| TROVIEW INTELLIGENCE | Australia Cooling and Energy Infrastructure Real Estate Market | Q2 2026 |

| TROVIEW INTELLIGENCE · COUNTRY INTELLIGENCE REPORT |

By Market · By Infrastructure Type · By Cooling Technology · By End-User Sector

Market Profiles: Sydney · Melbourne · Canberra · Brisbane · Perth

Australia's data centre market is expected to require approximately AUD 10 billion of additional grid investment to meet an extra 3.5 GW of power demand by 2035 per Moody's February 2025 analysis, Amazon committed AUD 20 billion to expand Australian data centre infrastructure by 2029, Microsoft committed AUD 5 billion, Blackstone acquired AirTrunk for USD 16.1 billion in 2024, AirTrunk is pursuing an AUD 5 billion Kemps Creek campus in Western Sydney planned for up to 1 GW with 936 cooling units and 7,488 cabinets of lithium-ion battery storage, NextDC secured AUD 3.5 billion in new senior debt facilities and acquired a 258,000 square metre Eastern Creek plot for AUD 353 million for its S7 hyperscale campus, and Macquarie Asset Management channelled USD 17 billion into Applied Digital and Aligned Data Centers in 2025 a capital deployment environment that is converting Australian data centre cooling and energy infrastructure from a component cost into a sovereign-scale investment category.

| Standard License: USD 6,500 | Enterprise License: USD 9,500 |

MARKET SYNOPSIS

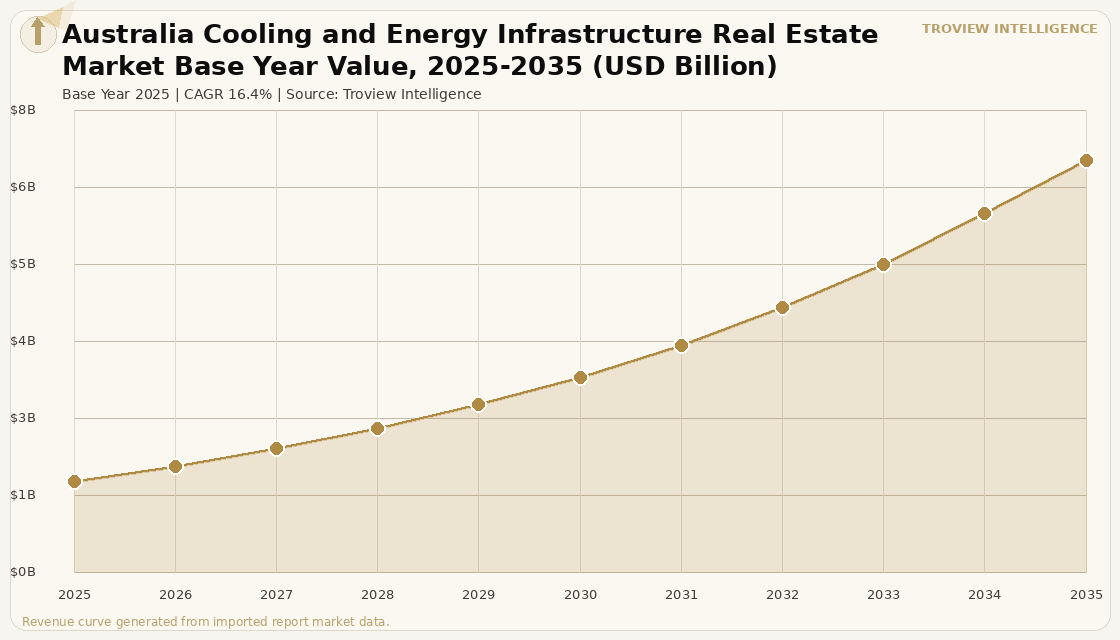

The Australia cooling and energy infrastructure real estate market size was USD 1.52 Billion in 2025 and is expected to register a revenue CAGR of 16.4% during the forecast period, reaching USD 6.84 Billion by 2035. Market revenue growth is supported by a data centre investment pipeline that is unprecedented in Australian infrastructure history: Amazon Web Services, United States, committed AUD 20 billion to expand its Australian data centre infrastructure by 2029, Microsoft Corporation, United States, committed AUD 5 billion to expand its Australian data centre portfolio, and Blackstone, United States, acquired AirTrunk for USD 16.1 billion in 2024 in the largest data centre transaction ever recorded in the Asia Pacific region per Westpac IQ analysis of November 2025. The Australian Government has classified data centres as Systems of National Significance under the Security of Critical Infrastructure Act 2018, and the National AI Plan published December 2, 2025 outlined Australia's goal to position itself as a principal gateway for AI infrastructure investment and sustainable digital development per Bird and Bird analysis of February 2026. Moody's analysis of February 2025 forecast that Australian data centres, if connected to national electricity networks, would require approximately AUD 10 billion of additional grid investment to meet an extra 3.5 GW of power demand that the industry is expected to require by 2035 a grid investment that directly drives cooling and energy infrastructure procurement across every new Australian data centre project. For instance, in November 2024, Macquarie Data Centres, Australia, part of the ASX-listed Macquarie Technology Group, began construction on its AUD 350 million IC3 Super West data centre in Sydney's Macquarie Park, incorporating advanced cooling systems, NABERS-rated energy efficiency infrastructure, and renewable energy sourcing to meet both commercial sustainability targets and the Australian Government's data centre energy efficiency framework per Westpac IQ reporting of November 2025. These are some of the key factors driving revenue growth of the market.

NEXTDC Limited, Australia, an ASX200-listed technology company and Australia's leading independent data centre operator, secured new senior debt facilities totalling AUD 3.5 billion following the completion of general syndication in 2025, and acquired a 258,000 square metre plot of land at Eastern Creek, Sydney for AUD 353 million to develop its S7 hyperscale campus, which is designed to serve hyperscale cloud providers in a new availability zone within the Sydney market complementing its existing S1, S2, and S3 facilities per NEXTDC company and Baxtel facility data. NEXTDC's solar arrays across its M1 Melbourne, S1 Sydney, P1 Perth, and SC1 Sunshine Coast facilities collectively avoided nearly 700 tonnes of carbon dioxide equivalent emissions in FY25 per NEXTDC sustainability reporting, reflecting the integration of on-site renewable energy generation into its cooling and energy infrastructure model. AirTrunk, Australia, owned by Blackstone and Canada Pension Plan Investment Board since the USD 16.1 billion acquisition, signed a long-term power purchase agreement with Google and OX2 in 2023 to develop a new solar farm in Australia adding 25 MW of renewable energy capacity to the grid per Westpac IQ reporting of November 2025, demonstrating the direct linkage between hyperscale data centre operations and renewable energy infrastructure investment in the Australian market. AirTrunk's planned AUD 5 billion Kemps Creek campus in Western Sydney, which is the subject of a AUD 4.3 billion construction financing package per Construction Review Online reporting of June 2026, is designed to include 936 cooling units, 852 diesel backup generators, and 7,488 cabinets of lithium-ion battery storage, constituting one of the largest single cooling and energy infrastructure procurement programmes in Australian history. These are some of the key factors driving revenue growth of the market.

However, the Australia cooling and energy infrastructure real estate market faces structural constraints that temper the pace of delivery even as the investment pipeline reaches record levels. Grid connection timelines remain the binding constraint on new data centre cooling and energy infrastructure commissioning, with network service providers in New South Wales and Victoria facing connection request backlogs that extend project timelines by 18 to 36 months and force operators to invest in on-site generation, battery storage, and microgrid infrastructure that increases capital costs per MW above equivalent markets with faster grid connectivity. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis affecting approximately 20% of global seaborne LNG flows, create upward pressure on Australian wholesale electricity prices given the nation's dependence on gas-fired peaking generation across the National Electricity Market, increasing the operating cost of cooling and energy infrastructure for data centre operators whose power purchase agreements are denominated in Australian dollars but benchmarked to LNG-linked spot price mechanisms. Water scarcity is an increasingly material constraint on evaporative cooling system deployment in New South Wales and South Australia, where data centre campus developments require water consumption assessments and water management plan approvals that add planning approval timelines and ongoing operational cost exposure to facilities reliant on evaporative cooling as their primary thermal management method. AirTrunk's Kemps Creek campus is estimated to consume approximately 22.4 million litres of water per year per NSW planning documents, equivalent to approximately nine Olympic swimming pools annually, a scale that is attracting regulatory scrutiny under NSW parliamentary inquiry proceedings commenced in May 2026. These factors substantially limit Australia cooling and energy infrastructure real estate market growth over the forecast period.

The Australian data centre market has absorbed more hyperscale capital commitment in the 24 months between 2024 and 2026 than in the previous decade of its existence. Amazon's AUD 20 billion, Microsoft's AUD 5 billion, Blackstone's USD 16.1 billion for AirTrunk, and NEXTDC's AUD 3.5 billion debt raise are not sequential infrastructure investments. They are concurrent bets on the same thesis: that Australia will be the primary regional hub for AI compute serving Southeast Asia and the Pacific, and that the operator who controls the power contract, cooling specification, and grid interconnection in Western Sydney today will control the market for the next 15 years. The cooling and energy infrastructure investment embedded in these commitments is not discretionary. The 1 GW Kemps Creek campus needs 936 cooling units. The S7 Eastern Creek campus needs new grid infrastructure. These are fixed costs of the AI infrastructure strategy, not variables. And they are being deployed regardless of short-term interest rate movements or geopolitical energy price volatility." Troview Intelligence Head of Australia Cooling and Energy Infrastructure Research

SEGMENT INSIGHTS

| 03 | MARKET PROFILE ANALYSIS |

Five Markets Defining Australia Cooling and Energy Infrastructure Investment

| Sydney's Share of Upcoming Capacity | AirTrunk Kemps Creek | NEXTDC S7 Eastern Creek | Grid Investment Required |

| ~65% of national pipeline (ResearchAndMarkets) | AUD 5B, up to 1 GW, 936 cooling units | AUD 353M land, AUD 7B AI facility, 550 MW | ~AUD 6.5B of AUD 10B national estimate |

Sydney is Australia's dominant data centre and cooling infrastructure market, accounting for approximately 65% of the national upcoming data centre power capacity pipeline per ResearchAndMarkets Australia colocation portfolio analysis of July 2025, anchored by the Western Sydney data centre corridor centred on Kemps Creek, Blacktown, Horsley Park, and Eastern Creek where the largest hyperscale campus developments in Australian history are simultaneously under development or planning approval. AirTrunk's planned Kemps Creek campus, the subject of a preliminary AUD 5 billion acquisition agreement with developer ISPT, is designed for up to 1 GW across 24 data halls with 936 cooling units, 852 diesel backup generators, and 7,488 cabinets of lithium-ion battery storage per NSW planning documents, making it the largest single cooling and energy infrastructure procurement programme in Australian commercial real estate history. NEXTDC's USD 7 billion S7 hyperscale AI facility in Western Sydney with approximately 550 MW of capacity, with ChatGPT developer OpenAI as the first major customer, was endorsed by the NSW Government's Investment Delivery Authority in March 2026 as one of 15 fast-tracked data centre projects, with NEXTDC securing AUD 3.5 billion in new senior debt facilities in 2025 to support its Sydney and national expansion pipeline per NEXTDC company disclosures.

| NEXTDC M4 | AirTrunk MEL2 | Key Demand | Infrastructure Profile |

| AUD 2B, liquid-cooled AI Factory, Port Melbourne | Major hyperscale capacity hub, Melbourne | Sovereign AI, government workloads, financial services | Tier III/IV, NABERS-rated, renewable-powered |

Melbourne is Australia's second-largest data centre market and the primary hub for sovereign AI compute and government workload infrastructure, with NEXTDC's AUD 2 billion M4 Melbourne AI Factory at Port Melbourne representing the most significant liquid cooling infrastructure investment in Australian data centre history. NEXTDC's M4 is explicitly designed as a sovereign AI facility liquid-cooled infrastructure engineered for high-density AI compute serving Australian government and enterprise requirements that cannot be hosted on US-headquartered hyperscale platforms due to data sovereignty and security classification requirements. AirTrunk's MEL2 campus serves as a major capacity hub in Melbourne, providing hyperscale-native data centre infrastructure for global cloud providers requiring multi-megawatt scale in the Victorian market. Melbourne's cooling and energy infrastructure market benefits from Victoria's higher share of renewable energy in the state electricity grid relative to New South Wales, reducing the renewable energy sourcing challenge for power purchase agreements and improving the economics of all-electric cooling systems that use electricity rather than diesel or gas for backup generation.

| Primary Operator | Key Classification | Cooling Requirement | Demand Driver |

| CDC Data Centres government-focused | System of National Significance (SOCI Act) | Tier IV, highest physical security, SCEC-rated | Australian Government AI Plan (Dec 2025) |

Canberra is Australia's government and defence data centre market, hosting the highest-security and most stringent cooling and energy infrastructure specifications of any Australian data centre submarket. CDC Data Centres, Australia, is the primary colocation operator in Canberra, with its facilities serving Australian federal government agencies, Department of Defence workloads, and the intelligence community that requires Tier IV uptime guarantees, Security Construction and Equipment Committee-rated physical security, and cooling infrastructure capable of sustaining operations through grid failure events without interruption. The Australian Government's National AI Plan published December 2, 2025 explicitly identified data centres as critical AI infrastructure and outlined government support for expanding sovereign AI compute capacity, a policy commitment that directly increases demand for the Canberra market's government-grade cooling and energy infrastructure above commercial colocation specifications. New data centre developments in the Australian Capital Territory face the most stringent environmental performance requirements of any Australian state or territory, including mandatory NABERS energy ratings, water efficiency reporting, and carbon emission disclosure under the ACT Government's Net Zero Emissions by 2045 strategy.

| Brisbane Appeal | Perth Appeal | NEXTDC Presence | Growth Driver |

| Lower land cost, Queensland renewable energy | Undersea cable gateway, WA gas grid, resources sector | B1/B2 Brisbane, P1/P2 Perth NABERS-rated | Edge AI, resources sector digitisation, latency relief |

Brisbane and Perth represent Australia's fastest-growing regional data centre markets, with cooling and energy infrastructure investment in both markets driven by lower land costs relative to Sydney, access to renewable energy resources that support direct power purchase agreement structures, and the latency relief they provide for enterprise and edge AI workloads serving Queensland and Western Australia populations that cannot be optimally served from Sydney or Melbourne campuses. NEXTDC operates its B1 and B2 Brisbane data centres and P1 and P2 Perth facilities with NABERS-rated energy efficiency and renewable energy integration, establishing the baseline cooling and energy infrastructure standard for regional Australian markets. Perth's Western Australian gas grid provides reliable backup power infrastructure for data centres at a cost per MWh competitive with east coast markets, while Western Australia's abundant solar irradiance creates favourable economics for on-site solar power purchase agreements that reduce data centre energy costs below the national electricity market rate available to Sydney and Melbourne operators.