| TROVIEW INTELLIGENCE | Northern Virginia Data Centre Real Estate Market | Q2 2026 |

| TROVIEW INTELLIGENCE · CITY INTELLIGENCE REPORT |

By Submarket · By Asset Type · By Tenant Sector · By Power Tier

Submarket Profiles: Ashburn · Sterling · Manassas · Leesburg · Stafford County · Prince William County

Northern Virginia recorded 1,102.0 MW of net absorption in 2025, a 144% increase from 2024, while its total inventory expanded to 4,039.6 MW 37% more than a year prior and nearly 3.5 times the combined inventory of all secondary US data centre markets yet ended the year with only 21.5 MW of available supply, a vacancy rate of 0.5%, and asking rates for 10 MW-plus requirements of USD 155 to USD 185 per kW per month, with the majority of 2026 capacity already committed under pre-lease agreements extending into 2027, as Amazon Web Services operated 156 sites in the market, purchased 189 acres in Prince William County and 100 acres in Leesburg, and Vantage Data Centers announced a USD 2 billion campus investment in Stafford County a market that is not running out of demand but is running out of land and power.

| Standard License: USD 2,200 | Enterprise License: USD 9,500 |

MARKET SYNOPSIS

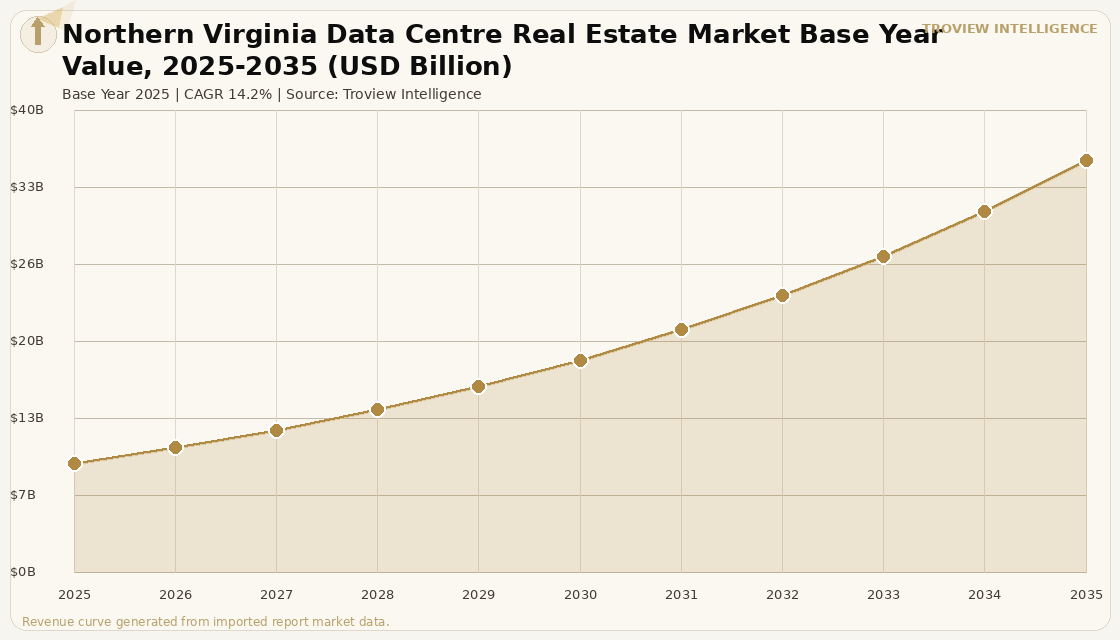

The Northern Virginia data centre real estate market size was USD 9.42 Billion in 2025 and is expected to register a revenue CAGR of 14.2% during the forecast period, reaching USD 35.47 Billion by 2035. Market revenue growth is supported by Northern Virginia's structural position as the world's highest-density data centre market, defined by the MAE-East internet exchange node in Ashburn that anchors 337 active peering points, the concentration of Amazon Web Services, Microsoft Azure, Google Cloud, and Meta hyperscale campuses across Loudoun, Prince William, and Stafford counties, and the I-95 corridor's emergence as a spine of new campus development as the Ashburn core reaches saturation. CBRE's H2 2025 North America Data Center Trends report records Northern Virginia's total inventory at 4,039.6 MW at year-end 2025, a 37% increase year-on-year, with net absorption of 1,102.0 MW in 2025 representing a 144% increase from 2024 and the single largest annual absorption figure recorded by any data centre market globally. For instance, in January 2025, STACK Infrastructure, United States, announced a 1 GW Stafford Technology Campus spanning 500 acres and 19 buildings in Stafford County, Virginia, targeting hyperscale and AI-native tenants requiring contiguous power blocks above 50 MW who cannot secure equivalent space in the saturated Ashburn core, per STACK Infrastructure company announcement of January 2025. These are some of the key factors driving revenue growth of the market.

Average monthly asking rates for 250 to 500 kW requirements in Northern Virginia rose 6.5% year-on-year to USD 195.94 per kW per month in H2 2025, the fourth consecutive annual increase, while requirements of 10 MW and above reached USD 155 to USD 185 per kW per month, a 30% increase from the USD 120 to USD 140 per kW per month range in 2023 per CBRE market data. Amazon Web Services, United States, operates 156 data centre sites in the Northern Virginia market, the largest single-operator concentration in any global data centre market, and purchased 189 acres for data centre development in Prince William County and 100 acres in Leesburg in early 2025, confirming its continued capacity expansion in a market where it already controls the majority of operational hyperscale infrastructure. Digital Realty Trust, Inc., United States, identified Manassas, Virginia as the top contributor to its above-1 MW hyperscale signings in Q4 2025 per its Q4 earnings disclosures, reflecting the southward migration of new capacity from the Ashburn core toward Prince William County and the I-95 corridor markets where land and power remain accessible. Preleasing activity in Northern Virginia has extended to capacity planned for delivery in 2027 and beyond, with large single-building and campus-sized requirements of 15 MW to 20 MW in contiguous blocks effectively impossible to satisfy from existing and near-term planned supply per CBRE H1 2025 Northern Virginia market profile. These are some of the key factors driving revenue growth of the market.

However, the Northern Virginia data centre real estate market faces supply constraints that are structural rather than cyclical, and that limit the pace of revenue growth and the market's ability to accommodate demand without prolonged lead times. Dominion Energy's batching system for new data centre interconnection requests has extended power delivery timelines for new projects to three to five years in the Loudoun County core, creating a queue that no amount of developer capital can accelerate, as transmission infrastructure expansion requires state regulatory approvals, environmental permitting, and physical construction that operates on utility timescales rather than data centre investment timescales. Land scarcity in the Ashburn and Sterling core submarkets has exhausted the supply of shovel-ready sites adjacent to existing high-capacity substations, forcing development into Leesburg, Manassas, Prince William County, and Stafford County where substation capacity must be purpose-built for each new campus rather than shared with existing infrastructure. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, create upward pressure on US natural gas prices that feeds into PJM grid power costs in Virginia, directly affecting the operating economics of the 4,039.6 MW of inventory that depends on PJM for grid power. These factors substantially limit Northern Virginia data centre real estate market growth over the forecast period.

Northern Virginia is the only data centre market in the world where the vacancy rate is 0.5%, the majority of 2026 capacity is already pre-leased, asking rates for large deployments have increased 30% in two years, and the largest operators are still buying land and announcing new campuses. That combination does not exist in Frankfurt, Singapore, or Tokyo. It exists only in Ashburn and the surrounding Loudoun County corridor because of a network effect that took 30 years to build from the MAE-East exchange point and that no new market can replicate. Investors who understand that they are not buying a building they are buying access to 337 peering points, proximity to Amazon's largest concentration of infrastructure on earth, and a lease with a hyperscaler that is contractually committed to Northern Virginia regardless of which alternative markets it also expands into will price Northern Virginia data centre real estate accordingly. The right comparison is not office at 4% or logistics at 5%. The right comparison is irreplaceable infrastructure with a 25-year income stream." Troview Intelligence Head of Northern Virginia Data Centre Real Estate Research

SEGMENT INSIGHTS

| 03 | SUBMARKET ANALYSIS |

Six Submarkets Defining Northern Virginia Data Centre Geography

| Peering Points | Vacancy H2 2025 | Dominant Operators | New Development |

| 337 active (MAE-East heritage) | Effectively zero no available blocks | Equinix, Digital Realty, CoreSite | Land exhausted retrofits and densification only |

The Ashburn core submarket is the highest-density data centre location on earth, anchored by the MAE-East internet exchange node that places Ashburn at the centre of 337 active peering points and creates an interconnection ecosystem that no alternative data centre location can replicate. Equinix's Ashburn campus is among its highest-revenue IBX complexes globally, while Digital Realty's multi-building campus on the Dupont Fabros acquisition footprint adjacent to Equinix provides the largest contiguous wholesale campus in the core submarket. Land in the Ashburn core is effectively exhausted, with no shovel-ready sites of meaningful scale remaining adjacent to existing high-capacity substations, forcing all new hyperscale development into the surrounding submarkets of Sterling, Leesburg, Manassas, and the I-95 corridor. Existing Ashburn operators are responding with densification strategies including liquid cooling retrofits that increase power density per square foot on established campus footprints, allowing incremental capacity additions without requiring new land.

| Sterling Profile | Leesburg Activity | Key Appeal | Power Status |

| QTS, Infomart, Cyxtera, CyrusOne campuses | Amazon 100 acres acquired Mar 2025; Google Dulles expansion | Proximity to Ashburn peering, land still available | Substation access constrained, development queues |

Sterling and Leesburg represent the primary overflow markets for Ashburn-adjacent data centre development, offering proximity to the Ashburn peering ecosystem, existing fibre infrastructure shared with the Loudoun County corridor, and access to land parcels that remain viable for campus-scale development where Ashburn is fully built out. Sterling hosts QTS Data Centers (Blackstone), Infomart, Cyxtera, and CyrusOne campuses, concentrating wholesale and enterprise colocation supply on the western edge of the Ashburn ecosystem. Leesburg is the most active development zone in the Northern Virginia market outside of Prince William County and Stafford, with Amazon Web Services acquiring 100 acres near the Dulles Greenway in March 2025 and Google's earlier 58-acre acquisition for a data centre campus confirming that hyperscalers view Leesburg as the near-term expansion zone of choice within the core Loudoun County corridor. Power substation capacity in both markets is constrained by the cumulative load of the wider Loudoun County build-out, extending new development timelines and reinforcing Dominion Energy's batching system pressure on the market.

| AWS Land Acquisition | Digital Realty Q4 2025 | Prince William Supervisors | Development Profile |

| 189 acres, Prince William County, 2025 | Manassas top contributor to 1+ MW signings | Amazon campus approved near Unity Reed HS, Feb 2025 | Hyperscale campus scale, build-to-suit dominant |

Prince William County and Manassas represent the primary active hyperscale expansion front in Northern Virginia, combining available land parcels of 100 to 500 acres with I-95 corridor fibre infrastructure and proximity to Dominion Energy transmission assets in the county. Amazon Web Services' acquisition of 189 acres in Prince William County in 2025 and the February 2025 approval by Prince William County supervisors of an Amazon campus near Unity Reed High School with community amenity provisions confirm that the county has adopted a pro-development posture for data centres that distinguishes it from the more constrained Loudoun County planning environment. Digital Realty Trust identified Manassas as the top contributor to its above-1 MW hyperscale signings in Q4 2025 per its Q4 earnings disclosure, reflecting the concentration of new hyperscale lease activity in the Prince William County corridor as tenants accept 2026 and 2027 delivery timelines in exchange for securing contiguous capacity that does not exist in the Ashburn core.

| STACK Campus | Vantage Investment | I-95 Connectivity | Development Stage |

| 1 GW, 500 acres, 19 buildings Jan 2025 announcement | USD 2 billion campus, 929,000 sq ft, Stafford County | Direct route to Richmond data centre expansion | Early-stage, lowest land cost in NoVA corridor |

Stafford County and the I-95 corridor south toward Richmond represent the largest contiguous land opportunity remaining within the Northern Virginia data centre catchment, with STACK Infrastructure's January 2025 announcement of a 1 GW campus on 500 acres and Vantage Data Centers' USD 2 billion commitment to a 929,000 square foot campus in Stafford County establishing the submarket as the most ambitious next-generation hyperscale development zone in the Americas. The Stafford County submarket offers land costs a fraction of the Ashburn core, I-95 motorway fibre infrastructure that maintains national connectivity, and Dominion Energy transmission capacity that has not yet been fully committed to the existing Loudoun County load, providing relative power access advantages over the northern parts of the corridor. Development at this scale 1 GW on a single campus requires build-to-suit hyperscale pre-commitments before financial close, and the pace at which operators are pre-leasing 2027 and 2028 capacity in the constrained Ashburn market makes Stafford County a credible destination for the next generation of hyperscale commitments that the core market physically cannot accommodate.