| TROVIEW INTELLIGENCE | New York Real Estate Investment Trust Market | Q2 2026 |

| TROVIEW INTELLIGENCE · CITY INTELLIGENCE REPORT |

By Asset Class · By Borough · By REIT Operator · By Sub-Market

Sub-Market Profiles: Midtown Manhattan · Downtown Manhattan · PENN District · Brooklyn and Queens · NYC Metro Residential

New York City's REIT market is anchored by SL Green Realty Corp. Manhattan's largest office landlord with interests in 56 buildings totalling 31.4 million square feet which leased 1.7 million square feet through mid-September 2025 and acquired the Park Avenue Tower for USD 730 million in early 2026, Vornado Realty Trust which owns and manages a 26-million-square-foot portfolio of premier New York City office, retail, and multifamily assets including nearly 2 million square feet of Manhattan street retail as the largest owner and manager of street retail in Manhattan, is developing the new PENN DISTRICT, and completed a USD 161 million refinancing of 61 Ninth Avenue in May 2026, Empire State Realty Trust's Empire State Building flagship, Paramount Group whose 13-million-square-foot NYC and San Francisco office portfolio attracted second-round bidding from SL Green, Vornado, Blackstone, and Rithm Capital in August 2025, and the JLL US Office Market Dynamics report confirming a new post-pandemic high in office leasing activity in Q4 2025 with office sales rising for seven consecutive quarters confirming New York City as the world's highest-value urban REIT market and the primary battleground for trophy office real estate capital allocation in 2025 and 2026.

| Standard License: USD 2,200 | Enterprise License: USD 9,500 |

MARKET SYNOPSIS

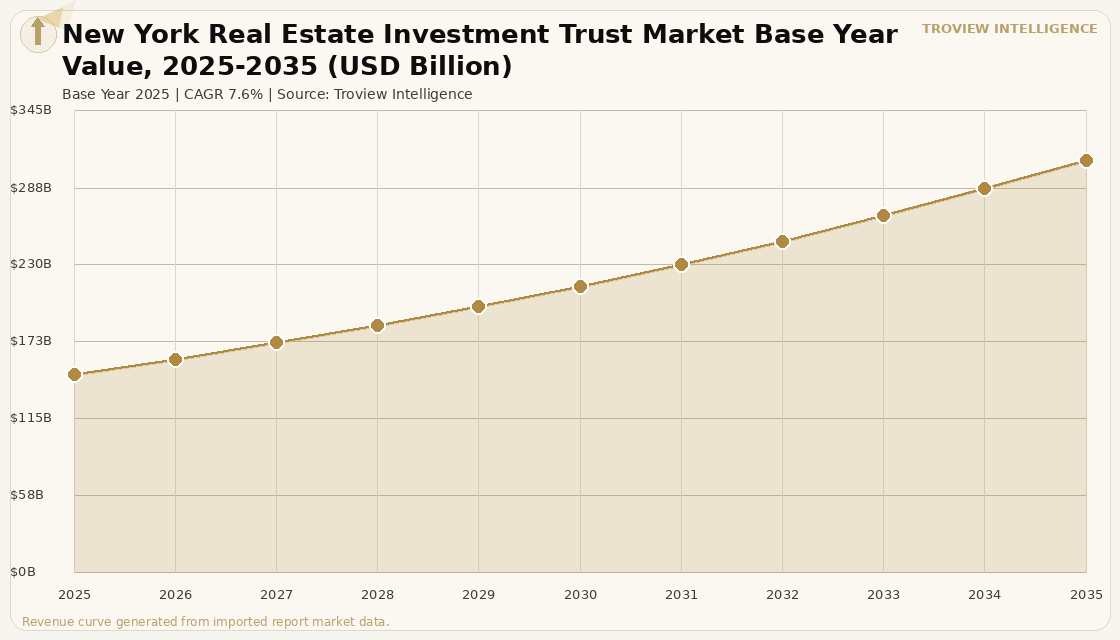

The New York real estate investment trust market size was USD 148.46 Billion in 2025 and is expected to register a revenue CAGR of 7.6% during the forecast period, reaching USD 308.14 Billion by 2035. The 2025 market estimate encompasses the combined market capitalisation of New York City-focused or New York City-headquartered publicly listed REITs with primary asset concentrations in the five boroughs and the adjacent New York metropolitan area, including office REITs, residential REITs, retail REITs, diversified REITs, and the mortgage REIT and non-traded REIT segments that manage New York City commercial and residential real estate debt and equity. Market revenue growth is anchored in New York City's irreplaceable position as the world's most globally connected, highest-value, and most institutionally capitalised commercial real estate market, generating the pricing power and capital depth that make Manhattan office, retail, and residential assets the global benchmark for trophy urban real estate valuations across all property classes. SL Green Realty Corp. is Manhattan's largest office landlord with interests in 56 buildings totalling 31.4 million square feet, having leased 1.7 million square feet through mid-September 2025 and tracking to exceed its 2 million square foot annual leasing goal per Crain's New York Business reporting, with the company's One Vanderbilt tower valued by analyst Piper Sandler's Alexander Goldfarb at USD 4.7 billion and the Park Avenue Avenue Tower acquisition for USD 730 million in early 2026 per Motley Fool analysis confirming SL Green's systematic accumulation of trophy Class A Manhattan office assets at what management believes are below-replacement-cost valuations relative to the long-term income potential of the Park Avenue office corridor. For instance, in May 2026, Vornado Realty Trust, United States, completed a USD 161 million refinancing of its 45.1% owned joint venture at 61 Ninth Avenue a 194,000 square foot office and retail property in the Meatpacking district of Manhattan fully leased to Aetna and Starbucks carrying a SOFR plus 3.00% interest-only rate maturing in March 2029 per Vornado Realty Trust press release of May 12 2026, illustrating the continued availability of institutional construction and refinancing debt for fully-leased Class A Manhattan properties in well-positioned non-Midtown locations. These are some of the key factors driving revenue growth of the market.

Vornado Realty Trust, a fully integrated equity REIT and one of the preeminent owners, managers, and developers of office and street retail properties, manages a 26-million-square-foot New York City portfolio of premier office, retail, and multifamily assets per Yahoo Finance company description, with additional flagship assets in Chicago's THE MART and San Francisco's 555 California Street, is the largest owner and manager of street retail in Manhattan with a portfolio of more than 2.4 million square feet of flagship stores for marquee brands, and is developing the new PENN DISTRICT the redevelopment of the area surrounding Madison Square Garden including the Penn 1 and Penn 2 towers where Vornado has been leasing space at up to USD 130 per square foot per Crain's New York Business reporting. Short interest in Vornado's stock declined from 13% to 8% in the year preceding October 2024 per Piper Sandler analysis, signalling that the institutional short thesis on New York City office REITs has materially dissipated as the JLL Q4 2025 leasing high confirmed the office market recovery trajectory. The Paramount Group strategic sale process that attracted second-round bidding from SL Green, Vornado, Empire State Realty Trust, Blackstone, Rithm Capital, and a partnership between DivcoWest and Dubai-based Saray Capital in August 2025 per industry reporting, covering Paramount's portfolio including 1301 Avenue of the Americas and 31 West 52nd Street at 88% occupancy as of Q2 2025, demonstrates that major institutional and REIT capital views New York City office assets as attractive at current valuation levels. These are some of the key factors driving revenue growth of the market.

However, the New York City REIT market faces structural constraints that limit the pace of market capitalisation recovery and new REIT acquisition activity through the forecast period. The elevated interest rate environment maintained through 2025 has created significant debt service pressure for New York City REIT balance sheets with high leverage ratios, with SL Green carrying approximately USD 11 billion in debt that is highly sensitive to interest rate changes with falling rates enabling refinancing of the USD 1.4 billion mortgage for 11 Madison Avenue due next September and improving the economics of new asset acquisitions per Crain's New York Business analysis. The Paramount Group SEC investigation into related-party transactions and executive compensation disclosed in July 2025, combined with the broader historical pattern of New York City office REIT corporate governance challenges, creates a reputational risk environment that requires institutional REIT investors in the New York office market to conduct particularly thorough governance due diligence alongside conventional financial underwriting. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, affect New York City REIT operating costs through the natural gas and electricity price transmission in Con Edison's New York distribution system, with the 24-hour office lobbies, HVAC systems, and data-intensive financial services tenant infrastructure of Manhattan Class A office buildings generating above-average energy consumption per square foot that exposes New York City REIT operating income to LNG-linked electricity price volatility. These factors substantially limit New York real estate investment trust market growth over the forecast period.

The New York City office REIT recovery story in 2025 and 2026 is not a story about the office market returning to 2019. It is a story about trophy assets in trophy locations separating permanently from the broad market. One Vanderbilt valued at USD 4.7 billion by Piper Sandler is not the same asset as a 1980s-vintage Midtown tower with insufficient floor-to-ceiling height for modern trading desk configurations. The Park Avenue corridor where SL Green is systematically acquiring is not the same market as Sixth Avenue's troubled towers. Vornado leasing Penn 1 and Penn 2 at USD 130 per square foot is not the same market as the suburban office parks that are being abandoned by their tenants at any price. The New York office REIT investment thesis for 2025 to 2030 is trophy asset concentration, leverage reduction, and selective Park Avenue and Hudson Yards corridor acquisition at prices that embed a conservative view of office utilisation normalisation. The REITs that execute that thesis SL Green, the Vornado Penn District will compound NAV through the recovery cycle. The ones that hold undifferentiated mid-market Manhattan office at legacy acquisition prices will not." Troview Intelligence Head of New York Real Estate Investment Trust Research

SEGMENT INSIGHTS

| 03 | SUB-MARKET ANALYSIS |

Five Sub-Markets Defining New York City's REIT Investment Geography

| Park Avenue Tower Acquisition | One Vanderbilt Valuation | SL Green Leasing 2025 | SL Green Portfolio |

| USD 730 Million SL Green early 2026 | USD 4.7 Billion (Piper Sandler analyst estimate) | 1.7 million sqft through mid-September 2025 | 56 buildings, 31.4 million sqft total interests |

Midtown Manhattan's Park Avenue corridor is the highest-value sub-market within the New York City REIT investment universe, anchored by SL Green's portfolio of trophy Class A office buildings along Park Avenue and the adjacent blocks where the combination of address prestige, floor plate efficiency, connectivity to Grand Central Terminal, and the critical mass of financial services, legal, and corporate headquarters tenants creates the most liquid and highest-valued office REIT asset geography in the world. SL Green's acquisition of the Park Avenue Tower for USD 730 million in early 2026 per Motley Fool analysis reflects a deliberate Park Avenue concentration strategy by Manhattan's largest office landlord, whose One Vanderbilt tower valued by Piper Sandler at USD 4.7 billion represents the standard-bearer for next-generation Manhattan office tower development that combines architectural distinction, LEED Platinum sustainability certification, and direct Grand Central Terminal connectivity to generate the highest per-square-foot achievable rental rates in the Midtown market. SL Green's clear track towards exceeding its 2 million square foot annual leasing goal as of mid-September 2025 per Crain's New York Business reporting, combined with Piper Sandler analyst Alexander Goldfarb describing the Manhattan office market as a sea of calm ahead of quarterly results, confirms that the Class A Midtown leasing environment has stabilised at levels consistent with REIT NOI recovery.

| Vornado Penn Lease Rate | Vornado NYC Portfolio | PENN District Status | VNO Short Interest |

| Up to USD 130/sqft Penn 1 and Penn 2 towers | 26 million sqft office, retail, and multifamily | Vornado-led redevelopment adjacent to Madison Square Garden | Declined from 13% to 8% bearish thesis unwinding |

The PENN District redevelopment zone, anchored by Vornado Realty Trust's Penn 1 and Penn 2 towers adjacent to Madison Square Garden and Pennsylvania Station, represents one of the most consequential large-scale New York City REIT development bets of the current cycle, with Vornado demonstrating that top-of-market lease rates of up to USD 130 per square foot are achievable in the redeveloped Penn 1 and Penn 2 towers despite their non-Park Avenue location, driven by the PENN District's unique combination of the world's busiest transit hub at Penn Station, the MSG entertainment venue, and the broader Hudson Yards commercial corridor that has attracted JPMorgan Chase, Pfizer, BlackRock, and other major corporate headquarters to the western Midtown extension of the Manhattan office market. Vornado's short interest decline from 13% to 8% in the year preceding October 2024 per Piper Sandler analysis, and the subsequent confirmation of Penn 1 and Penn 2 leasing momentum, confirms that the institutional short thesis on Vornado's New York City office and retail development strategy has been systematically dismantled as the Penn District asset values have materialised through lease execution at above-consensus rental rate assumptions.

| Paramount Group Portfolio | Bidders | 1301 Ave of the Americas | Downtown REIT Focus |

| 13M sqft NYC + SF strategic sale process 2025 | SL Green, Vornado, Blackstone, Rithm, DivcoWest/Saray | 88% occupancy Q2 2025; USD 900M refinancing completed | Mixed-use redevelopment, residential conversion |

Downtown Manhattan and the World Trade Centre district represent the New York REIT market's most actively transacted sub-market in 2025, with the Paramount Group's strategic sale process involving its Midtown and Downtown New York City portfolio attracting second-round bids from six of New York's most prominent institutional real estate operators SL Green, Vornado, Empire State Realty Trust, Blackstone, Rithm Capital, and DivcoWest-Saray Capital per industry reporting of August 2025 confirming broad institutional demand for New York City trophy office assets at valuations that reflect the Q4 2025 office leasing recovery momentum. Paramount's 1301 Avenue of the Americas one of its Midtown trophy assets operating at 88% occupancy as of Q2 2025 and recently refinanced with a USD 900 million loan per industry reporting illustrates the occupancy level and financing availability that characterise the upper tier of the Manhattan office REIT quality spectrum where recovery is most clearly established, in contrast to the challenged middle-market Manhattan office segments where hybrid work adoption has created more structural vacancy headwinds.

| Growth Driver | Industrial Conversion | Residential REIT | Data Centre Activity |

| Housing affordability-driven residential migration from Manhattan | Brooklyn Navy Yard, Long Island City light industrial | Equity Residential, AvalonBay Brooklyn presence | Queens industrial-to-data centre conversion pipeline |

Brooklyn and Queens represent the fastest-growing outer borough REIT investment geography in the New York City market, driven by the residential affordability dynamic that has accelerated housing demand migration from Manhattan to the outer boroughs among young professional and creative economy households priced out of Manhattan residential REIT properties and increasingly choosing professionally managed apartment communities in Brooklyn Heights, Williamsburg, Long Island City, and Astoria over Manhattan leases. Residential REITs including Equity Residential and AvalonBay Communities have expanded their Brooklyn and Queens portfolio footprints as the outer borough residential market has achieved rental rate growth competitive with Manhattan residential in absolute terms even as per-square-foot rates remain at a discount to Manhattan, generating above-average same-store NOI growth for residential REIT operators with outer borough portfolio concentrations. The Brooklyn Navy Yard and Long Island City industrial-to-data centre conversion pipeline represents an emerging new REIT investment category in the outer boroughs, as data centre operators and digital infrastructure REIT developers identify the available power capacity, fibre network density, and proximity to Manhattan's data-intensive financial services infrastructure as making Brooklyn and Queens attractive hyperscale and edge data centre development sites that complement the existing Manhattan colocation ecosystem.

| Market Dynamic | Key REITs | NYC Zoning | Return-to-City |

| Structural undersupply + high demand = rent growth above US avg | Equity Residential (NYSE: EQR), AvalonBay (NYSE: AVB) | Restrictive limits new multifamily supply in premium locations | NYC metro population recovery post-2020 migration |

The New York metropolitan area residential REIT market encompassing Manhattan, Brooklyn, Queens, the Bronx, and the New Jersey and Westchester suburban corridors served by NJ Transit and Metro-North rail connections is the highest per-unit residential rent market in the United States, with the combination of restrictive zoning that limits new multifamily supply in established neighbourhoods, the return-to-city migration recovery from the 2020 to 2021 pandemic-driven population outflow, and the structural demand from New York City's financial services, legal, technology, and media sector workforce sustaining residential REIT NOI growth at levels above the national apartment REIT average. Equity Residential and AvalonBay Communities, the two largest publicly listed apartment REITs in the United States by market capitalisation, both maintain significant New York metropolitan area portfolio concentrations that drive their above-national-average revenue per unit and same-store NOI metrics, with New York City representing one of Equity Residential's highest-revenue-per-unit markets globally. Vornado's 2,000-plus residential units in New York City including notable condominium developments at 1 Beacon Court, 220 Central Park South, and The Park Laurel per Vornado company information illustrate the integration of residential real estate into the diversified New York City REIT portfolio model that Vornado pioneered as one of the most comprehensive single-market urban REIT operators globally.

MAJOR COMPANIES

STRATEGIC DEVELOPMENTS

Ordered 2026 first. All developments sourced from verified company press releases, Crain's New York Business, Motley Fool analysis, industry reporting, and Nareit/JLL market data.