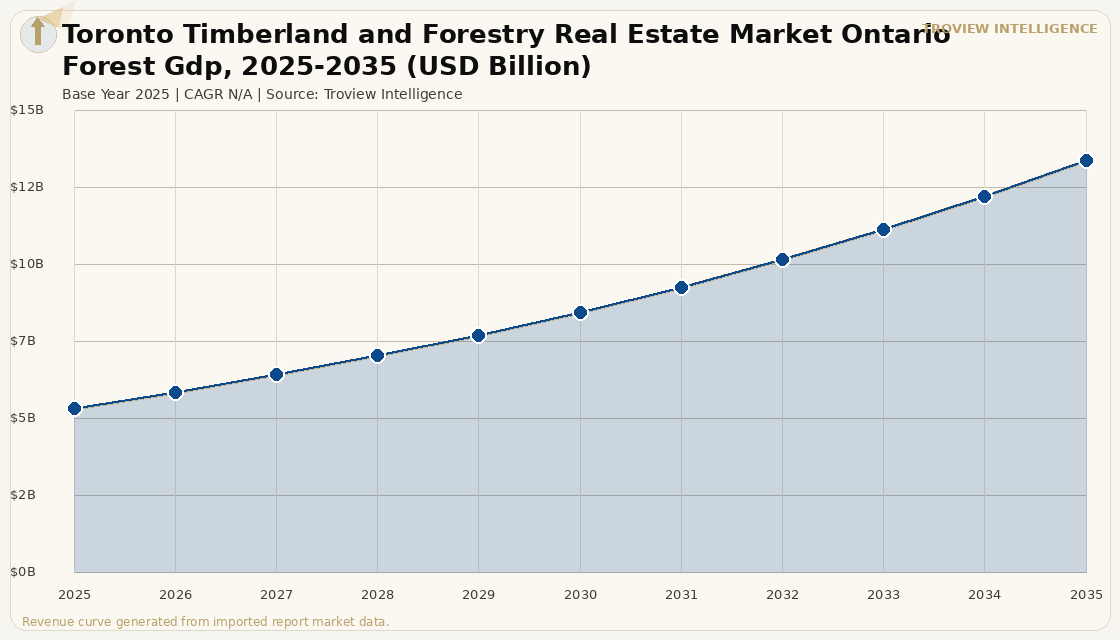

MARKET SYNOPSIS

The Toronto timberland and forestry real estate market represents the intersection of three distinct but interconnected investment dimensions: Toronto as the institutional capital headquarters for Ontario's pension fund timberland investors, Toronto's surrounding Ontario geography as the hinterland for boreal and mid-boreal commercial timberland assets serving the Great Lakes-St. Lawrence forest zone, and Toronto as the primary urban demand centre for mass timber construction that directly connects to Ontario's forestry real estate through the CLT and glulam supply chain. Ontario's forest sector contributed CAD 5.20 Billion to provincial GDP and generated CAD 8.30 Billion in forest sector exports in 2024, with forests covering 66% of Ontario's land area and 74% of forest management units certified as sustainably managed under international standards representing 6% of the world's total certified forest area per Invest Ontario verified forestry sector data. Toronto houses the management teams, investment committees, and capital deployment infrastructure of Ontario's major pension funds including Ontario Teachers' Pension Plan, Ontario Municipal Employees Retirement System, and Caisse de depot et placement du Quebec's Ontario operations that collectively represent among the most significant allocators of institutional capital to global timberland real estate. For instance, in 2025, Element5, Canada, announced a USD 107 Million investment to expand its mass timber manufacturing operations in St. Thomas, Ontario, a facility approximately 200 kilometres southwest of Toronto that will supply CLT and glulam products to Toronto-region mass timber construction projects, creating the first significant domestic mass timber manufacturing capacity within practical supply distance of Canada's largest construction market and directly linking Ontario's boreal timberland resource base to Toronto's urban development pipeline. These are some of the key factors driving revenue growth of the market.

Toronto's timberland and forestry real estate market is unique among Canadian cities in that its investment significance derives primarily from the city's role as an institutional capital hub rather than from proximity to a commercial timberland operating base. The Ontario Teachers' Pension Plan one of the world's largest pension funds with approximately CAD 250 Billion in assets under management has maintained long-standing exposure to global timberland through its real assets portfolio, executing an 870,000-acre redemption from an unidentified US timberland fund in 2022 per Forisk 2025 timberland transactions review data as a portfolio rebalancing measure, while continuing to hold significant forest real asset positions globally. The mass timber construction sector is establishing Toronto as an emerging mass timber development market: the National Building Code of Canada's 2020 edition allowing twelve-storey encapsulated mass timber construction is being progressively applied to Toronto residential and mixed-use development projects, with developers and architects actively pursuing mass timber opportunities in a city whose density targets, sustainability mandates, and carbon reporting requirements create natural demand for building systems that generate substantially lower embodied carbon than equivalent concrete construction. Canadian institutional investors and major pension funds are increasingly incorporating mass timber into their real estate portfolios per Morningstar Canada mass timber construction verified reporting of March 2026, creating alignment between Toronto's pension fund capital allocators and Toronto's mass timber development opportunity that makes the city a natural proving ground for pension fund investment in Canadian mass timber real estate.

However, the Toronto timberland and forestry real estate market faces structural constraints that limit the pace of institutional forest investment deployment and mass timber construction adoption. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy cost inflation that increases the operating costs of timberland harvesting and processing operations across Ontario's boreal forest zone, where diesel-powered logging equipment, log truck transport, and sawmill operations are subject to direct fuel cost pass-through that cannot easily be absorbed in stumpage pricing adjustments that lag real-time energy cost movements. The US countervailing duties on Canadian softwood lumber create direct revenue headwinds for Ontario timberland owners whose sawmilling and lumber production has historically targeted US residential construction markets across New England and the Northeast US, with ongoing duty rate uncertainty under CUSMA dispute resolution proceedings making long-term stumpage pricing agreements between timberland owners and lumber mills difficult to structure. Toronto's mass timber construction market faces a supply chain depth constraint: despite Element5's USD 107 Million expansion in St. Thomas and the National Building Code's twelve-storey provision, the number of certified CLT and glulam fabricators capable of supplying large-format commercial and residential mass timber projects in the Toronto market remains limited, creating lead time and cost premium issues for mass timber developers competing against concrete construction timelines that are well-supported by Toronto's deep concrete and steel supply chain. These factors substantially limit Toronto timberland and forestry real estate market growth over the forecast period.

TROVIEW ANALYST PERSPECTIVE "Toronto is a timberland market in two senses. First, it is the headquarters for the institutional capital that has been one of the world's largest allocators to global timberland through Ontario Teachers', OMERS, and the other major pension managers whose real assets teams sit in Toronto offices. That capital has flowed to US timberland REITs, global TIMOs, and direct forest acquisitions across North America and internationally. Second, it is becoming a mass timber construction market through a combination of the National Building Code's twelve-storey provision, Toronto's own sustainability and density targets, and the arrival of domestic CLT supply from Element5's St. Thomas facility. These two senses of timberland market are converging: the same pension funds whose real assets teams have been allocating to forest land globally are now being presented with domestic mass timber real estate development opportunities in their own city that combine the biological resource they understand with the urban real estate development that is their largest asset class. The developers who can package forest-to-building investment theses for Toronto pension capital with credible embodied carbon accounting, certified sustainable timber sourcing, and First Nations partnership economics are addressing the most capital-efficient audience for this thesis in North America." Troview Intelligence Senior Analyst, Toronto Timberland and Forestry Real Estate

SEGMENT INSIGHTS

Zone Deep-Dives

| Management Unit Certification | Commercial Forest Tenure | First Nations Role | Key Species |

| 74% of Ontario management units certified | Crown timber licences structured provincial tenure system | Significant forestry tenure rights across boreal | Black Spruce, Jack Pine, Balsam Fir |

Ontario's Boreal North zone encompassing the vast boreal forest from the Shield edge northward to Hudson Bay is the primary commercial timberland production zone from which Toronto-based institutional investors have historically derived their Ontario forest real asset returns, with the province's Crown timber licence system providing the legal framework for commercial forest management across a forest estate where 74% of management units are certified under international sustainable forestry standards per Invest Ontario data. The zone hosts black spruce, jack pine, and balsam fir stands that form the raw material base for Ontario's pulp, paper, and dimensional lumber industries, with tenure rights structured through the Sustainable Forestry Licences and Forest Management Agreements that obligate licensees to regenerate all harvested areas under the Ontario Crown Forest Sustainability Act creating the government-mandated regeneration cycle that institutional investors require as evidence of long-term forest asset sustainability. First Nations communities across Ontario's boreal north including Cree, Ojibwe, and Anishinaabe Nations hold constitutionally protected rights that create mandatory consultation obligations for all commercial forest management activities on Crown land, and increasingly participate directly in forestry enterprise, carbon credit programme development, and mass timber supply chain investment as economic partners rather than solely as consultation parties.

Georgian Bay and Muskoka RECREATIONAL TIMBERLAND, MIXED WOOD, CONSERVATION EASEMENTS, COTTAGE COUNTRY

| Zone Character | Land Market Dynamics | Carbon Opportunity | Key Uses |

| Mixed residential, recreational, and managed timber | High per-acre values driven by recreational demand | Conservation easements and carbon programme eligibility | Timber harvesting, recreational rental, carbon sequestration |

Georgian Bay and Muskoka represent Ontario's most valuable per-acre timberland geography for private landowners, where the intersection of recreational land values driven by Toronto cottage country demand and the underlying commercial value of mixed hardwood and softwood timber creates a multi-dimensional asset that generates revenue across timber harvesting, seasonal recreational rental, and conservation easement carbon credit programmes. Private forestland in the Georgian Bay and Muskoka region trades at significant premiums to northern Ontario commercial timberland per-acre values due to the recreational development optionality and proximity to Toronto that gives properties accessibility value beyond pure timber production economics. Conservation easements registered against Georgian Bay and Muskoka forested properties provide the legal mechanism for private landowners to monetise carbon sequestration by committing to permanent conservation of forested areas in exchange for carbon credits registered under verified voluntary carbon standards, with the proximity of these properties to major urban centres in Toronto improving credit marketing access and reducing the transaction cost of carbon programme registration. The Ontario Land Trust Alliance and conservation organisations including the Nature Conservancy of Canada are active acquirers of Georgian Bay and Muskoka timberland for conservation purposes, creating an additional buyer category that supports forestland values in the region above pure timber production metrics.

| Building Code Permission | Nearest CLT Supply | Pension Capital Alignment | Embodied Carbon Advantage |

| 12 storeys encapsulated mass timber (2020 NBC) | Element5 St. Thomas, Ontario, USD 107M expansion | Ontario Teachers, OMERS domestic mass timber RE | 40-70% lower embodied carbon vs concrete (UBC research) |

The Toronto Metropolitan Region is Canada's largest urban construction market and is in the early stages of adopting mass timber as a mid-rise construction system under the National Building Code of Canada's 2020 twelve-storey encapsulated mass timber provision, with a growing number of Toronto developers, architects, and real estate investors exploring mass timber as a structural system that satisfies the embodied carbon requirements of institutional real estate tenants and investors while offering faster construction schedules and superior thermal performance relative to concrete alternatives. Element5's USD 107 Million mass timber manufacturing expansion in St. Thomas, Ontario approximately 200 kilometres from downtown Toronto creates the first major domestic CLT and glulam supply facility within practical supply logistics distance of the Toronto construction market, reducing the import dependency on British Columbia CLT that has historically created cost premiums and long lead times for mass timber developers in Toronto competing against concrete supply chains with deep local contractor and material availability. Ontario Teachers' Pension Plan, OMERS, and other Toronto-headquartered pension managers are increasingly incorporating mass timber into their real estate portfolios per Morningstar verified reporting, creating institutional demand-side capital that can accelerate mass timber development in Toronto by combining long-duration real estate holding with the patient capital time horizon that mass timber development pipelines require. Research from the University of British Columbia and other Canadian institutions found mass timber buildings generate 40% to 70% lower embodied carbon than equivalent concrete structures per Morningstar Canada mass timber construction verified reporting, a competitive advantage that Toronto's sustainability-focused institutional tenants and development equity partners are incorporating into their building specifications and investment criteria.