By Mall · By District · By Tenant Sector · By Operator

Dubai Mall was the most visited place on earth for two consecutive years with 111 million visitors in 2024, Mall of the Emirates maintains 98% occupancy with 40 million annual visitors, Emaar committed AED 1.5 billion to expand Dubai Mall with 279 new luxury outlets in The District, and Majid Al Futtaim committed AED 5 billion to transform Mall of the Emirates as Dubai's retail sector grew 8% in 2025, prime super-regional mall rents rose 14.9% year-on-year to AED 350 to 450 per square foot, and retail transaction values reached AED 1.1 billion in Q3 2025 alone.

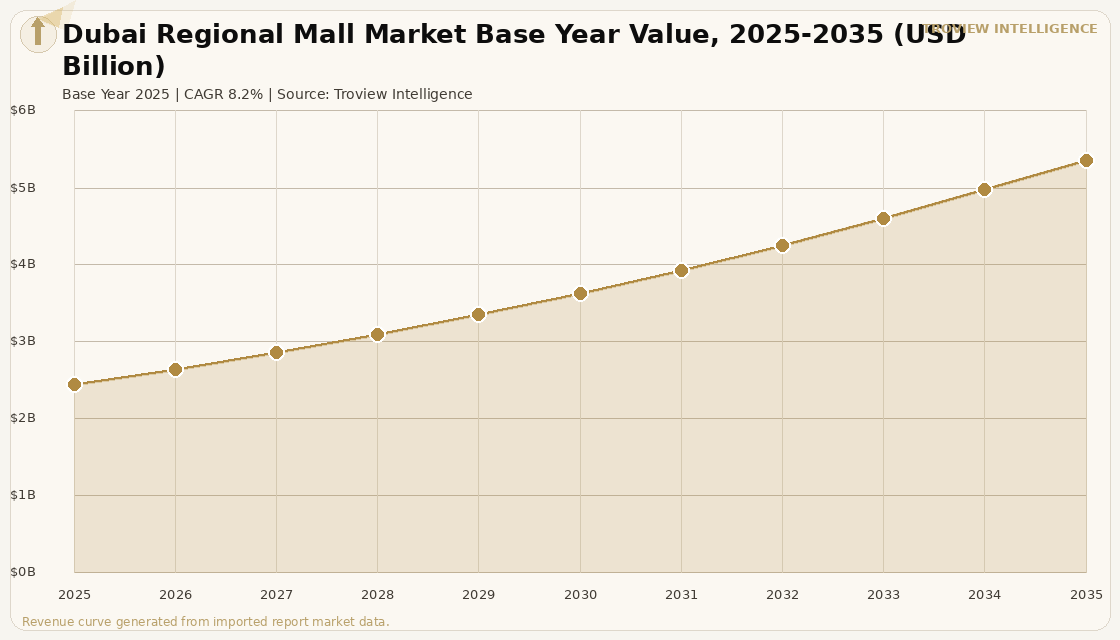

MARKET SYNOPSIS

The Dubai regional mall market size was USD 2.28 Billion in 2025 and is expected to register a revenue CAGR of 8.2% during the forecast period, reaching USD 4.99 Billion by 2035. Dubai's mall market is the highest-performing institutional retail real estate market in the world by occupancy rate, footfall per square foot, and year-on-year rent growth in the premium segment, with both Emaar Malls and Majid Al Futtaim maintaining 98% average occupancy across their respective Dubai mall portfolios in Q3 2025 per Cavendish Maxwell's quarterly retail market report. Dubai Mall ranked as the most visited place on earth for two consecutive years, achieving 111 million visitors in 2024 a 6% year-on-year increase and Emaar Properties announced in May 2025 that The District, the first phase of the AED 1.5 billion expansion, had opened with 279 new luxury outlets including 198 retail units and 81 food and beverage concepts. Retail sales transaction values in Dubai reached AED 1.1 billion in Q3 2025, the first time a single quarter exceeded the AED 1 billion threshold per Cavendish Maxwell data, and Dubai's retail sector grew 8% in 2025 driven by tourism recovery and the expatriate influx.

Dubai's regional mall market is structurally anchored by the Emaar-Majid Al Futtaim duopoly at the super-regional destination tier, where the two operators together own and manage the five most visited retail destinations in the emirate. Dubai Mall and Mall of the Emirates are more than retail assets: they are critical urban infrastructure in a city of 4 million residents where the mall is a primary social destination for residents during the long summer months when outdoor public space is unusable. The city's 85% expatriate population drawn from India, Pakistan, the UK, Europe, and dozens of other countries creates a uniquely cosmopolitan consumer base that sustains demand for global brand diversity across luxury, mid-market, and value formats within the same mall. Prime super-regional mall rents rose 14.9% year-on-year to AED 350 to 450 per square foot per year in prime locations per market data, confirming that occupier demand for Dubai's top-tier mall space is outstripping supply and enabling sustained rent growth. For instance, in April 2025, Majid Al Futtaim, UAE, launched the AED 5 billion Mall of the Emirates transformation to mark the mall's 20th anniversary, with the New Covent Garden cultural hub developed with the Dubai Performing Arts Academy opening in early 2025, the AED 165 million flyover linking Umm Suqeim Street and Sheikh Zayed Road completed, and new tenants including Ulta Beauty making their Middle East debut at the mall, per Majid Al Futtaim press release of April 2025. These are some of the key factors driving revenue growth of the market.

However, the Dubai regional mall market faces structural constraints. UAE mall landlords entered 2026 from a position of near-maximum occupancy but faced footfall pressure from a slowdown in international tourism related to regional geopolitical events, with retailers reporting reduced discretionary spending while landlords held firm on rents due to the structural lease commitments that kept tenants locked in, per AGBI reporting of April 2026. The concentration of Dubai's mall revenue in two super-regional assets Dubai Mall and Mall of the Emirates creates a market where the fortunes of a small number of operators are highly material to overall market performance. New Dubai mall supply additions, while primarily in the community and neighbourhood convenience format that serves different retail functions than super-regional destinations, create some competitive pressure at the lower-rent end of the rental curve. Saturation in the luxury retail segment at Dubai's top-tier malls poses risks for new brand entrants that cannot compete directly with the established fashion and luxury offer at Fashion Avenue and Mall of the Emirates' luxury concourse. These factors substantially limit Dubai regional mall market growth over the forecast period.

Dubai Mall at 111 million visitors is not a mall. It is a city attraction that happens to have retail attached. The Burj Khalifa, the Dubai Fountain, the Aquarium these are reasons to visit Downtown Dubai that generate millions of visits that have nothing to do with shopping. The retail operator who benefits from 111 million footfall visits is Emaar, and the brand that wants to be in that footfall stream is willing to pay AED 350 to 450 per square foot to access it. That is why the comparison to struggling malls in Ohio or Sheffield is irrelevant. Mall of the Emirates is a slightly different proposition the ski slope, the performing arts venue, the wellness club but the same logic applies: Majid Al Futtaim has created reasons to visit that are unrelated to shopping. AED 5 billion says they believe that model continues to work." Troview Intelligence Head of Dubai Regional Mall Research

SEGMENT INSIGHTS

By Mall Format

Super-regional destination malls are expected to account for a significantly large revenue share in the Dubai regional mall market during the forecast period.

Based on mall format, the Dubai regional mall market is segmented into super-regional destination malls, regional lifestyle malls, community and convenience malls, and specialty and strip retail centres. Super-regional destination malls including Dubai Mall at 13 million square feet and Mall of the Emirates at 255,000 square metres of GLA dominate market revenue per asset and command the highest per-square-foot rents, with prime location rents of AED 350 to 450 per square foot year-on-year representing 14.9% growth in 2025. Regional lifestyle malls including Dubai Hills Mall, Mirdif City Centre, and Ibn Battuta Mall serve established residential catchments at lower rent levels and deliver more stable, less tourism-dependent income. Community and convenience malls are the fastest-growing segment by new unit delivery, as the market is developing through the growth of smaller community malls focused on daily needs and convenience, a trend explicitly identified in Cavendish Maxwell's Q3 2025 Dubai retail market analysis.

By Tenant Category

Luxury and premium retail tenants are expected to account for a significantly large revenue share in the Dubai regional mall market during the forecast period.

Based on tenant category, the Dubai regional mall market is segmented into luxury and premium retail, mid-market fashion and lifestyle, food and beverage, entertainment and leisure, health and wellness, and grocery and convenience anchor tenants. Luxury and premium retail anchors Fashion Avenue at Dubai Mall, which houses over 150 luxury shopping and dining brands in a dedicated luxury precinct that is physically separated from the broader mall and functions as a standalone luxury retail destination. Food and beverage accounts for approximately 15% of Mall of the Emirates' tenant mix and has grown across Dubai's mall portfolio as operators invest in dining as the primary experiential differentiator against e-commerce. Entertainment and leisure Ski Dubai at Mall of the Emirates, the Dubai Aquarium and Underwater Zoo at Dubai Mall, KidZania Dubai, and Play DXB generate visit occasions that are wholly independent of retail and function as footfall anchors that fill the mall hours in the opposite direction to traditional anchor department stores.

By District

Downtown Dubai and the Sheikh Zayed Road corridor are expected to account for a significantly large revenue share in the Dubai regional mall market during the forecast period.

Based on district, the Dubai regional mall market is segmented into Downtown Dubai, the Sheikh Zayed Road-Al Barsha corridor, the Deira-Bur Dubai legacy retail districts, emerging suburban corridors including Dubai Hills and Dubai South, and integrated waterfront and resort districts. Downtown Dubai dominates by revenue per square metre, with Dubai Mall at the base of the Burj Khalifa generating the most concentrated retail revenue in the city. The Sheikh Zayed Road-Al Barsha corridor, anchored by Mall of the Emirates, is the city's most densely served mid-to-premium retail corridor, connecting the commercial hub of DIFC and Downtown Dubai to the residential and tourism districts of Al Barsha and the Marina. Dubai Hills Mall and the emerging Dubai South retail corridor are the fastest-growing districts by new mall supply, serving the expanding residential communities in the city's southern and inland growth direction.

MALL DEEP-DIVES

Dubai's Major Mall Destinations

| Footfall 2024 | 111 million visitors, 6% YoY growth (Emaar) | GLA | 13 million sq ft, 1,200+ stores |

| Expansion | AED 1.5 billion, The District: 279 new outlets (198 retail + 81 F&B) | Fashion Avenue | 150+ luxury brands, dedicated luxury precinct |

Dubai Mall is the world's most visited place, holding that designation for two consecutive years in 2023 and 2024 with 105 million and 111 million visitors respectively per Emaar Properties investor announcements. The mall's draw is inseparable from the surrounding Downtown Dubai ecosystem the Burj Khalifa, the Dubai Fountain, the Dubai Aquarium and Underwater Zoo, and the KidZania Dubai edutainment facility creating an integrated urban destination where millions of visits occur for reasons entirely independent of retail shopping. Emaar's AED 1.5 billion expansion, unveiled in May 2025 as The District, adds 279 luxury outlets including 198 retail units and 81 food and beverage concepts in a curated new precinct featuring terracotta palettes and wide boulevards adjacent to the Ice Rink. The District introduces tenants including Klay by Karak House for modern Emirati cuisine alongside specialty coffee concepts, hotel-quality bakeries, and international F&B brands seeking presence in the world's highest-footfall retail destination. Fashion Avenue, Dubai Mall's dedicated luxury corridor, houses over 150 luxury brands in a precinct that functions as the Gulf's primary physical luxury retail destination for international tourists and resident luxury shoppers.

| Footfall 2024 | 40 million annual visitors (Majid Al Futtaim) | Occupancy | 98% (H1 2025, Majid Al Futtaim) |

| Transformation | AED 5 billion, 20,000 m² new retail, 100+ stores, 600-seat theatre | GLA | 255,000 m², 630+ stores including 80 luxury brands |

Mall of the Emirates is Majid Al Futtaim's flagship Dubai asset and the mall most directly comparable to the world's top experiential retail destinations, combining 630 stores with 80 luxury brands, Ski Dubai, VOX Cinemas, and Magic Planet alongside a sustained investment programme that has kept it at 98% occupancy with 40 million annual visitors since 2024. The AED 5 billion transformation announced in April 2025 for the mall's 20th anniversary represents the largest single mall redevelopment investment in the UAE, adding 20,000 square metres of retail, a wellness club, the New Covent Garden cultural hub with a 600-seat theatre built with Dubai Performing Arts Academy, and an IMAX at VOX arriving in late 2026. Ulta Beauty made its Middle East debut at Mall of the Emirates in 2025, joining a series of first-to-market brand launches that have established the mall as the preferred Gulf entry point for international retail brands seeking credibility and footfall before expanding to other markets. Mall of the Emirates' tenant mix is approximately 55% fashion including luxury and mid-market, 15% food and beverage, 10% electronics, and 10% health and beauty, drawing from Dubai's diverse 3.7 million population with 85% expatriates per market analysis data.

| Location | Dubai Hills, Mohammed Bin Rashid City | Character | Community-anchored lifestyle mall, growing catchment |

| Developer | Emaar Properties | Growth Driver | Dubai Hills Estate residential development: 30,000+ homes |

Dubai Hills Mall is the most significant new super-regional mall addition to Dubai's retail landscape in the 2020s, serving the fast-expanding Dubai Hills Estate and Mohammed Bin Rashid City residential communities that are adding tens of thousands of residents to Dubai's inland southern corridor. The mall's position as the primary retail, dining, and entertainment destination for Dubai Hills Estate's 30,000 or more homes provides a structural captive catchment that delivers more predictable footfall than tourism-dependent assets. Emaar developed Dubai Hills Mall as part of the integrated Dubai Hills Estate master plan, ensuring that the retail destination was embedded into the residential community rather than positioned as a freestanding attraction. The mall's anchor strategy combining Carrefour hypermarket, a cinema, and international dining with fashion and lifestyle retail is calibrated for daily and weekly visit frequency rather than the once-a-year destination visits that Dubai Mall attracts from international tourists.

| Deira City Centre | Al Futtaim Group, oldest city centre mall, Deira heritage district | Ibn Battuta Mall | Nakheel Malls, themed international travel courts, 800 stores |

| Community Role | Serves Deira and Bur Dubai legacy residential communities | Character | Value retail, family entertainment, mid-market positioning |

Deira City Centre and Ibn Battuta Mall represent Dubai's legacy regional mall stock, serving different community functions than the super-regional destination malls of Downtown Dubai and Al Barsha. Deira City Centre, operated by Al Futtaim Group, was Dubai's original Western-style shopping centre and continues to serve the Deira and Rigga residential communities and Deira Creek heritage tourism district with mid-market fashion, hypermarket anchoring, and family entertainment. Ibn Battuta Mall, operated by Nakheel Malls, uses a themed court concept modelled on the travels of the medieval explorer Ibn Battuta Andalusia, Tunisia, Persia, India, China, and Egypt courts creating a distinctive architectural identity that differentiates it from generic mall stock. These legacy assets serve the price-sensitive and community-focused retail segments that the super-regional destination malls have progressively vacated as they concentrated on luxury, experiential, and first-to-market positioning.