| TROVIEW INTELLIGENCE | Sao Paulo Cell Tower and Telecom Infrastructure Market | Q2 2026 |

| TROVIEW INTELLIGENCE · CITY INTELLIGENCE REPORT |

By District Zone · By Tower Type · By Carrier · By Technology Generation

Zone Profiles: Centro and Paulista · Faria Lima and Berrini · Belo Horizonte Corridor · Guarulhos and ABС · Sao Paulo Metropolitan Periphery

Sao Paulo is Latin America's largest metropolitan area with 22 million residents across Greater Sao Paulo and the country's largest single mobile market, hosting the highest tower site density in Brazil, the most advanced commercial 5G deployment in Latin America per market intelligence, the primary office of SBA Communications Brazil's subsidiary SBA Torres Brasil Limitada which holds approximately 30% of SBA's global 44,500-plus site portfolio with Brazil site leasing representing 13.3% of total revenues per SEC filings, and commanding Brazil's highest lease rates and most active amendment revenue cycle as Vivo, TIM, and Claro compete to deploy mid-band 5G across the metropolis's 7,946 square kilometre municipal territory confirming Sao Paulo as the highest-revenue, highest-value, and most strategically prioritised single-city cell tower infrastructure market in Latin America.

| Standard License: USD 2,200 | Enterprise License: USD 9,500 |

MARKET SYNOPSIS

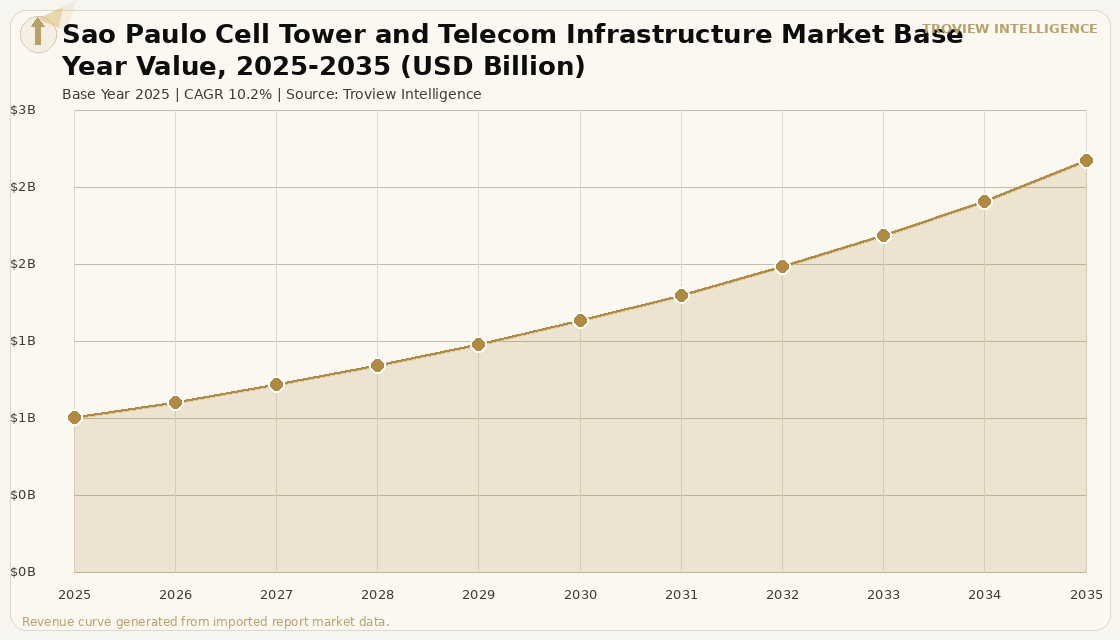

The Sao Paulo cell tower and telecom infrastructure market size was USD 891.4 Million in 2025 and is expected to register a revenue CAGR of 10.2% during the forecast period, reaching USD 2.37 Billion by 2035. The 2025 market estimate is grounded in Sao Paulo's position as approximately 28% of the Brazil cell tower and telecom infrastructure market reflecting the city's dominant share of Brazil's premium mobile subscriber base, corporate enterprise wireless demand, and 5G deployment activity applied to the verified Brazil market base anchored in SBA Communications' SEC disclosures confirming Brazil as approximately 30% of the company's global tower portfolio and 13.3% of total site leasing revenue. Sao Paulo is Latin America's largest metropolitan area with 22 million residents across Greater Sao Paulo, generating the highest single-city mobile data demand in the region from a population that combines the highest per-capita data consumption of any Brazilian metropolitan centre with the corporate enterprise, financial services, media, and technology sector workforce that drives the premium business-to-business wireless data traffic anchoring above-market tower lease rates in the city's central business districts. Market revenue growth is anchored in the structural reality that Sao Paulo's 5G commercial deployment, while the most advanced in Brazil, is still in the early stages relative to the midband and high-band coverage densification required to serve the city's 22 million residents at the data speeds that 5G promises, creating a sustained multi-year amendment and colocation revenue cycle for towercos holding Sao Paulo tower infrastructure as MNOs accelerate their 5G coverage programmes. Vivo, as the market-leading MNO and Sao Paulo's most active 5G investor, leads the amendment activity in the Faria Lima and Berrini financial district corridors where corporate enterprise 5G demand is highest, generating incremental colocation and amendment revenue for SBA Communications, American Tower, and Highline do Brasil towers in these premium urban precincts. For instance, SBA Communications Corporation's SBA Torres Brasil Limitada subsidiary, operating approximately 30% of the company's global tower portfolio in Brazil per SBA 10-K and 10-Q SEC filings, with Sao Paulo representing the highest-value concentration of sites in that Brazilian portfolio, generates above-portfolio-average site leasing revenue from Sao Paulo's colocation economics where multiple carrier tenants share infrastructure whose proximity to Brazil's highest-density corporate and consumer mobile subscriber base supports lease rates above the national average per SBA Communications 2025 Annual Report and SEC filings. These are some of the key factors driving revenue growth of the market.

American Tower Corporation's Sao Paulo tower portfolio, operated through the company's Brazilian subsidiary as part of its international operations spanning Argentina, Brazil, Chile, Colombia, Costa Rica, Mexico, Paraguay, Peru, and other Latin American markets per American Tower 424B2 SEC filing, represents one of the company's primary urban tower clusters in Latin America, with Sao Paulo's corporate enterprise and premium consumer mobile demand generating the type of above-market annual escalators and multi-tenant colocation economics that characterise the company's highest-performing international tower markets. Highline do Brasil, a DigitalBridge Group portfolio company, operates as Brazil's third leading towerco and holds a material Sao Paulo tower portfolio that serves all three major MNOs in the metropolitan market. The growing deployment of small cells and distributed antenna systems alongside macro towers in Sao Paulo's highest-density corporate and entertainment districts including the Faria Lima financial corridor, the Av. Paulista boulevard, the Vila Olimpia technology and media district, and the Guarulhos airport commercial zone creates incremental new investment opportunities for tower operators that supplement macro tower site leasing revenue with small cell and DAS infrastructure income in locations where macro tower coverage capacity is insufficient for peak-hour data demand. These are some of the key factors driving revenue growth of the market.

However, the Sao Paulo cell tower and telecom infrastructure market faces structural constraints that limit the pace of 5G deployment and premium revenue per site growth through the forecast period. Sao Paulo's municipal government has historically imposed strict visual pollution ordinances that restrict new tower construction in residential neighbourhoods and historic districts, requiring towercos to pursue rooftop installations, stealth towers, and small cell deployments that carry higher per-site development costs and longer approval timelines than conventional macro tower builds in less regulated environments, creating the same community resistance and zoning complexity challenge that FCC rulemaking data confirms in US urban markets but amplified by Sao Paulo's specific municipal permitting requirements. The Brazilian real's volatility against the US dollar creates currency translation risk for SBA Communications, American Tower, and Highline do Brasil whose capital is denominated in USD while their Sao Paulo lease revenues are in BRL, requiring active currency hedging programmes that add complexity and cost to the financial management of Sao Paulo tower portfolios for international towercos. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, affect Sao Paulo tower infrastructure operating costs through petroleum product price transmission to diesel generator fuel in Sao Paulo's frequent power outage events and backup power requirements for telecommunications-grade continuous availability, with the city's electrical grid reliability challenges creating above-average backup generator utilisation relative to tower sites in markets with more stable grid power. These factors substantially limit Sao Paulo cell tower and telecom infrastructure market growth over the forecast period.

Sao Paulo's tower market is the highest-revenue-per-site city in Latin America, and it is not particularly close. The corporate tenants in the Faria Lima financial district generate more mobile data per square kilometre than anywhere else in South America. The financial services firms, multinational corporate headquarters, and technology companies clustered between Av. Faria Lima and Av. Berrini consume bandwidth at densities comparable to Midtown Manhattan or the City of London. Vivo, TIM, and Claro all want to be the carrier that a Goldman Sachs or a Google Brazil employee uses for their corporate device. That competitive dynamic generates the amendment activity new MIMO radios, additional spectrum bands, power upgrades that drives the incremental rent escalation for SBA Torres Brasil and American Tower in those corridors at rates materially above the contractual 3% annual escalator. The 5G upgrade cycle in Sao Paulo's premium corporate districts is not scheduled to stop when the first 5G radio goes live. It accelerates as each carrier watches the other install more equipment on the same tower and realises they need to match it to maintain enterprise account competitiveness. That is the Sao Paulo tower market for the next decade: an amendment cycle that never ends, in the most data-intensive city in the Western Hemisphere." Troview Intelligence Head of Sao Paulo Cell Tower and Telecom Infrastructure Research

SEGMENT INSIGHTS

| 03 | ZONE ANALYSIS |

Five Zones Defining Sao Paulo's Cell Tower Infrastructure Geography

| Paulista Daily Footfall | Tower Type | 5G Status | Visual Ordinance |

| One of Latin America's highest 1M+/day estimated | Rooftop macro, stealth structures, building-integrated | Commercial 5G live Vivo, TIM, Claro all deployed | Strict municipal restrictions stealth/rooftop required |

The Centro and Av. Paulista zone constitutes the highest-density macro tower infrastructure corridor in the Sao Paulo cell tower market, encompassing the city's historic commercial heart from Praca da Se through Paulista to Pinheiros, where the combination of government offices, cultural institutions, corporate headquarters, retail destinations, and the extraordinary daily footfall of one of Latin America's most traffic-intense commercial boulevards creates mobile subscriber density that requires above-average tower site counts per square kilometre to maintain service quality. Sao Paulo's municipal visual pollution ordinances which restrict the visual impact of telecommunications structures in densely occupied commercial areas require towercos to deploy rooftop-mounted macro antennas, stealth tower designs integrated into architectural elements, and small cell infrastructure rather than conventional ground-based lattice or monopole towers, increasing per-site development costs but creating location-specific infrastructure advantages for early movers who secure premium rooftop rights-of-way in Centro and Paulista's dense urban canyon environment. The commercial 5G deployment by Vivo, TIM, and Claro across Paulista and Centro is generating the first wave of 5G amendment revenue for towercos in this zone, with massive MIMO radios, additional 3.5 GHz spectrum band equipment, and power upgrades to existing 4G macro sites representing the amendment activity that compounds above-contractual escalator organic revenue growth.

FARIA LIMA AND BERRINI FINANCIAL DISTRICT LATIN AMERICA'S HIGHEST ARPU ENTERPRISE CORRIDOR PREMIUM TOWER ECONOMICS

| Tenant Profile | Tower Revenue | 5G Priority | Small Cell Pipeline |

| Goldman Sachs, JP Morgan, BTG Pactual, major PE and VC firms | Premium enterprise ARPU drives above-market amendment rates | Carriers' #1 São Paulo deployment priority enterprise SLAs | Corporate campus DAS and street-level small cells |

The Faria Lima and Berrini financial district corridor is the highest-revenue-per-tower-site zone in the Sao Paulo cell tower market and the primary driver of above-market lease amendment activity by all three Brazilian MNOs, as the concentration of Brazilian and international financial institutions including BTG Pactual, Itau BBA, Goldman Sachs, JP Morgan, Credit Suisse, and the complete roster of major Brazilian private equity and venture capital managers creates enterprise-class 5G service demand that carriers are willing to invest disproportionately to serve, generating lease amendment revenue that exceeds the corporate financial district tower investment economics of any other Latin American city. Vivo's enterprise sales team specifically targets Faria Lima corporate accounts with premium 5G enterprise connectivity agreements that include dedicated network slicing, quality-of-service guarantees, and enterprise-grade SLA commitments the kind of service quality commitments that require dense 5G infrastructure with multiple redundant carrier options at every office building, making Faria Lima tower rights-of-way the most competitively contested real estate in the Brazilian tower market. The corridor's high-rise tower building stock creates favourable rooftop and building-integrated antenna installation economics, with building management companies receiving rooftop lease income from towercos while carriers access the height advantage and geographic positioning that rooftop installations provide in the compact Faria Lima canyon streetscape.

| Guarulhos Airport | ABC Region | Tower Profile | 5G Opportunity |

| Brazil's largest airport 47 million annual passengers | Santo Andre, Sao Bernardo, Sao Caetano manufacturing | Ground-based macro, airport DAS, industrial IoT | 4G to 5G upgrade cycle + industrial IoT private wireless |

The Guarulhos airport and ABC industrial corridor zone constitutes the highest-volume tower infrastructure zone in Greater Sao Paulo's metropolitan periphery, anchored by Guarulhos International Airport Brazil's largest airport and Latin America's second-largest whose 47 million annual passengers generate sustained indoor and outdoor mobile data demand from the airport terminal complex, surrounding logistics parks, and the commercial corridor along the Dutra highway connecting Guarulhos to Sao Paulo's metropolitan core. The ABC region encompassing Santo Andre, Sao Bernardo do Campo, and Sao Caetano do Sul is Brazil's historical manufacturing heartland, home to major automotive, petrochemical, and industrial manufacturing operations that are the primary drivers of industrial Internet of Things connectivity investment in the Greater Sao Paulo metropolitan market. Volkswagen, Ford, Mercedes-Benz, and their supply chain operations in the ABC region are emerging as enterprise private wireless network customers whose investment in Industry 4.0 automation requires dedicated 5G private network infrastructure either through dedicated private network slices with MNOs or through standalone campus private wireless deployments that represent a new incremental revenue stream for towercos and equipment vendors beyond the traditional carrier lease model.

| Population Zone | Tower Profile | 4G Status | Revenue Driver |

| 12M+ residents in peripheral zones mass market | Macro lattice and monopole full coverage mandate | 4G LTE well established 5G coverage gap | High site count, lower per-site revenue than Centro/Faria Lima |

The Sao Paulo metropolitan periphery zones Zona Norte, Zona Sul, Zona Leste, and the border municipalities of the Greater Sao Paulo Expanded Metropolitan Region constitute the largest geographic coverage area of the Sao Paulo cell tower market, encompassing the residential neighbourhoods, social housing estates, and periurban commercial zones that house more than 12 million of the metropolitan area's 22 million residents and generate the highest volume of mobile subscriber lease relationships in the city's tower portfolio. The peripheral zones' mass-market mobile subscriber base served by Vivo, TIM, and Claro through prepaid and value-segment post-paid plans generates lower ARPU per subscriber than the premium corporate corridors of Centro and Faria Lima, but drives the highest tower site count requirements in the metropolitan market as Anatel coverage obligations and carrier competitive network quality commitments require continuous 4G LTE and 5G coverage extension across all inhabited areas of the metropolitan zone. The Zona Leste in particular, encompassing the densely populated districts of Itaquera, Penha, and Ermelino Matarazzo with populations comparable to a medium-sized Brazilian city, requires sustained investment in tower densification to maintain acceptable service quality as subscriber data consumption per device increases through the 4G to 5G transition.

| Zone Character | Tower Challenge | Network Profile | Startup Economy |

| Historic residential, cultural institutions, cafes, startups | Heritage visual ordinances, high-density residential zoning | Dense small cell deployment + rooftop macro | Growing tech startup ecosystem fixed wireless 5G demand |

The Centro Expanded and Vila Mariana zone encompassing the neighbourhoods of Liberdade, Bela Vista, Paraiso, Vila Mariana, and the bohemian streets south of Paulista toward Vila Madalena represents Sao Paulo's cultural and residential core where historic heritage protections, residential land use dominance, and the visual character that makes these neighbourhoods desirable as both residential and artisanal commercial locations creates the most complex tower permitting environment in the metropolitan market. The growing concentration of technology startups, co-working spaces, creative economy firms, and digital media companies in the Vila Madalena, Pinheiros, and Bixiga corridors generates enterprise-quality mobile data demand from a demographic that requires premium 5G connectivity for cloud-based work platforms, video collaboration, and real-time software development tools, creating above-average ARPU from a segment that is difficult to serve at adequate quality without dense small cell infrastructure that navigates the zoning restrictions of these heritage-sensitive residential zones.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from verified company SEC filings, SBA Communications Annual Report 2025, American Tower earnings disclosures, and Inside Towers Intelligence.