| TROVIEW INTELLIGENCE | Edge Data Centre Market | Q2 2026 |

By Geography · By Component · By Facility Size · By End-Use Industry

Global edge data centre installed capacity reached approximately 10,000 facilities in 2024 and is projected to exceed 18,000 by 2033, as Equinix committed GBP 3.9 billion to a 250 MW Hertfordshire campus in October 2025, Telehouse International broke ground on a GBP 275 million West Two facility in London's Docklands adding 33 MW of AI-ready capacity, and 5G Americas confirmed more than 182 million 5G connections across the United States and Canada at end-2024, creating the distributed latency-sensitive workload base that makes edge data centre investment structurally necessary.

MARKET SYNOPSIS

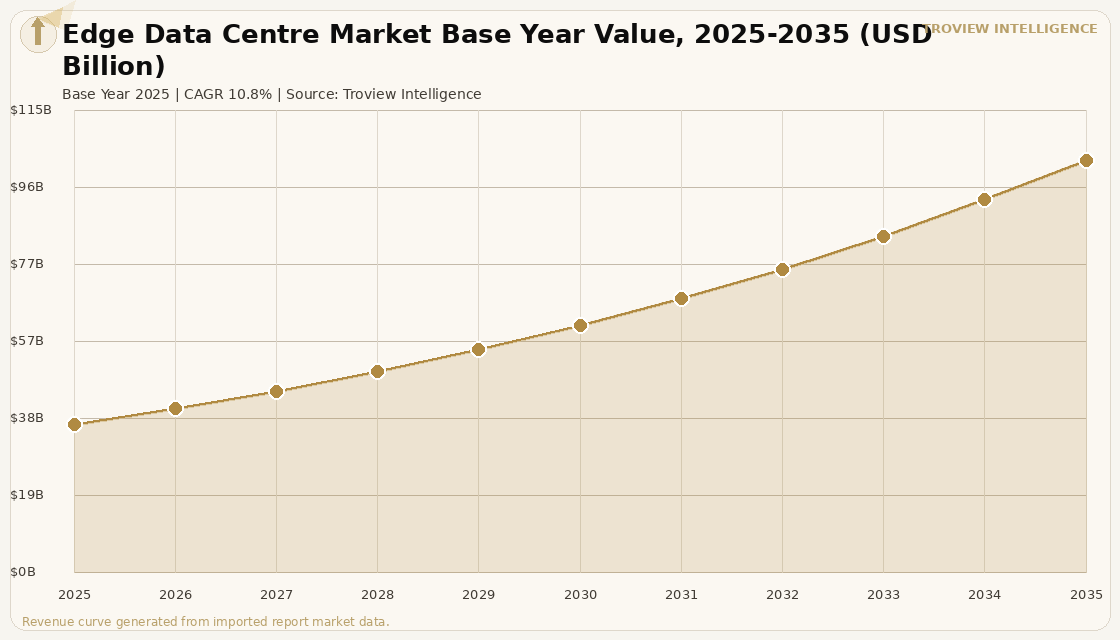

The global edge data centre market size was USD 36.82 Billion in 2025 and is expected to register a revenue CAGR of 10.8% during the forecast period, reaching USD 102.47 Billion by 2035. Market revenue growth is supported by the accelerating commercial rollout of 5G networks, the proliferation of Internet of Things devices generating latency-sensitive workloads that cannot be efficiently processed in centralised hyperscale facilities, and the rising adoption of artificial intelligence inference at the network edge across manufacturing, healthcare, autonomous mobility, and financial services verticals. 5G Americas confirmed more than 182 million 5G connections across the United States and Canada at end-2024, reflecting nearly 20% year-on-year growth, and the GSMA projects global 5G connections to reach 5.9 billion by 2030, each connection generating real-time data streams that require compute resources positioned within single-digit millisecond latency of the end device. For instance, in October 2025, Equinix, United States, announced a GBP 3.9 billion investment to acquire and develop the DC01UK Hertfordshire campus, a 250 megawatt facility across 85 acres that will serve as the largest single edge and co-location campus in the United Kingdom, with construction commencing in 2027 and initial operations targeting 2029 to 2030, demonstrating the scale at which institutional capital is committing to distributed edge infrastructure adjacent to dense urban demand centres. These are some of the key factors driving revenue growth of the market.

North America accounted for approximately 35.5% of global edge data centre revenue in 2025, anchored by the United States market where edge facilities serve hyperscaler cloud-on-ramp demand from financial institutions, media streaming operators, and enterprise private cloud deployments requiring sub-10 millisecond round-trip latency to end users. Europe's edge data centre market is concentrated in the United Kingdom, Germany, France, and the Netherlands, with the UK commanding the largest share of European edge investment following the government's classification of data centres as Critical National Infrastructure in 2024 and the January 2025 AI Opportunities Action Plan that provided planning certainty for large-format facilities. Asia Pacific is the fastest-growing region, with India projected to register the highest country-level CAGR through 2033 per verified industry data, driven by 5G network densification, rapid urbanisation, and the expansion of Global Capability Centre office infrastructure requiring adjacent compute resources. The global number of edge data centre facilities is projected to grow from approximately 10,000 in 2024 to over 18,000 by 2033, with average facility size expanding from USD 2.5 million to approximately USD 4 million in capital value as rack density requirements driven by AI inference workloads push operators toward higher-specification builds.

However, the global edge data centre market faces structural constraints that temper the pace of deployment across several markets. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy cost inflation that raises operational expenditure for edge data centres, which consume electricity at power usage effectiveness ratios of 1.15 to 1.6 depending on cooling technology, creating margin pressure for operators in energy-exposed markets including Europe and the Middle East. Grid connection constraints in established markets represent the most significant near-term bottleneck: National Grid ESO paused new 132 kV offers in parts of Greater London and surrounding counties, creating seven to ten year delays for developers who cannot fund costly upstream reinforcement, with Equinix committing to a bespoke 400 kV feed for its Hertfordshire campus at a cost premium adding 18 months to the pre-construction timeline. The construction and operational cost requirements for AI-ready high-density edge facilities liquid cooling infrastructure, specialist power management, and seismic-grade structural specifications mean that capital costs for next-generation edge builds in Western Europe are 40 to 60% above those of previous-generation air-cooled facilities. These factors substantially limit global edge data centre market growth over the forecast period.

The edge data centre investment cycle is not primarily driven by the number of 5G connections or IoT devices, although both matter. It is driven by the emergence of AI inference as a workload that cannot tolerate hyperscale round-trip latencies. When a financial exchange needs a risk model to run in under 2 milliseconds, or an autonomous vehicle needs a sensor fusion result in under 5 milliseconds, the physics of light-speed propagation over fibre makes the centralised cloud economically and technically unusable for that workload. Edge data centres are the answer to that physics constraint. Equinix's GBP 3.9 billion Hertfordshire commitment and Telehouse's GBP 275 million Docklands expansion are not speculative bets on future demand. They are infrastructure responses to workload characteristics that operators can already measure in their existing customer pipelines." Troview Intelligence Head of Global Data Centre Research

SEGMENT INSIGHTS

By Component

Solutions component is expected to account for a significantly large revenue share in the global edge data centre market during the forecast period.

Based on component, the global edge data centre market is segmented into solutions and services. The solutions segment, comprising IT infrastructure hardware including servers, storage, networking equipment, power distribution units, and cooling systems, held approximately 87% of total revenue in 2025 per verified industry data, as capital expenditure on physical infrastructure dominates the edge build-out cycle ahead of the managed services layer that follows facility commissioning. Dell Technologies, United States, introduced its software-driven disaggregated infrastructure initiative in May 2025, encompassing PowerProtect All-Flash storage, PowerStore ransomware detection, and the Dell Automation Platform with NativeEdge to automate and secure private cloud and edge operations, illustrating the transition of solutions providers from hardware vendors to full-stack edge infrastructure platforms. The services segment is expected to register the fastest revenue CAGR during the forecast period, driven by the increasing complexity of managing distributed edge estates across multiple geographies and the preference of enterprise customers for managed service contracts that transfer operational responsibility to specialist operators.

By Facility Size

Large facility segment is expected to account for a significantly large revenue share in the global edge data centre market during the forecast period.

Based on facility size, the global edge data centre market is segmented into micro facilities below 10 kW, small facilities from 10 to 19 kW, medium facilities from 20 to 49 kW, and large facilities above 50 kW. The large facility segment dominated revenue in 2025, reflecting the structural advantage of scale in capital efficiency, power purchase agreement negotiating leverage, and cooling economies of scale. Hyperscale and large-format edge campuses exceeding 50 megawatts achieved power usage effectiveness below 1.15 through economies of scale in liquid and immersion cooling deployment, compared with 1.4 to 1.6 for smaller builds. Micro facilities below 10 kW are expected to register a declining revenue share over the forecast period as compute consolidation into medium and large format facilities advances and edge telecom street furniture deployments shift toward operator-grade micro data centre enclosures managed by telecom infrastructure operators rather than sold as market revenue-generating assets.

By End-Use Industry

IT and telecommunications end-use industry is expected to account for a significantly large revenue share in the global edge data centre market during the forecast period.

Based on end-use industry, the global edge data centre market is segmented into IT and telecommunications, banking financial services and insurance, healthcare, manufacturing, government and defence, retail and e-commerce, and energy and utilities. The IT and telecom segment dominated total revenue in 2025, as telecommunications operators deploying 5G network slicing and mobile edge compute infrastructure represent the largest single category of edge data centre investment globally, with BT-AWS Wavelength Zones in Manchester and similar operator-cloud partnerships in all major markets embedding edge compute directly into 5G radio access networks. The manufacturing end-use segment is expected to register the fastest revenue CAGR during the forecast period, driven by Industry 4.0 adoption across automotive, aerospace, and precision manufacturing facilities that require real-time machine vision, predictive maintenance, and robotic control plane latencies below 5 milliseconds that cannot be served by centralised cloud infrastructure.

REGIONAL ANALYSIS

NORTH AMERICA LARGEST

| NA Revenue Share 2025 | 5G Connections US+Canada end-2024 | US Edge Market 2025 | NA Market Outlook |

| 35.5% of global revenue | 182 million (5G Americas) | ~USD 13.1 Billion est. | Fastest infrastructure capex cycle |

North America is the largest edge data centre region, accounting for approximately 35.5% of global revenue in 2025, underpinned by the United States' mature co-location market, the rapid commercial rollout of 5G networks that 5G Americas confirmed reached 182 million connections across the US and Canada at end-2024, and the enterprise demand from financial services, media streaming, and healthcare operators for sub-10 millisecond compute latency at scale. Blackstone Real Estate and other North American institutional investors have directed capital into edge-adjacent co-location and hyperscale facilities, with CBRE confirming that over USD 10 billion in open-air and data centre related real estate portfolios was anticipated to change hands in 2025. Bain Capital Real Estate and specialised data centre REITs have expanded acquisition mandates to include carrier-neutral edge facilities in secondary metropolitan markets including Dallas, Atlanta, and Chicago where 5G densification is creating latency-sensitive workload pipelines for industrial automation and financial high-frequency trading applications.

EUROPE

| UK Edge Market 2025 | Equinix Hertfordshire Investment | UK Electricity Cost vs US | London Installed Capacity 2025 |

| USD 628.69 Million | GBP 3.9 billion (250 MW campus) | 42c/kWh vs 16c/kWh | 2.45 GW installed (verified industry data) |

Europe's edge data centre market is led by the United Kingdom, Germany, and the Netherlands, with the UK established as the second-largest data centre market in EMEA and the largest edge investment destination in Europe following the government's 2024 classification of data centres as Critical National Infrastructure. Equinix, United States, announced in October 2025 a GBP 3.9 billion investment in the 85-acre Hertfordshire South Mimms campus, a 250 megawatt facility representing one of the largest single edge and co-location commitments in European history per The Register reporting of October 2025. Grid connection constraints represent the primary market headwind, with National Grid ESO having paused new 132 kV connection offers in parts of Greater London and surrounding counties, creating delays of seven to ten years for developers without the capital to fund upstream reinforcement, though the UK government's National Grid GBP 9 billion reinforcement framework awarded to Laing O'Rourke, AECOM, and Balfour Beatty in September 2025 is designed to unlock 15 gigawatts of South-East capacity over the medium term.

ASIA PACIFIC

| APAC Revenue Share 2025 | Fastest Country CAGR | Singapore Edge Driver | India GCC-Edge Demand Pipeline |

| ~29.9% of global revenue | India (highest through 2033) | Financial services, safe-haven capital | 40-45M sqft GCC office expansion 2026 |

Asia Pacific is the fastest-growing edge data centre region, with India projected to register the highest country-level CAGR through 2033 per verified market data, driven by the government's BharatNet broadband infrastructure programme, the rollout of 5G networks by Reliance Jio and Airtel, and the expansion of Global Capability Centres in Bengaluru, Hyderabad, Pune, and Chennai that is expected to absorb 40 to 45 million square feet of net new office space in India in 2026, creating a direct demand pipeline for edge compute resources serving employed technology sector workforces. Singapore's edge data centre market benefits from its position as the primary interconnection hub for Southeast Asia, with GIC Pte. Ltd. and Temasek Holdings both committed to data centre infrastructure investment through platform strategies targeting ASEAN connectivity nodes. Japan's market continues to attract investment from NTT, which confirmed its May 2025 land purchase for LON2 as part of a continued multi-gigawatt global expansion plan positioning Tokyo and London as its primary EMEA and Asia Pacific edge hubs.