| TROVIEW INTELLIGENCE | Data Centre REIT Market | Q2 2026 |

By Geography · By REIT Type · By Asset Strategy · By Tenant Sector

Equinix posted full-year 2025 revenues of USD 9.217 billion a 5% increase year-on-year and delivered record annualized gross bookings of USD 1.6 billion for the full year, a 27% increase, while Digital Realty reported 2025 operating revenues of USD 6.113 billion, a 10% increase, with Core FFO per share growing 10.1% to USD 7.39 and a backlog of USD 817 million in annualized GAAP base rent at year-end 2025, as both REITs guided to double-digit revenue and AFFO-per-share growth in 2026 anchored in AI inference demand, hyperscale pre-leasing, and the structural scarcity of power-connected, carrier-neutral data centre real estate in established global markets.

MARKET SYNOPSIS

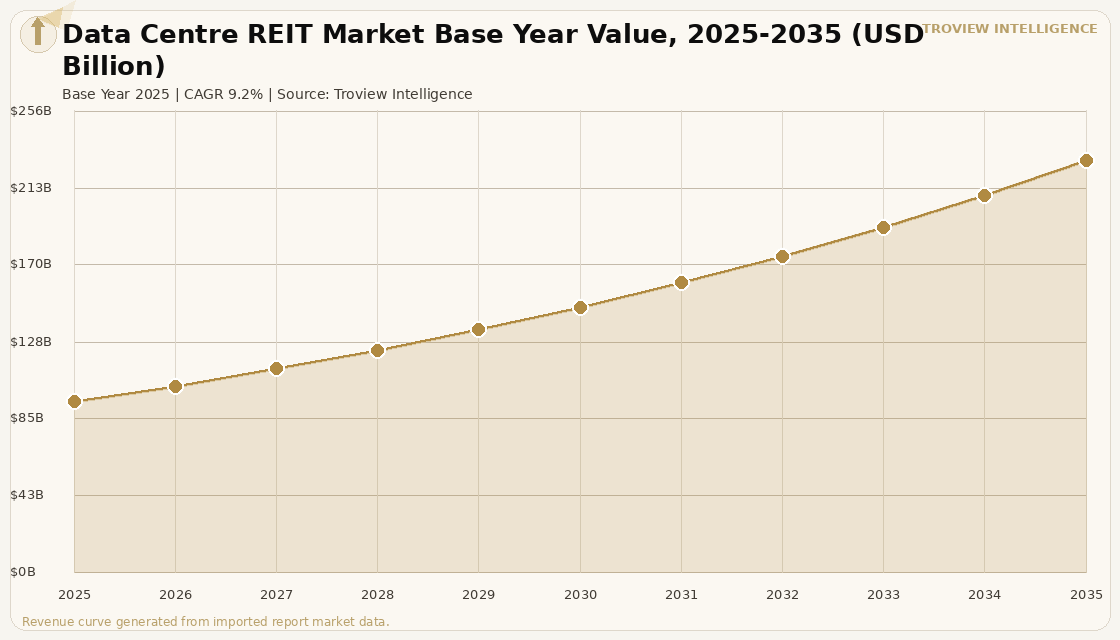

The global data centre REIT market size was USD 94.62 Billion in 2025 and is expected to register a revenue CAGR of 9.2% during the forecast period, reaching USD 228.14 Billion by 2035. Market revenue growth is supported by the structural expansion of AI inference and training workloads that require co-location in carrier-neutral, power-dense facilities operated by specialist REIT platforms, the accelerating pre-leasing of hyperscale capacity by cloud providers including Amazon Web Services, Microsoft Azure, and Google Cloud that provides long-term contracted revenue visibility to REIT balance sheets, and the entry of institutional capital into listed and unlisted data centre REIT structures attracted by the sector's inflation-linked lease escalators and the physical scarcity of power-connected sites in established markets. Equinix, United States, posted full-year 2025 revenues of USD 9.217 billion, a 5% increase year-on-year, delivered record annualized gross bookings of USD 1.6 billion for the full year representing a 27% increase, and exceeded 500,000 global interconnections for the first time in company history, guided by management to 9% to 10% revenue growth in 2026. For instance, in Q1 2026, Digital Realty Trust, United States, reported quarterly revenue of USD 1.6 billion, a 16% increase over Q1 2025, signed the largest hyperscale lease in company history, and guided to Core FFO per share of USD 7.90 to USD 8.00 for full-year 2026, representing 8% year-on-year growth, confirming the structural demand tailwind supporting both listed US data centre REITs from the same AI-driven hyperscaler capex cycle. These are some of the key factors driving revenue growth of the market.

North America dominates global data centre REIT revenue, anchored by Digital Realty's 309 data centres across global markets as of March 2026 and Equinix's portfolio of more than 144,000 cabinets with a commitment to add 24,000 further cabinets through 2027 per S&P Global Market Intelligence reporting. Digital Realty held the largest share of leased data centre power in the US in Q4 2024 at 15% per 451 Research analysis, while Equinix accounted for 4.9% of the US leased power market, reflecting the different strategic positions of the two dominant REITs Digital Realty focusing on hyperscale wholesale and Equinix on carrier-neutral interconnection co-location. Asia Pacific is the fastest-growing region for data centre REIT investment, led by Singapore-listed vehicles including Keppel DC REIT, which reported distributable income rising 55.5% year-on-year for the nine months to September 2025 with gross revenue growing 37.7% to SGD 322.4 million and net property income increasing 42.2%, driven by strategic acquisitions including the SGD 707 million Tokyo Data Centre 3 hyperscale acquisition completed in December 2025. Iron Mountain, United States, reported full-year data centre revenues of USD 416.3 million for 2025 and guided to USD 1 billion in data centre segment revenue for 2026, reflecting the accelerating migration of traditional records management REITs toward data centre asset exposure.

However, the global data centre REIT market faces structural constraints that temper the pace of expansion. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, which the IMF confirmed in March 2026 affect approximately 20% of global seaborne oil and LNG flows, are creating energy cost inflation that raises operational expenditure for data centre REITs, whose facilities consume electricity at scale and whose operating margins are sensitive to power purchase agreement pricing and utility rate movements in energy-exposed markets including Europe. Interest rate uncertainty with the Federal Reserve's trajectory influenced by energy-driven inflation affects the cost of capital for REIT balance sheets that rely on debt financing for acquisition and development programmes, with Digital Realty's USD 60.89 billion market capitalisation and leverage profile requiring consistent AFFO growth to maintain dividend coverage at payout ratios above 100%. The concentration of AI-driven hyperscale demand in Northern Virginia, which leaves Digital Realty heavily leveraged toward a single geography per S&P Global analysis, and the grid connection constraints affecting Equinix's Hertfordshire campus which required a bespoke 400 kV feed solution, represent location-specific risks that listed REIT investors must price into valuations at current AFFO multiples. These factors substantially limit global data centre REIT market growth over the forecast period.

The data centre REIT sector in 2025 and 2026 is experiencing a bifurcation that listed market investors are only partially pricing. On one side are the two dominant US REITs Equinix at USD 9.2 billion in 2025 revenues with 27% booking growth, and Digital Realty at USD 6.1 billion with 16% Q1 2026 revenue growth both of which are structurally advantaged by AI-driven hyperscaler demand that cannot be served without the carrier-neutral interconnection fabric and the hyperscale pre-leased wholesale capacity that only these platforms provide at scale. On the other side are the Asia Pacific specialist REITs, led by Keppel DC REIT with 55.5% distributable income growth in nine months to September 2025, that are pursuing the same AI demand wave but in markets Japan, Singapore, Australia where supply constraints are more severe than in Northern Virginia and where yen-denominated acquisition financing provides natural hedging advantages against JPY debt costs. The tension between these two pools of capital US-listed at scale, Asia Pacific-listed for growth is defining the REIT sector evolution for the next decade." Troview Intelligence Head of Global Data Centre REIT Research

SEGMENT INSIGHTS

By REIT Type

Listed data centre REIT segment is expected to account for a significantly large revenue share in the global data centre REIT market during the forecast period.

Based on REIT type, the global data centre REIT market is segmented into listed data centre REITs, unlisted wholesale data centre funds, and hybrid structures combining listed REIT equity with private fund co-investment. Listed data centre REITs dominate total market capitalisation, anchored by Equinix with a market capitalisation exceeding USD 80 billion and Digital Realty at USD 60.89 billion as of early 2026, both providing public market liquidity, AFFO yield transparency, and quarterly earnings disclosure that institutional investors require for benchmark-level portfolio allocation. The unlisted wholesale segment is expected to register the fastest revenue growth rate during the forecast period, driven by the entry of sovereign wealth funds, pension funds, and infrastructure managers including GIC Pte. Ltd., Brookfield Asset Management, and Blackstone Real Estate into direct data centre asset ownership outside listed REIT structures, motivated by the ability to negotiate build-to-suit hyperscale pre-leases without the quarterly earnings transparency constraints of listed REITs.

By Asset Strategy

Carrier-neutral co-location asset strategy is expected to account for a significantly large revenue share in the global data centre REIT market during the forecast period.

Based on asset strategy, the global data centre REIT market is segmented into carrier-neutral co-location, hyperscale wholesale pre-lease, hybrid interconnection-plus-hyperscale, and single-tenant build-to-suit. Carrier-neutral co-location dominates REIT revenue by asset count and by AFFO margin, as the multi-tenant structure of co-location facilities where revenue derives from rack licensing, cross-connect charges, and power billing across hundreds of tenants per facility provides the income diversification and per-megawatt revenue density that supports REIT valuation premiums. Hyperscale wholesale pre-lease is expected to register the fastest revenue CAGR during the forecast period, driven by Digital Realty's PlatformDIGITAL strategy targeting build-to-suit and powered shell facilities for Amazon Web Services, Microsoft, Google, Meta, and Oracle, with Digital Realty's USD 817 million backlog of annualized GAAP base rent at year-end 2025 providing revenue certainty for the next two to four years.

By Tenant Sector

Cloud and hyperscale tenant sector is expected to account for a significantly large revenue share in the global data centre REIT market during the forecast period.

Based on tenant sector, the global data centre REIT market is segmented into cloud and hyperscale tenants, financial services, enterprise and IT services, media and content delivery, and telecommunications. Cloud and hyperscale tenants Amazon Web Services, Microsoft Azure, Google Cloud, Meta Platforms, and Oracle dominate REIT revenue by square footage and by power consumption, with Equinix's tenant roster including all four major US cloud providers and Digital Realty serving Amazon Web Services, IBM, Oracle, and Meta at scale. Financial services is the second-largest tenant sector by co-location revenue density, as global investment banks, exchanges, and trading firms requiring carrier-neutral proximity to peer networks and market data feeds drive premium cross-connect and cage revenue per square foot in Equinix's Secaucus, Slough, Singapore, and Tokyo facilities.

REGIONAL ANALYSIS

NORTH AMERICA DOMINANT

| Equinix 2025 Revenue | Digital Realty 2025 Revenue | DLR Core FFO/Share 2025 | Equinix 2025 Gross Bookings |

| USD 9.217 billion (+5% YoY) | USD 6.113 billion (+10% YoY) | USD 7.39 (+10.1% YoY) | USD 1.6 billion (+27% YoY, record |

North America is the dominant data centre REIT market, hosting the two largest publicly traded data centre REITs globally and commanding the majority of global REIT market capitalisation in the sector. Equinix's 2025 revenues of USD 9.217 billion growing at 5% year-on-year and guided to USD 10.123 to USD 10.223 billion in 2026 representing 10 to 11% growth reflect the sustained demand from AI-driven interconnection and cloud-on-ramp workloads across Equinix's 144,000-cabinet global platform, with the company planning to add 24,000 further cabinets through 2027 and targeting a doubling of total capacity by end-2029 per CEO Adaire Rita Fox-Martin's June 2025 investor day statement. Digital Realty's Q1 2026 revenue of USD 1.6 billion, a 16% increase over Q1 2025, was anchored by the largest hyperscale lease in company history and a Core FFO guidance of USD 7.90 to USD 8.00 per share for 2026, with the company's 309 data centres globally serving over half of Fortune 500 companies through PlatformDIGITAL's build-to-suit and move-in-ready data centre suites.

ASIA PACIFIC

| Keppel DC REIT AUM (Sep 2025) | 9M 2025 Distributable Income | Tokyo DC3 Acquisition Value | Portfolio Occupancy (Sep 2025) |

| SGD 5.7 billion (25 DCs, 10 ctys) | SGD 195.3M (+55.5% YoY) | JPY 82.1 billion (~USD 530M) | 95.8% |

Asia Pacific is the fastest-growing data centre REIT region, led by Singapore-listed Keppel DC REIT, which reported gross revenue growing 37.7% year-on-year to SGD 322.4 million for the nine months to September 2025, with distributable income rising 55.5% to SGD 195.3 million and distribution per unit advancing 8.8% to 7.670 cents. The REIT completed the acquisition of Tokyo Data Centre 3 in Inzai City, Greater Tokyo, for JPY 82.1 billion (approximately USD 530 million) in December 2025, a freehold hyperscale facility fully leased to a leading global hyperscaler on a 15-year contract with annual rent escalations, expanding its Japan presence to two assets within the Asia Pacific's largest data centre market outside China. Japan's data centre market reached USD 12.76 billion in 2025 and is projected to grow at a CAGR of 20.42% to 2031, with 1.2 gigawatts of new capacity announced, planned, or under construction in 2025 alone per verified industry data, confirming the scale of the investment opportunity that Asia Pacific data centre REITs are pursuing through both direct acquisition and JPY-denominated debt financing structures.

EUROPE GROWING REIT

| European DC Colocation Market 2024 | European DC Investment CAGR to 2030 | Key EU REIT Players | Iron Mountain 2026 DC Revenue Guide |

| USD 9.45 billion (verified data) | 24.82% through 2030 | Equinix, Digital Realty, Keppel | USD 1 billion (data centre segment) |

Europe's data centre REIT market is dominated by the European portfolios of Equinix and Digital Realty, supplemented by Singapore-listed and unlisted institutional vehicles acquiring stabilised European data centre assets as a complement to Asia Pacific holdings. The European data centre colocation market was valued at USD 9.45 billion in 2024 and is projected to reach USD 35.73 billion by 2030 at a CAGR of 24.82%, with Western Europe accounting for approximately USD 101.51 billion of the estimated USD 144.03 billion in cumulative European data centre investment through 2030. Iron Mountain, United States, is transitioning from a records management REIT to a data centre REIT with USD 416.3 million in 2025 data centre revenues and a USD 1 billion 2026 guidance, representing the most visible example of a traditional REIT migrating its capital allocation toward data centre exposure in response to investor demand for AI-adjacent real estate income.