By District · By Property Format · By Tenant Profile · By Operator

Shanghai's institutionally managed rental housing sector recorded 14 en-bloc transactions at a total value of RMB 7.2 billion in 2023, up 18% year-on-year, and maintained occupancy of 89% to 90% through early 2025 per China Real Estate Index System data, yet the broader Shanghai rental market experienced a 12% rent decline in 2025 as 618,000 individually-owned units flooded 55 Chinese cities simultaneously creating a bifurcated market where the 90% of institutional stock in Pudong, Minhang, and premium Inner Ring Road buildings performs independently of the price war among 580,000 fragmented individual landlords competing for the same working-class and white-collar tenant pool.

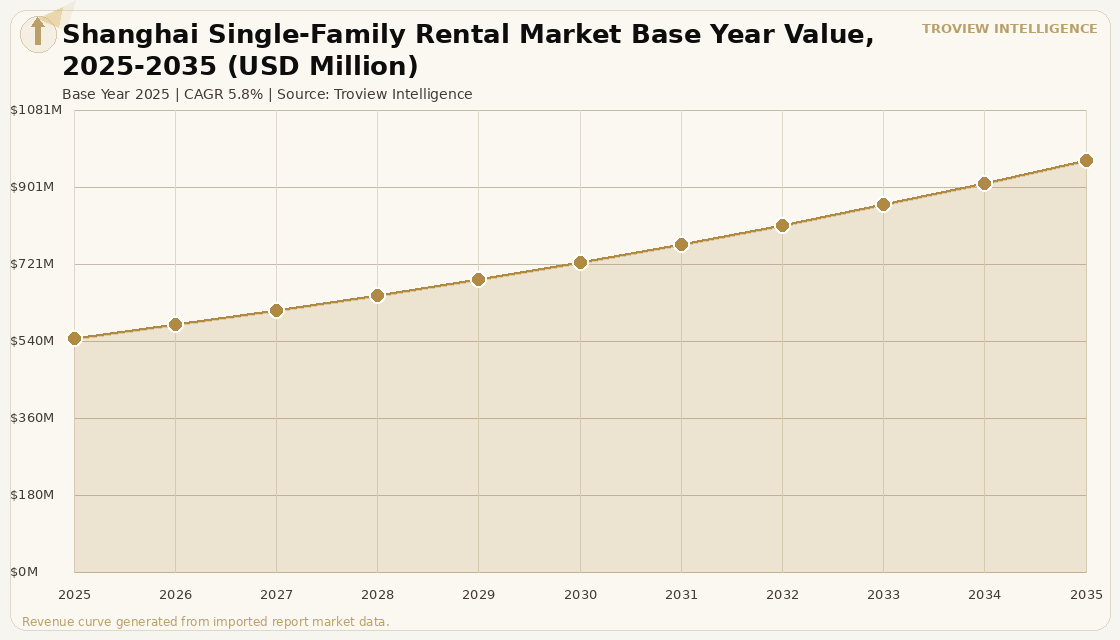

MARKET SYNOPSIS

The Shanghai single-family rental market size was USD 548.6 Million in 2025 and is expected to register a revenue CAGR of 5.8% during the forecast period, reaching USD 965.0 Million by 2035. Market revenue growth is supported by the structural demand for professionally managed rental housing from the white-collar, expatriate, and senior professional tenant cohorts concentrated in Shanghai's Inner Ring Road districts and suburban villa corridors, where institutional operators including Ziroom, Longfor Guan Yu, and foreign co-investment platforms maintain occupancy of approximately 89% to 90% even as the broader market experiences oversupply pressure from unsold residential inventory converting to rental listings. Shanghai recorded 14 en-bloc institutional rental housing transactions with a total transaction volume of RMB 7.2 billion in 2023, up 18% year-on-year per China Real Estate Index System data, establishing the city as the primary destination for institutional capital entering China's rental housing sector through direct property acquisition. The institutionally managed rental housing supply in Shanghai is set to evolve significantly by 2030, with Pudong District, Minhang District, and Qingpu District projected to collectively represent 58% of the city's total rental housing stock per the Shanghai institutional supply pipeline data, while 64.7% of future units are concentrated outside the Outer Ring Road, reflecting the land economics that concentrate new institutional supply in suburban corridors served by the expanded Shanghai Metro network. New-home prices in Shanghai continued to rise year-on-year in core locations as of April 2026 per the China Real Estate Index System's 100-city price survey, distinguishing Shanghai from the national downward price trend and confirming the structural homeownership affordability gap that sustains rental demand among the city's large non-hukou resident population.

Shanghai's rental housing market is shaped by a tenant base far more diverse than any other Chinese city. The city's 25 million population includes a large expatriate community requiring premium serviced and unfurnished rental formats in districts including Jing'an, Xuhui, Pudong Lujiazui, and Changning-Gubei; a domestic professional workforce employed in Shanghai's finance, technology, consulting, and trading sectors that generates demand for mid-to-premium apartment formats near metro connectivity; and a migrant working population that provides occupancy depth in suburban and industrial corridor rental stock. The Ziroom platform, which specialises in branded, renovated apartments with standardised furnishing and digital lease management, and the Beike platform, which aggregates individual landlord listings alongside institutional inventory, together represent the two dominant digital access points for Shanghai rental searches per rental platform market data. Shanghai's institutional rental housing attracted strong interest from families with children and mid-to-senior professionals from state-owned enterprises transitioning from build-to-sell properties to long-term rental formats, generating net absorption of 51,000 units in 2023, the highest on record per China Real Estate Index System research. For instance, in 2023, a record RMB 7.2 billion of en-bloc institutional rental housing transactions were completed in Shanghai, including foreign institutional capital entering through joint venture structures with Chinese state-owned operators who provide land access, regulatory relationships, and local market management capability, per Invesco's institutional rental housing market analysis of April 2025. These are some of the key factors driving revenue growth of the market.

However, the Shanghai single-family rental market faces structural constraints that moderate revenue growth across both the institutional and fragmented segments. China Real Estate Information Corp. data published by Caixin Global in August 2025 confirmed that individually-owned rental listings in 55 major Chinese cities including Shanghai reached 618,000 units in July 2025, with Shanghai experiencing a 12% rent decline as unsold residential inventory, investor-held properties, and units vacated by residents who left Shanghai during population rebalancing entered the rental supply simultaneously. The oversupply dynamic is concentrated in the segment below RMB 6,000 per month, where individually-owned properties compete directly for price-sensitive professional and migrant tenants, while premium institutional stock above RMB 10,000 per month maintains occupancy through differentiated product quality and service. China's residential new starts fell 19.8% year-on-year to 429.84 million square metres in 2025 per China's National Bureau of Statistics, and S&P Global Ratings forecasts primary property sales to decline a further 10-14% in 2026, maintaining the pipeline pressure on developers to convert unsold inventory to rental that has depressed market-wide Shanghai rents. The requirement to register residency with police within 24 hours of moving into a new rental property under Shanghai's hukou system creates friction for high-mobility professional renters who change residences frequently and are the most commercially attractive tenant segment for institutional operators. These factors substantially limit Shanghai single-family rental market growth over the forecast period.

Shanghai's rental market in 2025 is the most instructive case study for the institutional versus fragmented landlord bifurcation in any Asian market. The 90% institutional occupancy number and the 12% overall rent decline are not contradictory they are describing two completely different markets occupying the same city. Institutional operators in premium Jing'an and Xuhui buildings with amenity packages, digital management, and responsive maintenance teams are running at capacity with waiting lists. The 618,000 individual listings on Beike at 31 yuan per square metre per month are competing in a price war that the institutions have deliberately exited by charging 3 to 4 times that rate for a completely different product. The risk for institutional investors is not the rent decline they are largely insulated from it. The risk is that the 2030 pipeline of new suburban institutional supply in Pudong and Minhang delivers into a market where the institutional premium only holds in locations with Inner Ring Road proximity and metro connectivity." Troview Intelligence Senior Analyst, Shanghai Rental Housing Markets

SEGMENT INSIGHTS

By Property Format

Centralised branded apartment communities in premium Inner Ring Road locations are expected to account for a significantly large revenue share in the Shanghai single-family rental market during the forecast period.

Based on property format, the Shanghai single-family rental market is segmented into centralised branded apartment communities, detached villa and townhouse rental in suburban corridors, distributed scattered-site managed apartments, serviced and furnished apartment formats, and historic lane house rentals in premium inner-city districts. Centralised branded apartment communities dominate institutional revenue, maintaining 89% to 90% occupancy per China Real Estate Index System data, and generating the operational efficiency and tenant service quality that differentiates institutional product from individually-owned stock. Detached villa and townhouse rental in suburban corridors including Pudong-Jinqiao, Minhang-Hongqiao, and the Qingpu-Xinzhuang corridor is the fastest-growing segment by unit delivery, as Pudong District, Minhang District, and Qingpu District together represent 58% of Shanghai's future rental housing supply pipeline and will deliver large-format suburban communities at price points accessible to senior Chinese and expatriate families requiring school district proximity and private outdoor space.

By District

Jing'an, Xuhui, and Pudong Lujiazui premium districts are expected to account for a significantly large revenue share in the Shanghai institutional rental market during the forecast period.

Based on district, the Shanghai single-family rental market is segmented into Jing'an and the commercial CBD core, Xuhui and the French Concession, Pudong Lujiazui and financial district, Changning-Gubei as the primary expatriate hub, outer districts including Minhang, Qingpu, and Jiading, and Pudong suburban and international school corridor. The Jing'an district commands the highest rents in Shanghai as the commercial heart of the city, offering modern high-rises, luxury retail, and short metro commutes, attracting the professional tenant segment that accepts premium rent in exchange for location quality. The Changning-Gubei area is a long-established expatriate hub particularly for Japanese and Korean corporate assignee communities, with family-friendly infrastructure, international schools, and proximity to Hongqiao airport and transport hub. The outer districts including Pudong-Jinqiao international residential corridor, Minhang's Hongqiao villa zone, and Qingpu attract families requiring detached house formats near international schools, generating above-market rents that offset the suburban location discount.

By Tenant Profile

White-collar domestic professionals and expatriate corporate assignees are expected to account for a significantly large revenue share in the Shanghai institutional rental market during the forecast period.

Based on tenant profile, the Shanghai single-family rental market is segmented into domestic white-collar professionals, expatriate corporate assignees and foreign professionals, state-owned enterprise mid-to-senior management, students and graduate professionals, and migrant workers in peripheral districts. White-collar domestic professionals dominate the institutional rental base, attracted by the upgraded product quality and digital service platforms of branded operators including Ziroom and state-backed institutional landlords. Families with children and mid-to-senior-level professionals from state-owned enterprises represent the fastest-growing tenant category in Shanghai's institutional rental sector, transitioning from the homeownership market as prices remain unaffordable and pursuing long-term rental commitments of two or more years in well-managed communities near international and public school districts. Institutional operators in Shanghai reported in 2023 that this mid-to-senior professional and family cohort was driving the record net absorption of 51,000 units per China Real Estate Index System research, a multiple of the 21,000 units absorbed in 2022, confirming that the institutional rental product is attracting a tenant base that was previously committed to homeownership.

District Deep-Dives

JING'AN / COMMERCIAL CBD CORE HIGHEST RENTS IN THE CITY

| Character | Commercial heart, luxury high-rises, finance and consulting tenants | Metro Access | Multiple lines, highest connectivity in Shanghai |

| Rent Level | Highest in Shanghai, institutional premium fully sustainable | Key Platforms | Ziroom branded apartments, Beike institutional listings |

Jing'an is Shanghai's commercial hub and the district commanding the highest rents in the city's institutional rental market, attracting finance, consulting, and technology sector professionals who require proximity to Shanghai's central office district and acceptance of a significant rental premium for location quality and metro accessibility. Branded institutional apartment operators including Ziroom offer renovated units with standardised digital smart lock systems, managed maintenance, and flexible lease structures in Jing'an that command rents at a substantial premium to the surrounding scatter-site market, sustaining the institutional premium that generates the 4.5% to 5.5% stabilised yield on cost targeted by investors. The district's low vacancy rate in institutional stock reflects both genuine tenant demand and the severe constraint on Inner Ring Road new supply, with future rental housing supply inside the Inner Ring Road representing only 1.5% of Shanghai's total pipeline per the supply forecast data, meaning that existing well-located institutional stock in Jing'an faces minimal new competition through the forecast period. Senior professionals from financial institutions including HSBC, JPMorgan, and domestic securities firms headquartered in the nearby Lujiazui and Nanjing West Road clusters provide the primary tenant base for premium Jing'an institutional rentals.

XUHUI / FRENCH CONCESSION HERITAGE PREMIUM AND CREATIVE SECTOR

| Character | Tree-lined lane houses, creative industry hub, expat residential | Building Stock | Mix of historic lane houses and modern apartments |

| Tenant Base | Creative professionals, media, tech, legal, expatriates | Differentiation | Historic charm premium over modern high-rise alternatives |

Xuhui and the French Concession area offer Shanghai's most distinctive residential rental environment, combining historic tree-lined streets, Art Deco and Republican-era lane house architecture, and proximity to the Xujiahui commercial hub and the West Bund arts and cultural district that has emerged as one of Asia's most significant contemporary arts concentrations. The district attracts creative industry professionals, media executives, technology company designers, and expatriates who value the neighbourhood character and walkable environment over the generic high-rise format of central CBD locations, generating a stable tenant base that accepts above-market rents for authentically characterful accommodation. Older lane house buildings in the French Concession have variable insulation and plumbing quality that creates management complexity for institutional operators, but purpose-renovated boutique properties that have been professionally upgraded while retaining historic facades command strong premiums from the expatriate and creative professional segment. West Bund Central, one of the new commercial projects entering Shanghai's market in Q4 2025 per commercial real estate data, is generating additional professional tenant demand in the southern Xuhui waterfront area that will sustain premium residential rental demand in adjacent residential pockets.

| Character | Slick modern apartments, finance worker concentration | Proximity | Shanghai Stock Exchange, bank HQs, international firms |

| Pudong Share of Future Supply | Part of 58% Pudong-Minhang-Qingpu pipeline | Institutional Presence | High; en-bloc transactions concentrated in Pudong |

Pudong Lujiazui is the district of choice for finance sector professionals employed in the Shanghai Stock Exchange, China's major state-owned bank headquarters, international investment banks, and the asset management firms that have concentrated in the IFC Shanghai, Shanghai Tower, and Jin Mao Tower complex. The institutional rental housing supply in Pudong is concentrated along the Lujiazui core and expanding outward into the Jinqiao international residential corridor where detached villa formats serve senior executive families requiring international school proximity and private outdoor space that the Lujiazui high-rise rental format cannot provide. Pudong will represent a substantial share of Shanghai's future rental housing supply pipeline, with the district part of the Pudong-Minhang-Qingpu cluster that will collectively account for 58% of Shanghai's total institutional rental stock by end-2025, meaning the district will receive the largest volume of new institutional supply over the forecast period and must sustain occupancy through a significant increase in available units. The KAFD metro station in Lujiazui, part of the Shanghai Metro expansion delivering multiple new lines through 2025 and 2026, is improving connectivity between Pudong financial district rental housing and western Shanghai employment nodes, expanding the viable catchment for Pudong rental units beyond the immediate Lujiazui employment cluster.

CHANGNING-GUBEI / EXPATRIATE CORRIDOR PRIMARY INTERNATIONAL COMMUNITY HUB

| Character | Japanese, Korean, and Western corporate assignee families | Schools | Multiple international schools, proximity driver |

| Proximity | Hongqiao airport and transport hub, 20-min to Puxi CBD | Property Format | Villas, serviced apartments, low-rise compounds |

Changning and the Gubei international residential area form Shanghai's primary corporate assignee and expatriate family rental corridor, established over several decades as the location of choice for Japanese, Korean, Taiwanese, and Western multinational employees relocating to Shanghai with spouse and school-age children. The district's family-friendly infrastructure including the French, German, Japanese, and multiple international school campuses, proximity to Hongqiao airport for frequent business travellers, and the established community infrastructure of international supermarkets, restaurants, and healthcare providers create a self-reinforcing residential ecosystem that sustains premium rents independent of the broader Shanghai rental market dynamics. Rental formats in Gubei range from large-format detached houses in gated compounds to low-rise apartment buildings with concierge services, all positioned at premium price points relative to equivalent square metres in Jing'an or Pudong. The corporate assignee tenant base, whose rents are typically paid by multinational employer housing allowance packages at rates significantly above individual market capacity, provides the highest per-unit rental revenue in Shanghai's rental market and supports the most stable occupancy trajectory among all Shanghai institutional rental segments.