| TROVIEW INTELLIGENCE | Japan Cross-Border Real Estate Investment Market | Q2 2026 |

| TROVIEW INTELLIGENCE · COUNTRY INTELLIGENCE REPORT |

By Asset Class · By Capital Source · By Region · By Investor Type

Asset Profiles: Office (Tokyo Prime 3.13% Yield) · Hotel · Logistics · Residential · Data Centre

Japan's commercial real estate investment volume reached a record JPY 6.5 trillion in full-year 2025 per CBRE Japan Investment MarketView Q4 2025, up 31% year-on-year and approximately 20% above the previous annual record of JPY 5.4 trillion set in 2007, Q3 2025 alone established a new quarterly record at JPY 2.092 trillion up 68% year-on-year with large transactions above JPY 10 billion doubling in volume per CBRE, Q1 2025 saw investment rise 24% year-on-year to JPY 1.90 trillion predominantly driven by foreign investors completing multiple large-scale acquisitions above JPY 100 billion per CBRE Japan, foreign purchases of office buildings and other properties in H1 2025 reached a record high of over JPY 1 trillion double the H1 2024 level with Blackstone's approximately JPY 400 billion acquisition of Tokyo Garden Terrace Kioicho in February 2025 representing one of the largest-ever property deals by a foreign investor in Japan, Tokyo prime office NOI yields declined to a new all-time low of 3.13% in Q4 2025 per CBRE, office vacancy in Tokyo's Central 5 Wards fell to 0.9% at end-September 2025 per JLL, Japan ranked third globally for direct real estate investment after the United States and the United Kingdom across the first three quarters of 2025 per JLL, and Tokyo attracted the highest investment volume in US dollar terms among global cities surpassing both New York and London despite the yen's depreciation per JLL confirming Japan as the world's most actively targeted cross-border real estate investment destination in 2025.

| Standard License: USD 6,500 | Enterprise License: USD 9,500 |

MARKET SYNOPSIS

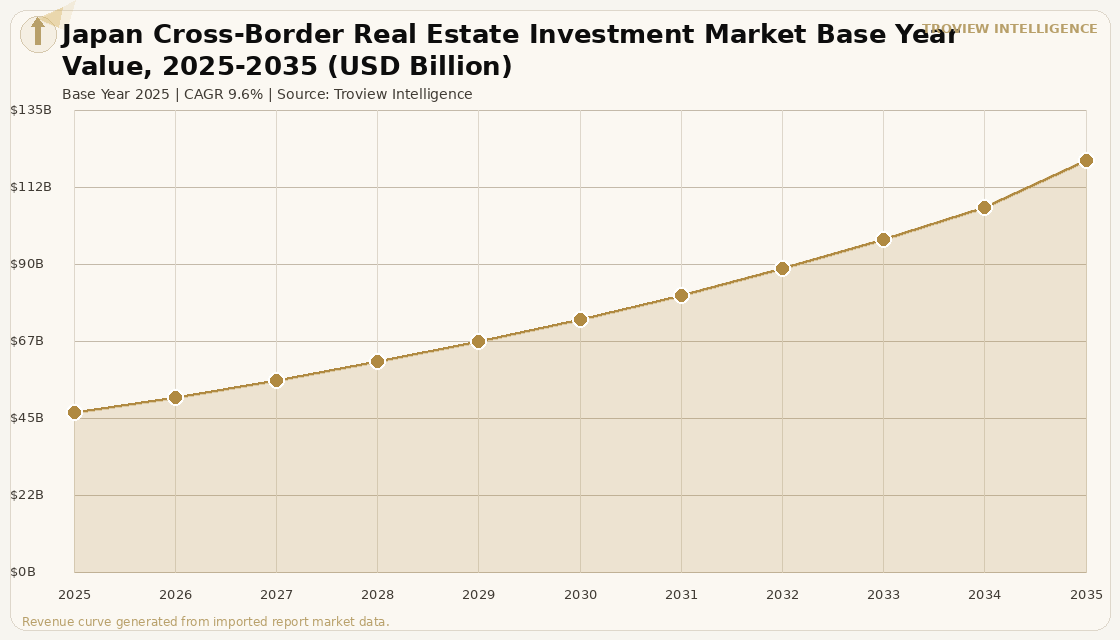

The Japan cross-border real estate investment market size was USD 46.82 Billion in 2025 and is expected to register a revenue CAGR of 9.6% during the forecast period, reaching USD 120.42 Billion by 2035. The 2025 market estimate is grounded in verified transaction data: Japan's full-year 2025 commercial real estate investment volume reached a record JPY 6.5 trillion, a 31% increase year-on-year and approximately 20% above the previous annual record of JPY 5.4 trillion set in 2007 per CBRE Japan Investment MarketView Q4 2025 published February 2 2026; Q3 2025 alone established a new quarterly record at JPY 2.092 trillion, up 68% year-on-year per CBRE Japan Investment MarketView Q3 2025 published November 4 2025; and Japan ranked third globally for direct real estate investment after the United States and the United Kingdom across the first three quarters of 2025 per JLL, with Tokyo attracting the highest investment volume in US dollar terms among global cities surpassing both New York and London. Market revenue growth is anchored in Japan's structural position as the global cross-border real estate market's highest-conviction destination for 2025 and 2026, driven by the combination of above-global office yield gaps Tokyo's central office yield gap of 1.9% exceeds New York's 1.7% and London's 1.2% per Sumitomo Mitsui Trust Research Institute estimates the yen's sustained depreciation against the US dollar making Japanese assets cheaper in USD terms than at any point in the past 30 years, and the fundamental real estate market strength of sub-1% vacancy and above-7% year-on-year rent growth in Tokyo's Central 5 Wards office market confirmed by JLL's Japan reporting. For instance, in February 2025, Blackstone, United States, acquired Tokyo Garden Terrace Kioicho in Japan for approximately JPY 400 billion, representing one of the largest-ever property deals by a foreign investor in Japan per Japan Direct Investment Company analysis, with the transaction driven by explicit yield gap analysis the 1.9% Tokyo office yield gap exceeding New York and London and by Japanese listed company balance sheet reform creating a pipeline of corporate real estate disposals where shareholders are increasingly advocating for property sales to improve return on equity. These are some of the key factors driving revenue growth of the market.

Foreign purchases of office buildings and other properties in H1 2025 reached a record high of over JPY 1 trillion, double the amount from the same period in 2024 per CBRE data cited by Japan Direct Investment Company analysis of September 2025, with office properties accounting for more than 40% of the total foreign investment volume and multiple large-scale deals above JPY 100 billion driving the record pace of Q1 2025 foreign acquisition activity per CBRE Japan Investment MarketView Q1 2025. The pipeline of Japanese corporate real estate disposals driven by shareholder pressure to improve asset efficiency is creating the supply of investible assets that sustains cross-border transaction activity beyond the opportunistic hotel and tourism-driven transactions that characterised Japan's first wave of foreign real estate interest in 2022 to 2023, with Sapporo Holdings announcing its exit from the real estate business and plans to sell prime properties including Ebisu Garden Place in central Tokyo per Japan Direct Investment Company analysis, and with Nissan Motor's headquarters sale mentioned as a large-scale deal emerging in H2 2025. LaSalle Investment Management's Co-Head of Asia Pacific Kunihiko Okumura confirmed that foreign investors are considering joint strategies that combine corporate acquisitions with real estate divestments, creating an integrated corporate-to-real estate investment opportunity that is unique to Japan's combination of corporate balance sheet reform and commercial real estate market strength. These are some of the key factors driving revenue growth of the market.

However, the Japan cross-border real estate investment market faces structural constraints that temper the pace of transaction activity through the forecast period. Rising Bank of Japan interest rates confirmed by the majority of investors surveyed by CBRE expecting further rate increases over the next 12 months per CBRE Japan Investment MarketView Q2 2025 create the risk of yield expansion in a market where Tokyo prime office NOI yields have already compressed to a new all-time low of 3.13% in Q4 2025, with future Bank of Japan rate hikes potentially reducing the 1.9% yield gap advantage that is the primary driver of cross-border capital allocation to Japan if yen-denominated financing costs rise faster than rental income growth. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, directly affect Japan's cross-border real estate investment market through the country's near-total dependence on LNG-fired electricity generation, with the 24-hour operations of the office buildings, logistics facilities, hotels, and data centres that attract cross-border foreign investment in Japan exposed to LNG spot price movements that increase operating costs and reduce the net cash yields that underpin cross-border investment underwriting assumptions. The Foreign Exchange and Foreign Trade Act's notification requirements for real estate acquisitions by foreign investors in Japan including areas designated as important for national security create regulatory compliance obligations for cross-border investors that require specialised legal and regulatory advisory support and can extend transaction timelines for large-scale acquisitions in commercially sensitive areas including defence-adjacent locations. These factors substantially limit Japan cross-border real estate investment market growth over the forecast period.

Japan's commercial real estate investment market in 2025 broke every record that had ever been set. JPY 6.5 trillion for the full year. JPY 2.092 trillion in a single quarter. Tokyo as the world's number one city for direct real estate investment in Q1 2025. Foreign purchases doubling in H1 2025. These are not marginal improvements on a healthy baseline. They are an entirely new level of market activity that reflects a structural change in how global institutional real estate capital views Japan. The narrative has shifted from 'Japan is interesting because the yen is weak' to 'Japan is compelling because the fundamentals are strong, the yen provides additional upside, and the corporate disposal pipeline from balance sheet reform will supply investible assets at scale for the next five to seven years.' Tokyo's Central 5 Wards office vacancy at 0.9% and rents rising 7.5% year-on-year does not happen in a market where the underlying economy is not performing. Japan's economy is delivering the conditions that create premium commercial real estate returns, and the world's largest cross-border real estate investors Blackstone, GIC, LaSalle, BentallGreenOak have all recognised this simultaneously. The record volumes in 2025 are the consequence of that recognition arriving at scale." Troview Intelligence Head of Japan Cross-Border Real Estate Investment Research

SEGMENT INSIGHTS

| 03 | ASSET CLASS PROFILE ANALYSIS |

Five Asset Classes Defining Japan's Cross-Border Real Estate Investment Landscape

TOKYO PRIME OFFICE 3.13% NOI YIELD, 0.9% VACANCY, +7.5% RENTS WORLD'S MOST COMPELLING OFFICE CROSS-BORDER INVESTMENT CASE

| Tokyo Prime NOI Yield Q4 2025 | Central 5 Wards Vacancy Sep 2025 | Grade-A Rents Q1 2025 | Tokyo Yield Gap vs NYC/London |

| 3.13% new all-time low (CBRE) | 0.9% (JLL) | JPY 33,947/tsubo (+4.2% YoY, Savills) | 1.9% vs 1.7% (NYC) vs 1.2% (LDN) SMTRI |

Tokyo prime office is the highest-conviction cross-border real estate investment in the world as of 2025 to 2026 by the standard of yield gap analysis, with the Tokyo central office yield gap of 1.9% exceeding New York's 1.7% and London's 1.2% per Sumitomo Mitsui Trust Research Institute estimates as cited in Japan Direct Investment Company analysis, confirming that in a global market where prime London and New York office assets deliver returns that are insufficient to justify their capital risk for most institutional mandates, Tokyo offers the highest yield spread over local financing costs of any gateway office market globally. CBRE's Q4 2025 Japan Investment MarketView confirmed that expected NOI yields for Tokyo prime office assets slipped by 2 basis points quarter-on-quarter to 3.13% in Q4 2025, establishing a new all-time low even as the Bank of Japan raised interest rates during the quarter, confirming that investor appetite for top-tier Tokyo office assets remained strong enough to compress yields further against the upward rate pressure. JLL confirmed that vacancy in Tokyo's Central 5 Wards fell to 0.9% at the end of September 2025 with gross rents reaching JPY 37,042 per tsubo per month representing 2.4% quarter-on-quarter and 7.5% year-on-year growth, with the market having almost fully absorbed the large-scale supply delivered in 2025 and prospective tenants already shifting attention to buildings scheduled for completion in 2026 per JLL Japan reporting.

| Hotel Share of Cross-Regional Inflows H1 2024 | Q3 2025 Hotel Investment | Investor Profile | Driver |

| ~40% of all APAC cross-regional flows (CBRE) | Fourth highest ever quarterly total (CBRE) | North American investors dominant (CBRE H2 2024) | Inbound tourism recovery + yen depreciation ADR opportunity |

Japan's hotel and hospitality sector attracted approximately 40% of all cross-regional inflows to Asia Pacific in H1 2024 per CBRE's H1 2024 cross-regional investment analysis, making Japan hotels the single largest category of Asia Pacific cross-border real estate investment by volume in that period, driven by North American investors specifically targeting the combination of strong inbound tourism recovery, yen-driven acquisition cost advantages, and the ADR (average daily rate) growth opportunity from hotel properties whose rates have not fully caught up with the global dollar-denominated accommodation pricing that international tourists expect at Japanese premium hotels in the post-COVID operating environment. CBRE's Q3 2025 Japan Investment MarketView confirmed that hotel investment volume remained at its fourth highest ever quarterly total in Q3 2025, maintaining the hotel sector's above-trend performance relative to the pre-2023 investment cycle. The continuing yen weakness against the US dollar creates a near-term revenue opportunity for foreign-owned Japanese hotels whose room rates can be set in yen while foreign currency earnings are converted at below-historical exchange rates, creating the operational income premium above yen-denominated operating costs that makes hotel investments in Japan particularly attractive for North American and European cross-border investors.

| Logistics Sales Q3 2025 | E-Commerce Driver | Key Investors | Logistics Yield Trend |

| All-time quarterly high in Japan (CBRE) | Japan e-commerce growth driving modern logistics demand | GIC, Mapletree, Prologis established Japan logistics platforms | Yields at all-time lows in H1 2025 (CBRE) |

Japan's logistics and industrial sector has emerged as one of the highest-conviction cross-border real estate asset classes in the country, with retail and logistics sales volume recording all-time quarterly highs in Q3 2025 per CBRE Japan Investment MarketView Q3 2025, and logistics yields falling to all-time lows in Japan per CBRE Q1 2025 data, confirming that cross-border institutional capital has compressed Japan logistics yields to levels that reflect the structural long-term demand from e-commerce-driven last-mile and urban fulfilment logistics infrastructure requirements. GIC, Singapore's sovereign wealth fund, Mapletree Investments, and Prologis have established market-leading Japan logistics platforms over the past decade that now trade at above-market pricing relative to historical Japan logistics yield levels, as the sustained compression of logistics yields in Japan's gateway industrial corridors Greater Tokyo, Osaka, Nagoya reflects the combination of strong demand from modern logistics users, limited supply of purpose-built Grade-A logistics facilities, and sustained cross-border institutional capital allocation to the asset class that has historically delivered the most consistent risk-adjusted total returns in the Asia Pacific logistics sector.

| Tokyo Condo Average Asking Price Jul 2025 | YoY Price Change | Foreign Capital Impact | Inflation Driver |

| JPY 104.77M (70sqm) record (Tokyo Kantei) | +1.4% month-on-month July 2025 | Contributing to surging condominium prices | Foreign investors counting on inflation and rising rents |

Japan's residential real estate sector has become an increasingly important cross-border investment category, with the influx of foreign capital contributing to surging Tokyo condominium prices the average asking price in July 2025 hit a record high of JPY 104.77 million for a 70-square-metre unit, up 1.4% from the previous month per Tokyo Kantei data cited in Japan Direct Investment Company analysis. Foreign investors are explicitly counting on inflation and rising rents as core components of Japan residential real estate investment returns per analysis by CBRE's Associate Director Tomoya Nose, with Japan's post-deflation transition to positive inflation creating the rental growth environment that makes residential real estate investment return positively correlated to the broader economic reflation narrative that defines the current Japanese economic cycle. The combination of rising domestic real estate prices, yen depreciation making Japanese assets cheaper for foreign purchasers, and the structural undersupply of modern residential properties in premium Tokyo neighbourhoods creates the residential cross-border investment opportunity that is driving condominium prices to record levels in central Tokyo sub-markets including Minato, Shibuya, and Shinjuku.

| Sapporo Holdings | Nissan Motor HQ | LaSalle Strategy | Shareholder Pressure |

| Exiting real estate business Ebisu Garden Place disposal | Large-scale disposal emerging H2 2025 | Joint corporate acquisition + real estate divestment strategies | More shareholder proposals pushing for property sales (LaSalle) |

The Japanese corporate real estate disposal pipeline driven by shareholder pressure for listed companies to improve return on equity and asset efficiency by selling non-core real estate holdings is creating the supply of large-scale, prime-location commercial real estate assets that enables cross-border institutional investors to acquire above-market-quality assets at scale in Japan's gateway cities. Sapporo Holdings has decided to exit the real estate business and plans to sell prime properties including Ebisu Garden Place, a landmark mixed-use facility in central Tokyo, per Japan Direct Investment Company analysis, redirecting proceeds into growth investments for its beer business in the kind of capital reallocation that Tokyo Exchange's governance reform programme is specifically designed to incentivise from Japan's large-cap listed companies. LaSalle Investment Management's Co-Head of Asia Pacific Kunihiko Okumura confirmed that foreign investors are increasingly considering joint strategies that combine corporate acquisitions with real estate divestments an approach that creates strategic alignment between the corporate governance objectives of Japanese listed company acquirers and the real estate investment objectives of cross-border institutional capital, generating a transaction pipeline that is unique to Japan's combination of corporate balance sheet reform and premium commercial real estate market strength.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from CBRE Japan Investment MarketView series, JLL Japan reports, Japan Direct Investment Company analysis, and verified trade press.