| TROVIEW INTELLIGENCE | Retail Park Market | Q2 2026 |

By Geography · By Asset Format · By Anchor Tenant Type · By Occupier Sector

European retail park vacancy stands at 1.2% the tightest of any tracked retail asset class in CBRE's 155-asset European Shopping Centre Performance Index while UK retail park investment volumes grew 48% year-on-year to EUR 3.0 billion in 2024 and British Land acquired 15 retail parks for GBP 738 million in fiscal 2025, as the format's combination of affordable occupier costs, omnichannel compatibility, and necessity-anchored tenant mix delivers the income resilience that institutional capital is migrating toward from enclosed malls and high-street retail.

MARKET SYNOPSIS

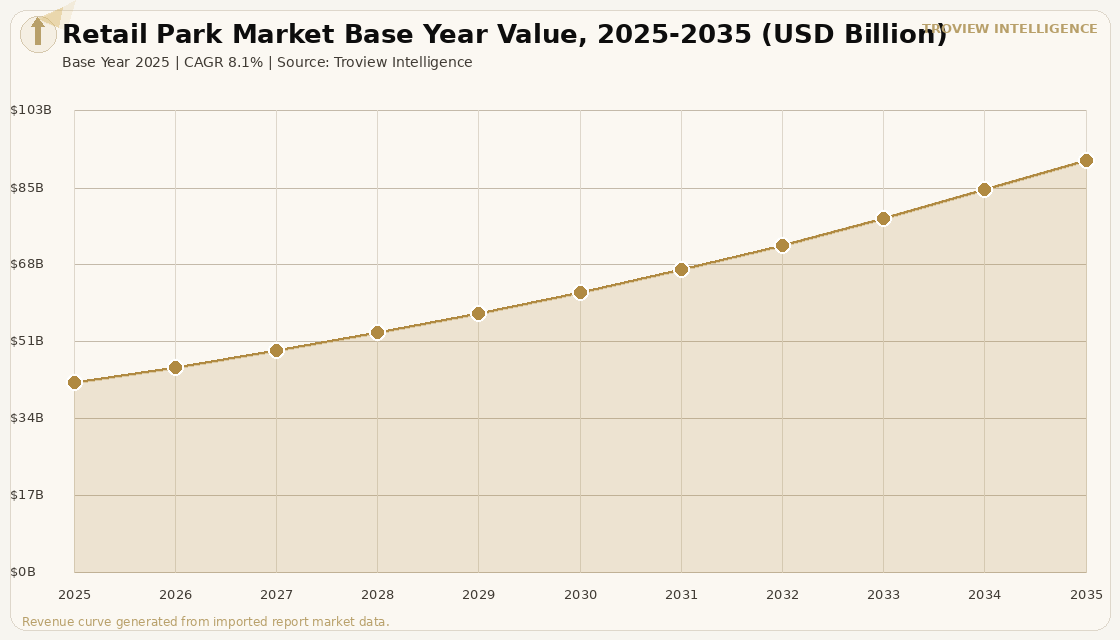

The global retail park market size was USD 42.18 Billion in 2025 and is expected to register a revenue CAGR of 8.1% during the forecast period, reaching USD 91.54 Billion by 2035. Market revenue growth is supported by structurally constrained new supply across European and North American markets, a sustained flight of institutional capital from enclosed mall formats toward open-air necessity-anchored parks, and the format's demonstrated compatibility with omnichannel retail operations including click-and-collect, drive-to convenience, and in-store return hubs. European retail park vacancy stood at 1.2% across CBRE's 155-asset European Shopping Centres Performance Index as of Q3 2024, the tightest of any tracked retail asset class, while US open-air retail centres recorded vacancy of 5.3% in Q2 2023 per JLL and CoStar data against 3.7 billion square feet of total open-air stock and only 10.9 million square feet under construction a supply-demand imbalance that has kept rental growth positive across primary markets. For instance, in the fiscal year ending March 2025, British Land, United Kingdom, acquired 15 retail parks across the UK for GBP 738 million at yields exceeding 7%, with retail parks reaching 99% occupancy across its 44-property portfolio and contributing approximately 48% of annual rental income, up from 27% in 2021, as the company redeployed GBP 3.7 billion of capital over four years from mature enclosed shopping centres into the open-air format. These are some of the key factors driving revenue growth of the market.

Savills data show European retail investment volumes reached EUR 35.5 billion in 2025, a 5% year-on-year increase and 4% above the five-year average, with retail parks representing 42% of total European retail investment volume the leading segment by capital allocation share. UK retail warehouse investment volumes grew 48% year-on-year to EUR 3.0 billion in 2024 per JLL research, with investor sentiment for UK retail warehouses at the highest level since the early 2000s as prime yields remain 125 basis points above their 2015 peak, indicating latent value that institutional buyers are actively compressing. Blackstone, United States, acquired Retail Opportunity Investments for USD 4 billion in 2024, one of the largest single transactions in North American retail real estate in the preceding five years, while Bain Capital Real Estate and 11North Partners specifically targeted necessity-based grocery-anchored open-air centres as their acquisition mandate. Green Street data confirmed that foot traffic at grocery-anchored open-air centres grew 12% in 2024 compared to 2019 levels, while foot traffic at enclosed malls remained 5% below pre-pandemic levels, validating the structural footfall advantage of the open-air park format across the North American market.

However, the global retail park market faces structural constraints that temper the pace of revenue growth across several markets. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, which the IMF confirmed in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy cost inflation that is compressing retailer operating margins and causing some tenants to defer new store rollouts into retail park locations across energy-exposed markets in Europe and the Middle East. LVMH and Kering reported declining revenues in H1 2025, and the broader softening of consumer discretionary spending in the face of persistent inflation limits the addressable tenant mix for retail parks seeking to upgrade beyond essential-goods anchors. The high construction and fit-out standards required for purpose-built retail parks including large-format car park infrastructure, specialist loading configurations, and climate control mean that new park development costs in Western Europe are 30 to 40% above those of conventional retail strip formats, suppressing speculative supply additions and limiting the pace at which new park capacity can be delivered to undersupplied markets including India and Southeast Asia. These factors substantially limit global retail park market growth over the forecast period.

The retail park format is experiencing the most straightforward institutional re-rating of any commercial real estate asset class in 2025. The investment case is not complicated: vacancy at 1.2% in Europe, yields of 7% or above in the UK market, a tenant base dominated by grocery chains and value retailers who generate necessity-driven footfall regardless of the economic cycle, and a building format that can be reconfigured for click-and-collect without a single planning permission. British Land's decision to deploy GBP 738 million into 15 retail parks in a single fiscal year is not a contrarian bet. It is the logical allocation when every data point occupancy, rental growth, foot traffic, investment volume is pointing in the same direction. The only genuine risk is entry pricing: the more institutional capital that migrates from malls, the faster prime retail park yields compress toward office and logistics equivalents, narrowing the return premium that attracted the first movers." Troview Intelligence Head of Global Retail Real Estate Research

SEGMENT INSIGHTS

By Geography

Europe and North America are expected to account for a significantly large revenue share in the global retail park market during the forecast period.

Based on geography, the global retail park market is segmented into Europe, North America, Asia Pacific, and Middle East and Africa. Europe dominates by investment volume and rental income density, with retail park vacancy at 1.2% across CBRE's European Shopping Centres Performance Index as of Q3 2024 and retail parks representing 42% of total European retail investment volume in 2025 per Savills data. The UK, Poland, and Spain have exceeded their pre-2019 investment volume peaks per CBRE Investment Management analysis, while Germany and France lag, creating a bifurcated European market where capital concentrates in higher-growth repriced markets. Asia Pacific is expected to register the fastest revenue CAGR over the forecast period, driven by India's underdeveloped large-format open-air retail infrastructure, where demand for necessity-anchored park formats is growing alongside urbanisation and rising mid-income household formation in Tier 1 and Tier 2 cities. North America's open-air retail park market is characterised by 3.7 billion square feet of existing stock per CoStar data, vacancy of 5.3%, and a construction pipeline limited to 10.9 million square feet, conditions sustaining positive rental growth across grocery-anchored park formats.

By Asset Format

Grocery-anchored open-air retail park format is expected to account for a significantly large revenue share in the global retail park market during the forecast period.

Based on asset format, the global retail park market is segmented into grocery-anchored open-air parks, power centres anchored by large-format category specialists, convenience and neighbourhood strip centres, and factory outlet and discount retail parks. Grocery-anchored formats dominate by income stability and investor demand, with foot traffic at grocery-anchored open-air centres growing 12% in 2024 compared to 2019 per Green Street data, outperforming enclosed mall formats which remained 5% below pre-pandemic levels. The power centre format, anchored by homewares, electronics, and sporting goods category retailers, registered the strongest leasing momentum in 2024 across Spain per Cushman and Wakefield data, recording 6.4% sales growth with electronics and furniture sub-sectors leading. Factory outlet and discount retail parks are expected to register a rapid revenue growth rate in the global market over the forecast period, driven by consumer value-seeking behaviour in inflationary environments across Europe and North America and the format's appeal to premium brands seeking to liquidate end-of-season inventory through off-price formats in high-footfall out-of-town locations.

By Anchor Tenant Type

Food and grocery anchor tenant category is expected to account for a significantly large revenue share in the global retail park market during the forecast period.

Based on anchor tenant type, the global retail park market is segmented into food and grocery anchors, home and DIY anchors, fashion and value apparel anchors, health and pharmacy anchors, and leisure and food service anchors. Food and grocery anchors dominate by footfall generation and income security, with necessity-based grocery tenants providing the consistent draw that insulates retail park occupancy from e-commerce displacement and macroeconomic slowdowns. British Land's retail park portfolio as at March 2025 shows grocery anchors including J Sainsbury, Tesco, and Asda Group collectively accounting for approximately 4.3% of total portfolio rent across parks sustaining 99% overall occupancy per the company's June 2025 investor presentation. Home and DIY anchors including Kingfisher and DFS are the fastest-growing anchor category in European retail parks, benefiting from the post-pandemic structural shift toward home improvement spending and the format's large-unit configurations that accommodate furniture and home goods retailers who cannot operate viably in high-street or enclosed mall environments.

REGIONAL ANALYSIS

EUROPE TIGHTEST

| European Retail Park Vacancy | UK Investment Volume Growth 2024 | European Retail Investment 2025 | Retail Parks Share of EU Volume |

| 1.2% (Q3 2024) | +48% YoY to EUR 3.0 billion | EUR 35.5 billion (+5% YoY) | 42% of total EU retail volume |

Europe is the global benchmark for retail park institutional investment, with vacancy of 1.2% across CBRE's tracked portfolio of 155 assets in 12 European countries as of Q3 2024, lower than the 5.8% overall retail index vacancy and lower than any other retail asset format tracked. CBRE's European Real Estate Market Outlook 2025 identified retail parks as the asset type most likely to see stronger rental growth than any other retail format, citing strongest occupier demand and lowest vacancy as the dual drivers of rent uplift. The UK leads European retail park transaction volume recovery, with investment growing 48% year-on-year to EUR 3.0 billion in 2024 per JLL data, driven by REIT strategic pipeline acquisitions from British Land and institutional mandates. British Land's April 2026 trading update confirmed retail park values up 3.3% for full-year 2026 and estimated rental value growth of 4.4% across the retail park portfolio, with 3.8 million square feet of leasing completed across the total portfolio at 7.2% ahead of ERV, affirming the rental growth thesis that institutional buyers underwrote at acquisition.

NORTH AMERICA RECORD LOW

| US Open-Air Retail Stock | US Vacancy (Q2 2023) | Blackstone ROIC Acquisition | 2025 Portfolio Transaction Est. |

| 3.7 billion sq ft (CoStar) | 5.3% tightest in decades | USD 4.0 billion (2024) | USD 10 billion+ per CBRE estimate |

North America's retail park and open-air shopping centre market is characterised by a record low availability rate with limited new supply scheduled for delivery in 2025, per CBRE's US Real Estate Market Outlook 2025, conditions sustaining upward pressure on asking rents across necessity-anchored formats. The open-air sector has outperformed enclosed malls consistently since 2020, with average time to secure tenants once space became available dropping to 8.5 months in 2024 the fastest pace in more than two decades per CoStar data confirming demand velocity that gives landlords negotiating leverage on rent reviews and lease renewals. Blackstone, United States, completed the USD 4 billion acquisition of Retail Opportunity Investments in 2024, one of the largest single transactions in North American retail real estate in the preceding five years, with a portfolio of grocery-anchored shopping centres in high-barrier-to-entry West Coast markets. Bain Capital Real Estate and 11North Partners specifically targeted necessity-based grocery-anchored open-air centres as their joint acquisition mandate, and CBRE forecasted that over USD 10 billion in open-air retail portfolios would change hands in 2025, with lending conditions improving as multiple banks competed to finance retail transactions.

ASIA PACIFIC

| India Organised Retail Supply | India Luxury Mall Count | APAC Primary Demand Driver | Regional CAGR Outlook to 2035 |

| Nascent strong mid-format supply gap | 3 nationwide (supply-constrained) | GCC employment, urbanisation | Highest among all regions |

Asia Pacific is the fastest-growing region in the global retail park market, driven by India's structural undersupply of organised large-format open-air retail, Australia's maturing suburban retail park investment market, and the rapid growth of necessity-anchored retail formats in Southeast Asian cities including Jakarta, Bangkok, and Ho Chi Minh City. India's retail real estate market operates with extreme demand-supply imbalance: the country has only three genuine luxury malls nationwide while the mid-format and value-oriented retail park segment which in European and North American markets serves the mass-market consumer cohort is similarly underdeveloped relative to the size of India's urban consuming class. The expansion of Global Capability Centres in Bengaluru, Hyderabad, Pune, and Chennai, which is expected to absorb 40 to 45 million square feet of net new office space in India in 2026, is generating a direct demand pipeline for mid-format retail parks serving employed technology sector households in suburban corridors adjacent to office clusters. In November 2025, Galeries Lafayette, France, opened its first India flagship in Mumbai's Fort area in partnership with Aditya Birla Fashion and Retail Limited, confirming that international retail brands will enter India when appropriately formatted retail real estate is created.