By Format · By District · By Operator · By Consumer Segment

City Spotlights: Tokyo · Osaka · Nagoya · Other Cities

Japan's inbound tourism exceeded 30 million annual visitors in 2025, the weak yen enhanced visitor purchasing power to make Japan an irresistibly cheap destination, tax-free retail spending surged 231.2% year-on-year in 2024 per Japan Tourism Agency data, Isetan Shinjuku achieved record sales of JPY 421 billion in 2024, the Japan Commercial Real Estate Price Index for retail assets rose 2.9% in Q3 2025 alone, and the depachika Japan's uniquely multi-sensory gourmet basement food hall format is described by industry analysts as the single most underrated experiential surface in Japanese retail.

MARKET SYNOPSIS

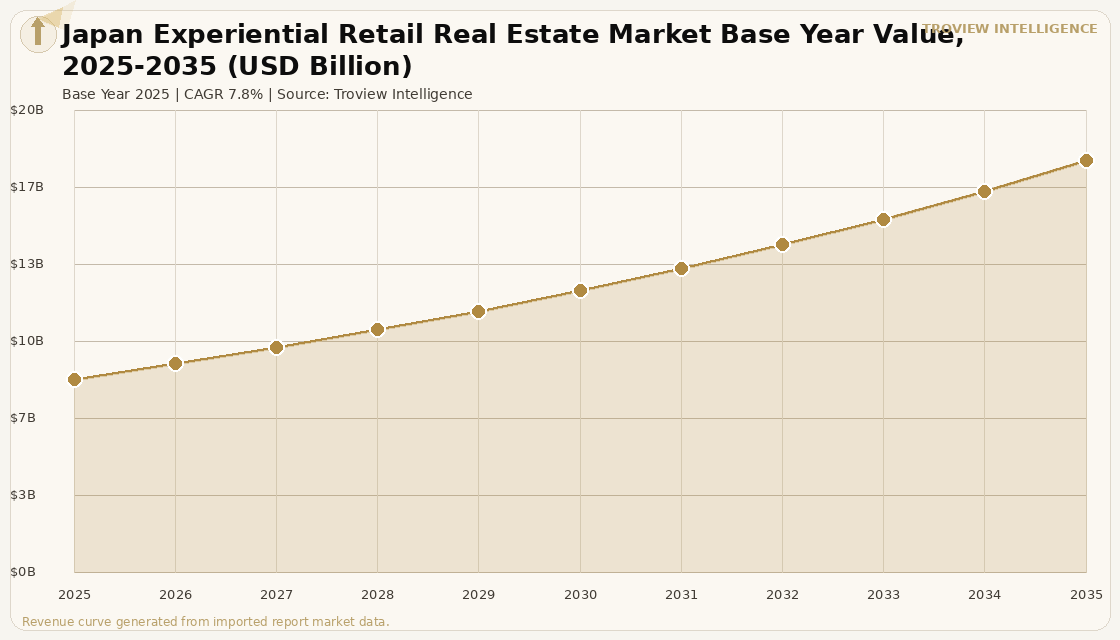

The Japan experiential retail real estate market size was USD 8.46 Billion in 2025 and is expected to register a revenue CAGR of 7.8% during the forecast period, reaching USD 17.99 Billion by 2035. Japan's experiential retail real estate market encompasses the rental and operational revenue generated by a uniquely advanced ecosystem of immersive digital art venues, department store depachika food halls, interactive luxury brand flagship stores, themed entertainment retail, and culturally embedded pop-up experience formats that collectively represent the world's most sophisticated physical retail environment. Japan's inbound tourism surpassed 30 million annual visitors in 2025 per Japan National Tourism Organization data, with the weak yen sustaining strong visitor purchasing power in commercial districts. The Japan Commercial Real Estate Price Index for retail assets rose 2.9% in Q3 2025, demonstrating relative resilience while office assets declined 5.4% in the same period, confirming that experiential and destination retail real estate is among the strongest-performing commercial asset classes in Japan's current cycle.

Japan's experiential retail real estate ecosystem is built on several uniquely Japanese formats that have no direct equivalent in other markets. The depachika, a gourmet food hall occupying the basement floors of department stores, functions as a multi-sensory installation that simultaneously sells premium food, generates extraordinary dwell time, and creates a cultural anchor that attracts repeat visits independent of other floors' fashion and luxury offer. Industry analysis identifies the depachika as the single most underrated experiential surface in Japanese retail, with Mitsukoshi, Takashimaya, and Isetan collectively operating some of the world's most elaborate and commercially successful basement food environments. teamLab's digital art venues teamLab Borderless at Azabudai Hills spanning approximately 9,300 square metres and teamLab Planets TOKYO in Toyosu, which expanded to 1.5 times its previous size in January 2025 attract a disproportionately international visitor mix compared to Tokyo's overall tourist profile, per teamLab official ticket purchase data covering January to December 2025. The 2025 Osaka World Expo targeted 42 to 44 million visitors with its conclusion accelerating the experiential retail investment pipeline across the Kansai region. For instance, in February 2025, Gaw Capital Partners and Patience Capital Group, Hong Kong and Japan, completed the acquisition of Tokyu Plaza Ginza in central Ginza, a 50,093 square metre retail facility with direct access to Ginza Station, citing Tokyo retail sales outperformance fuelled by inbound tourist spending and yen depreciation and citing the Tokyo Sky Corridor High Line opening in 2029 as a forward value catalyst, per Gaw Capital Partners press release of February 2025. These are some of the key factors driving revenue growth of the market.

However, the Japan experiential retail real estate market faces structural constraints. Tax-free retail spending, which surged 231.2% year-on-year in 2024, softened by 12.7% in 2025 and May 2025 saw a 41% decline across more than 80 stores per department store industry data, as inbound tourism patterns normalised and a modest yen strengthening reduced the purchasing power premium that had driven record foreign visitor spending. Japan's overall population declined to 120.65 million in 2024 at a rate of 0.75% annually per government data, with all prefectures outside Tokyo experiencing population decline, creating a structural demand ceiling for domestic consumer-driven experiential retail outside the capital. Japan's premium immersive experience formats carry significantly higher production costs than comparable activations in other Asian markets, running 20 to 30% above equivalent activations in competing markets due to labour costs, quality standards, and real estate costs, per industry cost analysis. These factors substantially limit Japan experiential retail real estate market growth over the forecast period.

Japan's experiential retail market is not copying the Western model. The depachika emerged in the 1960s as a multi-sensory food experience anchored in presentation, scarcity, seasonal produce, and gift-giving culture and it works because it understands consumer desire in a way that a food court in a Western mall never has. teamLab is the most globally recognised experiential retail format to have emerged in Asia in twenty years. Both of these things are Japanese inventions. When Western developers talk about adding experiential anchors to their malls, they are trying to import a quality of retail experience that Japan has been perfecting for six decades. The inbound tourism tailwind is real and the yen depreciation is a significant revenue multiplier. The structural question is whether experiential retail real estate can sustain revenue growth when the tourism cycle normalises and Japan must rely primarily on its declining domestic consumer base." Troview Intelligence Head of Japan Experiential Retail Research

SEGMENT INSIGHTS

By Format

Department store depachika and immersive digital art venues are expected to account for a significantly large revenue share in the Japan experiential retail real estate market during the forecast period.

Based on format, the Japan experiential retail real estate market is segmented into department store depachika food hall and gourmet basement formats, immersive digital art venues, interactive luxury flagship stores, themed entertainment retail and pop-up activation spaces, and mixed-use cultural-retail developments. Depachika dominate market revenue by square metre in Japan, with Isetan Shinjuku's basement food hall housing over 200 food stalls contributing to the store's record JPY 421 billion total sales in 2024 per Isetan Mitsukoshi Holdings investor data, and Mitsukoshi Nihombashi, Ginza Mitsukoshi, and Takashimaya operating depachika that attract destination visits independent of their upper-floor fashion and luxury departments. Immersive digital art venues are the fastest-growing format, with teamLab Borderless and teamLab Planets collectively drawing international visitors who make the experience a primary reason for visiting Japan, generating demand for the retail, dining, and hotel assets in their surrounding mixed-use developments.

By City

Tokyo is expected to account for a significantly large revenue share in the Japan experiential retail real estate market during the forecast period.

Based on city, the Japan experiential retail real estate market is segmented into Tokyo, Osaka, Nagoya, Kyoto, and other regional cities. Tokyo dominates, accounting for approximately 60% of Japan's experiential retail real estate market revenue and housing the world's highest concentration of internationally recognised experiential retail formats per square kilometre of commercial district. Osaka is the second-largest market, boosted by the 2025 World Expo that targeted 42 to 44 million visitors and generated sustained investment in Namba, Umeda, and the Expo site's post-event commercial development. Nagoya's Hankyu Umeda department store is identified as Japan's leading practitioner of theater-type experiential programming within department stores per industry analysis, deploying live performance and events as footfall drivers that integrate the store's retail floors with the experience programming.

By Consumer Segment

International tourists and affluent domestic consumers are expected to account for a significantly large revenue share in the Japan experiential retail real estate market during the forecast period.

Based on consumer segment, the Japan experiential retail real estate market is segmented into international tourists, affluent domestic high-net-worth consumers, youth and Gen Z trend consumers in Harajuku and Shibuya districts, and corporate and group experience purchasers. International tourists are the most commercially significant segment, generating disproportionately high per-visit spending due to yen depreciation purchasing power amplification, with tax-free retail spending surging 231.2% year-on-year in 2024 before normalising in 2025. The depachika and luxury flagship store format serves the affluent domestic consumer who visits regularly as part of social and gift-giving rituals deeply embedded in Japanese culture. teamLab venues attract a disproportionately international visitor base from Western markets including the United States, Australia, Canada, and the United Kingdom relative to those markets' share of total Tokyo tourism per teamLab ticket purchase data covering 2025.

Four Cities Shaping Japan's Experiential Retail Market

| teamLab Borderless | ~9,300 m², Azabudai Hills (Mori Building), Feb 2024 | Isetan Shinjuku 2024 Sales | Record ¥421 billion (Isetan Mitsukoshi Holdings) |

| Gaw Capital Tokyu Plaza Ginza | Feb 2025 acquisition, 50,093 m² | Tokyo World Best Cities 2026 | Ranked 4th globally (2026 World's Best Cities Report) |

Tokyo is the global capital of experiential retail real estate, combining the world's most commercially sophisticated depachika food hall ecosystem with immersive digital art venues that attract international visitors from every major economy and luxury flagship concept stores that have defined the global standard for experiential brand activation. The 2026 World's Best Cities Report ranked Tokyo 4th globally, reflecting rising global tourism evaluation and the city's concentration of world-class retail, culture, and food experiences in its commercial districts. The weak yen sustained exceptional visitor purchasing power in Ginza and Shibuya throughout 2025 per Japan Commercial Real Estate Price Index Q3 2025 analysis, and retail assets rose 2.9% in that quarter alone. Large urban commercial facilities including Azabudai Hills, GINZA SIX, and Shibuya Scramble Square saw strong leasing demand from domestic and international brands with tight vacancies per industry analysis.

| Expo 2025 Osaka | 42-44 million visitors targeted as event concluded | Key Districts | Dotonbori, Shinsaibashi, Umeda luxury corridor |

| Shinsaibashi | Inbound tourism retail sales recovery per market analysis | Hankyu Umeda | Leading Japanese practitioner of theater-type experiential programming |

Osaka is Japan's second experiential retail real estate market, catalysed by the 2025 World Expo that brought 42 to 44 million visitors to the Kansai region and sustained investment in the Shinsaibashi, Namba, and Umeda luxury retail and entertainment corridors. The weak yen supported retail sales across Shinsaibashi's luxury corridor throughout 2025, with Osaka named as a city where yen depreciation supported retail sales in major commercial districts alongside Tokyo per Japan real estate market analysis. Hankyu Umeda department store is recognised as Japan's leading practitioner of theater-type experiential programming per industry analysis, deploying live performance events and cultural programming that integrate the store's retail floors with audience-generating entertainment, setting a benchmark that other Japanese department stores are attempting to replicate. The post-Expo development pipeline, including commercial facilities on and adjacent to the Expo site, is expected to add to Osaka's experiential retail stock through the late 2020s.

| Nagoya Distinction | First Japanese city to develop the depachika (Matsuzakaya, 1936) | Hankyu Men's | Entire building dedicated to menswear experiential retail |

| Craft Tourism | Tea ceremony, ceramics, craftsmanship experiences integrated into retail | Market Role | Automobile industry wealth supporting premium experiential retail demand |

Nagoya holds a unique position in Japan's experiential retail history as the city where the first department store basement food market was developed at Matsuzakaya's flagship store in 1936, making it the origin point of the depachika concept that has since defined Japanese retail's experiential identity. The city's retail market benefits from the wealth concentration of the Toyota Motor Corporation and the broader central Aichi automotive manufacturing ecosystem, which sustains high-income consumer demand for premium experiential retail. Hankyu Men's Tokyo, a dedicated menswear building in Nagoya, represents an extreme version of the specialist experiential flagship concept where the depth of product curation and the service experience creates a destination visit distinct from general department store shopping. Nagoya's ceramics and craft tourism industry, centred on the Seto ware and Tokoname ware traditions of the broader Aichi region, has generated experiential retail formats integrating artisanal workshops into retail environments.

| Kyoto | Cultural tourism capital, seasonally intense experiential retail demand | Fukuoka | Fastest-growing Japanese city, Hakata retail district |

| Kyoto Luxury | International luxury brands establishing culturally localised flagship formats | Market Role | Heritage tourism sustaining premium experiential retail demand |

Kyoto and Fukuoka represent the experiential retail real estate markets that benefit from different growth dynamics: Kyoto from the intersection of Japan's cultural heritage tourism with international luxury brand activation, and Fukuoka from its status as one of Japan's few genuinely growing cities with a young, consumption-oriented demographic. Kyoto's seasonal visitor calendar cherry blossom in April, autumn foliage in November, Gion Matsuri festival in July creates intense demand concentrations that sustain short-term pop-up and seasonal experiential retail formats at premium rents, with international luxury brands establishing Kyoto-specific store formats that integrate Japanese craft references into their global brand visual language. Fukuoka's Hakata district is evolving as a testing ground for experiential retail formats targeting the city's young professional demographic, with the city's geographic position as the closest major Japanese city to South Korea and China sustaining inbound tourism that amplifies domestic consumer retail spending.