By Service Type - By Operator Model - By End-User - By City

City Spotlights: Paris - Marseille - Hauts-de-France

France's carrier-neutral co-location market grew at a CAGR of 15.6% during 2021 to 2025 to reach USD 2.09 billion, Brookfield Asset Management raised its French data centre investment commitment to EUR 30 billion through Data4 in June 2026, targeting 1.5 gigawatts of new carrier-neutral hyperscale capacity by 2030, Equinix opened a new Paris facility adding 20 megawatts in February 2025 extending its ten-facility Paris network hosting 160-plus network providers, and France's EUR 109 billion in AI infrastructure pledges at the February 2025 Paris AI Action Summit established the country as Europe's primary AI carrier-neutral data centre investment destination.

MARKET SYNOPSIS

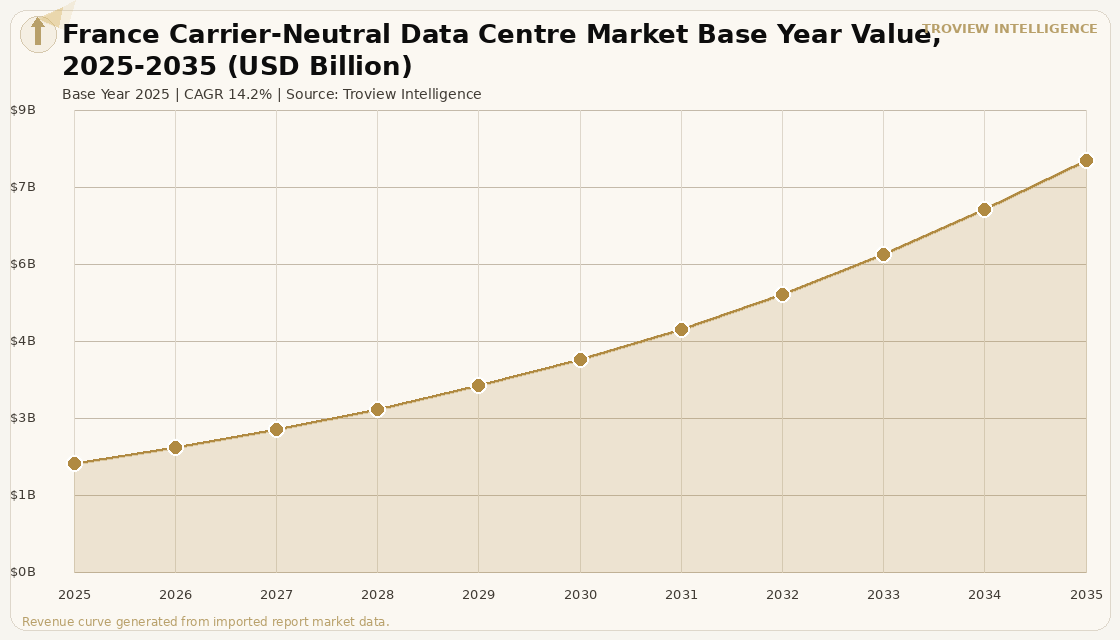

The France carrier-neutral data centre market size was USD 2.09 Billion in 2025 and is expected to register a revenue CAGR of 14.2% during the forecast period, reaching USD 7.84 Billion by 2035. France is the fourth-largest carrier-neutral co-location market in Europe, with the French co-location market having grown at a CAGR of 15.6% during 2021 to 2025 per verified industry data. The market serves a mix of hyperscale, enterprise, and public sector demand concentrated in Paris, with France's national AI sovereignty strategy creating a new category of carrier-neutral demand from domestic AI model training and inference operators including Mistral AI and HuggingFace requiring GPU-optimised co-location. France hosts 139 data centres with Paris dominating at more than 600 megawatts of installed capacity per verified operator data, with 16 operators delivering approximately 250,000 racks and a rack density profile among the highest in Europe. For instance, in February 2025, Brookfield Asset Management, Canada, committed EUR 20 billion to AI infrastructure in France at the Paris AI Action Summit subsequently raised to EUR 30 billion in June 2026 with EUR 15 billion allocated to Data4 Group for carrier-neutral hyperscale campus construction across multiple French regions targeting 1.5 gigawatts of new capacity by 2030 and positioning France as Data4's single largest European market, per Brookfield press release and Data Centre Dynamics reporting. These are some of the key factors driving revenue growth of the market.

The France carrier-neutral data centre market is led by Equinix, Digital Realty (Interxion), and Data4 Group, which collectively dominate the operator landscape across 117 active facilities managed by 36 operators per verified France data centre market data. Equinix operates the largest French footprint with ten Paris data centres and multiple Marseille facilities, providing carrier-neutral interconnection to more than 160 network service providers and over 100 cloud service providers per Equinix product disclosure. France's upcoming data centre capacity is projected to exceed 3 gigawatts, which is nearly 30 times current existing capacity per verified October 2025 portfolio data, driven by hyperscaler demand from Amazon Web Services, Microsoft Azure, and Google alongside sovereign AI infrastructure from Mistral AI, whose 40 megawatt Essonne facility deployed 18,000 NVIDIA Grace Blackwell Superchips following its EUR 1.7 billion funding round at an EUR 11.7 billion valuation with ASML as the largest shareholder. France's Cloud au Centre strategy directing public sector IT toward SecNumCloud-qualified carrier-neutral facilities is generating sovereign co-location demand that reinforces France's structural position as the primary European carrier-neutral market for government workloads.

However, the France carrier-neutral data centre market faces structural constraints that limit the pace of supply delivery. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy cost inflation that, while less severe for France than for LNG-dependent European markets due to EDF's nuclear baseload dominance, is creating power purchase agreement pricing uncertainty for carrier-neutral operators planning long-term energy procurement for the gigawatt-scale capacity additions committed by Brookfield-Data4. EDF capacity constraints could delay Brookfield's Data4 1 gigawatt carrier-neutral build by 12 to 24 months and push delivery past 2029 if grid reinforcement programmes in northern France do not advance on schedule, per verified AI infrastructure analysis. The structural shift of hyperscale cloud providers including Microsoft, Amazon, and Google toward self-built campus infrastructure in France bypassing carrier-neutral co-location entirely for their core cloud region capacity requirements is reducing the share of new hyperscale demand that flows through carrier-neutral facilities and increasing operator dependence on enterprise, AI, and sovereign cloud segments for occupancy growth. These factors substantially limit France carrier-neutral data centre market growth over the forecast period.

TROVIEW ANALYST PERSPECTIVE "France has done something no other European country has managed: it has convinced the private sector and the French state to align simultaneously on AI infrastructure investment at a scale that makes the country's carrier-neutral data centre market structurally different from every other European market. Brookfield's EUR 30 billion Data4 commitment, Mistral AI's 40 MW Essonne facility, the EUR 109 billion in total pledges at the February 2025 AI Action Summit these are not promotional announcements. They are capital commitments that are already appearing in planning applications and grid connection requests across Ile-de-France and Hauts-de-France. The carrier-neutral market benefits from this AI surge in two ways: through direct demand from AI model operators like Mistral who need carrier-neutral multi-cloud interconnection for inference traffic distribution, and through the enterprise demand wave that follows AI infrastructure investment as businesses deploy AI applications requiring carrier-neutral co-location proximity to the model hosting infrastructure. The constraint is EDF. France's nuclear grid is a structural advantage for carbon-efficient carrier-neutral operations. It is also the bottleneck for any build above 100 megawatts on a single site without extraordinary grid reinforcement measures." Troview Intelligence Head of France Data Centre Market Research

SEGMENT INSIGHTS

Three Cities Shaping France's Carrier-Neutral Market

Paris PRIMARY CARRIER-NEUTRAL HUB, 600MW+, EUR 109BN AI PLEDGES

| Installed Capacity | Existing Data Centres | Upcoming Capacity | Key CN Operators |

| 600MW+ (Paris metro) | 139 nationwide, Paris leads | 3GW pipeline (30x current) | Equinix (10 DCs), Interxion, Data4 |

Paris is France's primary carrier-neutral data centre hub and Europe's fourth-largest co-location market by revenue, concentrating the majority of French carrier-neutral rack capacity across carrier-neutral campuses in Saint-Denis, Pantin, La Courneuve, and La Plaine Saint-Denis. Equinix operates ten Paris data centres including PA2, PA3, PA4, PA5, PA6, PA7, PA8, PA9, PA10, and its newly opened February 2025 facility, collectively hosting more than 160 network service providers and over 100 cloud service providers and providing carrier-neutral ultra-low-latency routes between the United States and Europe as well as access to southern European, African, and Middle Eastern markets via Paris's subsea cable landing proximity in Normandy. OVHcloud launched a multi-zone Paris cloud region in April 2025, strengthening redundancy for enterprise clients and adding a domestically-operated sovereign cloud endpoint to the Paris carrier-neutral ecosystem. Prologis announced four hyperscale-ready sites in the greater Paris area in May 2025, increasing land inventory for build-to-suit carrier-neutral projects from the logistics real estate perspective.

| Market Position | Subsea Cable Advantage | Key Operator | Growth Driver |

| France's 2nd DC market | 15+ subsea cables landing | Interxion MRS1, Equinix MRS | Africa-Europe data flows, MENA |

Marseille is France's second-largest carrier-neutral data centre market and Europe's most important subsea cable gateway for Africa-Europe and Middle East-Europe data flows, with more than 15 major subsea cables landing in the city including the 2Africa cable serving 46 countries across Africa and the Seacom and SEWFA systems that connect European carrier-neutral facilities to MENA and Sub-Saharan African markets. Interxion's MRS1 facility and Equinix's Marseille campus constitute the primary carrier-neutral co-location infrastructure for the subsea cable landing ecosystem, enabling submarine cable operators, ISPs, and content delivery networks to interconnect at the physical landing point without the latency overhead of backhaul to Paris. Marseille's carrier-neutral market is growing faster than Paris on a percentage basis, driven by the increasing volume of transatlantic-alternative routing that uses the Marseille cable ecosystem to bypass congested North Atlantic routes, and by African hyperscaler demand from cloud providers building out content delivery infrastructure to serve the continent's fastest-growing internet user population.

| Data4 Investment Committed | Target Capacity | Key Sites | Government Support |

| EUR 30bn (Brookfield-Data4) | 1.5 GW by 2030 | Cambrai (E-Valley), Escaudain | France AI Action Plan, EDF grid |

The Hauts-de-France region in northern France is emerging as a primary carrier-neutral hyperscale development zone under Brookfield's EUR 30 billion Data4 investment programme, with two confirmed campus sites the E-Valley development in Cambrai and an AI-focused campus in Escaudain both designed as carrier-neutral hyperscale facilities for AI inference and training workloads from cloud providers, sovereign AI operators, and enterprise customers requiring large-format GPU-dense co-location. The region's advantages for hyperscale carrier-neutral development include available large industrial land parcels at substantially lower cost than Ile-de-France, proximity to cross-Channel subsea cables connecting to the UK carrier-neutral market, EDF grid connection timelines that benefit from the region's existing industrial power infrastructure, and French government incentives under the AI Action Plan that prioritise infrastructure investment in regions outside Paris. The Hauts-de-France campuses represent the largest single carrier-neutral capacity addition in Europe planned for delivery before 2030 and will structurally rebalance the French carrier-neutral market geography from its current Paris concentration toward a multi-city footprint with Paris, Marseille, and northern France each serving distinct demand categories.