By Experience Type · By Geography · By Format · By Operator

The USD 132 billion experiential retail market is projected to more than quadruple by 2035 per ICSC analysis as brands and landlords invest in immersive experiences, experiential REITs recorded 8% AFFO growth and 99% occupancy in 2025, 70% of Gen Z respondents would sacrifice retail purchases to fund experiential outings per survey data, and Louis Vuitton CEO Pietro Beccari told Vogue Italia that retailtainment represents the future of retail as location-based entertainment is projected to reach USD 73.5 billion by 2035 and Disney committed USD 60 billion over a decade to its experiential pipeline.

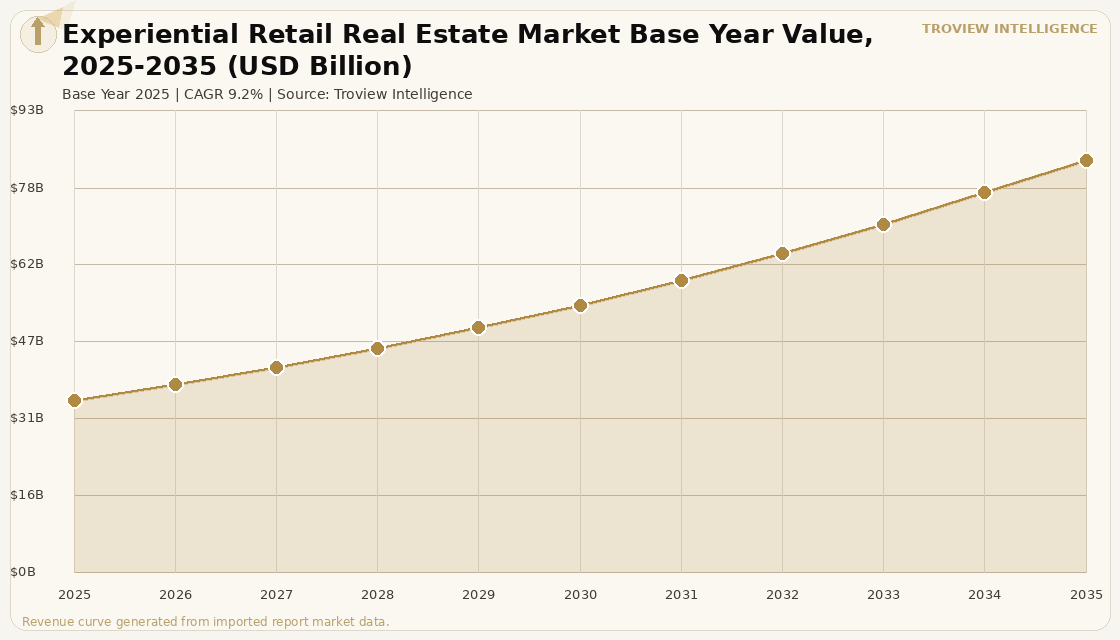

MARKET SYNOPSIS

The global experiential retail real estate market size was USD 34.86 Billion in 2025 and is expected to register a revenue CAGR of 9.2% during the forecast period, reaching USD 83.38 Billion by 2035. Experiential retail real estate encompasses the physical spaces purpose-built or repositioned to deliver experiences that cannot be replicated online including immersive digital art venues, curated food halls, interactive brand flagship stores, entertainment zones within malls, fitness and wellness destinations, and live performance integrated retail formats. The USD 132 billion experiential retail market is projected to more than quadruple by 2035 as brands and landlords invest in immersive experiences per ICSC analysis, with experiential real estate investment trusts recording 8% AFFO growth and 99% occupancy in 2025, confirming that purpose-built experience venues have achieved near-year-round utilisation that traditional retail categories could not sustain. The consumer shift is structural: survey data shows 70% of Gen Z respondents would sacrifice retail purchases to fund experiential outings, per industry survey analysis, and NAIOP identified experience-driven spaces as a defining retail trend of 2025 among its commercial real estate members.

The global experiential retail real estate market is being shaped by the simultaneous action of global luxury brands investing in flagship experiential stores and institutional developers repositioning former anchor department store space as entertainment and experience hubs. Louis Vuitton CEO Pietro Beccari told Vogue Italia that retailtainment represents the future of retail, describing the Paris Champs-Élysées concept under development as something never seen before, blending products, brands, experiences, and culture. Global location-based entertainment is projected to reach USD 73.5 billion by 2035 with a CAGR of 28.82% from 2026 to 2035 per Valo Motion analysis, as the attractions sector achieves commercial scale at retail locations. PREIT, the US mall REIT, reported significant traffic and dwell time gains from retailtainment investments per ICSC reporting, and Walmart hosted a 12-stop Nitro Circus and Dickies tour featuring BMX stunts and live music to drive store traffic. For instance, in May 2025, Emaar Properties, UAE, unveiled The District at Dubai Mall, a 279-outlet AED 1.5 billion expansion that introduced immersive dining experiences and culturally themed precincts where Emirati cuisine concepts debut alongside specialty coffee and experiential F&B, per Emaar Properties press release of May 2025, confirming that even the world's most visited retail destination is investing in experiential formats to sustain and grow its appeal. These are some of the key factors driving revenue growth of the market.

However, the global experiential retail real estate market faces structural constraints. Partners' Steve Triolet described retailtainment as being in its honeymoon phase at ICSC, noting that some concepts risk oversaturation as every developer attempts to incorporate entertainment anchors regardless of market viability, per ICSC reporting of August 2025. The capital expenditure required to build or convert retail space for immersive experiences is substantially higher than for standard retail, with major named-artist atrium installations running from USD 500,000 to over USD 2 million and full floor renovations with permanent experiential layers above USD 2 million per project per industry cost analysis, extending developer payback periods and increasing execution risk. Not all retailtainment concepts endure through competitive market exposure, with experts at ICSC noting that best-in-class formats will prevail while others fade, suggesting a shakeout is likely in the early period before the market matures. These factors substantially limit global experiential retail real estate market growth over the forecast period.

Experiential retail real estate is the asset class that emerged from the answer to a question every mall landlord asked between 2015 and 2020: what do you put in the anchor box after the department store leaves? The first answer was fitness studios and restaurants. The current answer is immersive digital art, active indoor entertainment, and branded flagship experience centres. The structural advantage of the experiential model over traditional retail is that the dwell time is incompatible with e-commerce. You cannot buy three hours at teamLab Borderless online and receive it delivered to your door. That irreplaceability is what institutional capital is buying when it acquires experience-anchored retail real estate at sub-6% cap rates." Troview Intelligence Head of Global Experiential Retail Real Estate Research

SEGMENT INSIGHTS

By Experience Type

Immersive digital art and entertainment venues are expected to account for a significantly large revenue share in the global experiential retail real estate market during the forecast period.

Based on experience type, the global experiential retail real estate market is segmented into immersive digital art and entertainment venues, curated food halls and dining precincts, fitness and wellness experience destinations, interactive brand flagship stores, live performance and cultural programming retail, and active indoor play and family entertainment. Immersive digital art and entertainment venues dominate institutional investment value, with the global location-based entertainment market projected to reach USD 73.5 billion by 2035 per Valo Motion industry analysis and Sandbox VR's pipeline of 25 new locations across Asia Pacific and Europe. Curated food halls are the fastest-growing segment by unit count globally, as the Japanese depachika format a multi-sensory gourmet food hall on the basement floors of department stores has been adopted and adapted by Western developers who are repositioning former anchor department store basement space into curated artisanal food markets. Active indoor entertainment including climbing walls, trampolining, and mixed-reality game zones is explicitly identified as the new anchor format by retail centre operators, with Valo Motion noting that families prefer active options where kids move and play together rather than sitting in cinemas.

By Geography

Asia Pacific is expected to account for a significantly large and fastest-growing revenue share in the global experiential retail real estate market during the forecast period.

Based on geography, the global experiential retail real estate market is segmented into Asia Pacific, North America, Europe, and Middle East. Asia Pacific dominates the market's most advanced experiential retail real estate formats, with Japan's teamLab Borderless and teamLab Planets defining the global benchmark for immersive digital art venues in retail contexts, South Korea's K-pop brand flagship stores deploying interactive AR and gamified retail experience in Myeongdong and Hongdae, and China's Alibaba and JD.com testing phygital store formats. North America's market is driven by the repositioning of former department store space and the addition of entertainment anchors to Class A malls, with EPR Properties as the largest experiential real estate REIT in the US market. Europe's market features Louis Vuitton's Champs-Élysées retailtainment concept, UK food hall investments in former market buildings, and German mixed-use entertainment retail developments.

By Format

Anchor-scale immersive experience venues within mall and mixed-use developments are expected to account for a significantly large revenue share in the global experiential retail real estate market during the forecast period.

Based on format, the global experiential retail real estate market is segmented into anchor-scale standalone immersive venues, experiential flagship brand stores above 10,000 square feet, curated food and dining precincts, fitness and wellness destination facilities, pop-up and temporary activation spaces, and adaptive reuse entertainment venues. Anchor-scale immersive venues dominate institutional revenue per square foot, with teamLab Borderless at Azabudai Hills spanning approximately 9,300 square metres and serving as the primary driver of footfall to Mori Building's mixed-use development. Experiential flagship brand stores are the fastest-growing format by number of openings, as Apple, Lululemon, Nike, and global luxury houses develop stores that function as brand experience centres hosting fitness classes, live demonstrations, art exhibitions, and community events rather than primarily serving as transaction points.

REGIONAL ANALYSIS

ASIA PACIFIC MOST ADVANCED

| teamLab Borderless Azabudai | ~9,300 m², Mori Building, Tokyo (Feb 2024 opening) | teamLab Planets Expansion | Expanded 1.5x size, 20+ new artworks, January 2025 |

| Japan Inbound Tourism 2025 | 30 million+ visitors; Expo 2025 Osaka targeting 42-44M | Isetan Shinjuku 2024 Sales | Record ¥421 billion (Isetan Mitsukoshi Holdings) |

Asia Pacific leads the global experiential retail real estate market in format innovation and visitor density, anchored by Japan's teamLab venues, South Korea's K-pop brand experience flagship stores, and China's phygital retail laboratories. teamLab Borderless relocated from Odaiba to Azabudai Hills in February 2024, occupying approximately 9,300 square metres of the Mori Building mixed-use development's basement level as its primary experiential anchor. In January 2025 teamLab Planets expanded to approximately 1.5 times its previous size, introducing three new educational project areas and over 20 new artworks. Japan's inbound tourism exceeded 30 million visitors annually in 2025, with the yen depreciation sustaining exceptional visitor spending power in commercial districts including Ginza and Shibuya. Isetan Shinjuku recorded record sales of JPY 421 billion in 2024 per Isetan Mitsukoshi Holdings investor data, driven by affluent domestic shoppers and foreign tourist spending amplified by yen weakness.

NORTH AMERICA ANCHOR

| Experiential REIT AFFO Growth | 8% (2025), 99% occupancy | LBE Market Forecast | USD 73.5 billion by 2035 (Valo Motion analysis) |

| Six Flags-Cedar Fair Merger | USD 8 billion combined North American entity | Sandbox VR | Pipeline of 25 new locations, Asia Pacific and Europe focus |

North America's experiential retail real estate market is defined by the repositioning of former anchor department store space into entertainment zones and the growth of EPR Properties as the largest pure-play experiential real estate REIT. EPR Properties recorded 8% AFFO growth and 99% occupancy in 2025, with its portfolio of theatre, ski, golf, and family entertainment assets generating near year-round utilisation above the historical peak-season model. Six Flags' merger with Cedar Fair created a USD 8 billion North American outdoor entertainment giant, reducing the standalone entertainment anchor universe and concentrating the indoor experiential retail opportunity that Sandbox VR, Meow Wolf, and immersive art operators are filling. PREIT reported significant traffic and dwell time gains from retailtainment investments at its mall portfolio, per ICSC reporting, with tenants actively seeking proximity to entertainment attractions.

EUROPE AND MIDDLE EAST LUXURY EXPERIENCE

| Louis Vuitton | Champs-Élysées retailtainment concept in development | Dubai Mall The District | AED 1.5 billion, 279 outlets, immersive dining experiences |

| MAF Mall of Emirates | AED 5 billion transformation: theatre, wellness, cultural hub | UK Food Halls | Repositioned market buildings and former retail as curated F&B |

Europe and the Middle East's experiential retail real estate market is led by Paris luxury retailtainment and Dubai's destination mall investment cycle. Louis Vuitton CEO Pietro Beccari described the Champs-Élysées retailtainment concept as something never seen before, blending retail with culture and experience at the most prestigious retail address in Europe. In Dubai, both Emaar's AED 1.5 billion Dubai Mall expansion and Majid Al Futtaim's AED 5 billion Mall of the Emirates transformation are explicitly experiential investments adding theatres, wellness facilities, cultural hubs, and immersive dining precincts rather than conventional retail GLA. The UK's food hall repositioning market, where former market buildings and department store ground floors are being converted to curated artisanal food markets, represents Europe's fastest-growing experiential retail format by unit count, with operators including Market Halls and independent food hall developers creating neighbourhood gathering places that generate comparable dwell times to entertainment venues.