| TROVIEW INTELLIGENCE | Hong Kong Distressed Real Estate Assets Market | Q2 2026 |

| TROVIEW INTELLIGENCE · COUNTRY INTELLIGENCE REPORT |

By Asset Class · By District · By Investor Type · By Resolution Strategy

Asset Profiles: Grade A Office · Hotel and Conversion Assets · Retail · Industrial · SME Developer NPLs

Hang Seng Bank's NPL ratio reached 6.69% as of June 30 2025, up from 1.04% as of December 31 2021, with its CRE loan exposure at HKD 123.82 billion (USD 15.87 billion) equivalent to 15.1% of its total loan book and impairment charges for CRE loans surging 224% in H1 2025 per its 1H25 financial statements, Hong Kong Grade A office values are now more than 50% below their peak with citywide Grade A vacancy at 17.5% in 2025 and aggregate vacant space of approximately 15 million square feet requiring at least seven years to absorb per J.P. Morgan Private Bank Asia and CBRE analysis, Grade A office rents fell 43% over five years per Savills with Central and Admiralty rents declining an average of 5.7% in the first nine months of 2025, Shanghai Commercial Bank was selling two NPL portfolios at deep discount comprising HKD 1.7 billion (USD 218 million) in loans secured by Hong Kong real estate per ION Analytics Debtwire, units in The Center sold at HKD 18,800 per square foot 43% below the average 2017 acquisition price per SCMP reporting, eight hotel deals with total transaction value of HKD 4.61 billion (USD 591 million) were recorded through December 12 2025 for student accommodation conversion, nine more hotels with total indicative value of HKD 7.95 billion (USD 1.02 billion) are being marketed for student dormitory conversion, and Hong Kong SME developers face HKD 210 billion in liabilities with NPL ratios at 6.69% at Hang Seng Bank per Ainvest analysis confirming Hong Kong as the most deeply distressed major financial centre commercial real estate market in Asia Pacific.

| Standard License: USD 6,500 | Enterprise License: USD 9,500 |

MARKET SYNOPSIS

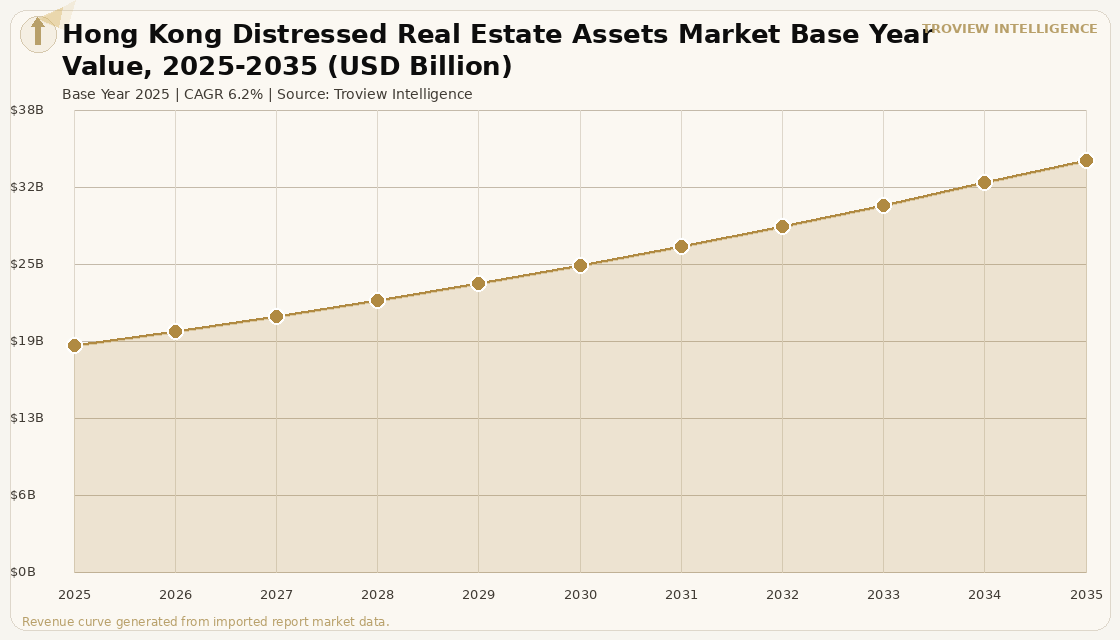

The Hong Kong distressed real estate assets market size was USD 18.64 Billion in 2025 and is expected to register a revenue CAGR of 6.2% during the forecast period, reaching USD 33.82 Billion by 2035. The market encompasses the total investible and transaction-generating activity in distressed Hong Kong commercial and residential real estate, including non-performing loan portfolio transactions, distressed asset direct sales and note acquisitions, hotel and commercial building conversion transactions, receiver-led dispositions, and the advisory and restructuring services supporting the resolution of Hong Kong's accumulated commercial real estate distress across Grade A office, Grade B office, retail, hotel, industrial, and residential asset classes. The 2025 market estimate is grounded in verified banking sector distress data and transaction evidence: Hang Seng Bank's NPL ratio grew to 6.69% as of June 30 2025 from 1.04% as of December 31 2021 per its 1H25 financial statements, with the bank's CRE loan exposure at HKD 123.82 billion (USD 15.87 billion) equivalent to 15.1% of its total loan book, and impairment charges for CRE loans surging 224% in H1 2025; Hong Kong's five domestic systemically important banks collectively hold 25.75% of their loan portfolios in CRE per Ainvest analysis; and Hong Kong Grade A office values are now more than 50% below their peak per J.P. Morgan Private Bank Asia analysis of March 2026. Market revenue growth is anchored in the structure of Hong Kong's commercial real estate distress which is not a single-event crisis but a multi-year rolling resolution process driven by the convergence of five simultaneous structural pressures: the hybrid work-driven Grade A office demand destruction that has accumulated 15 million square feet of vacant space requiring at least seven years to absorb per CBRE, the Chinese mainland developer deleveraging that has reduced cross-border property investment from mainland developers into Hong Kong, the elevated global interest rate environment that has made refinancing at 2019 to 2021 era LTV ratios impossible at current market values, the demographic and business confidence shift that followed the 2020 national security law implementation, and the excess supply of Grade B and Grade C office, retail, and industrial assets that accumulated during Hong Kong's peak development cycle of 2018 to 2022. For instance, in 2025, eight hotel deals with a total transaction value of HKD 4.61 billion (USD 591 million) were recorded through December 12 2025 for conversion into student dormitories per ION Analytics analysis, driven by the surge in students from mainland China and overseas, with an additional nine hotels carrying total indicative value of HKD 7.95 billion (USD 1.02 billion) being marketed for student dormitory conversion confirming that adaptive reuse from distressed hotel and commercial assets into education sector accommodation is the most active distressed resolution transaction category in the Hong Kong market in 2025. These are some of the key factors driving revenue growth of the market.

The total investment consideration in Hong Kong's capital market reached HKD 34.0 billion year-to-date as at December 8 2025, up 11.1% from the full-year 2024 total of HKD 34.6 billion-equivalent per Cushman and Wakefield's December 2025 Hong Kong market review, confirming that distressed pricing has attracted both end-user and opportunistic investment capital back to the market at levels above the prior year even in a still-challenging environment. The softer pricing level has made the office sector attractive to end-users and long-term investors especially for assets in prime locations per Cushman and Wakefield, with notable office transactions including Alibaba and JD.com in Q4 2025 suggesting that Chinese technology companies are opportunistically deploying capital in Hong Kong Grade A office at below-peak pricing that represents long-term value relative to the GBA business presence these companies maintain in Hong Kong's financial and professional services ecosystem. JLL's December 2025 year-end review confirmed that after a six-year correction that began in late 2019, Hong Kong's property market has turned the corner with office leasing and housing markets leading the recovery in Q4 2025, with JLL forecasting Central's Grade A office rents and mass residential prices to rebound 0% to 5% in 2026 establishing the first positive rent recovery outlook for Hong Kong office since the correction began. These are some of the key factors driving revenue growth of the market.

However, the Hong Kong distressed real estate assets market faces structural constraints that limit the pace of distressed resolution and market value recovery through the forecast period. Hong Kong's Grade A office sector remains the weakest segment of the city's property market with citywide Grade A vacancy rates at 17.5% in 2025 and values now more than 50% below their peak per J.P. Morgan Private Bank Asia March 2026 analysis, with JLL's year-end 2025 report confirming that aggregate Grade A office vacancy rose from approximately 5 million square feet in mid-2019 to slightly above 15 million square feet as of end-2024 a volume that is larger than the size of all existing offices in the prime Central district and that will require at least seven years to be absorbed at current absorption rates per CBRE. Prime warehouse vacancy rates have surged to a decade-high of 10.1% at end-2025 with rents down 7.2% per JLL, adding industrial distress to the primarily office-concentrated commercial property correction and creating the multi-sector vacancy overhang that makes a rapid Hong Kong commercial real estate recovery structurally improbable within the near-term forecast horizon. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, affect Hong Kong distressed real estate through the electricity cost transmission in Hong Kong's near-totally LNG-dependent power generation system, with the operating cost pressure on Grade A office buildings, hotels, and retail centres directly reducing the net operating income that distressed asset acquirers can underwrite when establishing acquisition prices for Hong Kong commercial real estate in the current operating environment. These factors substantially limit Hong Kong distressed real estate assets market growth over the forecast period.

Hong Kong's commercial real estate distress is qualitatively different from the US office distress because the demand destruction in Hong Kong has multiple non-cyclical components that interest rate normalisation alone will not fix. US office is distressed because hybrid work reduced space demand by 15% to 30% in most markets a demand shock that is real and secular but that leaves 70% to 85% of the pre-COVID demand in place. Hong Kong's Grade A office distress has a demand component (hybrid work, same as everywhere else), a supply component (15 million square feet of vacant space that took five years to accumulate), and a business composition component where a meaningful share of the tenants who drove the 2019 peak demand international law firms, investment banks, Chinese mainland conglomerates with Hong Kong listing and advisory operations have either right-sized, relocated to Singapore, or reduced their Hong Kong presence in ways that reflect structural rather than cyclical decisions. The seven-year vacancy absorption timeline that CBRE calculates is not a pessimistic scenario. It is a mathematical consequence of current net absorption rates applied to current vacant stock. That timeline creates a very specific investor mandate: patient capital with a cost of carry that can survive seven years of below-stabilised occupancy while collecting a discount to replacement cost that compensates for that wait." Troview Intelligence Head of Hong Kong Distressed Real Estate Assets Research

SEGMENT INSIGHTS

| 03 | ASSET CLASS PROFILE ANALYSIS |

Five Asset Classes Defining Hong Kong's Distressed Real Estate Investment Landscape

GRADE A OFFICE 17.5% VACANCY, 50%+ BELOW PEAK, 7-YEAR ABSORPTION LARGEST DISTRESSED ASSET CATEGORY IN HONG KONG

| Citywide Grade A Vacancy 2025 | Grade A Values vs Peak | Aggregate Vacant Space | Grade A Rents 5-Year |

| 17.5% (J.P. Morgan Private Bank Asia) | More than 50% below peak (J.P. Morgan, Mar 2026) | ~15 million sqft 7+ years to absorb (CBRE) | -43% per Savills 1H25 Hong Kong Offices report |

Hong Kong's Grade A office market is the most structurally distressed component of the city's commercial real estate sector, with citywide Grade A vacancy rates at 17.5% in 2025 per J.P. Morgan Private Bank Asia March 2026 analysis, values more than 50% below their peak, and CBRE's March 2026 report confirming that aggregate Grade A office vacancy rose from approximately 5 million square feet in mid-2019 to slightly above 15 million square feet as of end-2024 a vacant stock that is larger than the entire existing office market in prime Central and that will require at least seven years to absorb at current absorption rates. Grade A office rents fell 43% over the past five years per Savills' 1H25 Hong Kong Offices report, with ION Analytics confirming that Central and Admiralty Grade A rents declined an average of 5.7% in the first nine months of 2025. Notable distressed or deep-discount Grade A office transactions in 2025 and 2026 include Alibaba and JD.com's Q4 2025 opportunistic acquisitions per J.P. Morgan, and estate sales of floors in The Center at HKD 18,800 per square foot 43% below the average price at which the consortium acquired the building in 2017 per SCMP reporting confirming that distressed sellers are accepting marks far below peak-cycle valuations and that opportunistic buyers are finding entry points that represent compelling long-term value if Hong Kong's broader economic and financial centre positioning stabilises. JLL's December 2025 year-end review provided the first positive signal in years, noting that Central and Tsimshatsui registered rental growth of 0.5% and 0.2% respectively in H2 2025, driven by hedge fund and private banking expansion.

HOTEL AND STUDENT ACCOMMODATION CONVERSION HKD 4.61B (USD 591M) COMPLETED 2025, HKD 7.95B (USD 1.02B) PIPELINE

| Completed Hotel Deals 2025 | Hotels Being Marketed | Demand Driver | Government Support |

| HKD 4.61B (USD 591M) 8 deals (ION Analytics) | HKD 7.95B (USD 1.02B) 9 hotels for student dorms | Mainland Chinese and overseas student surge at HK universities | HK Government July 2025 pilot hotel/office to student housing |

Hong Kong's hotel and commercial building adaptive reuse conversion market has emerged as the most active and most government-supported distressed asset transaction category in 2025, with a total of eight hotel deals carrying a total transaction value of HKD 4.61 billion (USD 591 million) recorded through December 12 2025 for conversion into student dormitories per ION Analytics Debtwire reporting, driven by the surge in students from mainland China and overseas that has created unprecedented demand for quality student accommodation in Hong Kong's university catchment areas. The pipeline of additional student accommodation conversion opportunities is substantial: nine hotels with a total indicative value of HKD 7.95 billion (USD 1.02 billion) are being marketed for sale specifically for student dormitory conversion per ION Analytics, creating a combined completed-plus-pipeline conversion transaction market of approximately HKD 12.56 billion (USD 1.61 billion) in a single year. The Hong Kong government's July 2025 pilot programme to convert offices and hotels into student accommodation announced in the Policy Address 2024 per JLL December 2024 market review provides the regulatory framework and institutional credibility that enables banks to assess loan applications for conversion projects, landlords to obtain planning permission for use-change, and institutional investors to underwrite conversion economics with confidence in the regulatory pathway.

| High Street Vacancy Q4 2025 | Retail Sales YoY | Capital Values Forecast 2026 | Divergence |

| 6.6% lowest since pandemic (Cushman and Wakefield) | Positive since May 2025 (+6% YoY by highest level Feb 2020) | High Street shops expected to fall 5-10% (JLL Dec 2025) | Central and Mongkok resilient; lower-tier streets struggling |

Hong Kong's retail real estate market presents a mixed distress picture, with JLL's December 2025 year-end review confirming that the average high street vacancy rate fell to 6.6% in Q4 2025 the lowest level since the pandemic while simultaneously forecasting that prices of high street shops are expected to fall 5% to 10% in 2026, reflecting the divergence between improving leasing activity and continued capital value pressure from the combination of high interest rates, the structural shift in consumer behaviour driven by northbound shopping to mainland China, and the polarisation between prime locations in Central and Mongkok that attract tenants at improving rents and lower-tier streets where vacancy remains structurally elevated despite highly negotiable rents per JLL and Cushman and Wakefield analysis. Retail sales showed signs of stabilisation with monthly sales recording year-on-year increases since May 2025 per Cushman and Wakefield's December 2025 review, backed by improved tourist arrivals and more sustained local consumption, with J.P. Morgan Private Bank Asia confirming that Hong Kong retail sales growth reached the highest level since February 2020 at approximately 6% year-on-year backed by a strong 40% year-on-year growth in tourist arrivals.

| Prime Warehouse Vacancy End-2025 | Prime Warehouse Rents | Modern Logistics Vacancy | Driver |

| 10.1% decade-high (JLL Dec 2025) | -7.2% (JLL Dec 2025) | 9.4% up from 8.2% in Q4 2023 (Knight Frank) | 3PLs scaling back amid retail/F&B sector downturn |

Hong Kong's industrial and logistics real estate sector has added a new dimension to the city's commercial property distress cycle in 2025, with prime warehouse vacancy rates surging to a decade-high of 10.1% at end-2025 with rents down 7.2% per JLL's December 2025 year-end review, and overall industrial vacancy reaching a record high of 8.2% per Knight Frank with modern logistics facilities at 9.4% vacancy up from 8.2% in Q4 2023 largely driven by third-party logistics operators scaling back operations amid economic uncertainty and the downstream impact of the retail and food and beverage sector downturns on distribution supply chains. The industrial sector's decade-high vacancy represents a structural shift from the pre-pandemic period when Hong Kong's industrial market was among the tightest in Asia Pacific, with the combination of e-commerce supply chain localisation trends that bypassed Hong Kong in favour of direct mainland China fulfilment, the reduction in Hong Kong's role as an import-export hub for mainland China-origin goods following geopolitical trade friction, and the physical constraints of Hong Kong's limited industrial land stock creating the mismatch between available industrial supply and a reduced demand base that sustains elevated vacancy despite the city's strategic logistics position.

SME DEVELOPER NPLs AND BANKING SECTOR DISTRESS HKD 210B SME LIABILITIES, HANG SENG NPL 6.69%, D-SIBs 25.75% CRE EXPOSURE

| HK SME Developer Liabilities | Hang Seng NPL Ratio June 2025 | D-SIBs Collective CRE Exposure | Shanghai Commercial Bank |

| HKD 210 Billion (Ainvest analysis) | 6.69% (from 1.04% Dec 2021) | 25.75% of total loan portfolios | Selling HKD 1.7B NPL portfolios at deep discount |

Hong Kong's small and medium-sized enterprise property developer sector is at the epicentre of the banking sector's commercial real estate NPL formation cycle, with SME developers facing liabilities exceeding HKD 210 billion per Ainvest analysis, Hang Seng Bank's impairment charges for CRE loans surging 224% in H1 2025, and the bank's NPL ratio growing from 1.04% as of December 31 2021 to 6.69% as of June 30 2025 per its 1H25 financial statements reflecting the concentration of Hong Kong's SME developer distress in Hang Seng's loan book as the most CRE-exposed of the five domestic systemically important banks with a CRE loan exposure of 15.1% of its total loan book per S&P data. Shanghai Commercial Bank's reported intention to sell two NPL portfolios at deep discount by year-end 2025, comprising HKD 1.7 billion (USD 218 million) in loans to Stan Group and Star Group Asia secured by Hong Kong real estate per ION Analytics Debtwire reporting of November 19 2025, illustrates the active NPL portfolio sale market through which Hong Kong's smaller banks are seeking to reduce their CRE concentration and recognise losses on the SME developer exposures that have been classified as non-performing through the 2024 to 2025 cycle. The one-month HIBOR's decline from 3.73% in March 2025 to 0.72% by June per Ainvest data provides the refinancing environment that has supported some borrowers in avoiding default, but the structural gap between peak-cycle property values, current market values, and original loan amounts remains too large for rate normalisation alone to resolve.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from ION Analytics Debtwire, J.P. Morgan Private Bank Asia, JLL Hong Kong, Cushman and Wakefield, CBRE, Ainvest, and verified trade press.