| TROVIEW INTELLIGENCE | Singapore Colocation Data Centre Market | Q2 2026 |

| TROVIEW INTELLIGENCE · COUNTRY INTELLIGENCE REPORT |

By Submarket · By Colocation Type · By Data Centre Tier · By Occupier Sector

Submarket Profiles: Jurong · Loyang · Tai Seng · Tuas · Tampines · Woodlands

Singapore's colocation data centre market operates as the most constrained and premium-priced market in Southeast Asia, with a vacancy rate of approximately 1.4% the lowest in APAC as of December 2024 per Arizton market data, more than 780 MW of operational power capacity across 44 existing facilities per ResearchAndMarkets colocation portfolio analysis, rack rates at Equinix's SG campuses reaching SGD 3,500 to SGD 8,000 per month per RebootMonkey Q1 2026 market data, and the Singapore Economic Development Board and IMDA launching the DC-CFA2 framework in December 2025 allocating at least 200 MW of new capacity with a 50% green energy mandate the most stringent data centre development standard in Asia Pacific while KKR and Singtel entered advanced talks in November 2025 to acquire over 80% of ST Telemedia Global Data Centres in a transaction valued at more than USD 5 billion, confirming the depth of international institutional appetite for Singapore's capacity-constrained colocation ecosystem.

| Standard License: USD 6,500 | Enterprise License: USD 9,500 |

MARKET SYNOPSIS

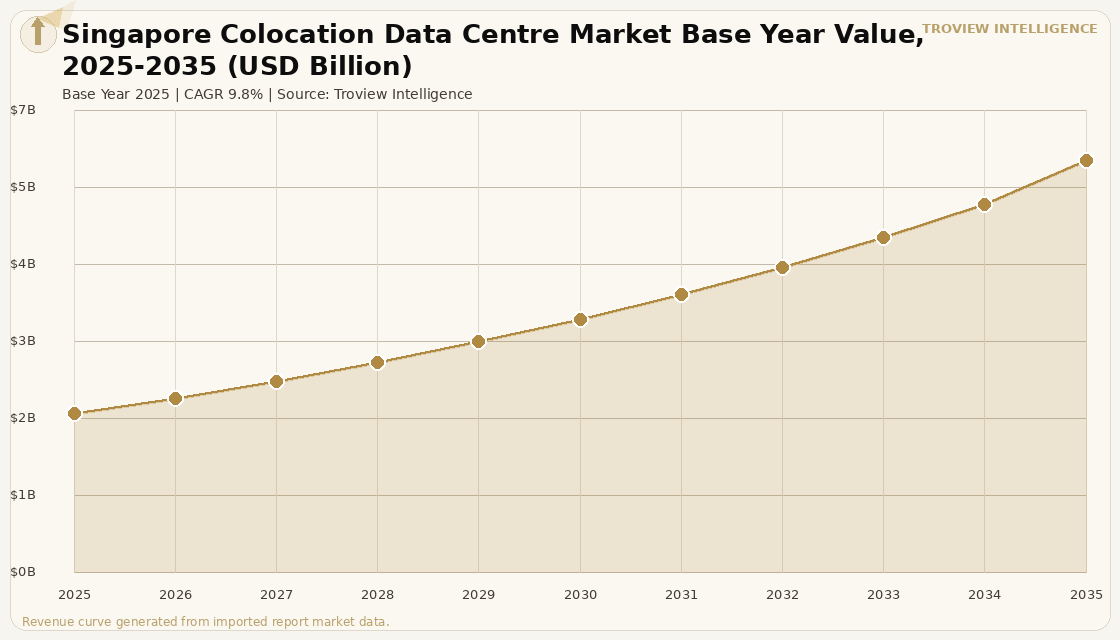

The Singapore colocation data centre market size was USD 2.24 Billion in 2025 and is expected to register a revenue CAGR of 9.8% during the forecast period, reaching USD 5.81 Billion by 2035. Market revenue growth is supported by Singapore's structural position as Southeast Asia's primary digital infrastructure hub, anchored by its fibre optic submarine cable network connecting to more than 30 international cable systems, its role as the financial services capital of ASEAN, and the government-regulated supply environment that ensures colocation operators with approved Data Centre Call for Applications allocations face no effective competition from new market entrants without equivalent regulatory clearance. The Singapore Economic Development Board and IMDA launched the DC-CFA2 framework in December 2025, allocating at least 200 MW of new data centre capacity with mandatory 50% green energy sourcing and a Power Usage Effectiveness target of 1.25 at full load the most stringent PUE standard of any regulated data centre market globally with the application window closing March 31, 2026 per Morgan Lewis analysis of March 2026. Singapore hosts approximately 44 existing colocation data centres with more than 780 MW of operational power capacity, representing approximately 60% of Southeast Asia's total data centre capacity per RebootMonkey Q1 2026 market data and KWM analysis. For instance, in 2023, Equinix, Inc., United States, GDS Holdings, United States, Microsoft Corporation, United States, and a consortium of AirTrunk, Australia, and ByteDance, China, were collectively allocated 80 MW of new Singapore data centre capacity under the DC-CFA1 pilot framework per Singapore EDB and IMDA official allocation announcement of 2023, establishing the precedent for government-controlled capacity rationing that gives Singapore's approved operators a permanent competitive moat against new market entrants. These are some of the key factors driving revenue growth of the market.

Equinix, Inc., United States, operates Singapore's most interconnection-dense colocation facilities across its SG1, SG2, SG3, and SG5 campuses with 758 total networks across four campuses and 11 internet exchange connections per RebootMonkey Q1 2026 data, with rack rates reaching SGD 3,500 to SGD 8,000 per month at Equinix SG campuses, the highest in the Singapore market, reflecting the interconnection premium that Equinix's carrier-neutral ecosystem commands over competing facilities. Equinix announced the SG6 Singapore data centre with an initial USD 260 million investment and a planned 20 MW build under the DC-CFA1 pilot framework, expected to open in 2027 per verified company disclosure. ST Telemedia Global Data Centres, Singapore, operates four Singapore campuses in Jurong West, Loyang, Tai Seng, and a fourth location serving the mid-market and regional enterprise segment at rack rates of SGD 2,500 to SGD 5,500 per month, with KKR, United States, and Singtel, Singapore, entering advanced talks in November 2025 to acquire over 80% of STT GDC from ST Telemedia in a transaction valued at more than USD 5 billion per verified trade press of November 2025. Keppel Data Centres, Singapore, announced a staged SGD 1.4 billion divestment of two AI-ready hyperscale data centres at its Singapore campus to Keppel DC REIT with completion expected by end 2025 subject to approvals per Keppel company disclosure, while AirTrunk, Australia, is developing SGP2, one of Singapore's largest upcoming data centres with planned capacity exceeding 70 MW per ResearchAndMarkets colocation portfolio analysis of December 2025. These are some of the key factors driving revenue growth of the market.

However, the Singapore colocation data centre market faces structural constraints that will limit the pace of revenue growth and market expansion through the forecast period regardless of demand strength. The government's controlled capacity release under the CFA framework ensures that new supply can only enter the market through a regulated approval process with lead times measured in years rather than months, creating a permanent supply ceiling that benefits existing CFA-approved operators but prevents the market from responding to demand spikes at the velocity that commercial operators would otherwise achieve. Singapore's construction costs reached USD 14.53 per watt in 2025, the second highest globally after Tokyo per Turner and Townsend 2025 data, creating a development capital intensity that limits the pool of operators capable of funding new CFA-approved facilities at scale and concentrating development activity among the largest global operators. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, which handles approximately 20% of global seaborne LNG per IMF March 2026 confirmation, directly affect Singapore's electricity generation costs given its near-total dependence on natural gas for grid power, with SP Group industrial power at approximately SGD 0.20 per kWh per RebootMonkey Q1 2026 data subject to upward revision as LNG spot prices respond to Middle East supply disruptions. The establishment of the Johor-Singapore Special Economic Zone is redirecting some hyperscale demand from Singapore to Johor, where Malaysia's planned approximately 4.8 GW of new data centre capacity provides a lower-cost alternative for operators that do not require Singapore's interconnection density per ResearchAndMarkets SEA colocation portfolio analysis of January 2026. These factors substantially limit Singapore colocation data centre market growth over the forecast period.

Singapore's colocation market is the most explicit demonstration in the world of what happens when a government decides that data centre infrastructure is critical national infrastructure and regulates it accordingly. The CFA framework does not suppress demand the DC-CFA1 allocation of 80 MW in 2023 was oversubscribed within weeks of opening. It suppresses supply, and in doing so it has created an environment where every CFA-approved operator holds a permit that is worth more than the building they are constructing on it. The SGD 5 billion valuation being discussed for STT GDC in November 2025 is not primarily a valuation of the physical assets. It is a valuation of the CFA approvals, the carrier relationships, the Singapore government goodwill, and the impossibility of a new entrant replicating that position from a standing start. Investors who understand this are not asking whether Singapore colocation demand will grow. They are asking who holds the permits." Troview Intelligence Head of Singapore Colocation Data Centre Research

SEGMENT INSIGHTS

| 03 | SUBMARKET ANALYSIS |

Six Submarkets Defining Singapore Colocation Geography

| Key Operators | CFA2 Potential Site | Power Infrastructure | Upcoming Supply |

| Keppel DC, AirTrunk SG1, Singtel DC, STT GDC | JTC Jurong Island land identified by EDB/IMDA | Jurong industrial grid highest capacity in Singapore | AirTrunk SGP2: 70+ MW planned |

The Jurong and Tuas western corridor is Singapore's primary hyperscale and wholesale colocation zone, hosting Keppel Data Centres' SGX-listed REIT-backed campus, AirTrunk's SG1 hyperscale-native facility serving Amazon Web Services and Google as primary tenants, the Singtel Data Centre, and two of ST Telemedia Global Data Centres' four Singapore campus locations. The corridor benefits from proximity to Jurong Island's industrial power infrastructure, which provides the highest grid capacity available in Singapore and makes it the preferred development zone for the largest-format wholesale colocation campuses requiring multi-MW power feeds. IMDA identified JTC land on Jurong Island as a potential site for the DC-CFA2 allocation of at least 200 MW in the December 2025 framework announcement per Morgan Lewis analysis, signalling that the western corridor will absorb the majority of Singapore's next capacity increment. AirTrunk's SGP2 development with planned capacity exceeding 70 MW represents the largest single incoming addition to the Singapore colocation market in the near-term pipeline per ResearchAndMarkets portfolio analysis of December 2025.

| Strategic Asset | Cable Systems | Operator Presence | Latency Profile |

| Changi Beach cable landing station proximity | JUPITER and Bifrost (US West Coast latency advantage) | STT GDC Loyang, Equinix connectivity node | Lowest US-route latency in Singapore |

The Loyang and Changi eastern corridor is Singapore's submarine cable gateway, with proximity to the Changi Beach cable landing station providing the lowest-latency connectivity on trans-Pacific routes to the United States via the JUPITER and Bifrost submarine cable systems per RebootMonkey Q1 2026 connectivity analysis. ST Telemedia Global Data Centres operates its Loyang campus in this corridor, serving the latency-sensitive financial services and regional enterprise tenants who require optimal positioning on US West Coast routes as well as intra-Asia connections to Hong Kong, Tokyo, and Sydney. The Changi Airport logistics and commercial infrastructure that surrounds the eastern corridor provides a talent recruitment advantage for data centre operations staff, as the aviation and logistics industry's engineering workforce has transferable skills applicable to facility management. The corridor's colocation supply is constrained by planning restrictions in the vicinity of Changi Airport's approach paths, limiting the height and density of new data centre construction relative to the western industrial corridor.

| Primary Tenants | Equinix Campuses | Rack Rates | Connectivity |

| Financial services, MNCs, regional enterprise | SG1/SG2/SG3/SG5: 758 networks, 11 IXPs | SGD 3,500 to SGD 8,000/month (Equinix highest) | SGIX Singapore Internet Exchange proximity |

The Tai Seng and central Singapore submarket hosts the densest concentration of retail colocation and carrier-neutral interconnection facilities in Southeast Asia, anchored by Equinix's four SG campuses that collectively aggregate 758 networks, 11 internet exchange connections, and rack rates reaching SGD 8,000 per month for premium interconnection-dense deployments per RebootMonkey Q1 2026 data. The proximity of these facilities to the SGIX Singapore Internet Exchange and to the headquarters of the Monetary Authority of Singapore creates an interconnection ecosystem that serves the direct connectivity requirements of the financial services sector international banks, asset managers, insurance firms, and payment processors whose trading, settlement, and compliance infrastructure requires colocation within the carrier-neutral Singapore internet exchange fabric. STT GDC's Tai Seng campus serves the same financial services and multinational enterprise cohort at rack rates of SGD 2,500 to SGD 5,500 per month, providing a cost-competitive alternative to Equinix for tenants whose interconnection requirements are satisfied by fewer than 100 peering relationships and who do not require the full depth of the Equinix SG ecosystem.

| Strategic Context | Cross-Border Fibre | Johor Pipeline | Market Role |

| Johor-Singapore Special Economic Zone (JS-SEZ) | Woodlands Causeway and Second Link connectivity | ~4.8 GW planned capacity (Amazon, Microsoft, Google) | Singapore overflow and Johor gateway |

The Woodlands and northern Singapore submarket is acquiring strategic importance as the operational gateway to the Johor-Singapore Special Economic Zone, which is redirecting hyperscale demand that cannot be accommodated within Singapore's CFA-constrained supply framework to Johor Bahru in Malaysia. Malaysia's data centre pipeline includes approximately 4.8 GW of planned capacity from Amazon Web Services, Microsoft Azure, Google Cloud, and a growing cohort of Chinese hyperscalers, with the JS-SEZ framework designed to allow Singapore-regulated operators to maintain cross-border operational connectivity across the Woodlands Causeway and Tuas Second Link. Colocation operators with facilities in the Woodlands corridor benefit from the lowest-latency Singapore-Johor fibre connectivity and from proximity to the causeway infrastructure that supports the physical movement of engineers and equipment between Singapore and Johor campuses. The Woodlands submarket is currently the smallest by installed colocation capacity, but is the fastest-changing in strategic positioning as the JS-SEZ regulatory framework matures and hyperscaler operators formalise their cross-border infrastructure strategies.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from verified company announcements, Singapore EDB and IMDA official communications, and verified trade press.