| TROVIEW INTELLIGENCE | Sydney Cooling and Energy Infrastructure Real Estate Market | Q2 2026 |

| TROVIEW INTELLIGENCE · CITY INTELLIGENCE REPORT |

Submarket Profiles: Kemps Creek · Eastern Creek · Horsley Park · Macquarie Park · Minchinbury · Gore Hill

Sydney accounts for approximately 65% of Australia's upcoming data centre power capacity pipeline per ResearchAndMarkets colocation portfolio analysis of July 2025, with the Western Sydney corridor absorbing the largest concentration of cooling and energy infrastructure capital in Australian data centre history: AirTrunk's planned Kemps Creek campus incorporating 936 cooling units, 852 diesel backup generators, and 7,488 cabinets of lithium-ion battery storage across a 400,000 square metre campus designed for up to 1 GW, NEXTDC's AUD 353 million Eastern Creek land acquisition for its S7 AI facility with OpenAI as first customer at 550 MW, Goodman Group and Amazon Web Services pursuing sites in the Kemps Creek and Horsley Park corridors, Starwood Capital and Doma Infrastructure developing a carrier-neutral campus in Minchinbury, and the NSW Government's Investment Delivery Authority endorsing all 15 submitted data centre projects in March 2026 a single approval wave that committed more cooling and energy infrastructure to Western Sydney than any other city in the Southern Hemisphere has deployed in a decade.

| Standard License: USD 2,200 | Enterprise License: USD 9,500 |

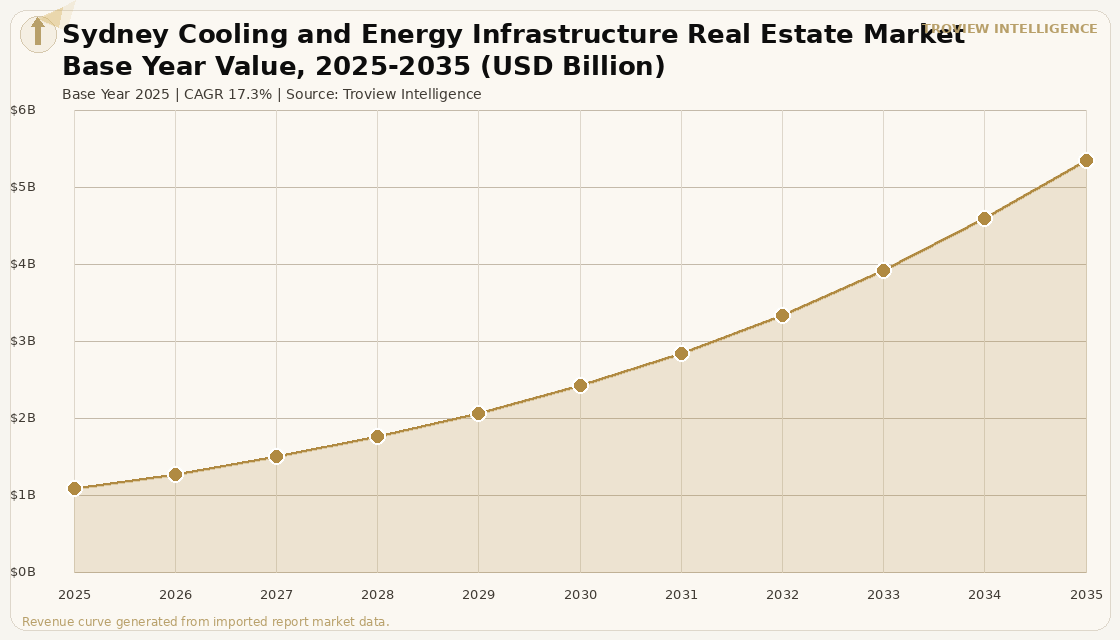

MARKET SYNOPSIS

The Sydney cooling and energy infrastructure real estate market size was USD 1.01 Billion in 2025 and is expected to register a revenue CAGR of 17.3% during the forecast period, reaching USD 4.94 Billion by 2035. Market revenue growth is supported by Sydney's position as the primary destination for Australian hyperscale data centre capital, with the Western Sydney corridor concentrated in the Kemps Creek, Eastern Creek, Horsley Park, and Minchinbury sub-markets absorbing a development pipeline without precedent in the city's infrastructure history. Sydney accounts for approximately 65% of Australia's upcoming data centre power capacity per ResearchAndMarkets Australia colocation portfolio analysis of July 2025, and the land acquisition activity concentrated in the corridor bounded by the M7 Motorway, the Great Western Highway, and the Western Sydney Airport at Badgerys Creek confirms that international capital has identified Western Sydney as the primary AI infrastructure hub for the entire Asia Pacific time zone. The NSW Government's Investment Delivery Authority endorsed all 15 data centre projects submitted to it in March 2026, including NEXTDC's AUD 7 billion S7 hyperscale AI facility at Eastern Creek with approximately 550 MW capacity, a fast-track approval that signals the NSW Government's commitment to positioning Sydney as the regional AI compute capital per ACS Information Age reporting of April 2026. For instance, in 2025, NEXTDC Limited, Australia, acquired a 258,000 square metre plot of land at Eastern Creek, Sydney for AUD 353 million to develop its S7 hyperscale data centre campus, designed to serve hyperscale cloud providers in a new availability zone within the Sydney market with OpenAI as the first confirmed major customer, requiring cooling and energy infrastructure at a scale including liquid cooling systems capable of operating at 40 kW to 100 kW per rack for AI GPU clusters that makes S7 one of the most technically demanding data centre infrastructure projects in Australian history per NEXTDC company disclosures and Baxtel facility data. These are some of the key factors driving revenue growth of the market.

AirTrunk, Australia, owned by Blackstone and Canada Pension Plan Investment Board since the USD 16.1 billion acquisition in 2024, entered a preliminary agreement to acquire the ISPT-developed Kemps Creek campus at 706 to 752 Mamre Road in Western Sydney, a AUD 5 billion development planned to include six four-storey data centre buildings spanning 400,000 square metres with capacity from 600 MW up to 1 GW across 24 data halls per Data Center Dynamics reporting of May 2026, incorporating 936 cooling units, 852 diesel backup generators, and 7,488 cabinets of lithium-ion battery storage per NSW planning documents. The NSW Government's Investment Delivery Authority endorsed the Kemps Creek campus as one of its 15 fast-tracked data centre projects in March 2026, and AirTrunk is pursuing an AUD 4.3 billion construction financing package to fund the build per Construction Review Online reporting of June 2026. Goodman Group, Australia, and Starwood Capital Group, United States, alongside Doma Infrastructure Group and Telstra InfraCo, Australia, announced a strategic agreement to develop a carrier-neutral data centre campus in Minchinbury, Western Sydney, with Starwood and Doma responsible for financing, development, construction, and ongoing management per Baxtel and Data Center Dynamics verified trade press, adding a further hyperscale-grade cooling and energy infrastructure asset to the Western Sydney corridor. Macquarie Data Centres' AUD 350 million IC3 Super West facility in Macquarie Park and Equinix's SY series of campuses across the Sydney metropolitan area complete the city's institutional-grade colocation and cooling infrastructure ecosystem, collectively drawing AUD 10 billion-plus of committed capital to Sydney's data centre and cooling infrastructure market between 2024 and 2027. These are some of the key factors driving revenue growth of the market.

However, the Sydney cooling and energy infrastructure real estate market faces structural constraints that will govern the pace of delivery and the operational economics of committed projects through the forecast period. Grid connection timelines are the primary constraint, with Transgrid and Endeavour Energy facing connection request backlogs in the Western Sydney corridor that extend power delivery timelines for new data centre projects, requiring operators to invest in on-site generation infrastructure including diesel backup generator banks 852 generators are planned at Kemps Creek alone that increase capital costs and create ongoing fuel logistics requirements for facilities that cannot immediately access full grid capacity at the scale their IT load demands. Water scarcity is an increasingly material operational constraint in the Western Sydney data centre corridor, where the AirTrunk Kemps Creek campus is estimated to consume approximately 22.4 million litres of water annually per NSW planning documents, a volume that is attracting scrutiny from the NSW Parliamentary inquiry into data centres commenced in May 2026 and from Greater Western Sydney water utilities managing demand across a rapidly growing residential and industrial base. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, create upward pressure on NSW wholesale electricity prices given gas-fired generation's role in the state's electricity mix during peak demand periods, increasing the energy cost component of data centre cooling and energy infrastructure operations in a market where cooling systems for AI GPU clusters operate at maximum load continuously rather than cyclically. Planning community objections to the scale, noise, visual impact, and infrastructure demand of hyperscale data centre campuses in Western Sydney residential and agricultural corridors are extending development approval timelines for projects beyond the NSW IDA fast-track mechanism. These factors substantially limit Sydney cooling and energy infrastructure real estate market growth over the forecast period.

Western Sydney has not made a strategic decision to become Australia's AI infrastructure capital. It has had that decision made for it by geography, grid infrastructure, and land availability. The M7 Motorway corridor, the proximity to Transgrid's Western Sydney transmission assets, and the availability of 50-to-100-hectare industrial zoned sites that are impossible to assemble in Sydney's east or inner west have created an irresistible convergence of factors for hyperscale operators who need 400,000 square metres and 1 GW of power in a single location. NEXTDC saw this in 2024 when it paid AUD 353 million for Eastern Creek. AirTrunk saw it when it agreed to acquire Kemps Creek at AUD 5 billion before a shovel had broken ground. Amazon, Google, and Microsoft are all acquiring land in the same corridor. The cooling and energy infrastructure investment embedded in this pipeline is not a five-year forecast. It is a ten-year capital commitment that has already been authorised at board level and is in the ground. The question is not whether Sydney becomes the Southern Hemisphere's primary AI compute hub. It is whether the grid infrastructure arrives in time to power it." Troview Intelligence Head of Sydney Cooling and Energy Infrastructure Research

SEGMENT INSIGHTS

| 03 | SUBMARKET ANALYSIS |

Six Submarkets Defining Sydney Cooling and Energy Infrastructure Geography

| AirTrunk Campus Value | Planned Capacity | Cooling Units | Battery Storage |

| AUD 5 Billion (ISPT development) | 600 MW to 1 GW across 24 data halls | 936 cooling units (planning documents) | 7,488 cabinets lithium-ion batteries |

Kemps Creek in Western Sydney is the site of the largest single data centre cooling and energy infrastructure development ever proposed in Australia, anchored by the ISPT-developed AirTrunk campus at 706 to 752 Mamre Road for which AirTrunk, owned by Blackstone and Canada Pension Plan Investment Board, has entered a preliminary acquisition agreement conditional on full planning permission. The campus, designed across six four-storey data centre buildings spanning 400,000 square metres with 24 data halls, incorporates 936 cooling units, 852 diesel backup generators, 18,000 kilolitres of diesel storage, and 7,488 cabinets of lithium-ion battery storage per planning documents submitted to the NSW Department of Planning, with AirTrunk pursuing an AUD 4.3 billion construction financing package to fund the build per Construction Review Online reporting of June 2026. The Mamre Road corridor in Kemps Creek is adjacent to the Western Sydney Airport at Badgerys Creek, the Western Sydney Aerotropolis, and the M7 Motorway interchange, providing the logistics, fibre, and road infrastructure access required for a campus-scale data centre development while remaining within the Western Sydney transmission corridor served by Transgrid's high-voltage assets.

EASTERN CREEK NEXTDC AI FACTORY HUB OPENAI'S AUSTRALIAN ANCHOR

| NEXTDC S7 Site | S7 Planned Capacity | Anchor Tenant | NSW IDA Status |

| 258,000 sqm at AUD 353M, acquired 2024 | ~550 MW, AUD 7 Billion AI facility | OpenAI first major customer confirmed | Endorsed March 2026 for fast-track delivery |

Eastern Creek is the site of NEXTDC's S7 hyperscale AI facility, the single largest data centre capital commitment by an Australian-headquartered operator in the company's history, designed to provide a new hyperscale cloud availability zone in the Sydney market for Amazon Web Services, Microsoft Azure, and Google Cloud complementing NEXTDC's existing S1 Artarmon, S2 Macquarie Park, and S3 Alexandria facilities. NEXTDC acquired the 258,000 square metre Eastern Creek plot for AUD 353 million in 2024 and subsequently announced the site would host an AUD 7 billion data centre development with approximately 550 MW of capacity, endorsed by the NSW Government's Investment Delivery Authority in March 2026 for fast-track planning delivery. OpenAI, United States, was confirmed as the S7's first major customer, a client whose AI inference infrastructure requirements at scale mandate liquid cooling systems capable of managing GPU cluster deployments at 40 kW to 100 kW per rack, and whose commitment to a Sydney availability zone creates sustained, long-term demand for the cooling and energy infrastructure investment at Eastern Creek through the forecast period.

| NEXTDC S4 | Starwood / Doma / Telstra | Submarket Appeal | Energy Specification |

| Horsley Park, 124,000 sqm, new availability zone | Carrier-neutral campus, Minchinbury | M7 access, substation proximity, fibre connectivity | Dual-active power feeds, renewable sourcing |

Horsley Park and Minchinbury form the core of the Western Sydney data centre corridor's second tier, absorbing demand from hyperscale and enterprise operators who require campus-scale colocation adjacent to the Kemps Creek and Eastern Creek primary development zone but whose operational timelines, power requirements, or lease structures differ from the largest hyperscale campus developments. NEXTDC's S4 data centre at Horsley Park, covering approximately 124,000 square metres and located near a major electricity substation with telecommunications and public infrastructure access, is designed to provide data centre services to hyperscale cloud providers in a new Sydney availability zone complementing the existing S1, S2, and S3 network per NEXTDC company and Baxtel facility data. Starwood Capital Group, United States, Doma Infrastructure Group, and Telstra InfraCo, Australia, announced a strategic agreement to develop a carrier-neutral data centre in Minchinbury, with Starwood and Doma providing financing, development, construction, and ongoing management bringing an additional carrier-neutral cooling and energy infrastructure asset to the Western Sydney corridor and extending the interconnection ecosystem westward from the legacy Macquarie Park and Gore Hill colocation hubs.

| Macquarie DC IC3 Super West | Equinix SY Campuses | Cooling Profile | Tenant Profile |

| AUD 350M, NABERS-rated, renewable-powered | SY1 to SY9, carrier-neutral, enterprise focus | Air-cooled existing, liquid cooling retrofit pipeline | Financial services, enterprise, government agencies |

Macquarie Park and Gore Hill are Sydney's established inner-metropolitan colocation markets, hosting Equinix's SY series of IBX campuses, Macquarie Data Centres' IC3 Super West facility, and Global Switch's Sydney campus, serving the enterprise, financial services, and government tenant base that requires proximity to the Sydney CBD, direct connectivity to the Sydney Internet Exchange, and carrier-neutral access to the full range of Australian and international network providers. Macquarie Data Centres' AUD 350 million IC3 Super West facility in Macquarie Park began construction in November 2024 with advanced cooling systems, NABERS-rated energy efficiency infrastructure, and on-site solar power generation, establishing the cooling and energy infrastructure specification standard for inner-metropolitan Sydney data centre development in the AI era. Equinix's SY1 to SY9 campus network provides the densest interconnection ecosystem in the southern hemisphere, with cooling infrastructure primarily based on air-cooled systems installed between 2005 and 2020 that are now subject to retrofit assessment as AI-native enterprise tenants require rack densities above the specifications of existing cooling infrastructure.