| TROVIEW INTELLIGENCE | Cooling and Energy Infrastructure Real Estate Market | Q2 2026 |

| TROVIEW INTELLIGENCE · GLOBAL INTELLIGENCE REPORT |

The global data centre cooling market expanded from USD 18.4 billion in 2024 to USD 20.8 billion in 2025 per JLL Global Data Center Market Outlook 2026 and Vertiv Holdings 10-K 2024, while JLL's 2026 Global Data Center Market Outlook projects that the broader infrastructure investment supercycle will require up to USD 3 trillion by 2030 as global data centre capacity doubles from 100 GW to 200 GW, with AWS introducing its proprietary IRHX in-row heat exchanger co-designed with NVIDIA in July 2025 to cool GPU racks without facility modification, Schneider Electric acquiring a controlling stake in Motivair Corporation for approximately USD 850 million in October 2024 to lead the liquid cooling market, Vertiv Holdings leading the liquid cooling market with over 11.3% market share in 2025, and Modine Manufacturing securing approximately USD 180 million in orders through its Airedale cooling business from a leading AI infrastructure developer in February 2025 confirming that the transition from air to liquid cooling is no longer a future investment thesis but a present capital deployment reality across hyperscale, colocation, and enterprise data centre real estate globally.

| Standard License: USD 7,500 | Enterprise License: USD 10,500 |

MARKET SYNOPSIS

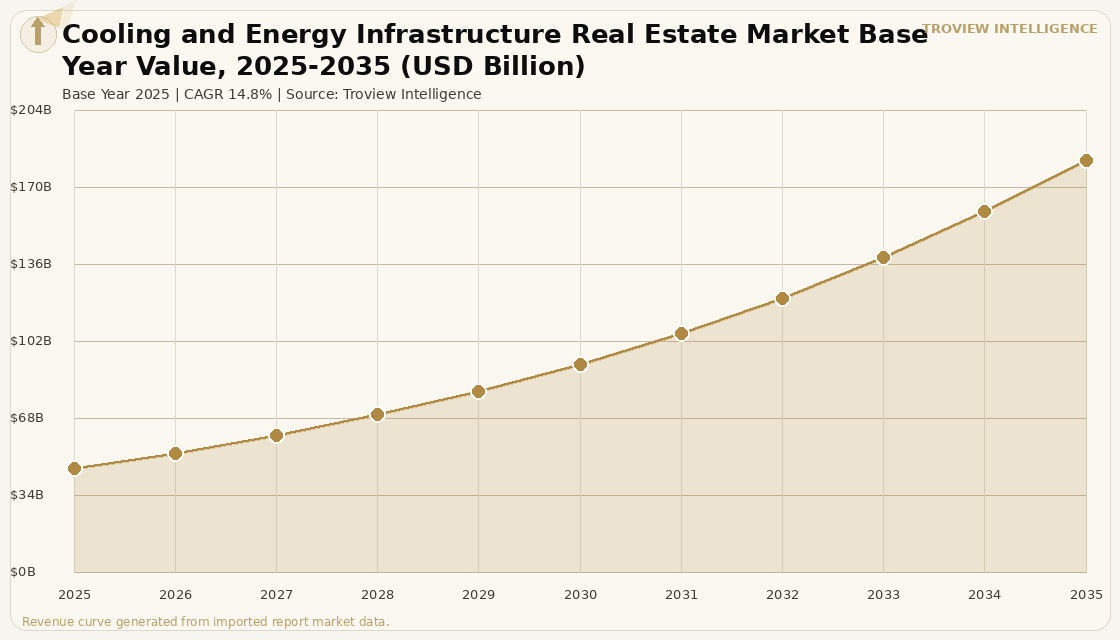

The global cooling and energy infrastructure real estate market size was USD 46.17 Billion in 2025 and is expected to register a revenue CAGR of 14.8% during the forecast period, reaching USD 182.34 Billion by 2035. The market encompasses the capital investment in cooling systems, power distribution infrastructure, uninterruptible power supply installations, battery energy storage systems, on-site generation and backup power assets, and renewable energy procurement infrastructure that is embedded within or directly serves data centre real estate assets. Market revenue growth is supported by the structural obsolescence of air-cooled data centre infrastructure in the face of AI compute demand: JLL's 2026 Data Center Market Outlook documents that global data centre capacity must expand by 97 GW between 2025 and 2030, with the majority of new capacity built to accommodate AI GPU clusters operating at 30 kW to 100 kW per rack a power density that air-cooling systems physically cannot manage without facility redesign, driving a mandatory transition to liquid cooling that generates cooling infrastructure investment independent of real estate development decisions. The global data centre cooling market reached USD 20.8 billion in 2025, growing from USD 18.4 billion in 2024 per JLL Global Data Center Market Outlook 2026 and Vertiv Holdings SEC 10-K 2024, with liquid cooling specifically comprising direct-to-chip, cold plate, and immersion cooling technologies representing the fastest-growing sub-segment as the GPU-intensive workload transition accelerates. For instance, in October 2024, Schneider Electric SE, France, agreed to pay approximately USD 850 million for a controlling stake in Motivair Corporation, United States, a specialist in liquid cooling for high-performance computing, acquiring the company's direct-to-chip cooling product lines, customer relationships with AI infrastructure developers, and manufacturing capability to position itself as the global leader in data centre liquid cooling infrastructure supply per Schneider Electric company announcement of October 2024. These are some of the key factors driving revenue growth of the market.

Vertiv Holdings Co., United States, led the data centre liquid cooling market with over 11.3% market share in 2025, with the top five players in the liquid cooling market Schneider Electric, Vertiv, Rittal, Stulz, and Boyd collectively holding approximately 35% of market share in 2025 per GMI analysis, reflecting the concentrated supplier landscape for mission-critical power and cooling infrastructure. In February 2025, Modine Manufacturing Company, United States, secured approximately USD 180 million in orders through its Airedale cooling business from a leading AI infrastructure developer for high-efficiency cooling systems designed for next-generation AI data halls per Modine company announcement of February 2025, illustrating the scale of individual procurement contracts being placed for AI-ready liquid cooling infrastructure. In July 2025, Amazon Web Services, United States, introduced its proprietary IRHX in-row heat exchanger co-designed with NVIDIA, United States, enabling cooling of GPU racks within standard rack footprints without major facility modification, a product that directly addresses the retrofit challenge facing the majority of existing data centre real estate globally per verified trade press of July 2025. Boston Consulting Group estimated that hyperscalers will need to invest approximately USD 1.8 trillion between 2024 and 2030 to meet AI and cloud demand, with cooling and energy infrastructure representing the single largest proportion of that investment above the cost of IT equipment itself. These are some of the key factors driving revenue growth of the market.

However, the global cooling and energy infrastructure real estate market faces structural constraints that limit the pace and geographic distribution of investment through the forecast period. Power grid capacity is the binding constraint in the most active data centre development markets, with utility interconnection timelines of three to five years in Northern Virginia and equivalent delays in Singapore, Amsterdam, and Frankfurt creating revenue recognition gaps between infrastructure investment commitments and operational cash flow generation that strain developer and operator balance sheets. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis affecting approximately 20% of global seaborne LNG, create upward pressure on data centre power costs across LNG-dependent electricity markets including Japan, Singapore, South Korea, and parts of Western Europe, increasing the operating cost component of energy infrastructure investment and reducing the net return on power purchase agreement structures that have anchored cooling and energy infrastructure financing in Asia Pacific. The specialist construction and commissioning workforce required for liquid cooling retrofits mechanical engineers, thermal management specialists, and coolant distribution unit commissioning technicians remains critically scarce globally, with lead times for liquid cooling system installations reaching 12 to 18 months across primary data centre markets and constraining the rate at which existing air-cooled data centre real estate can be upgraded to AI-ready liquid cooling specifications. High upfront capital requirements for liquid cooling approximately 40% to 60% above the cost of equivalent air-cooled installations per industry analysis slow retrofit adoption among operators with constrained capital budgets. These factors substantially limit global cooling and energy infrastructure real estate market growth over the forecast period.

Cooling and energy infrastructure has historically been treated as an operating expense embedded in data centre development costs. The AI supercycle has converted it into a strategic asset class in its own right. When AWS co-designs a proprietary in-row heat exchanger with NVIDIA, it is not optimising its energy bill. It is building a moat: a cooling system engineered specifically for Blackwell GPU architecture that competitors operating on standard liquid cooling infrastructure cannot match on density or operational efficiency. When Schneider Electric pays USD 850 million for Motivair, it is acquiring not a cooling manufacturer but a seat at the table in every hyperscale AI data hall procurement decision for the next decade. The investment thesis for cooling and energy infrastructure real estate is no longer derivative of data centre real estate investment. For the first time, it is leading it. The operator who controls the power contract, the cooling specification, and the grid interconnection agreement controls the data centre. The building is secondary." Troview Intelligence Head of Global Cooling and Energy Infrastructure Research

SEGMENT INSIGHTS

Four Regions Defining Global Cooling and Energy Infrastructure Investment

| US Liquid Cooling 2025 | US Liquid Cooling 2035 | AWS IRHX | Grid Constraint |

| USD 1.30 Billion (Vertiv/JLL DCMO 2026) | USD 7.33 Billion (18.88% CAGR) | Co-designed with NVIDIA, launched Jul 2025 | 3-5 year interconnection queue, primary markets |

North America is the largest market for cooling and energy infrastructure real estate investment globally, driven by the concentration of hyperscale AI development in Northern Virginia, Dallas, Atlanta, Chicago, and Phoenix where GPU cluster deployments are generating unprecedented per-facility cooling and power infrastructure requirements. The US data centre liquid cooling market reached USD 1.30 billion in 2025 and is projected to reach USD 7.33 billion by 2035 at an 18.88% CAGR per Vertiv Holdings 10-K 2024 and JLL Global Data Center Market Outlook 2026, with North America holding the largest regional share of global liquid cooling investment due to early adoption of direct-to-chip technology by Amazon Web Services, Microsoft Azure, and Google Cloud in their US hyperscale campuses. In July 2025, AWS introduced its proprietary IRHX in-row heat exchanger co-designed with NVIDIA, engineered to cool GPU racks within standard rack footprints without major facility modification, enabling smooth scaling of AI workloads in both new build and legacy data centre environments per verified trade press of July 2025. Macquarie Asset Management committed USD 17 billion to Applied Digital and Aligned Data Centers in 2025, signalling the scale of infrastructure fund capital targeting AI-ready power and cooling platform investments in North America per Westpac IQ analysis of November 2025.

| Europe Colo Cooling | PUE Standard | Schneider-Motivair | Key Constraint |

| USD 9.45B total colo investment; cooling dominant | EU Energy Efficiency Directive 1.3 target | USD 850M acquisition, Dec 2024 Paris HQ | Amsterdam moratorium; Frankfurt grid capacity |

Europe's cooling and energy infrastructure real estate market is characterised by the strictest regulatory framework for data centre energy efficiency of any major region, with the EU Energy Efficiency Directive establishing energy efficiency targets for large data centres and national authorities in Germany, the Netherlands, Ireland, and the United Kingdom applying PUE thresholds and renewable energy sourcing requirements that drive investment in advanced cooling infrastructure beyond the specifications required by market economics alone. Schneider Electric SE, France, whose acquisition of Motivair Corporation for approximately USD 850 million in October 2024 created the global leader in AI-ready liquid cooling infrastructure, is also the primary supplier of cooling and power distribution infrastructure to the European FLAP-D data centre cluster in Frankfurt, London, Amsterdam, Paris, and Dublin per company product portfolio documentation. In December 2024, Schneider Electric partnered with NVIDIA, United States, to roll out AI-ready data centre reference architectures supporting high-density liquid cooling at the rack level, with the collaboration extending sustainable infrastructure solutions to hyperscale clients across the European data centre market per Schneider Electric company announcement of December 2024.

| APAC Liquid Cooling CAGR | Singapore PUE Mandate | NTT Development | Key Driver |

| Fastest-growing sub-region (GMI 2025) | 1.25 at full load (DC-CFA2, Dec 2025) | India and Indonesia: direct-to-chip, immersion | Sovereign AI mandates, hyperscale PPA demand |

Asia Pacific is the fastest-growing region for cooling and energy infrastructure real estate investment, driven by sovereign AI infrastructure mandates in Japan, Australia, Singapore, and India that require new data centre developments to meet the most stringent cooling efficiency standards of any regional market. Singapore's DC-CFA2 framework, launched December 2025 by the EDB and IMDA, mandates a PUE of 1.25 at full load and at least 50% green energy sourcing for all new approved data centre capacity requirements that can only be met through liquid cooling systems operating in combination with renewable power purchase agreements, directly driving cooling and energy infrastructure investment in every new Singapore data centre project. NTT Global Data Centers, Japan, announced new large-scale developments in India and Indonesia in June 2025 featuring direct-to-chip and immersion cooling, extending hyperscale-grade cooling infrastructure specifications into markets where data centre construction standards had previously been set by air-cooled, lower-density enterprise facilities per NTT company announcements of June 2025. Australia's data centre market is expected to require approximately AUD 10 billion of additional grid investment to meet an extra 3.5 GW of power demand that the industry is forecast to require by 2035 per Moody's February 2025 analysis, a grid investment that is directly linked to cooling and energy infrastructure scaling across the Sydney, Melbourne, and Canberra data centre corridors.