By Structure Type · By Province · By Application · By Material

Province Spotlights: Ontario · Alberta · British Columbia · Quebec

Ontario leads Canada's manufactured housing market with 30.6 percent of 2025 sales, British Columbia's Bill 44 and Bill 25 now mandate 3 to 6 units per lot implicitly favouring modular typologies, and Firm Capital and SunPark Communities LP agreed in April 2026 to acquire 1,752 MHC sites across Alberta and Saskatchewan for CAD 218 million a transaction that confirms institutional capital is treating Canadian land-lease communities as a core real estate asset class.

MARKET SYNOPSIS

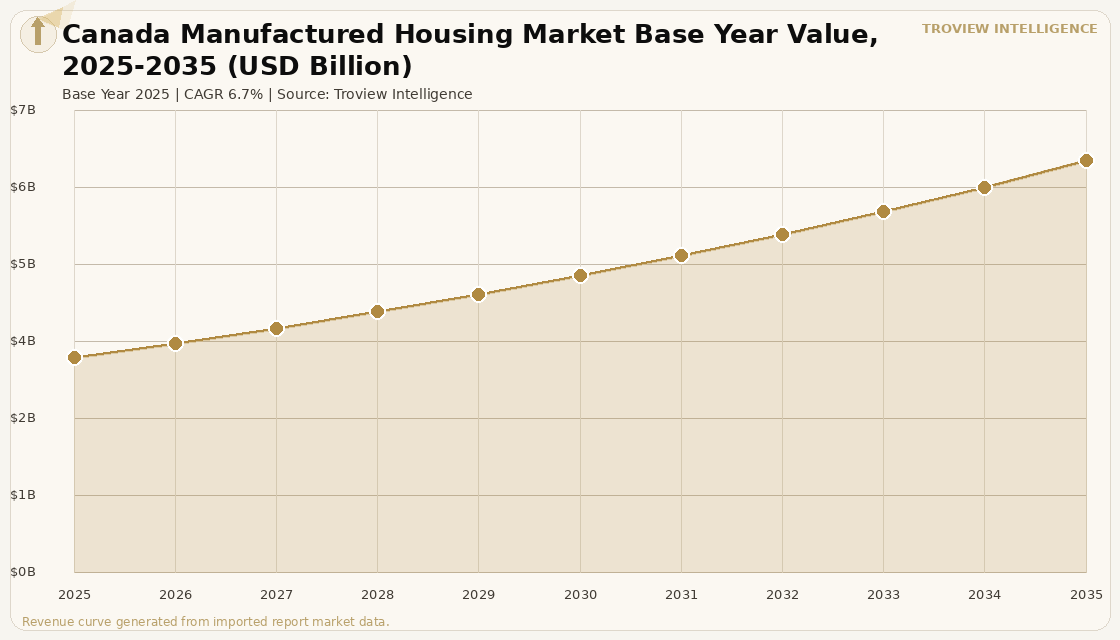

The Canada manufactured housing market size was USD 3.28 Billion in 2025 and is expected to register a revenue CAGR of 6.7% during the forecast period, reaching USD 6.29 Billion by 2035. Manufactured and modular homes are factory-built dwellings produced to CSA A277 standard, which grants full building code equivalency and conventional mortgage eligibility when certified, and transported to their installation sites. Multi-section homes captured 53.7 percent of the 2025 Canadian market by volume, with single-family applications accounting for 73.5 percent of shipments as first-time buyers in Ontario and British Columbia increasingly turn to multi-section units as entry-level ownership through conventional construction becomes less attainable. Ontario led all provinces with 30.6 percent of 2025 sales per Natural Resources Canada housing start data. Alberta is forecast to expand at the highest provincial CAGR, driven by energy-sector community housing demand and the province's 2024 guidance encouraging municipalities to remove zoning barriers for factory-built formats.

Canada's federal government made manufactured housing central to its housing supply agenda in 2025. Budget 2025 announced the USD 13 billion Build Canada Homes programme and directed volume-purchase contracts to modular producers, creating a guaranteed production floor that reduces the investment risk for new factory capacity. Skilled-trade wages now exceed CAD 85 per hour in British Columbia and Ontario, making the factory's 35 percent reduction in on-site labour inputs a direct financial advantage for both private developers and government housing agencies. Lumber tariffs imposed in October 2025 raised framing costs by 12 to 18 percent, yet manufacturers can hedge through bulk purchasing and forward contracts that smaller site builders cannot access. For instance, in April 2026, Firm Capital Property Trust and SunPark Communities LP, Canada, agreed to acquire 11 manufactured housing communities comprising 1,752 MHC sites across Alberta and Saskatchewan from Cove Communities for CAD 218 million, with a further single Alberta site acquired for CAD 8.5 million, bringing SunPark's total portfolio to 2,572 MHC sites and signalling that the institutionalisation of the Canadian land-lease community sector has moved from early-stage to mainstream capital allocation, per Real Estate News Exchange reporting of April 2026. These are some of the key factors driving revenue growth of the market.

However, the Canada manufactured housing market faces structural constraints. Municipal zoning in many Ontario and British Columbia cities continues to restrict manufactured home placement to designated parks or rural zones, limiting the sector's ability to serve urban affordability needs in the markets where the housing deficit is most acute. Financing conditions for manufactured homes, while improving under CMHC's broadened factory-built housing standards, remain less uniform than for site-built homes, with some lenders applying higher rates or lower loan-to-value ratios for non-foundation units. Lumber tariff volatility introduced by the October 2025 tariff adjustments creates input cost uncertainty for manufacturers whose order books extend 12 to 18 months ahead. Provincial building code variance, while diminishing as Health Canada's harmonised standards compress regional differences, still creates compliance costs for producers shipping into multiple provinces. These factors substantially limit Canada manufactured housing market growth over the forecast period.

Canada's manufactured housing market has entered a new phase. For decades it was a rural affordability product quietly serving resource communities and retirees. What is different now is that federal volume-purchase contracts, provincial zoning reform, and institutional MHC acquisitions above CAD 200 million are happening simultaneously. The sector is not just responding to affordability pressure. It is being structurally incorporated into Canada's mainstream housing supply strategy for the first time. The question is whether factory capacity can scale fast enough to meet the procurement volumes being committed." Troview Intelligence Head of Canada Manufactured Housing Research

SEGMENT INSIGHTS

By Structure Type

Multi-section manufactured homes are expected to account for a significantly large revenue share in the Canada manufactured housing market during the forecast period.

Based on structure type, the Canada manufactured housing market is segmented into single-section homes, multi-section homes, modular homes, and park model units. Multi-section homes accounted for 53.7 percent of 2025 market volume and are the primary growth format in Ontario and British Columbia, where affordability-driven buyers need floor plans large enough to compete with entry-level condominiums. Modular homes built to CSA A277 certification are the fastest-growing segment, as certification grants full building code equivalency and access to conventional mortgage financing, removing the financing disadvantage that historically constrained manufactured housing to buyers outside the mainstream lending system. Park model units, recreational dwellings under 400 square feet, serve seasonal occupancy in Quebec lake regions and British Columbia retirement clusters where retirees seek low-maintenance seasonal homes at price points well below site-built equivalents.

By Province

Ontario is expected to account for a significantly large revenue share in the Canada manufactured housing market during the forecast period.

Based on province, the Canada manufactured housing market is segmented into Ontario, Alberta, British Columbia, Quebec, the Prairies, and Atlantic Canada. Ontario leads all provinces with 30.6 percent of 2025 market sales, driven by the concentration of housing demand in the Greater Toronto Area and the shortage of affordable site-built entry-level homes that has redirected first-time buyer interest toward factory-built formats. Alberta is expected to register the fastest provincial CAGR, driven by energy-sector communities in Fort McMurray, Grande Prairie, and Lloydminster where site-built delivery costs remain prohibitive and manufactured homes are the primary housing format for a transient and growing workforce. British Columbia's Bill 25, passed in 2025, mandates that municipalities approve 3 to 6 units per lot by June 2026, creating zoning conditions that favour modular multi-unit formats in Vancouver's constrained land market.

By Application

Residential single-family applications are expected to account for a significantly large revenue share in the Canada manufactured housing market during the forecast period.

Based on application, the Canada manufactured housing market is segmented into residential single-family, residential multi-family, and non-residential including emergency, disaster relief, and remote workforce housing. Residential single-family applications account for 73.5 percent of Canadian shipments, reflecting the dominance of owner-occupied demand from first-time buyers and retirees. Residential multi-family is the fastest-growing segment, as Assembly Corp., Element5, and Smart Modular Canada are delivering modular apartment buildings for city affordable housing programmes and private rental developers. Element5's CAD 107 million production expansion announced in October 2025, which will double its mass timber manufactured housing capacity, directly targets the multi-family pipeline from Toronto's modular housing initiative and Ontario's government procurement channels.

Four Provinces Shaping Canada's Manufactured Housing Market

| 2025 Market Share | 30.6% of Canada shipments | Key Policy | Bill 109, Toronto Modular Housing Initiative |

| Primary Demand | First-time buyers, affordable housing agencies | Key Builders | Assembly Corp., Element5, Smart Modular Canada |

Ontario is Canada's largest manufactured housing market, accounting for 30.6 percent of 2025 national sales per Natural Resources Canada housing data. First-time buyers in the Greater Toronto Area are increasingly considering multi-section manufactured homes as conventional construction entry-level prices have moved beyond reach. The City of Toronto's Modular Housing Initiative committed to 1,000 new modular homes under the HousingTO 2020-2030 Action Plan, with 216 supportive housing units delivered across four completed buildings as of early 2026 per City of Toronto data. Assembly Corp., a mass timber modular builder, has become a key delivery partner for the City's affordable housing programme. Ontario's housing supply crisis has created strong government procurement demand that is underwriting factory production volumes independent of private market cycles.

| Key Demand Drivers | Energy sector workforce, remote communities, retirees | Policy | 2024 provincial guidance removing zoning barriers for factory-built homes |

| Key Operators | ATCO Ltd and Alta-Fab, SunPark Communities (post-acquisition) | MHC Acquisition Activity | SunPark portfolio expansion to 2,572 sites after CAD 218M deal |

Alberta is the fastest-growing manufactured housing province, driven by energy sector workforce housing in Fort McMurray and the Athabasca oil sands corridor where site-built construction costs and logistics make manufactured homes the only practical housing format. ATCO Ltd, through its ATCO Structures division, and Alta-Fab supply modular and manufactured units to oil sands operators and remote industrial sites across the province. The province's 2024 guidance actively encourages municipalities to remove zoning barriers for factory-built housing, creating a more permissive planning environment than Ontario or British Columbia. Institutional investors have recognised Alberta MHCs as stable income assets. Firm Capital Property Trust and SunPark Communities' April 2026 acquisition of 10 Alberta and Saskatchewan communities for CAD 218 million confirms the depth of institutional demand for land-lease community exposure in western Canada.

| Key Policy | Bill 44 (2023), Bill 25 (2025): 3-6 units per lot by June 2026 | Trade Wage Pressure | CAD 85/hour skilled trades; factory cuts on-site labour 35% |

| Key Markets | Vancouver, Kelowna, Victoria, Fraser Valley | Demand Profile | First-time buyers, downsizing retirees, seasonal park model |

British Columbia's manufactured housing market is being reshaped by the most significant provincial zoning reform in a generation. Bill 44 (2023) and Bill 25 (2025) together mandate that municipalities permit 3 to 6 units per lot by June 2026, a requirement that implicitly favours modular typologies capable of meeting density requirements on constrained urban lots at lower cost than site-built construction. Skilled-trade wages exceeding CAD 85 per hour in Metro Vancouver make factory production's labour efficiency advantage its single most important commercial attribute in British Columbia. The seasonal park model segment, serving retirees in Okanagan and Vancouver Island retirement communities, maintains steady demand independent of urban market cycles. The province remains the primary market for CSA A277-certified modular multi-unit housing that can be financed conventionally and placed in urban residential zones.

| Key Segment | Seasonal park model units in lake regions | Language | French-language regulatory compliance required from manufacturers |

| Affordable Housing | Growing government procurement pipeline | Key Operators | Multi-section dealers, regional prefab builders |

Quebec's manufactured housing market is anchored by seasonal park model demand in the Laurentian and Eastern Townships lake regions, where retirees and second-home buyers purchase compact manufactured units for seasonal occupancy at price points well below conventional construction. Quebec's distinct building code environment, which requires French-language compliance documentation and provincial certification for some factory-built housing categories, has historically insulated the market from competition by English-speaking producers based in Ontario and western Canada. The provincial government's social housing deficit has generated growing affordable housing procurement interest in factory-built formats, particularly for rapid-deployment supportive housing that can be installed on cleared sites faster than conventional construction. Quebec's cold climate construction window of eight months or fewer provides the same timeline advantage to factory-built formats that is driving adoption in Alberta and Ontario.