| TROVIEW INTELLIGENCE | Carrier-Neutral Data Centre Market | Q2 2026 |

By Geography - By Service Type - By Facility Size - By End-User Industry

The global carrier-neutral data centre market reached USD 42.8 billion in 2024, as Equinix exceeded 500,000 global interconnections in 2025, Brookfield Asset Management committed EUR 30 billion to Data4-led AI data centre infrastructure in France at the February 2025 Paris AI Action Summit subsequently raised from EUR 20 billion with EUR 15 billion directed to carrier-neutral hyperscale campuses capable of tripling Data4's French capacity to 1.5 gigawatts by 2030, and Mistral AI deployed 18,000 NVIDIA Grace Blackwell Superchips across a 40 megawatt carrier-neutral facility in Essonne, France, as European sovereign AI ambitions concentrate hyperscale demand in carrier-neutral facilities that provide the multi-cloud and multi-carrier interconnection architectures that self-built hyperscale campuses cannot replicate.

MARKET SYNOPSIS

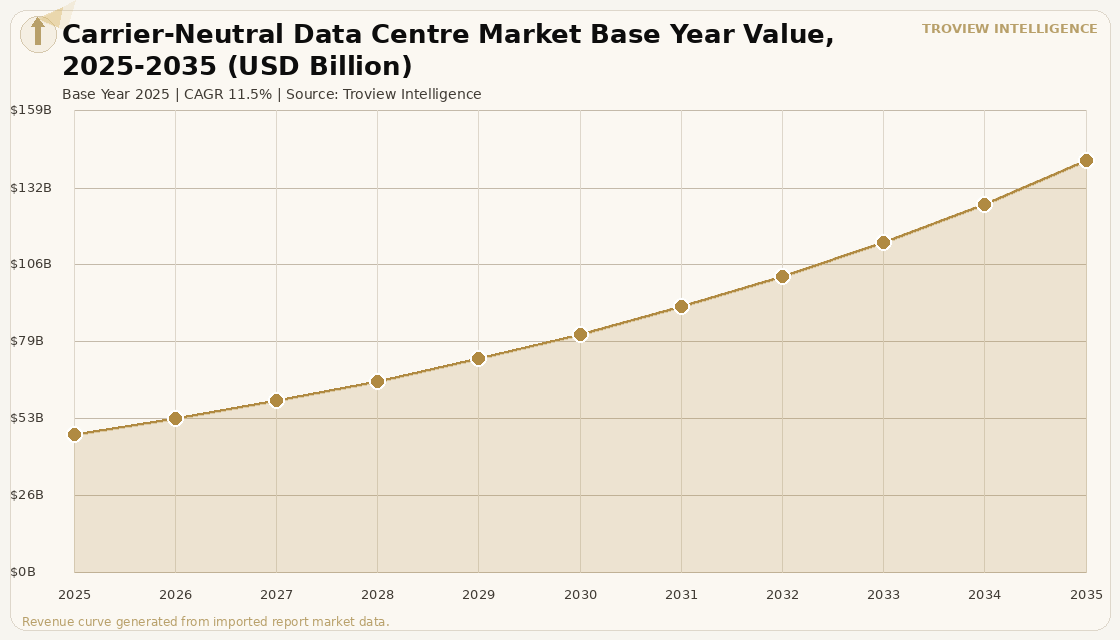

The global carrier-neutral data centre market size was USD 47.62 Billion in 2025 and is expected to register a revenue CAGR of 11.5% during the forecast period, reaching USD 141.83 Billion by 2035. The carrier-neutral model where data centres provide co-location infrastructure accessible to multiple network carriers, cloud providers, and internet service providers without favouring any single operator generates revenue through rack licensing, cross-connect fees, power billing, and managed services across multi-tenant facilities that serve the hybrid cloud strategies of enterprise, financial services, media, and government customers. Market revenue growth is supported by the accelerating multi-cloud adoption among global enterprises that require physical carrier-neutral interconnection points to distribute workloads across Amazon Web Services, Microsoft Azure, Google Cloud, and Oracle simultaneously, the expansion of AI inference demand that requires carrier-neutral facilities with dense fibre ecosystems and cloud-on-ramp connectivity to serve latency-sensitive workloads, and the structural scarcity of power-connected, carrier-neutral sites in established markets that creates pricing power for incumbent operators. For instance, in February 2025, Equinix, United States, opened a new Paris facility adding 20 megawatts of IT load and extending the vendor's metropolitan interconnection fabric to ten Paris data centres hosting more than 160 network service providers and over 100 cloud service providers, confirmed by Equinix investor disclosure and per Equinix investor disclosure and verified market data. These are some of the key factors driving revenue growth of the market.

North America dominated the carrier-neutral data centre market in 2025 with approximately 40% revenue share, anchored by Equinix's more than 144,000 cabinets globally and the dense interconnection ecosystems of its Ashburn, New York, Silicon Valley, and Chicago facilities that host the majority of North American financial services and cloud provider cross-connect demand. Europe is the second-largest regional market, with carrier-neutral data centres in London, Frankfurt, Amsterdam, and Paris collectively constituting the primary interconnection backbone of European digital infrastructure, with the European carrier-neutral co-location market valued at USD 12.4 billion in 2024 per verified industry data and projected to grow at a CAGR of 11.7% through 2033, outpacing the global average. Asia Pacific is the fastest-growing region, with India projected to register the highest country-level CAGR through 2033 as 5G densification, Global Capability Centre expansion, and sovereign cloud mandates drive enterprise demand for carrier-neutral facilities that provide multi-operator connectivity to domestic and international enterprise customers. The global carrier-neutral data centre market is projected to grow from USD 42.8 billion in 2024 at a CAGR of 11.3% through 2033, reaching USD 110.1 billion, with Europe recording a slightly faster CAGR of 11.7% reflecting its structural investment deficit relative to demand compared to the more mature North American market.

However, the global carrier-neutral data centre market faces structural constraints that temper the pace of expansion. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy cost inflation that raises operational expenditure for carrier-neutral data centre operators whose facilities consume electricity at scale across hundreds of co-located customers, creating margin pressure that is difficult to pass through to enterprise tenants on multi-year lease contracts with fixed or inflation-capped escalators. The structural shift of hyperscaler cloud providers toward self-built campus infrastructure with Microsoft's three self-built sites in northern France, Amazon's self-built French projects, and Google's campus expansions all representing demand that does not flow through carrier-neutral co-location facilities is limiting the addressable hyperscale revenue pool available to carrier-neutral operators and increasing dependence on enterprise and financial services demand for occupancy. Grid connection constraints in established European markets including Greater London, Frankfurt, and Amsterdam are creating supply delivery delays that restrict the pace at which carrier-neutral operators can add new interconnection-dense capacity, compressing available space and raising per-rack co-location prices but also reducing the operator's ability to serve new customer demand in constrained geographies. These factors substantially limit global carrier-neutral data centre market growth over the forecast period.

The carrier-neutral model is being stress-tested by two forces simultaneously. On the hyperscale side, the largest cloud providers are increasingly self-building campus infrastructure rather than paying carrier-neutral co-location premiums for space they can own outright. On the AI workload side, the inference and training infrastructure being deployed by Mistral AI, HuggingFace, and the emerging European sovereign AI ecosystem requires carrier-neutral multi-cloud interconnection that only Equinix and Digital Realty's PA-series in Paris can provide at the rack density now required. The net result is a market where the hyperscale wholesale segment of carrier-neutral revenue is under structural pressure while the AI-driven enterprise and sovereign cloud segment is growing faster than the market consensus projects. France is the clearest example of this bifurcation: Brookfield's EUR 30 billion commitment to Data4 is for hyperscale carrier-neutral campuses, while Equinix's ten-facility Paris presence is generating the cross-connect and cloud-on-ramp revenue that no self-built hyperscale campus can replicate. Both are growing. The question is which one grows faster." Troview Intelligence Head of Global Carrier-Neutral Data Centre Research

SEGMENT INSIGHTS

By Service Type

Colocation service type is expected to account for a significantly large revenue share in the global carrier-neutral data centre market during the forecast period.

Based on service type, the global carrier-neutral data centre market is segmented into colocation, interconnection, managed services, and others. Colocation dominates total revenue by providing the physical rack, cage, and suite space from which enterprises operate their own IT infrastructure within a shared carrier-neutral facility, with rental income from rack space, power billing, and cage licensing accounting for the majority of carrier-neutral co-location operator revenue globally. The interconnection segment comprising cross-connect fees, internet exchange port charges, and cloud exchange access fees generates the highest revenue per unit of physical space in carrier-neutral facilities, as cross-connect revenue at USD 30 to USD 300 per cross-connect per month on high-density interconnection campuses like Equinix's Paris PA series compounds significantly across the carrier, cloud, and enterprise ecosystems hosted within each facility. The managed services segment is expected to register the fastest revenue CAGR during the forecast period, driven by enterprise demand for remote hands, infrastructure monitoring, and managed network services that reduce in-facility operational staffing requirements.

By End-User Industry

Financial services and banking end-user industry is expected to account for a significantly large revenue share in the global carrier-neutral data centre market during the forecast period.

Based on end-user industry, the global carrier-neutral data centre market is segmented into banking, financial services and insurance, IT and telecommunications, media and content delivery, government and public sector, healthcare, and retail and e-commerce. Financial services dominates carrier-neutral co-location demand by revenue density, as investment banks, exchanges, trading firms, and asset managers require the sub-millisecond latency cross-connects to peer networks, market data feeds, and prime broker platforms that are exclusively available at carrier-neutral interconnection hubs including Equinix's LD4 in Slough, NY5 in Secaucus, TY3 in Tokyo, and PA3 in Paris. Government and public sector is the fastest-growing end-user segment in European carrier-neutral data centres, driven by France's Cloud au Centre strategy directing public sector IT toward SecNumCloud-qualified carrier-neutral facilities that meet ANSSI's French sovereignty requirements, and Germany's data localisation mandates requiring federal government workloads to remain within carrier-neutral facilities on German territory.

By Facility Size

Large-scale facility segment above 20 MW is expected to account for a significantly large revenue share in the global carrier-neutral data centre market during the forecast period.

Based on facility size, the global carrier-neutral data centre market is segmented into micro and edge facilities below 1 MW, retail co-location facilities from 1 to 10 MW, mid-scale campus facilities from 10 to 20 MW, and large-scale campus facilities above 20 MW. Large-scale facilities dominate total revenue by megawatt, as the economies of scale in power purchasing, cooling infrastructure, and security operations that make large-scale carrier-neutral campuses structurally more cost-competitive than smaller facilities have directed institutional capital toward campus-scale development since 2020. The mid-scale retail co-location segment from 1 to 10 megawatts is expected to register the fastest CAGR during the forecast period in emerging markets including India, Southeast Asia, and the Middle East, where carrier-neutral co-location demand from domestic enterprises and regional cloud provider deployments is growing faster than the large-campus hyperscale segment.

REGIONAL ANALYSIS

NORTH AMERICA LARGEST MARKET, EQUINIX DOMINATED, ~40% GLOBAL SHARE

| NA Revenue Share 2025 | Equinix Global Interconnections | Equinix 2025 Revenue | US Leased DC Power Share (DLR) |

| ~40% of global market | 500,000+ (first time exceeded) | USD 9.217 billion | 15% of total US leased DC power |

North America is the dominant carrier-neutral data centre market, anchored by Equinix's interconnection platform that exceeded 500,000 global cross-connects for the first time in 2025 and generated record annualized gross bookings of USD 1.6 billion representing a 27% year-on-year increase. Equinix's Ashburn, Virginia campus the world's highest-concentration internet exchange point hosts the majority of North American financial services, media, and cloud provider cross-connect demand, while its New York, Silicon Valley, Chicago, and Atlanta facilities collectively serve the enterprise and financial services segments that require physical proximity to peer networks and market data infrastructure. The US carrier-neutral market benefits from the most mature fibre ecosystem globally, with Zayo, Lumen Technologies, and Colt providing the dense dark fibre connectivity between carrier-neutral hubs that enables the multi-site redundancy architectures required by financial services and government clients operating under continuity obligations.

EUROPE SECOND

| Europe CN Colo Market 2024 | Europe CAGR 2025-2033 | France AI Pledges (Feb 2025) | Brookfield-Data4 Commitment |

| USD 12.4 billion | 11.7% (above global average) | EUR 109 billion total pledges | EUR 30 billion, 1.5 GW target |

Europe is the second-largest carrier-neutral data centre market, with London, Frankfurt, Amsterdam, and Paris constituting the FLAP-D interconnection corridor that hosts the majority of European enterprise, financial services, and cloud-provider co-location demand. France has emerged as Europe's most dynamic carrier-neutral investment market following the February 2025 Paris AI Action Summit at which EUR 109 billion in total AI infrastructure pledges were announced, including Brookfield Asset Management's commitment to invest EUR 30 billion through Data4 subsequently raised from the original EUR 20 billion with EUR 15 billion directed to new carrier-neutral hyperscale campuses designed to triple Data4's French capacity to 1.5 gigawatts by 2030 per Brookfield press release and Data Centre Dynamics reporting. Germany's data sovereignty regulations and the Dutch Hyperscale Data Centre Moratorium are creating structural demand for compliant carrier-neutral facilities across Europe that redirect investment toward France's more permissive planning environment and lower relative energy costs supported by EDF's nuclear power capacity.

ASIA PACIFIC

| APAC Revenue Share 2025 | Fastest Country CAGR | India GCC-Driven Demand | Japan CN Colo Operators |

| ~29% of global market | India (highest through 2033) | 40-45M sqft GCC expansion 2026 | AT TOKYO, Equinix, NTT, KDDI |

Asia Pacific is the fastest-growing carrier-neutral data centre region, with India recording the highest country-level CAGR driven by the expansion of Global Capability Centres requiring multi-operator connectivity in Bengaluru, Hyderabad, Pune, and Chennai, and by sovereign cloud mandates from the Indian government that require data residency within carrier-neutral facilities on Indian territory. Singapore maintains its position as the primary carrier-neutral interconnection hub for Southeast Asia, with Equinix's SG series and Digital Realty's facilities providing the multi-cloud connectivity fabric that multinational enterprises require for regional operations, while Singapore's restrictive data centre moratorium partially lifted in 2022 but still constraining new supply keeps carrier-neutral co-location pricing at premium levels. Japan's carrier-neutral market is led by AT TOKYO's Shibaura campus, which hosts the Tokyo Internet Exchange alongside 530 carriers and service providers, while Equinix's TY series and Telehouse KDDI's Docklands-equivalent campus in Tokyo provide the financial services and cloud-on-ramp interconnection that the Japanese banking and securities market requires.