By Ownership Model · By Geography · By Property Type · By Tenant Segment

Invitation Homes and American Homes 4 Rent together own 145,000+ single-family rental homes in the United States, average occupancy held at 97.2% and 95.9% respectively through Q1 2025, and NCREIF funds now collectively own USD 7.5 billion in SFR assets up from USD 5.4 billion a year earlier as the build-to-rent pipeline delivers approximately 80,000 purpose-built units annually, around 8 to 10 percent of all US single-family housing starts, while Blackstone's acquisition of Tricon Residential in 2024 and China's September 2025 national housing rental ordinance signal that institutional capital and government policy are simultaneously reshaping single-family rental from a fragmented landlord market into a professionally managed global asset class.

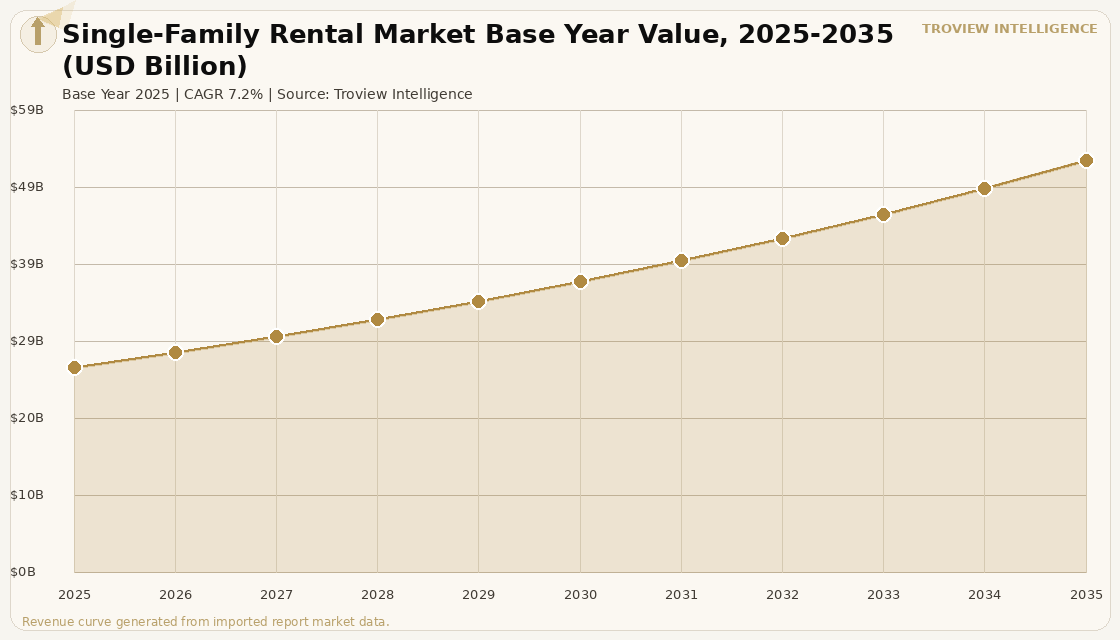

MARKET SYNOPSIS

The global single-family rental market size was USD 26.14 Billion in 2025 and is expected to register a revenue CAGR of 7.2% during the forecast period, reaching USD 52.44 Billion by 2035. Market revenue growth is supported by the sustained expansion of institutionally owned and professionally managed single-family rental portfolios across North America, the accelerating build-to-rent pipeline that is delivering purpose-built single-family communities at institutional scale, and the entry of sovereign wealth funds and pension capital into a sector that was dominated by individual landlords until the post-2012 institutional accumulation cycle. The US Census Bureau tracks approximately 15.7 million single-family rental units in the United States per BatchData analysis of Census Bureau data, representing 31.5% of all rental households and making single-family rental the second-largest rental housing type in the country. Invitation Homes and American Homes 4 Rent together held a combined portfolio of over 145,000 single-family rental homes as of Q1 2025 per each company's SEC filings, with Invitation Homes maintaining same-store occupancy of 97.2% and American Homes 4 Rent at 95.9%, and average tenant tenure at Invitation Homes extending to over 39 months per household per Capright REIT analysis of October 2025. The build-to-rent sector is now delivering approximately 80,000 purpose-built single-family rental units annually, representing 8 to 10 percent of all single-family housing starts in the United States per National Association of Realtors and US Census Bureau construction permit data, confirming the sector's transition from scattered-site acquisitions to purpose-designed communities.

Institutional capital concentration is accelerating rapidly in a market that remains predominantly small-scale. NCREIF funds collectively held USD 7.5 billion in SFR assets in 2025, up from USD 5.4 billion a year earlier per the National Council of Real Estate Investment Fiduciaries' quarterly data, confirming that institutional pension capital is increasing its SFR allocation at a pace that outstrips the broader commercial real estate market. Blackstone completed its acquisition of Tricon Residential, a publicly traded Canadian company with approximately 38,000 SFRs in the United States and Canada, in 2024 per SEC filings and Tricon investor communications, consolidating the Tricon portfolio under Blackstone's real estate operating platform following its 2021 acquisition of Home Partners of America. The 2025 Gallup survey of US renters found the vast majority rented for economic reasons, with mortgage payments on a typical starter home exceeding equivalent rent by USD 1,091 per month per Arbor Realty Trust's August 2025 SFR Market Update compiled with Chandan Economics, confirming that affordability constraints are the primary structural driver of SFR demand and will remain intact as long as elevated mortgage rates or home prices persist. For instance, in Q2 2025, Invitation Homes, United States, acquired 1,040 homes for USD 350 million, focusing on newly-built properties in high-growth Sun Belt markets at a target investment yield of approximately 6%, per Invitation Homes Q2 2025 SEC filing, reflecting the strategic shift from large-block portfolio acquisitions to builder-partnership models that allow institutional SFR operators to add scale through the BTR pipeline rather than competing directly in an illiquid acquisition market. These are some of the key factors driving revenue growth of the market.

However, the global single-family rental market faces structural constraints that moderate revenue growth across the institutional operator segment. Year-end annual SFR rent gains averaged 2.9% in 2025, down from 4.1% in 2024 per Arbor Realty Trust's SFR Investment Trends Report Q4 2025 compiled with Chandan Economics, marking the most modest rent growth since 2015 as the supply of BTR completions and investor-to-renter conversions increased available single-family rental inventory in Sun Belt markets. The US Department of Housing and Urban Development's Comprehensive Housing Market Analysis confirms that housing affordability constraints that sustain rental demand also limit the income-growth potential of working-class SFR tenants, capping achievable rent growth at rates that may not cover cost inflation for property tax, insurance, and maintenance. Average homeowners insurance premiums have risen materially in high-risk markets including Florida, Texas, and coastal California, per the Federal Emergency Management Agency's National Flood Insurance Program premium adjustment data, compressing net operating income for institutional SFR operators with concentrated Sun Belt exposure. Legislative pressure on institutional SFR ownership is intensifying, with multiple US states and the federal executive considering restrictions on large investor purchases of single-family homes, creating a regulatory overhang that is already causing institutional investors to avoid less business-friendly jurisdictions. These factors substantially limit global single-family rental market growth over the forecast period.

The global SFR market is in a transition that mirrors what happened to multifamily apartments thirty years ago from fragmented individual ownership to institutionally managed, REIT-listed, purpose-built communities that are underwritten with the same rigour as office or industrial portfolios. The build-to-rent pipeline delivering 80,000 units per year in the US is the visible surface of this transition. The deeper signal is NCREIF funds growing SFR allocations from USD 5.4 billion to USD 7.5 billion in a single year. That is pension capital making a multi-decade commitment to single-family rental as an institutional asset class. The regulatory risk is real and the legislative pressure is building. But the structural driver a mortgage market that prices starter home ownership at USD 1,091 per month above the equivalent rent does not turn off quickly regardless of who sits in Washington." Troview Intelligence Head of Global Single-Family Rental Research

SEGMENT INSIGHTS

By Ownership Model

Institutional build-to-rent operators and large-portfolio SFR REITs are expected to account for a significantly large and growing revenue share in the global single-family rental market during the forecast period.

Based on ownership model, the global single-family rental market is segmented into publicly traded SFR REITs, private equity-owned institutional portfolios, build-to-rent specialist operators, individual and family landlords, and government-subsidised affordable rental housing. Publicly traded SFR REITs dominate institutional market revenue, with Invitation Homes reporting Q1 2025 new lease rate growth of 1.3% improving to 2.7% in April per SEC filings, and American Homes 4 Rent reporting April new lease growth of 3.9% with 4.1% same-store NOI growth for the period. Build-to-rent operators represent the fastest-growing ownership model, with approximately 80,000 purpose-built units delivered annually in the United States, around 8 to 10 percent of all single-family housing starts per National Association of Realtors permit data, as developers construct entire communities of rental homes with institutional amenities, HOA management, and lease flexibility that scattered-site landlords cannot replicate. Individual and family landlords own over 95% of US single-family rental units per BatchData analysis but are gradually losing market share to institutional operators in high-growth Sun Belt markets including Atlanta, Phoenix, Tampa, and Charlotte where Invitation Homes, AMH, and Tricon concentrations are highest.

By Geography

North America is expected to account for a significantly large revenue share in the global single-family rental market, while Asia Pacific is expected to register the fastest revenue CAGR during the forecast period.

Based on geography, the global single-family rental market is segmented into North America, Europe, Asia Pacific, and Middle East and Africa. North America dominates institutional SFR market revenue, underpinned by the US public SFR REIT infrastructure including Invitation Homes, American Homes 4 Rent, and the Blackstone-Tricon platform, and by the Federal Housing Finance Agency's National Mortgage Database confirming that 70.4% of US homeowners with mortgages carried rates below 5.0% in Q2 2025, anchoring a lock-in effect that suppresses housing supply turnover and sustains rental demand. Asia Pacific is expected to register the fastest revenue CAGR over the forecast period, driven by China's September 2025 national housing rental ordinance, the first administrative-level regulation for the rental market in the People's Republic, and by Australia's build-to-rent sector that received FIRB approval reforms enabling foreign capital to accelerate BTR development in Sydney, Melbourne, and Brisbane. Europe's institutionalised BTR sector, led by the United Kingdom, Germany, and the Netherlands, is scaling rapidly as pension funds and listed residential REITs deploy capital into purpose-built rental communities that address housing shortages in major European cities.

By Property Type

Detached single-family homes and purpose-built build-to-rent communities are expected to account for a significantly large revenue share in the global single-family rental market during the forecast period.

Based on property type, the global single-family rental market is segmented into detached single-family homes, build-to-rent townhouse and cottage communities, attached single-family homes, and small multi-unit structures within single-family zoning designations. Detached single-family homes dominate the existing rental inventory globally, comprising the historically accumulated stock of individual landlord-owned properties across the United States, Australia, Canada, and the UK that represents the broad base of the SFR market by unit count. Build-to-rent communities are the fastest-growing segment by new investment volume, as the purpose-designed format featuring uniform floorplans, centralised management offices, amenity packages, and professional maintenance enables institutional operators to achieve the economies of scale, technology leverage, and lease standardisation that scattered-site portfolios cannot provide. The share of single-family renters living in attached single-family homes increased in each of the past five years, reaching approximately 20% of all SFR households per US Census Bureau data, confirming the broadening of the SFR tenant base beyond traditional detached home formats.

REGIONAL ANALYSIS

NORTH AMERICA LARGEST

| US SFR Units (total) | 15.7M (BatchData / US Census Bureau 2025) | SFR REIT Combined Portfolio (INVH + AMH) | 145,000+ homes (Q1 2025 SEC filings) |

| NCREIF SFR AUM | USD 7.5B (2025, up from USD 5.4B year prior) | BTR Annual Delivery | ~80,000 units (8-10% of all SF housing starts) |

North America is the largest and most institutionally developed single-family rental market globally, anchored by Invitation Homes and American Homes 4 Rent as the two dominant publicly traded SFR REITs and by Blackstone's consolidated Tricon Residential platform following the 2024 acquisition. The US SFR market contains approximately 15.7 million rental units out of 86.5 million total single-family homes per BatchData analysis of US Census Bureau data, representing 31.5% of all US rental households. Institutional operators own less than 5% of total SFR units nationally but hold disproportionate market influence in Sun Belt metros including Atlanta, Phoenix, Charlotte, Tampa, and Dallas where portfolio concentrations exceed the national average per Cotality and Wall Street Journal market data. Arbor Realty Trust's SFR Investment Trends Report Q4 2025, compiled with Chandan Economics, documented year-end rent gains of 2.9%, occupancy stabilisation, and improving tenant retention as indicators of renewed operational strength after the rapid expansion phase. NCREIF funds' SFR allocation growing to USD 7.5 billion from USD 5.4 billion in a single year confirms accelerating institutional pension capital commitment to the asset class.

EUROPE GROWING BTR

| Leading Market | United Kingdom (PRS/BTR) and Germany (Mietrecht) | UK BTR Sector | Growing rapidly, institutional focus on regional cities |

| Key Operators | Grainger plc, CBRE Investment Management, Legal & General | Policy Driver | UK Renters Rights Act 2025, Germany rent brake extensions |

Europe's single-family and build-to-rent rental sector is expanding under sustained housing shortage pressure and policy frameworks that support long-term institutional tenancies. The United Kingdom's build-to-rent sector, tracked by the British Property Federation and MHCLG housing supply data, continued to deliver professionally managed rental communities across London, Manchester, Birmingham, and Edinburgh as institutional operators scaled in response to acute housing undersupply relative to population and employment growth. The UK Renters Rights Act 2025 strengthened tenant protections by abolishing no-fault evictions and introducing periodic tenancies as the default, increasing tenant security and tenure length in ways that benefit institutional BTR operators whose business models depend on long-duration, low-turnover tenancies. Germany's Mietrecht framework and rent brake extensions in Berlin, Hamburg, and Munich have constrained rent growth for existing tenancies but supported stable long-term occupancy for institutional operators managing new-build stock that enters the market at prevailing market rents. Grainger plc, the UK's largest listed residential landlord, expanded its professionally managed BTR portfolio with a focus on energy-efficient, amenity-rich communities in regional UK cities that attract the professional renter demographic targeted by institutional SFR operators.

ASIA PACIFIC FASTEST-GROWING

| China National Rental Ordinance | September 2025 (first administrative-level regulation) | Beijing/Shanghai Institutional Occupancy | ~90% (CREIS, February 2025) |

| China Public REIT Eligibility | Market-oriented rental housing added 2024 | Australia BTR Reform | FIRB foreign investment approval streamlined for BTR |

Asia Pacific is the fastest-growing single-family and institutionally managed rental region globally, driven by China's regulatory formalisation of the rental market, Australia's BTR investment reforms, and Japan's accelerating shift toward professional rental housing management platforms. China unveiled its first administrative-level regulation for the rental market in September 2025 per China's Ministry of Housing and Urban-Rural Development, marking a milestone in the formalisation of the private rental sector. As of February 2025, occupancy rates for institutionally managed rental housing in Beijing and Shanghai remained around 90% per China Real Estate Index System data, with market-oriented rental housing added to the eligible assets list for China's public REITs in 2024, enhancing liquidity and broadening exit strategies for institutional investors per China Securities Regulatory Commission disclosures. Australia's built-to-rent sector accelerated following FIRB approval reforms that reduced withholding tax rates for foreign institutional investors in BTR assets from 30% to 15% per the Australian Treasury's housing reform package, enabling international capital to flow into Sydney, Melbourne, and Brisbane BTR developments targeting the growing renter demographic priced out of ownership in coastal Australian cities.