By City - By Operator - By Technology - By Ownership

City Spotlights: London - Manchester - Birmingham

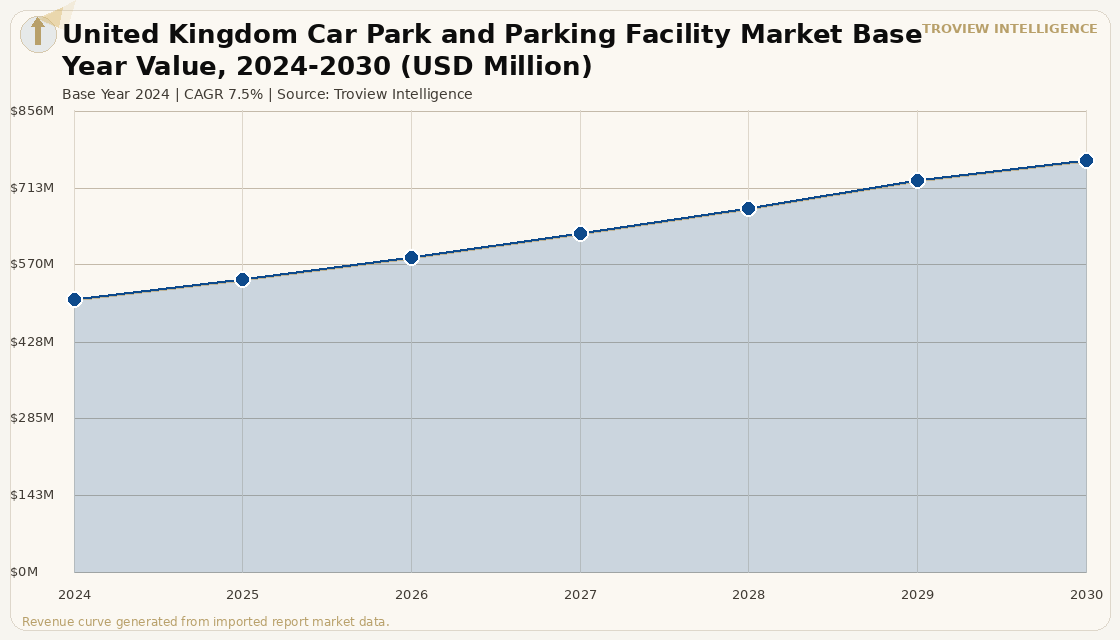

The UK parking management market was valued at USD 506.1 Million in 2024 growing to USD 764 Million by 2030 at a CAGR of 7.5%, 33.18 million cars were registered in the UK in 2022 rising from 32.88 million in 2021, the urban population rose from 83.4% in 2019 to 84.2% in 2022, NCP holds the largest UK market share as the number one car park operator with the most extensive network, APCOA signed a multi-million deal with Compleo for 1,000 EV charging stations across Network Rail car parks, GreenPoint Partners acquired a GBP 305 Million UK car park portfolio in February 2023, and 30% of UK ANPR parking enforcement appeals were upheld in 2024.

MARKET SYNOPSIS

The United Kingdom car park and parking facility market size was USD 506.1 Million in 2024 and is estimated to reach a value of USD 764 Million by 2030 with a CAGR of 7.5% during the forecast period per MarkSpark Solutions verified market data. The UK car park and parking facility market encompasses the operation and management of multi-storey car parks, surface-level off-street parking, on-street parking management concessions held by local authorities and private operators, transport hub and airport parking, hospital and retail car parks, and the associated smart parking technology, ANPR enforcement, and digital payment platforms that serve the UK's 33.18 million registered cars which increased from 32.88 million in 2021 to 33.18 million in 2022 per UK vehicle licensing authority data across a vehicle stock that continues to grow despite the emergence of hybrid working patterns and urban modal shift. The UK urban population rose from 83.4% in 2019 to 84.2% in 2022, confirming the structural concentration of vehicle and parking demand in metropolitan areas including London, Manchester, Birmingham, Leeds, and Edinburgh that defines the primary addressable geography for UK car park investment and technology deployment. National Car Parks holds the largest UK car park market share and is identified as the UK's number one car park operator by IBISWorld UK Car Parks industry analysis, with the most extensive UK network and the broadest range of products and services for both consumer and business customers. For instance, in 2024, APCOA Parking UK signed a multi-million deal with Compleo Charging Solutions to supply 1,000 AC EV charging stations across its Network Rail car park network, building on a prior partnership that installed 451 AC chargers across six Network Rail public car parks, confirming the sector-wide transition toward EV-charging-enabled parking facilities that generate dual revenue from parking fees and energy services per REFIRE investment market reporting. These are some of the key factors driving revenue growth of the market.

The UK car park market is shaped by the interplay of institutional investment in parking real estate confirmed by GreenPoint Partners' GBP 305 Million acquisition of a UK car park portfolio in February 2023 in consortium with Ivanhoe Cambridge and Greater Manchester Pension Fund and the digitalisation of parking management through ANPR enforcement, mobile payment platforms including RingGo and JustPark, and smart parking sensor networks. The level of competition in the UK car parks industry is identified as moderate and increasing per IBISWorld UK Car Parks analysis, with National Car Parks (acquired by Park24), APCOA Parking UK, Q-Park, and Euro Car Parks competing for long-term management contracts alongside a growing tier of technology-first challengers including JustPark that win transient users through frictionless app-based interfaces and algorithmic pricing. The AFIR regulation requiring every parking site with more than 20 spaces to install at least one EV charger, a rule that entered force across the EU in 2024 while not directly binding on post-Brexit UK, is creating competitive pressure on UK operators to match European EV charging standards or risk losing fleet and corporate accounts that manage multi-country vehicle portfolios against consistent EV infrastructure benchmarks. Westminster Council, which controls the largest concentration of on-street parking in central London, shifted its parking charging model in 2024 to emissions-based pricing, reducing the preferential treatment for EVs that had previously applied and beginning the transition of on-street parking revenue to reflect vehicle environmental classification rather than zero-rate EV exemptions.

However, the United Kingdom car park and parking facility market faces structural constraints that limit revenue recovery and sustainable growth. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy cost inflation that increases the operating costs of UK multi-storey car parks whose electricity consumption for LED lighting, mechanical ventilation, lift systems, ANPR cameras, and the rapidly expanding EV charging point network represents an increasingly significant proportion of total operating expenditure. The sustained effect of hybrid working on weekday car park utilisation where commuter season ticket revenue that represented a reliable high-margin income stream for city-centre car parks prior to 2020 has not fully recovered as employers continue to offer 2-to-3-day office attendance patterns creates persistent structural revenue headwinds for the multi-storey car park segment. ANPR enforcement litigation risk is material and increasing: 30% of UK ANPR parking appeals were upheld in 2024 per verified UK parking enforcement analysis, forcing operators to invest in audit trails and human review processes that increase the cost of enforcement and reduce the net revenue yield from penalty charges. These factors substantially limit United Kingdom car park and parking facility market growth over the forecast period.

TROVIEW ANALYST PERSPECTIVE "The UK car park market in 2025 is more nuanced than a simple recovery story. The GBP 305 million GreenPoint portfolio acquisition confirmed that institutional capital still values car park real estate cash flows correctly, because a well-located multi-storey in a busy UK city generates near-inelastic daily demand from workers, shoppers, and visitors who have no alternatives at peak pricing. But the hybrid working structural shift has permanently impaired the season ticket revenue that was the premium income layer of city-centre operators: the commuter who used to spend GBP 250 per month on a parking season ticket is now coming in three days a week and paying transient rates, cutting their car park spend by 40%. The EV charging revenue opportunity is real and APCOA's 1,000-charger Compleo deal is a concrete execution of it, but the charging revenue per dwell event is still lower than equivalent tariff per parking hour at most sites the economics improve significantly only with V2G capability, and the UK grid integration framework for V2G is still being developed. The market is generating steady 7.5% CAGR in managed parking revenue. The real upside is in the transformation of car park infrastructure from single-purpose to multi-purpose urban assets that combine parking, charging, and potentially energy storage." Troview Intelligence Head of United Kingdom Car Park and Parking Facility Research

SEGMENT INSIGHTS

Three Cities Shaping the UK Parking Market

| London Congestion Charge (Jan 2026) | EV CVD Status (Dec 2025) | ULEZ Coverage | Key Operators |

| GBP 18/day (up from GBP 15), EV pays GBP 13.50 (Auto Pay) | Cleaner Vehicle Discount ended 25 Dec 2025 | All 33 London boroughs, 24/7, EVs exempt indefinitely | NCP (largest network), APCOA, Q-Park, Euro Car Parks |

London is the UK's dominant car park and parking facility market, hosting the largest concentration of multi-storey car parks, managed surface car parks, and on-street parking management operations of any UK city, with NCP operating the most extensive London car park network including EV charging points on a first-come-first-served basis across central and inner London locations. The Congestion Charge in central London rose from GBP 15 to GBP 18 per day from 2 January 2026, simultaneously ending the Cleaner Vehicle Discount for electric vehicles on 25 December 2025 with EVs now paying a reduced charge of GBP 13.50 when registered on Auto Pay, representing a 25% discount versus the full GBP 18 charge for petrol and diesel vehicles per The Electric Car Scheme verified 2026 guidance. Transport for London estimated that the CVD change would reduce approximately 2,200 vehicles daily from entering the Congestion Charge Zone, as EV drivers who previously benefited from zero-cost entry re-evaluate the financial case for driving into central London. The ULEZ expanded across all 33 London boroughs in August 2023 and operates 24 hours a day seven days a week, with electric vehicles remaining completely exempt from ULEZ charges indefinitely, creating a sustained cost differential between EV and non-EV operation in London that supports EV adoption but does not prevent petrol and diesel vehicles from accessing car parks outside the Congestion Charge Zone.

| Market Position | Hybrid Working Impact | Institutional Investor | Key Operators |

| Second-largest UK car park market | Significant commuter season ticket volume reduction post-2020 | GMPF co-invested in GBP 305M portfolio (GreenPoint) | NCP, APCOA, Q-Park, independent regional operators |

Manchester is the UK's second-largest car park and parking facility market, serving a metropolitan area of approximately 2.8 million residents with a dense network of multi-storey and surface car parks in the city centre, MediaCityUK, Airport City, and the Manchester Piccadilly and Victoria transport interchange catchments. Manchester's car park market has experienced the structural hybrid working impact more acutely than London due to the higher proportion of Manchester city centre workers who rely on car commuting as opposed to public transport with the Manchester and Salford commuter belt served by relatively limited rapid transit compared to London's Underground network, making car park season tickets a more significant share of city-centre operator revenue. The Greater Manchester Pension Fund was a co-investor in the GreenPoint Partners GBP 305 Million UK car park portfolio acquisition in February 2023, confirming Manchester's institutional capital alignment with UK car park real estate as a long-term income asset, and positioning the portfolio for EV charging integration and smart parking technology deployment that enhances revenue per bay above traditional tariff structures. Manchester Airport's car park complex is one of the highest-revenue airport parking operations in the UK, generating significant pre-booking revenue through dynamic pricing as the airport serves approximately 28 million passengers annually with multi-day parking demand that commands premium pricing during school holiday and peak travel periods.

| Market Position | Key Demand Anchor | HS2 Impact | Parking Technology |

| Third-largest UK car park market | NEC (National Exhibition Centre) + Birmingham Airport | Changing city-centre accessibility dynamics | ANPR and app-based booking expansion |

Birmingham is the UK's third-largest car park and parking facility market, anchored by the National Exhibition Centre complex which operates one of the UK's largest single-site car park operations across its event, arena, and convention venues and by Birmingham Airport's extensive terminal car park estate that serves approximately 12 million annual passengers. Birmingham's car park market benefits from the Commonwealth Games 2022 infrastructure legacy that improved transport connectivity and urban regeneration across the city centre, with new development in Curzon Street and the HS2 terminus zone creating future parking demand as the area transitions from industrial to mixed-use commercial. The HS2 high-speed rail programme despite its scope reduction to Birmingham from London only is reshaping Birmingham's transport connectivity economics and creating uncertainty about the long-term demand for car park capacity in areas adjacent to the Curzon Street terminus where park-and-ride demand versus direct urban pedestrian access will depend on future transport mode decisions by Birmingham commuters and visitors. Birmingham City Council's car park estate and the city's major private operators including Q-Park and NCP have invested in ANPR enforcement and app-based booking platforms that improve revenue yield and reduce the manual barrier maintenance costs that had historically been a significant operational overhead in Birmingham's predominantly older multi-storey car park stock.