By Operator Type · By City Tier · By Property Format · By Tenure

City Spotlights: Shanghai · Beijing · Shenzhen · Hangzhou

China's rental housing market faced an unusual dislocation in mid-2025: individually owned rental listings in 55 major cities surged to 618,000 units in July, up 12.2% year-on-year, while rents fell for 11 consecutive months at an average of RMB 31.65 per square metre per month per China Real Estate Information Corp. data, and Shanghai rents declined 12% yet institutionally managed rental housing in Beijing and Shanghai maintained 90% occupancy through February 2025 per CREIS data and the September 2025 national housing rental ordinance, China's first administrative-level rental market regulation, is establishing the compliance framework required to accelerate foreign institutional capital into a sector that added market-oriented rental housing to the public REIT eligible asset list in 2024.

MARKET SYNOPSIS

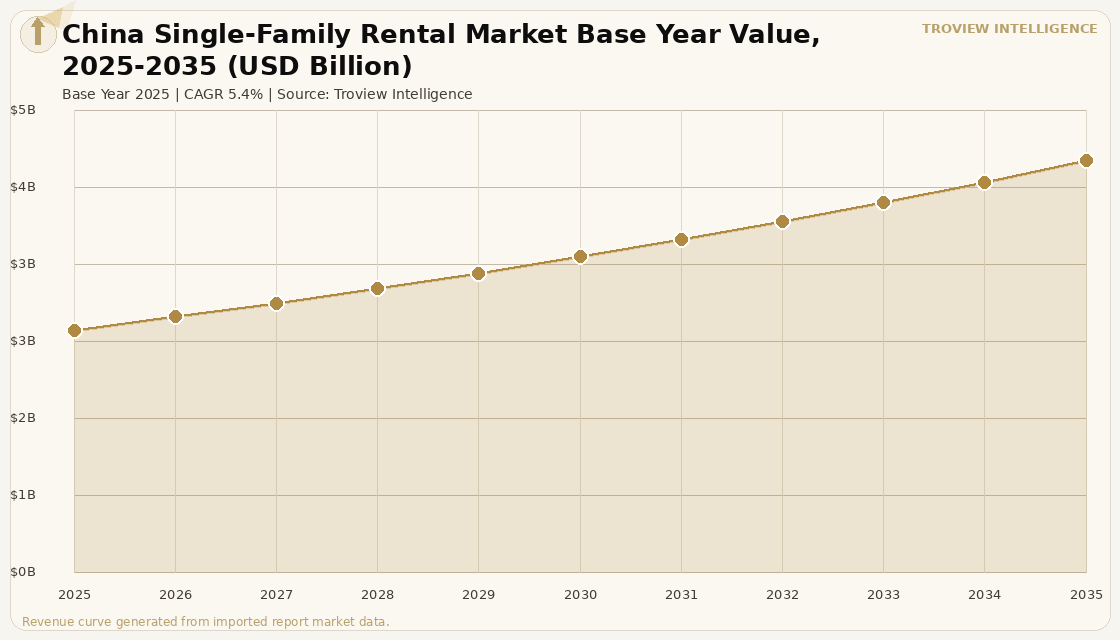

The China single-family rental market size was USD 2.68 Billion in 2025 and is expected to register a revenue CAGR of 5.4% during the forecast period, reaching USD 4.55 Billion by 2035. Market revenue growth is supported by the Chinese government's sustained commitment to expanding institutionally managed rental housing as a pillar of housing policy, with over 200 housing leasing-related policies introduced at the local government level in 2024 focusing on regulation enhancement and market stability per Global Property Guide's analysis of China housing policy. China's Ministry of Housing and Urban-Rural Development unveiled the country's first national administrative-level regulation for the rental market in September 2025, a milestone that introduced standardised lease structures, platform operator licensing requirements, and tenant protection provisions that formalise the legal foundation for institutional rental housing at national scale. The Chinese government added market-oriented rental housing to the list of eligible assets for China's public REITs in 2024 per the China Securities Regulatory Commission's expansion of the public REIT eligible asset categories, creating a liquidity pathway for developers and operators holding institutional rental housing portfolios and enabling exit strategies that had previously been unavailable in the sector. As of February 2025, occupancy rates for institutionally managed rental housing in Beijing and Shanghai remained at approximately 90% per China Real Estate Index System data, confirming that professionally managed and operated properties maintain stable occupancy even as the broader rental market faces oversupply pressure from unsold residential inventory entering the rental pool.

China's institutionally managed rental housing sector has undergone two distinct development phases. The first phase, from 2015 to 2021, was characterised by rapid expansion of long-term apartment rental platforms including Ziroom and Beike-affiliated operators that adopted asset-light models, leasing properties from individual owners and sub-leasing to tenants at a spread. Multiple platform failures and the homelessness of thousands of tenants that resulted from operator collapses led to a regulatory tightening cycle that fundamentally changed the operating model. The second phase, from 2022 onward, has been characterised by asset-heavy or en-bloc institutional investment by state-owned enterprises, pension funds, and foreign investors that own the underlying properties directly rather than relying on sub-leasing spreads. Shanghai recorded 14 en-bloc transactions with a total transaction volume of RMB 7.2 billion in 2023, up 18% year-on-year per China Real Estate Index System data, confirming the scale of institutional capital entering the sector through direct property acquisition. Invesco's analysis of the China rental housing market published in April 2025 confirmed that most institutional investors expect stabilised yield on cost ranging from 4.5% to 5.5% and that 51% of investors expected further cap rate compression of up to 50 basis points over the following five years. For instance, in 2024, China's Securities Regulatory Commission approved market-oriented rental housing as an eligible asset class for public REITs, enabling Longfor Group Holdings, Shanghai-based, to structure its rental housing portfolio into a REIT-eligible vehicle that provides institutional investors with a regulated, liquid instrument for China rental housing exposure, per CSRC official policy documentation. These are some of the key factors driving revenue growth of the market.

However, the China single-family rental market faces structural constraints that meaningfully moderate revenue growth and institutional investor confidence. China Real Estate Information Corp. reported that the number of individually owned rental units listed in 55 major cities surged to 618,000 in July 2025, up 12.2% year-on-year and 7% from June, the highest level in nearly three years, while average rents fell for 11 consecutive months to RMB 31.65 per square metre per month per Caixin Global's reporting of CRIC data published August 2025. Shanghai's rental market saw a 12% rent decline, driven by the flood of unsold residential inventory entering the rental pool as developers and individual owners sought rental income from units that could not be sold at prevailing prices. Residential new starts in China fell 19.8% year-on-year to 429.84 million square metres in 2025 per China's National Bureau of Statistics, confirming that the property market contraction is reducing the future pipeline of housing stock while simultaneously pushing existing inventory into the rental market. S&P Global Ratings expects China's nationwide primary property sales to fall by 10-14% in 2026 to approximately RMB 7.2-7.6 trillion, suggesting the oversupply dynamic affecting rental rents will persist through the forecast period. These factors substantially limit China single-family rental market growth over the forecast period.

China's institutional rental housing market is threading the needle between two powerful forces. On one side, 90% occupancy in professionally managed Beijing and Shanghai projects confirms that high-quality, well-located, institutionally operated rental product has genuine and sustained demand from China's white-collar workforce, international professionals, and upwardly mobile urban residents who have made a deliberate choice to rent rather than purchase. On the other side, 618,000 individual rental listings flooding the market and 11 consecutive months of rent declines confirm that the second tier of rental supply individually-owned, poorly managed, unsold inventory converted to rentals is creating a price war that is depressing market rents even as institutional operators maintain occupancy. The September 2025 rental ordinance and the public REIT approval are the policy signals that China is building the institutional infrastructure to support the sector long-term. The near-term noise is real but it is separate from the structural opportunity." Troview Intelligence Senior Analyst, China Residential Rental Markets

SEGMENT INSIGHTS

By Operator Type

State-owned enterprise-backed rental housing platforms and en-bloc institutional operators are expected to account for a significantly large revenue share in the China single-family rental market during the forecast period.

Based on operator type, the China single-family rental market is segmented into state-owned enterprise rental housing platforms, foreign institutional en-bloc investors, private Chinese developers operating rental assets, asset-light rental management platforms, and individual and family landlords. State-owned enterprise-backed operators dominate the institutional segment, supported by government land allocation policies that direct R4 rental housing land to state-controlled entities and by dedicated lending facilities from the People's Bank of China targeting rental housing development. Foreign institutional investors including pension funds and sovereign wealth vehicles account for an increasing share of en-bloc transactions in Shanghai and Beijing, with Invesco's April 2025 analysis confirming that international capital is entering the sector through both direct investments and co-investment partnerships with local state-owned operators who provide land access and regulatory relationship management. Asset-light platforms including Ziroom remain operational at scale but are expanding under the tighter regulatory framework introduced by the September 2025 national rental ordinance, which requires platform operator licensing and financial reserves that reduce the solvency risk that triggered multiple platform failures in the 2021 regulatory crackdown.

By City Tier

Tier 1 cities including Shanghai, Beijing, Shenzhen, and Guangzhou are expected to account for a significantly large revenue share in the China single-family rental market during the forecast period.

Based on city tier, the China single-family rental market is segmented into Tier 1 cities, New Tier 1 cities including Hangzhou, Chengdu, Wuhan, and Xi'an, Tier 2 cities, and lower-tier cities. Tier 1 cities dominate institutional rental revenue and transaction volume, with Shanghai recording 14 en-bloc rental housing transactions at RMB 7.2 billion in 2023 per China Real Estate Index System data, and Beijing and Shanghai institutional rental occupancy holding at approximately 90% through early 2025 per CREIS data while broader market rents declined due to individual landlord oversupply. New Tier 1 cities including Hangzhou and Chengdu are the fastest-growing segment by new institutional supply delivery, as government pilot programmes in cities including Shenzhen and Hangzhou extended subsidised lending to gig-economy workers for homeownership, per China's National Bureau of Statistics housing policy data, while simultaneously expanding the affordable rental housing supply through state-backed operators that generate demand for institutionally managed product from upwardly mobile renters not yet eligible for ownership schemes.

By Property Format

Centralised apartment building rental communities are expected to account for a significantly large revenue share in the China single-family rental market during the forecast period.

Based on property format, the China single-family rental market is segmented into centralised long-term apartment communities, distributed scattered-site residential units, villa and single-family detached rental properties, employee dormitory-style housing, and serviced apartment rental formats. Centralised long-term apartment communities dominate institutional revenue in China, as the concentration of units within a single building or campus enables the operational efficiency, cost leverage, and professional management quality that generates the 4.5% to 5.5% stabilised yield on cost expected by institutional investors per Invesco's China rental housing market analysis of April 2025. Scattered-site single-family and villa rental properties are the fastest-growing segment in Shanghai's premium western districts and Beijing's Shunyi villa corridors, where expatriate professionals and senior Chinese executives require detached house formats with private garden space and proximity to international schools that centralised apartment communities cannot provide, generating above-market rents that compensate for the management complexity of operating geographically dispersed individual units.

Four Cities Shaping China's Single-Family Rental Market

| 2023 En-Bloc Transactions | RMB 7.2B total, 14 deals (+18% YoY) | Rent Decline 2025 | 12% (CRIC data, August 2025) |

| Future Supply Concentration | 58% in Pudong, Minhang, Qingpu by end-2025 | Premium District Rents | Jing'an, Xuhui: highest in city |

Shanghai is China's largest institutional single-family and rental housing market, recording 14 en-bloc transactions with a total volume of RMB 7.2 billion in 2023, up 18% year-on-year per China Real Estate Index System data, confirming the scale of institutional capital entering the sector through direct property acquisition in the city. The institutional rental housing supply in Shanghai is geographically concentrated, with Pudong District, Minhang District, and Qingpu District collectively expected to account for 58% of the city's total rental housing stock by end-2025 per the institutional supply pipeline analysis, while future supply within the Inner Ring Road accounts for only 1.5% of total pipeline, confirming the suburban character of new institutional rental development. Shanghai's rental market experienced a 12% rent decline in 2025 per China Real Estate Information Corp. data, driven by unsold residential inventory flooding the rental pool, yet institutionally managed projects with operating histories above six months maintained occupancy of approximately 89% to 90% per China Real Estate Index System project-level occupancy tracking, confirming the bifurcation between professionally managed stock and the broader market. Premium districts including Jing'an, Xuhui, and the French Concession area command the highest rents in Shanghai, attracting the white-collar professional and expatriate tenant base that underpins institutional rental revenue in the city's Inner Ring Road locations.

| Institutional Occupancy | ~90% (CREIS, February 2025) | Policy Role | Key pilot city for rental housing regulation |

| Demand Driver | State-owned enterprise workforce, returnees, students | Key Operator Presence | Ziroom, state-backed rental platforms |

Beijing is China's second-largest institutional rental housing market and a primary pilot city for the government's rental housing policy experiments that preceded the September 2025 national rental ordinance. As of February 2025, occupancy rates for institutionally managed rental housing in Beijing remained at approximately 90% per China Real Estate Index System data, driven by strong unmet demand from white-collar workers, freelancers, and students employed in the technology and professional services clusters of Zhongguancun, Sanlitun, and the Central Business District. Beijing's regulatory environment has been more active than any other Chinese city in shaping rental market rules, with the municipal government introducing multiple pilot measures on rental registration, lease standardisation, and platform operator licencing ahead of the national ordinance. The Beijing rental market is supported structurally by the large floating population non-Beijing hukou holders residing in the city who are ineligible for public housing and represent the primary tenant base for professional rental operators. Beijing's rental housing development pipeline is concentrated in the periphery of the Fifth Ring Road, delivering large-format centralised rental communities in districts including Tongzhou, Daxing, and Fangshan that are connected to central employment via the expanded Beijing Metro system.

| Policy Innovation | Gig-economy subsidised loan pilot 2025 | Key Tenant Profile | Technology sector workers, Huawei, Tencent employees |

| Price Performance | New-home prices rising YoY (core locations 2026) | Vacancy Risk | Lower than average; supply below demand in premium stock |

Shenzhen is China's most dynamic rental housing market by tenant quality and technology sector concentration, with the workforce of Huawei, Tencent, DJI, and hundreds of deep technology and advanced manufacturing companies generating sustained demand for professionally managed rental housing in the Nanshan, Futian, and Longhua districts adjacent to Shenzhen's primary technology employment corridors. In 2025, a government pilot programme in Shenzhen extended subsidised loans at rates near 2.85% to gig-economy workers a cohort exceeding 200 million nationally per China's National Bureau of Statistics labour force data with early data showing a 15% rise in new borrower accounts in Shenzhen during Q1 2025, per the pilot programme's results reported by China's Ministry of Housing and Urban-Rural Development. Shenzhen's new-home prices continued to rise year-on-year in core locations as of April 2026 per the China Real Estate Index System's 100-city price survey, distinguishing the city from the national trend of declining new-home prices and confirming its status as one of China's most supply-constrained premium residential markets. The innovation economy tenant base in Shenzhen has a distinctly younger age profile and higher income level than Beijing and Shanghai's broader rental market, generating demand for technology-enabled smart apartment formats that align with the digital-native preferences of engineering and product management professionals.

| Designation | New Tier 1 city, institutional rental growth pilot | Key Employers | Alibaba, NetEase, numerous tech scale-ups |

| Policy Support | Rental housing land allocation, subsidised developer financing | Cross-border Flows | Digital economy workforce driving premium rental demand |

Hangzhou is the fastest-growing institutional rental housing city in China's New Tier 1 category, driven by the concentration of Alibaba's global headquarters, NetEase, and a large ecosystem of e-commerce, fintech, and digital economy companies that collectively employ one of China's highest-earning private sector workforces outside Shanghai and Beijing. Hangzhou's government has designated rental housing land through the R4 allocation system and provided developer financing through the People's Bank of China's targeted lending facility for rental housing, creating an institutional-grade pipeline of purpose-built rental communities adjacent to Alibaba's Xixi campus and the city's expanding digital economy corridors. The city's digital economy workforce has a higher-than-average preference for professionally managed rental housing over homeownership due to frequent internal company relocations, equity compensation packages that reduce the urgency of property ownership as a wealth accumulation vehicle, and a generational shift in housing attitudes among technology professionals in their 20s and 30s. China's first pilot programme for Shenzhen-style gig-economy housing subsidies was extended to Hangzhou in 2025, per Ministry of Housing and Urban-Rural Development programme expansion disclosures, confirming the city's status as a laboratory for housing policy innovations that precede national adoption.