By Structure Type · By Geography · By End-Use · By Material

Factory-built homes now account for roughly 7 to 10 percent of all new housing placements globally, delivering at half the build time of site construction, as the US Department of Housing and Urban Development announced plans to overhaul its manufactured housing programme including eliminating the chassis requirement, and Canada's USD 13 billion Build Canada Homes programme directed volume-purchase contracts to modular producers for the first time.

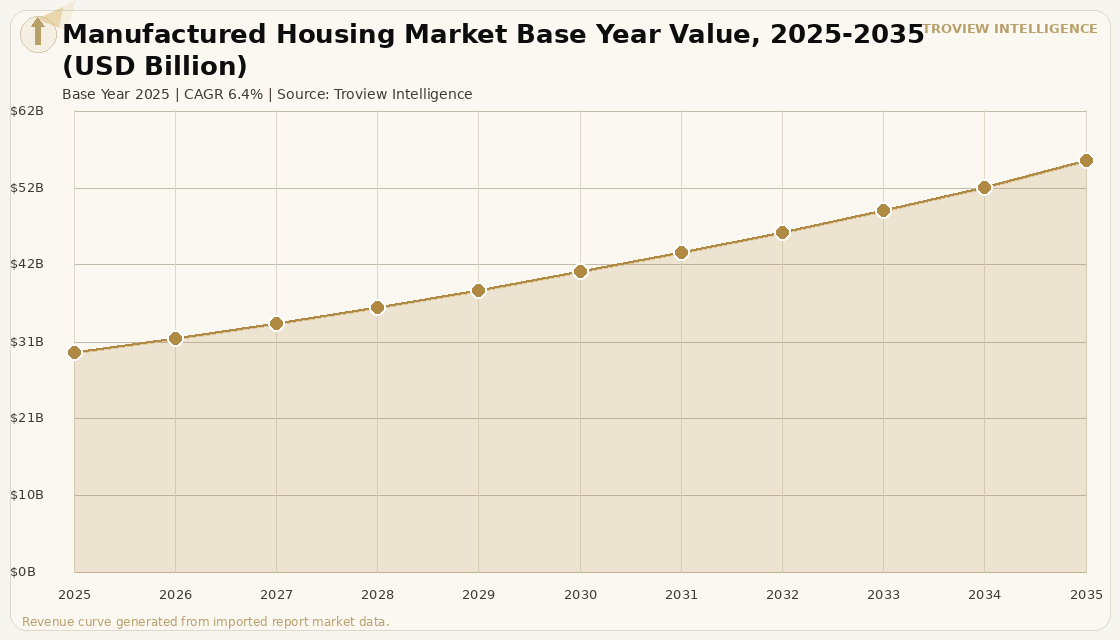

MARKET SYNOPSIS

The global manufactured housing market size was USD 29.84 Billion in 2025 and is expected to register a revenue CAGR of 6.4% during the forecast period, reaching USD 55.76 Billion by 2035. Manufactured homes are factory-built dwellings constructed in controlled production environments on permanent chassis and transported to their installation sites. Factory assembly compresses overall build timelines by 40 to 50 percent compared to traditional site construction and reduces on-site labour requirements by up to 35 percent, making manufactured housing the most scalable response to housing shortages in markets where skilled trade shortages and land costs are acute. North America generated approximately 40.8 percent of 2025 global revenue, led by the United States. The US recorded 103,000 manufactured home shipments in 2024, a 16 percent increase year-on-year per the Manufactured Housing Institute, confirming that demand is recovering from the post-2022 correction as affordability pressure redirects first-time buyers toward factory-built alternatives. The US Department of Housing and Urban Development announced plans to overhaul its manufactured housing programme in 2025, including eliminating the chassis requirement that has historically differentiated manufactured homes from other housing types, a reform that HUD Secretary Scott Turner specifically cited as central to solving the affordability and supply shortage.

The manufactured housing sector is attracting institutional capital at a pace not previously seen in the category. Land-lease manufactured housing communities, where residents own their homes but rent the land beneath them, are being acquired by institutional investors at scale because of their combination of stable rent revenue, low capital expenditure, and below-market rents that protect occupancy through economic downturns. Canada's federal Budget 2025 directed USD 13 billion through the Build Canada Homes programme toward volume-purchase contracts with modular producers, de-risking new plant investment and guaranteeing a production floor for factory-built housing supply. Factory schedules compress overall delivery by 40 to 50 percent because site preparation and module fabrication occur in parallel, a critical advantage in cold-climate markets where construction windows are limited to eight months annually. For instance, in April 2026, Firm Capital Property Trust and SunPark Communities LP, Canada, agreed to acquire 11 manufactured housing communities across Alberta and Saskatchewan comprising 1,752 sites from Phoenix-based Cove Communities for CAD 218 million, immediately expanding SunPark's portfolio to 2,572 MHC sites across Ontario, Alberta, and Saskatchewan and demonstrating the scale at which institutional capital is entering the Canadian land-lease community sector, per Real Estate News Exchange reporting of April 2026. These are some of the key factors driving revenue growth of the market.

However, the global manufactured housing market faces structural constraints that limit the pace of growth. Zoning restrictions continue to exclude manufactured homes from the majority of residential land in the United States and Canada, confining demand to a subset of available sites and limiting the product's ability to compete directly with site-built housing in high-demand urban markets. Financing access remains narrower than for site-built homes in most markets. Manufactured home buyers in the US typically rely on personal property loans, also known as chattel loans, which carry higher interest rates and shorter terms than conventional mortgages, increasing the effective cost of ownership relative to the purchase price advantage. Public perception of manufactured housing as lower-quality stock persists in many markets despite significant improvements in energy efficiency, design standards, and durability in the current generation of factory-built homes. These factors substantially limit global manufactured housing market growth over the forecast period.

Manufactured housing sits at the intersection of the two biggest structural problems in global residential real estate: an affordability crisis that conventional construction cannot solve at the speed required, and a skilled labour shortage that inflates the cost of every site-built home. Factory production addresses both. The institutional capital flowing into land-lease communities is not chasing a niche. It is recognising that manufactured housing is the only segment of the housing market where the product improves in quality while the price gap versus site-built construction widens rather than narrows." Troview Intelligence Head of Global Manufactured Housing Research

SEGMENT INSIGHTS

By Structure Type

Multi-section manufactured homes are expected to account for a significantly large revenue share in the global manufactured housing market during the forecast period.

Based on structure type, the global manufactured housing market is segmented into single-section homes and multi-section homes. Multi-section homes are built as two or more modules joined on-site, creating floor plans that exceed 2,000 square feet and compete directly with entry-level site-built construction in product quality and space. They account for 53.7 percent of the Canadian market by volume and are the preferred format for first-time buyers in Ontario and British Columbia where conventional construction affordability has deteriorated sharply. Single-section homes are expected to register the fastest growth rate in rural markets and remote resource communities where delivery logistics favour narrower units that can be transported by standard highway transport without oversize permits. Demand for single-section units concentrates in Alberta retirement communities, First Nations reserves in Canada, and off-grid rural US markets where pier foundations and faster installation reduce total cost relative to multi-section alternatives.

By Geography

North America is expected to account for a significantly large revenue share in the global manufactured housing market during the forecast period.

Based on geography, the global manufactured housing market is segmented into North America, Europe, Asia Pacific, and Middle East and Africa. North America dominates global market revenue, anchored by the United States' 103,000 annual shipments and Canada's institutional MHC acquisition cycle. Europe's manufactured housing market is led by Germany's modular construction sector and the United Kingdom's park home and static caravan industry, both of which serve retiree downsizers and holiday resort operators respectively. Asia Pacific is expected to register the fastest revenue CAGR over the forecast period, driven by Japan's established prefabricated housing industry and India's emerging factory-built affordable housing programmes under the Pradhan Mantri Awas Yojana, which has created government procurement channels for standardised housing units that factory production can serve at scale.

By End-Use

Residential single-family applications are expected to account for a significantly large revenue share in the global manufactured housing market during the forecast period.

Based on end-use, the global manufactured housing market is segmented into residential single-family, residential multi-family, and non-residential applications including commercial, educational, and emergency housing. Residential single-family accounts for 73.5 percent of shipments in Canada and a comparable share in the United States, driven by owner-occupied demand from first-time buyers, downsizing retirees, and rural households. The multi-family manufactured housing segment is expected to register the fastest CAGR through the forecast period, as modular construction technology enables the stacking and interlocking of manufactured modules into three-to-eight storey apartment buildings that achieve city building code compliance through CSA A277 certification in Canada and HUD code equivalency programmes in the United States.

REGIONAL ANALYSIS

NORTH AMERICA LARGEST

| US Shipments 2024 | 103,000 units (+16% YoY, Manufactured Housing Institute) | HUD Reform 2025 | Chassis requirement elimination proposed |

| Canada Build Canada Homes | USD 13 Billion modular volume-purchase programme | Key Institutional Move | Firm Capital / SunPark: CAD 218M Alberta-Saskatchewan MHC acquisition |

North America is the dominant manufactured housing market, anchored by the United States' national HUD code framework and Canada's federal housing programme that, for the first time, directed volume-purchase contracts to modular producers in Budget 2025. The US recorded 103,000 home shipments in 2024 per the Manufactured Housing Institute, recovering from the post-2022 correction as the monthly mortgage payment for a starter home exceeded equivalent rent by over USD 1,000, redirecting first-time buyers toward factory-built alternatives. HUD's 2025 announcement of planned programme overhauls including the chassis requirement elimination signals the most significant regulatory shift for the sector in decades. In Canada, skilled trade wages exceeding CAD 85 per hour in British Columbia and Ontario are making factory production's 35 percent reduction in on-site labour inputs increasingly compelling for developers and government housing agencies.

EUROPE RETIREE AND HOLIDAY

| UK Park Homes | Long-established sector, retiree downsizing primary driver | Germany | Modular construction advancing under energy retrofit mandates |

| Netherlands | Tinyhome and modular innovation hub | Policy Trend | EU Energy Performance of Buildings Directive accelerating factory builds |

Europe's manufactured housing market is structured around the United Kingdom's park home sector, Germany's modular construction industry, and a growing contingent of countries adopting off-site fabrication as a response to construction labour shortages and energy efficiency mandates. The UK's park home sector serves retirees downsizing from family homes to single-storey manufactured units on residential parks, underpinned by the Mobile Homes Act framework that governs site licensing and tenant protections. Germany's federal government has incorporated modular construction into its social housing expansion programme, with Deutsche Wohnen and municipal housing corporations procuring factory-built apartment modules to accelerate delivery against housing production targets. The EU Energy Performance of Buildings Directive, which requires all new buildings to meet zero-emission standards by 2028, is creating a structural advantage for factory-built homes where energy systems and insulation are installed under controlled conditions with consistent quality outcomes.

ASIA PACIFIC

| Japan | World's largest prefab sector by domestic market share (~15% of new homes) | India | PMAY affordable housing procurement creating factory-built pipeline |

| Australia | FIRB reforms enabling foreign BTR capital into modular projects | China | Government-backed affordable rental housing requiring faster delivery formats |

Asia Pacific is the fastest-growing manufactured housing region, led by Japan's mature prefabricated housing industry where companies including Sekisui House and Daiwa House produce approximately 150,000 factory-built homes annually for domestic buyers who value the quality consistency and fast installation of prefabricated formats. India's Pradhan Mantri Awas Yojana urban mission, which targets 10 million housing units under government procurement, is creating a direct channel for factory-built construction that reduces timeline pressure on contractors in markets where site-based labour coordination is complex. Australia's build-to-rent sector, supported by the Treasury's FIRB withholding tax reform, is incorporating modular construction into rental community development pipelines in Sydney and Melbourne to shorten construction cycles for institutional operators with capital deployment timelines.