| TROVIEW INTELLIGENCE | Cross-Border Real Estate Investment Market | Q2 2026 |

| TROVIEW INTELLIGENCE · GLOBAL INTELLIGENCE REPORT |

Global direct real estate transactions reached USD 216 billion in Q1 2026 rising 18% year-on-year per JLL Global Real Estate Trends and Perspectives of May 2026, cross-border investment finished up 37% year-on-year globally reaching USD 55 billion in Q1 2026 marking the strongest first-quarter performance since 2022, global direct transaction volume hit USD 185 billion in Q1 2025 up 34% year-on-year per JLL data, Tokyo alone attracted USD 11 billion in Q1 2025 to claim the world's top spot for property deals ahead of New York at USD 7.3 billion and Dallas-Fort Worth at USD 6.3 billion, Asia Pacific recorded the strongest Q1 2026 regional growth at 31% year-on-year with Japan leading liquidity and Singapore recording its highest quarterly volume on record, cross-regional inflows to Asia Pacific surged 221% year-on-year in H2 2024 to USD 6.3 billion per CBRE H2 2024 Global Real Estate Capital Flows analysis, Blackstone acquired Tokyo Garden Terrace Kioicho for approximately JPY 400 billion in February 2025 representing one of the largest-ever property deals by a foreign investor in Japan per Japan Direct Investment Company analysis, and all five largest real estate services firms CBRE, JLL, Cushman and Wakefield, Colliers, and Newmark upgraded their financial outlooks for 2025 following a strong second quarter performance marking the first time since the pandemic that all five raised expectations in the same quarter per CoStar reporting confirming that global cross-border real estate investment is in the most broadly based capital markets recovery since 2021.

| Standard License: USD 7,500 | Enterprise License: USD 10,500 |

MARKET SYNOPSIS

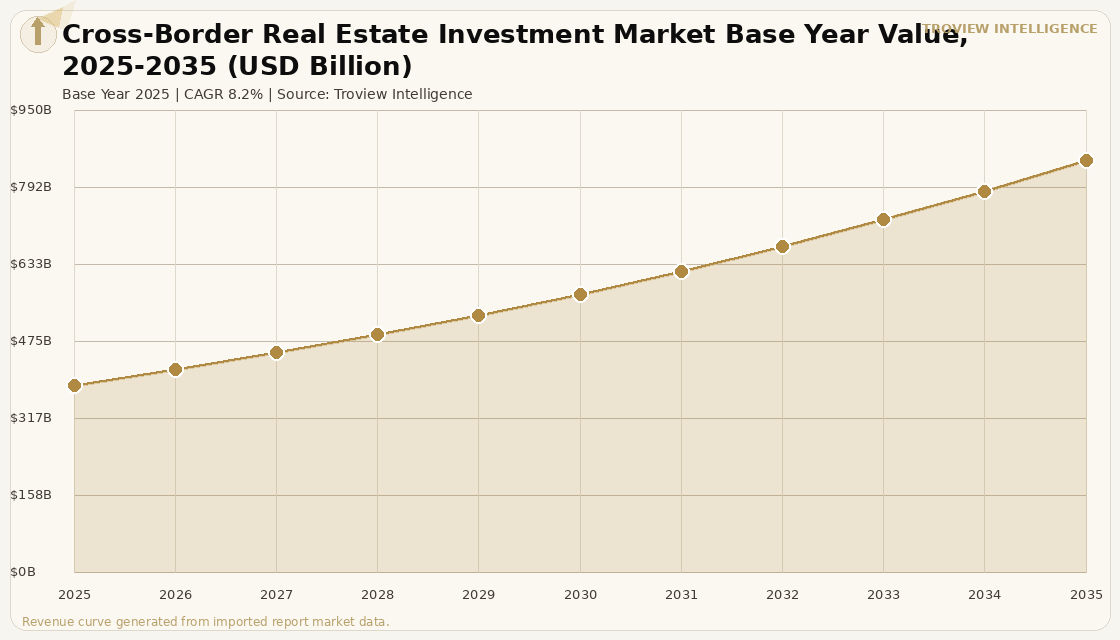

The global cross-border real estate investment market size was USD 386.42 Billion in 2025 and is expected to register a revenue CAGR of 8.2% during the forecast period, reaching USD 848.16 Billion by 2035. The 2025 market estimate is grounded in verified transaction data: global direct real estate transaction volume reached USD 185 billion in Q1 2025 up 34% year-on-year per JLL data cited in Tokyo Portfolio analysis; JLL's Global Real Estate Trends and Perspectives of May 2026 confirmed that global direct transactions reached USD 216 billion in Q1 2026 rising 18% year-on-year; and cross-border investment reached USD 55 billion in Q1 2026 alone, up 37% year-on-year, marking the strongest first-quarter cross-border performance since 2022 per JLL. The market encompasses the total annual volume of direct commercial real estate investment transactions in which the investor acquires assets in a country or region different from their domicile, including cross-regional portfolio acquisitions, single-asset trophy purchases, joint venture and club deal structures, and cross-border REIT and institutional real estate fund investments across all commercial property sectors. Market revenue growth is anchored in the progressive normalisation of global monetary policy following the 2022 to 2024 interest rate tightening cycle, with CBRE forecasting cross-border capital flows to further increase in 2025 as interest rates continue to fall and market fundamentals improve, and the European Central Bank's initiation of interest rate cuts in June 2024 specifically cited as triggering increased European investment activity that contributed to cross-regional flows to Europe increasing 30% year-on-year to USD 18.4 billion in H1 2024 per CBRE Global Cross-Regional Investment Volume analysis of August 2024. For instance, in February 2025, Blackstone, United States, acquired Tokyo Garden Terrace Kioicho in Japan for approximately JPY 400 billion representing one of the largest-ever property deals by a foreign investor in Japan per Japan Direct Investment Company analysis with the acquisition driven by Tokyo's central office yield gap of 1.9% being higher than New York's 1.7% and London's 1.2% per Sumitomo Mitsui Trust Research Institute estimates, confirming that relative yield advantage and currency-driven value creation are the primary drivers of the most consequential cross-border real estate acquisitions in 2025. These are some of the key factors driving revenue growth of the market.

Asia Pacific recorded the strongest regional growth in Q1 2026 at 31% year-on-year with Japan leading liquidity while Singapore recorded its highest quarterly volume on record per JLL May 2026 global trends report, confirming the continuing structural shift in global cross-border real estate capital allocation toward the Asia Pacific region that CBRE's H2 2024 analysis first identified as a 221% year-on-year surge in cross-regional inflows to the region. The Americas delivered 25% year-on-year growth in Q1 2026 with the US and Canada both performing strongly, while EMEA transactions fell 2% year-on-year coming off the heels of a particularly robust Q1 2025 with the UK and Germany leading European liquidity and Spain, Poland, the Netherlands, and Portugal demonstrating impressive growth per JLL. All five of the world's largest real estate services firms CBRE, JLL, Cushman and Wakefield, Colliers, and Newmark upgraded their financial outlooks for 2025 following a strong second quarter performance, marking the first time since the pandemic that all five raised expectations in the same quarter per CoStar reporting of August 2025, with CBRE specifically reporting record second-quarter global leasing revenue and expectations to reach a new earnings high in 2025 just two years after the market hit its lowest point in 2023. These are some of the key factors driving revenue growth of the market.

However, the global cross-border real estate investment market faces structural constraints that temper the pace of capital redeployment and cross-regional transaction volume recovery through the forecast period. Uncertainties about tariffs and trade policies specifically the US tariff environment introduced in early 2025 could inhibit cross-regional investment in the United States in the near term per CBRE's H2 2024 Global Real Estate Capital Flows analysis, with policy uncertainty elevating the risk premium that cross-border investors assign to US assets and creating the conditions where some international investors may prefer to deploy capital into markets with more stable trade and regulatory frameworks during periods of heightened US policy volatility. Global geopolitical volatility and the recent energy crisis were specifically noted by JLL in its May 2026 global trends report as posing new uncertainty, although not currently affecting transactional volumes, with JLL warning that prolonged challenges may raise the risk of future central bank rate increases as well as heightened development and operational costs. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, affect cross-border real estate investment activity through the energy operating cost exposure of the industrial logistics, data centre, and hotel assets that attract the highest cross-border capital flows, with LNG price-linked electricity costs in the Asia Pacific and European markets that are the fastest-growing cross-border investment destinations creating margin risk for cross-border investors whose underwriting assumptions are based on stable energy cost forecasts. These factors substantially limit global cross-border real estate investment market growth over the forecast period.

The global cross-border real estate market in 2025 and 2026 is the most geographically dispersed it has ever been. In any prior cycle from 2005 to 2019, the answer to where cross-border capital was flowing was straightforward: London, New York, Paris, Sydney, Singapore. These were the five cities that absorbed the overwhelming majority of cross-border institutional real estate capital because they combined liquidity, legal certainty, asset quality, and currency exposure into a package that institutional mandates could underwrite without board-level questions about the destination's risk profile. The 2025 to 2026 cycle is different. Tokyo is the world's top destination for direct real estate investment in Q1 2025. Singapore recorded its highest quarterly volume on record in Q1 2026. Warsaw and Porto are showing impressive year-on-year growth per JLL. Spain is in the growth cohort. The geographic broadening of cross-border capital flows reflects three structural shifts: the global search for yield in a world where prime London and Manhattan assets trade at historically compressed yields; the return of currency-driven opportunistic investment in markets where yen weakness has made Japanese assets cheaper in dollar terms than at any point in the past 30 years; and the maturation of cross-border institutional infrastructure in markets that would previously have been considered frontier allocations for North American and European pension funds." Troview Intelligence Head of Global Cross-Border Real Estate Investment Research

SEGMENT INSIGHTS

Four Regions Defining Global Cross-Border Real Estate Capital Flows

ASIA PACIFIC TOKYO #1 GLOBAL Q1 2025, APAC Q1 2026 +31%, SINGAPORE QUARTERLY RECORD

| Tokyo Q1 2025 Volume | APAC Cross-Regional Inflows H2 2024 | APAC Q1 2026 Growth | Singapore Q1 2026 |

| USD 11 Billion #1 global city (JLL, ahead of NYC) | +221% YoY to USD 6.3B (CBRE) | +31% YoY strongest global region (JLL May 2026) | Highest quarterly volume on record (JLL) |

Asia Pacific emerged as the dominant story of the global cross-border real estate capital flow recovery, with Tokyo claiming the world's top spot for direct real estate investment in Q1 2025 at USD 11 billion, surpassing New York at USD 7.3 billion and Dallas-Fort Worth at USD 6.3 billion per JLL data cited in Tokyo Portfolio analysis, as foreign capital attracted by Japan's above-global yield gap, yen-driven acquisition cost advantages, and rapidly rising office rents executed the largest cross-border property transactions in any single city market globally. The APAC Q1 2026 regional growth of 31% year-on-year the strongest of any region per JLL's May 2026 global trends report confirms that the 221% year-on-year surge in cross-regional inflows to Asia Pacific documented by CBRE in H2 2024 was not a one-period anomaly but the beginning of a sustained structural reorientation of global institutional real estate capital toward Asian gateway markets. Tokyo, Sydney, and Singapore are expected to remain the top three Asia Pacific investment destinations per CBRE's Asia-Pacific Investor Intentions Survey, with the industrial and logistics sector particularly attractive to cross-regional investors alongside increased office sector interest in Sydney and Tokyo.

EUROPE +30% H1 2024, UK HOTEL/OFFICE BOOM, ECB RATE CUTS, 75% SURVEY POSITIVE

| Cross-Regional Flows to Europe H1 2024 | London Inflows H1 2024 | CBRE European Investor Survey | ECB Rate Cutting |

| +30% YoY to USD 18.4 Billion (CBRE) | +100% YoY doubled (CBRE) | 75% expect increased investment activity 2025 | June 2024 cycle initiated CBRE forecast 2.15% Eurozone |

Europe's cross-border real estate investment market recorded a 30% year-on-year increase in cross-regional inflows to USD 18.4 billion in H1 2024 per CBRE Global Cross-Regional Investment Volume analysis, driven by North American capital flows to UK hotels and offices where cross-regional flows to London doubled year-on-year in H1 2024 and increased substantially in secondary UK cities including Manchester and Bristol. The European Central Bank's initiation of its interest rate cutting cycle in June 2024 with CBRE forecasting policy rates falling to 2.15% for the Eurozone and 3.75% for the UK by year-end 2025 provided the monetary policy backdrop that 75% of respondents to CBRE's European Investor Intentions Survey expected to translate into increased investment activity in 2025. Spain, Poland, the Netherlands, and Portugal demonstrated impressive cross-border investment growth in Q1 2026 per JLL, confirming the geographic broadening of European cross-border capital beyond the traditional London-Paris-Frankfurt primary market concentration that defined the 2015 to 2019 cycle.

AMERICAS Q1 2026 +25%, US AND CANADA STRONG, TARIFF RISK NEAR-TERM HEADWIND

| Americas Q1 2026 Growth | US Tariff Risk | Global Transaction Volume Q1 2026 | Industrial Strength |

| +25% YoY US and Canada both strong (JLL) | CBRE: could inhibit cross-regional investment short-term | USD 216 Billion (+18% YoY, JLL May 2026) | Nearshoring-driven demand Mexico FIBRA growing |

The Americas region delivered 25% year-on-year growth in Q1 2026 with the US and Canada both performing strongly per JLL's May 2026 global real estate trends report, contributing to the global Q1 2026 direct transaction volume of USD 216 billion that rose 18% year-on-year. However, CBRE's H2 2024 capital flows analysis specifically warned that uncertainties about tariffs and trade policies could inhibit cross-regional investment in the United States in the near term, with Singaporean, Japanese, and Gulf sovereign wealth investors historically the largest cross-border acquirers of US assets potentially reassessing allocation priorities in the context of elevated US trade policy uncertainty. Mexico's FIBRA market is advancing at a 5.62% CAGR driven by nearshoring-related industrial demand per AMEFIBRA (Mexican REIT association) and BMV listed FIBRA corporate disclosures, with the Mexico City and Monterrey industrial markets attracting cross-border logistics investors seeking the proximity to US consumption markets that US tariff structures on China-origin goods are making strategically valuable.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from CBRE Japan Investment MarketView series, JLL Global Real Estate Trends and Perspectives, verified company announcements, and CoStar reporting.