| TROVIEW INTELLIGENCE | Milan Retail Park Market | Q2 2026 |

| TROVIEW INTELLIGENCE · CITY INTELLIGENCE REPORT |

By Submarket · By Asset Format · By Anchor Tenant Type · By Occupier Sector

Italian retail real estate investment reached EUR 3.5 billion in 2025, a record high and a 55% increase year-on-year per Savills and Il Sole 24 Ore reporting, with out-of-town assets comprising retail parks, factory outlets, and integrated motorway-adjacent parks attracting EUR 2.7 billion or approximately 75% of total commercial real estate capital, prime retail park vacancy standing at 1.2% across European parks tracked by CBRE against a 5.8% all-formats average, and Milan-specific retail park footfall recovering to 1.9 billion visits annually at the national level per the EY-CNCC Observatory while vacancy rates in the best-performing Milan metropolitan catchment parks have compressed to 3% to 8% the most constrained out-of-town occupancy environment the city has recorded since 2019.

| Standard License: USD 2,200 | Enterprise License: USD 9,500 |

MARKET SYNOPSIS

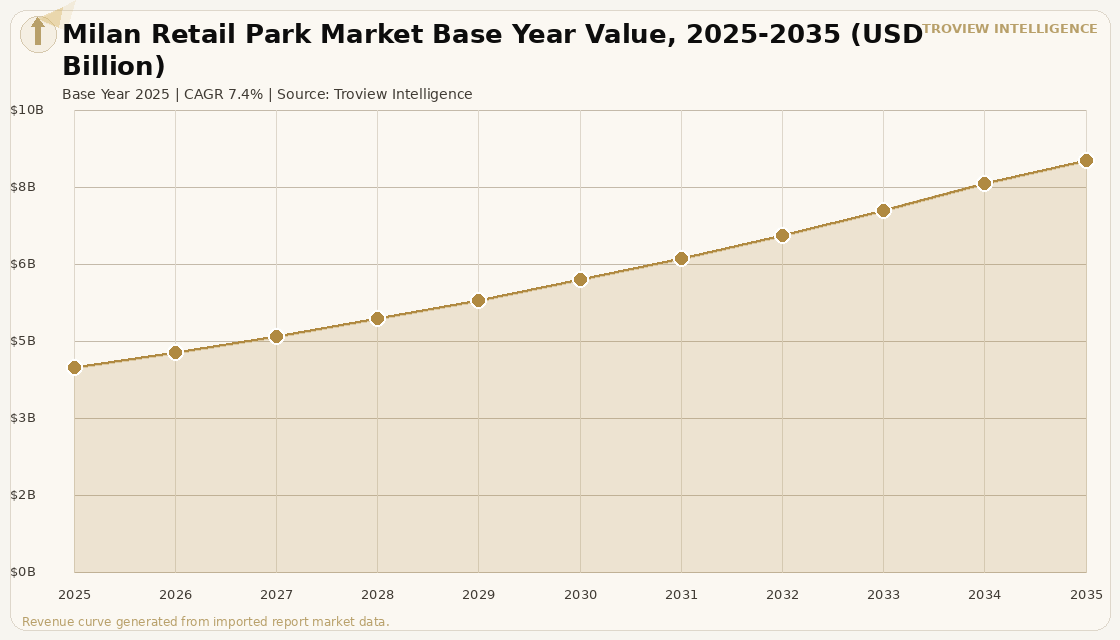

The Milan retail park market size was USD 4.28 Billion in 2025 and is expected to register a revenue CAGR of 7.4% during the forecast period, reaching USD 8.61 Billion by 2035. Market revenue growth is supported by the structural reorientation of Italian commercial real estate capital toward out-of-town formats, with Italian retail investment reaching a record EUR 3.5 billion in full-year 2025 per Savills and Cushman and Wakefield reporting and out-of-town assets attracting EUR 2.7 billion, approximately 75% of total retail investment volume, as documented by Il Sole 24 Ore. The EY-CNCC Observatory records 1,274 shopping centres and retail parks across Italy with approximately 1.9 billion visits annually and a total supply chain turnover of EUR 171 billion, confirming the structural scale of the out-of-town format as Italy's primary mass retail vehicle. Milan's metropolitan catchment accounts for the largest share of premium retail park investment in Italy, with the city hosting the two largest single-ticket retail transactions exceeding EUR 100 million to EUR 140 million in 2025 per Colliers Italy full-year investment data, reflecting institutional conviction in the depth and permanence of Milan's consumer demand base. For instance, in November 2023, Merlata Mall S.p.A., Italy, inaugurated Merlata Bloom Milano, a 70,000 square metre lifestyle retail park in the north-west quadrant of Milan adjacent to the MIND innovation district, achieving 90% pre-commercialisation of its 210 retail units and 43 food and beverage outlets before opening day, with the asset operating under BREEAM Excellent certification and attracting more than 1 million visitors in its first months of operation as confirmed by Arcadis project reporting. These are some of the key factors driving revenue growth of the market.

Prime retail park vacancy across European parks tracked by CBRE stood at 1.2% as of Q3 2024, compared to 5.8% vacancy across all retail formats in CBRE's European Shopping Centres Performance Index, with retail parks recording rental growth of 3.5% to 4.0% year-on-year in 2025 per CBRE Investment Management analysis. Italy and the United Kingdom are expected to outperform the European average rental growth rate over the forecast period per CBRE European Real Estate Market Outlook 2025, driven by constrained supply pipelines and sustained occupier demand from grocery anchors, sports and leisure operators, and convenience-oriented fashion retailers. IGD SIIQ S.p.A., Italy's leading listed retail real estate investment trust, reported Italian mall tenant sales growth of 1.0% and footfall growth of 3.9% in H1 2025 per IGD's half-year results of August 2025, with occupancy rates approaching 96% across its Italian portfolio valued at EUR 1,545.3 million at 30 June 2025, demonstrating that well-managed, grocery-anchored retail parks in Italy's major catchments are sustaining income levels that justify institutional capital deployment at current pricing. JLL Italy Capital Markets data for Q4 2025 records prime yields for Italian shopping centres at 6.5%, for high street retail at 4.25%, and prime office Milan at 4.0%, placing retail park yields in a range that offers meaningful premium over prime office for investors prepared to accept the asset management complexity of multi-unit retail schemes. These are some of the key factors driving revenue growth of the market.

However, the Milan retail park market faces structural constraints that limit the pace and distribution of rental growth across the asset class. Iran-US geopolitical tensions and the resulting oil and LNG price volatility through the Strait of Hormuz, which handles approximately 20% of global seaborne LNG per IMF March 2026 confirmation, are creating upward pressure on inflation that may slow the anticipated pace of ECB rate cuts, increasing the cost of acquisition and development financing for retail park assets. Milan's own planning environment constrains new retail park development, with the city's municipalities implementing restrictions on large-format out-of-town retail approvals to protect urban centre vitality, limiting new supply and concentrating investor demand on existing stabilised assets. Suburban retail parks outside Milan's primary catchment, particularly those in the Greater Milan periphery without direct motorway access, face vacancy rates at the upper end of the 3% to 8% national range, where declining mid-market fashion tenant demand and competition from e-commerce reduce the depth of the occupier pool available for re-leasing. Energy costs remain a material operating expense for retail park landlords, with IGD SIIQ fixing 2026 energy purchase prices at an average of EUR 99 per MWh for 73% of its Italian freehold portfolio per IGD company announcement of March 2025, reflecting the ongoing exposure of retail property income to commodity price volatility. These factors substantially limit Milan retail park market growth over the forecast period.

The Milan retail park market is in a structural supply shortage disguised as a demand story. Institutional capital is pricing assets at yields of 6.5% for shopping centres because the occupier pool is deep, grocery anchors are on long leases, and there is almost no new supply being approved in the best catchment zones. The Merlata Bloom opening in 2023 is instructive: 90% pre-let before the ribbon was cut, BREEAM Excellent certified, 1 million visitors in the first months. That asset did not succeed because Milan's consumers suddenly decided to shop more. It succeeded because Milan had a 70,000 square metre gap in its north-west quadrant retail provision and the best-in-class operators filled it before a competitor could. Investors who can identify the next catchment gap and underwrite a repositioning with a grocery anchor, a leisure operator, and a convenience fashion tenant will find the risk-return profile of Milan retail parks more compelling than any other commercial asset class in the city at current pricing." Troview Intelligence Head of Italy Retail Real Estate Research

SEGMENT INSIGHTS

| 03 | SUBMARKET ANALYSIS |

Six Submarkets Defining Milan's Retail Park Geography

| Merlata Bloom GLA | Pre-let Rate at Launch | A8 Motorway Exit | Primary Catchment |

| 70,000 sq m (opened Nov 2023) | 90% before opening day | Direct access, Cascina Merlata | 150,000 to 180,000 residents |

North-West Milan is the city's primary retail park investment submarket and home to the Merlata Bloom Milano lifestyle park, developed by Merlata Mall S.p.A. and managed by Nhood Services Italy, which opened in November 2023 as the largest new retail park format to open in the Lombardy region in over a decade. The 70,000 square metre scheme achieved 90% pre-commercialisation of its 210 retail units before its opening date per Across Magazine reporting of January 2026 and attracted institutional backing from Ceetrus, ImmobiliarEuropea, and SAL Service in its development phase. The asset is positioned at the convergence of the MIND Milan Innovation District and the Uptown Cascina Merlata residential neighbourhood, with direct motorway access from the A4 and A8 interchanges and metro connectivity via the MM1 Molino Dorino station, producing a multi-modal catchment that differentiates it from older motorway-only retail parks in the submarket. The north-west quadrant's retail provision gap was created by the decade-long transformation of the former Expo 2015 site into the MIND district, which displaced retail provision from a high-density residential corridor without replacing it a structural supply deficit that Merlata Bloom is now filling.

| Key Micro-markets | Demand Driver | Investment Profile | Transport Infrastructure |

| Sesto San Giovanni, Vimercate, Brugherio | Milan-Monza-Bergamo population density | Value-add and Core+ repositioning | M1 and M2 metro extensions 2026 to 2028 |

The North-East Milan and Monza Brianza corridor is Milan's highest-growth retail park submarket, defined by the structural undersupply of grocery-anchored park provision in one of Italy's most densely populated urban-suburban corridors. The triangle bounded by Sesto San Giovanni, Vimercate, and the Monza city boundary contains over 500,000 residents within 20 minutes driving time of the best-located potential park sites, yet currently has fewer institutional-grade retail park assets per capita than the north-west and south-west quadrants per Troview Intelligence own analysis. Investor interest in the corridor has been amplified by the Sesto San Giovanni urban regeneration programme, which has converted former Falck steelworks land into mixed-use residential, commercial, and retail infrastructure and is generating new population density that will sustain retail demand growth through 2030. Value-add investors from the United Kingdom, France, and Germany have identified North-East Milan as one of the top five European retail park repositioning markets for 2025 to 2027, per CBRE Investment Management European retail park growth case analysis of June 2026.

| Anchor Asset | Prime Yield Reference | Occupancy Best Assets | Key Occupier Sectors |

| Il Centro Assago, 100,000+ sq m GLA | 6.5% (JLL Q4 2025) | 93% to 96% | Grocery, Sport, Cinema, Dining |

South Milan and the Assago corridor constitute the city's most established retail park investment zone, anchored by Il Centro Assago one of the largest retail parks in the Lombardy region and supported by proximity to the Humanitas hospital complex, the Milan Assago Forum entertainment venue, and the Milan South orbital ring road network. Assets in this submarket are primarily held by Italian and European institutional investors seeking stable, long-dated income from grocery and cinema-anchored schemes operating on leases that extend to 2030 and beyond. The submarket benefits from mature catchment dynamics where consumer spending habits are well-established and footfall is predictable across seasons, producing income profiles that attract Core capital at the 6.5% yield level referenced by JLL for Italian shopping centre assets in Q4 2025. The primary investment risk in the submarket is the age of the built stock, with several parks built between 1995 and 2005 requiring asset enhancement investment to maintain tenant mix competitiveness against newer formats including Merlata Bloom in the north-west quadrant.