| TROVIEW INTELLIGENCE | Cell Tower and Telecom Infrastructure Market | Q2 2026 |

| TROVIEW INTELLIGENCE · GLOBAL INTELLIGENCE REPORT |

By Geography · By Tower Type · By Ownership Model · By Tenant Technology

American Tower Corporation, one of the largest global REITs, operates a portfolio of nearly 150,000 communications sites and a highly interconnected footprint of US data center facilities as of 2025, with 5G network densification, broad-based midband upgrades, and accelerating AI-ready interconnection demand fuelling double-digit growth at its CoreSite data centre division in 2025, SBA Communications reporting a portfolio of more than 44,500 communications sites throughout the Americas and Africa with Brazil representing approximately 30% of total tower count and 13.3% to 13.5% of total site leasing revenue per SEC filings, China Tower Corporation completing 329,000 5G base stations in H1 2024 alone bringing its total to approximately 2.676 million stations across 2 million-plus towers globally, the global telecom tower market reaching USD 67.87 billion in 2025 per China Tower Corporation annual report and GSMA Mobile Economy 2025 with Asia Pacific commanding the largest regional market share, T-Mobile executing 2,800 tower lease amendments to add mid-band massive MIMO radios elevating median download speeds by up to 40% per T-Mobile corporate press release of November 2025, and the FCC approving final rules capping tower-siting reviews at 60 days for colocation and 90 days for new builds in September 2025 confirming that cell tower and telecom infrastructure is among the most structurally resilient and growth-anchored categories in the global real estate and infrastructure investment universe.

| Standard License: USD 7,500 | Enterprise License: USD 10,500 |

MARKET SYNOPSIS

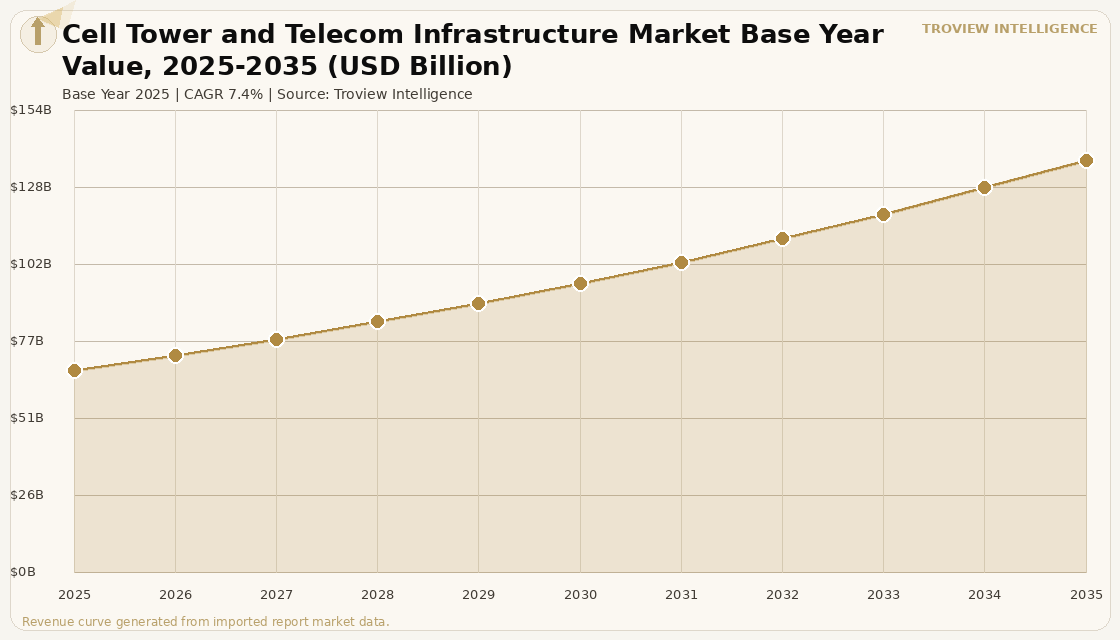

The global cell tower and telecom infrastructure market size was USD 67.42 Billion in 2025 and is expected to register a revenue CAGR of 7.4% during the forecast period, reaching USD 137.24 Billion by 2035. The 2025 market estimate is grounded in verified company revenues: American Tower Corporation operates a portfolio of nearly 150,000 communications sites as of 2025 per company disclosure, generating property revenues of approximately USD 1.9 billion in Q3 2025 alone per SEC 8-K filing and serving as one of the largest global REITs; SBA Communications Corporation holds a portfolio of more than 44,500 communications sites throughout the Americas and Africa per SEC 8-K filing, with Brazil representing approximately 30% of total tower count and 13.3% to 13.5% of total site leasing revenue per SBA Communications 10-Q filings of 2025; and Asia Pacific led the global market with 45% share in 2024 per China Tower Corporation H1 2024 earnings disclosure, with China Tower Corporation having completed 329,000 5G base stations in H1 2024 alone bringing its total to approximately 2.676 million 5G stations. The market encompasses the total revenue generated by tower infrastructure companies from site leasing, tower development services, colocation, and ancillary services for wireless carriers, broadband providers, government agencies, and private wireless network operators across all tower formats including lattice towers, monopoles, guyed towers, rooftop installations, and small cell distributed antenna systems. Market revenue growth is anchored in the structural certainty that 5G network deployment requires substantially greater tower site density than 4G, with the average number of towers required per 1,000 subscribers increasing 12% between 2021 and 2024 per market analysis, and urban 5G densification requiring macro tower colocation upgrades, small cell deployment, and rooftop installation programmes that generate sustained amendment, colocation, and new site revenue for tower operators. For instance, in November 2025, T-Mobile, United States, executed 2,800 tower lease amendments to add mid-band massive MIMO radios, elevating median download speeds by up to 40% in affected blocks per T-Mobile corporate press release of November 2025, illustrating the upgrade amendment activity that generates incremental revenue for tower operators from existing sites without requiring new tower construction. These are some of the key factors driving revenue growth of the market.

American Tower Corporation's CEO Steven Vondran stated in the Q2 2025 earnings release that demand for the company's high-quality global portfolio of telecommunications sites continued into the second quarter, with broad-based midband upgrades, accelerating densification activity, and growing demand for AI-ready interconnection solutions fuelling performance, and that the business entered H2 2025 with continued momentum and strategic clarity per American Tower Q2 2025 earnings disclosure. SBA Communications' 2025 Annual Report confirmed that the international business delivered solid new leasing activity results anchored by Brazil, where carrier customers continued to invest in advancing 5G coverage, with a younger demographic, increasing reliance on mobility, and upcoming spectrum auctions reinforcing the long-term opportunity in that market per SBA Communications 2025 Annual Report. The Brookfield-led consortium acquired American Tower Corporation's Indian tower business for approximately USD 2.2 billion (INR 18,200 crore) in September 2024, establishing Altius as the largest telecom tower portfolio in India, enabling American Tower to streamline operations and redeploy capital into strategic priorities in other regions per DBMR research. In December 2025, Crown Castle, United States, acquired 450 small-cell nodes including 80 miles of fiber rights-of-way in metropolitan Chicago, bolstering dense-urban service offerings per Crown Castle SEC 8-K filing of December 2025, while in January 2026, American Tower partnered with a renewable-energy developer to fit 1,200 Texas and California sites with solar-plus-battery systems by end-2027, targeting 40% renewable energy penetration across those states. These are some of the key factors driving revenue growth of the market.

However, the global cell tower and telecom infrastructure market faces structural constraints that temper the pace of new site development and REIT valuation appreciation across the forecast period. The elevated interest rate environment maintained by the Federal Reserve near 4.75% to 5.00% through 2025 has pushed American Tower's weighted average debt cost to 3.8%, up 90 basis points versus 2022, and Crown Castle's leverage reached 5.2 times EBITDA, nearing covenant ceilings that impede additional borrowing for acquisitions per American Tower Corporation 10-K 2024, with a 100-basis-point uptick in rates stripping 8% to 12% of portfolio net present value and creating bid-ask spread widening that stalled several scale transactions in 2025. Community resistance to new tower structures lengthens approval timelines by up to 18 months in some US municipalities, even as federal rules attempt to preempt excessive local control, with stringent design standards, health-impact debates, and zoning complexity disproportionately affecting dense urban zones where 5G site counts must multiply, softening near-term new-site growth momentum and driving operators toward pricier stealth or rooftop solutions. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, affect tower operator energy costs as diesel generator fuel consumption at off-grid tower sites representing the dominant fuel type at off-grid tower sites per GSMA Mobile Economy 2025 remains exposed to petroleum price movements, and the interconnection queue delays of up to 24 months in California and Texas for renewable energy tie-ins compound energy cost management challenges at scale. These factors substantially limit global cell tower and telecom infrastructure market growth over the forecast period.

Cell tower infrastructure is the only real estate asset class where the tenant a major wireless carrier literally cannot function without the asset. You cannot move a Verizon 5G base station from a tower to an office building. You cannot substitute a Crown Castle colocation site with cloud computing. The tower has to be there, in that location, at that height, with that line of sight, or the network does not work. That physical irreplaceability is the underwriting thesis for every institutional investor who has allocated to tower real estate since the first sale-leaseback transactions in the 1990s. What has changed in 2025 is not the irreplaceability. It is the complexity. 5G requires three to five times the tower site density of 4G for equivalent coverage. Every midband spectrum band that T-Mobile or AT&T acquires in an auction requires tower amendments across thousands of sites. Every massive MIMO radio installation is a lease amendment that generates incremental annual rent for American Tower or SBA Communications. The upgrade cycle does not end. The spectrum auctions do not stop. The data demand does not plateau. The tower infrastructure market is not a story about building new towers. It is a story about making existing towers more valuable by hanging more equipment on them, and that story has a very long runway." Troview Intelligence Head of Global Cell Tower and Telecom Infrastructure Research

SEGMENT INSIGHTS

Five Regions Defining Global Cell Tower and Telecom Infrastructure Revenue

ASIA PACIFIC 45% GLOBAL SHARE, CHINA TOWER 2M+ SITES, INDIA USD 16.1B RURAL PLAN

| APAC Global Market Share 2024 | China Tower 5G Stations | India Rural Connectivity | APAC CAGR Outlook |

| Largest region (GSMA 2025) | 2.676 million (H1 2024 cumulative) | USD 16.1 Billion plan (TRAI India Rural) | Fastest-growing region per GSMA Mobile Economy 2025 |

Asia Pacific is the world's largest cell tower and telecom infrastructure market by site count and by aggregate market share, with China Tower Corporation's 2 million-plus tower portfolio and 2.676 million 5G base stations (cumulative as of H1 2024 following 329,000 base station completions in the first six months of 2024 alone per China Tower Corporation H1 2024 earnings disclosure) representing the most concentrated single-country telecom tower infrastructure asset base in the world. India's Indus Towers, affiliated with Bharti Airtel, operates one of the largest tower portfolios in South Asia and has received government backing for USD 16.1 billion in rural connectivity programmes that will require substantial new tower builds in underserved rural areas per GSMA Mobile Economy 2025 and TRAI Annual Report 2024. The Asia Pacific telecom tower market is the world's largest by site count and is growing above the global average per GSMA Mobile Economy 2025, driven by the region's continuing 4G to 5G transition in markets including Japan, South Korea, Australia, and Thailand where regulatory spectrum auctions are triggering new infrastructure investment cycles alongside the continuing rural 4G rollout in India, Indonesia, and the Philippines.

| American Tower Sites | FCC Reform Sep 2025 | T-Mobile Nov 2025 | American Tower AEI |

| ~150,000 globally, ~41,000 in US (per ATC disclosures) | 60-day colocation, 90-day new build review caps | 2,800 lease amendments MIMO, +40% download speed | Jan 2026: 1,200 Texas/California solar-battery retrofits |

North America's cell tower infrastructure market is anchored by the three US-headquartered tower REITs American Tower, Crown Castle, and SBA Communications whose combined portfolio of US tower sites serves Verizon, AT&T, T-Mobile, Dish Network, and the growing field of private wireless network operators in the most revenue-intensive wireless infrastructure market globally. The FCC's September 2025 final rules capping tower-siting reviews at 60 days for colocation and 90 days for new builds, with automatic deemed-granted provisions, represent the most consequential federal telecommunications infrastructure reform in years, directly reducing the 18-month approval timeline delays that have slowed 5G densification in US urban markets per FCC rulemaking order of September 2025. T-Mobile's November 2025 execution of 2,800 tower lease amendments to add mid-band massive MIMO radios elevating median download speeds by up to 40% in affected blocks illustrates the amendment activity that generates incremental annual rent escalation for American Tower and SBA Communications tower portfolios, compounding the organic revenue growth from contractual escalators that typically run at 3% per year in US tower leases.

| Cellnex Acquisition 2024 | Vantage Towers | Telecom Tower Market | Orange 2G |

| Spain regional towerco 2,000+ towers added | 1,200 multifunction smart poles Germany/Spain/Poland | USD 30.07B in 2025 (Mordor, incl. EMEA-heavy weighting) | France deactivating 2G by end-2025 (tower upgrade trigger) |

Europe's cell tower infrastructure market is defined by the consolidation activity of Cellnex Telecom, headquartered in Spain, which expanded its European footprint in 2024 by acquiring a regional tower operator in Spain adding over 2,000 towers, demonstrating the continued trend of consolidation within mature European markets driven by 5G rollout pressures and the need for economies of scale in integrated network deployment per Verified Market Reports analysis. Vantage Towers, Germany, deployed over 1,200 multifunction smart poles across Germany, Spain, and Poland in 2023 to 2024, integrating 5G small cells, LED lighting, environmental sensors, and public Wi-Fi into unified urban infrastructure poles that address both connectivity and smart city requirements per cell site tower market research. France-based Orange announced plans to deactivate its 2G network by the end of 2025, triggering a cascade of equipment upgrades across the French tower estate as 3G, 4G, and 5G equipment replaces 2G radios on existing tower structures, generating colocation amendment revenue for tower companies managing the French carrier estate.

| Brazil Tower Count | SBA Brazil Share | Brazil 5G Status | Africa Driver |

| 72,212 towers (Q1 2024, Inside Towers Intelligence) | ~30% of SBA's total towers; 13.4% of site leasing revenue | Significantly lags 4G LTE coverage major build-out ahead | IHS Towers, Helios Towers Sub-Saharan greenfield |

Latin America's cell tower market, anchored by Brazil as the largest market in the region with 72,212 towers at Q1 2024 per Inside Towers Intelligence, is entering a structural growth phase driven by the 5G coverage buildout that significantly lags 4G LTE coverage across the country, with the economy improving and Anatel streamlining regulatory processes creating the conditions for MNOs to execute major new 5G infrastructure investment per Inside Towers Intelligence and SBA Communications 2025 Annual Report. SBA Communications held approximately 30% of its total tower portfolio in Brazil as of June 30, 2025, per SBA 10-Q filing, with Brazil site leasing representing 13.5% of total site leasing revenue for the period. Africa's tower infrastructure market is driven by IHS Towers and Helios Towers, which operate sub-Saharan African tower portfolios serving carriers across Nigeria, South Africa, Cameroon, and neighbouring markets, with greenfield tower construction continuing at pace in markets where 4G mobile broadband infrastructure is still being deployed.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from verified company SEC filings, earnings disclosures, FCC regulatory releases, and verified trade press.