By Cluster · By Facility Type · By Tenant Sector · By Development Stage

Cluster Spotlights: Paris-Saclay · Villejuif-Gustave Roussy · Genopole · Lyon Biopole

France is experiencing its largest pharmaceutical manufacturing investment boom in decades, with Sanofi, Pfizer, AstraZeneca, and Novo Nordisk collectively committing over EUR 4 billion in new investments since 2023, France's 864 biotechnology companies generated USD 1.7 billion in fundraising in 2024 a 39% increase from 2023 and the Paris region's marketable life sciences real estate supply is on course to more than double by end-2026, underpinned by the France 2030 strategy's five designated bio-clusters and EUR 7 billion committed to health innovation.

MARKET SYNOPSIS

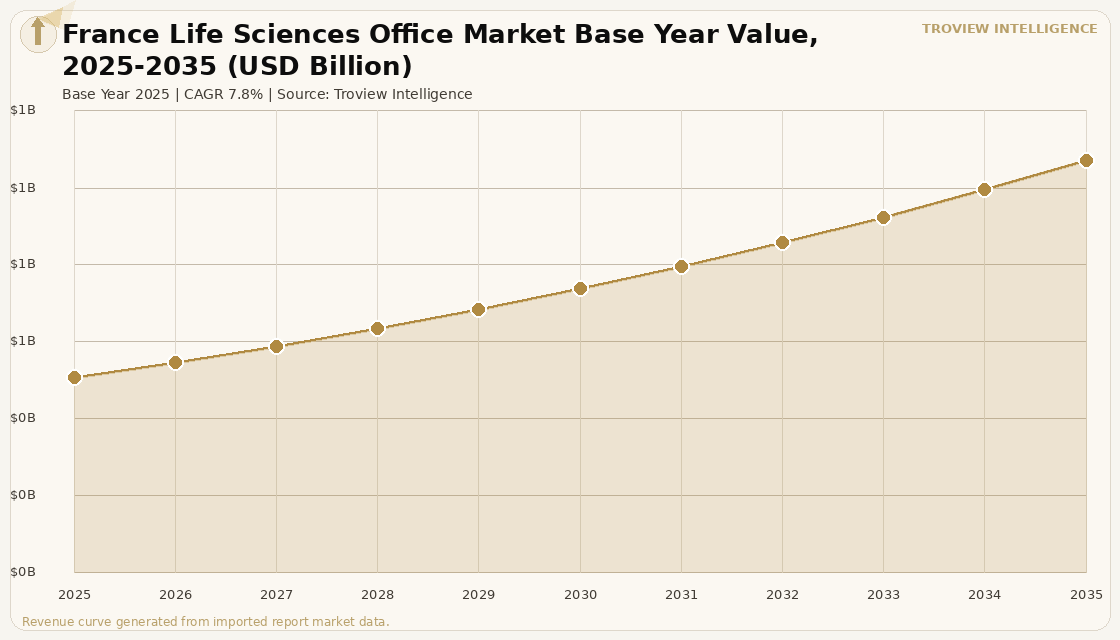

The France life sciences office market size was USD 487.4 Million in 2025 and is expected to register a revenue CAGR of 7.8% during the forecast period, reaching USD 1.03 Billion by 2035. Market revenue growth is supported by the French government's France 2030 strategy, which committed EUR 7 billion to health innovation and designated five bio-clusters for active development support, with 42 biotherapy production projects receiving state funding as France targets increasing domestically produced biomedicines from approximately 10% of medicines used in France today to around 60 domestically produced products by 2030. France's biotechnology industry comprises approximately 864 companies employing 25,000 professionals, generating total revenue of USD 1.1 billion and R&D investments exceeding USD 900 million in 2024 per EY and France Biotech analysis, with fundraising reaching USD 1.7 billion in 2024, a 39% increase from 2023, confirming accelerating investor confidence in the French life sciences ecosystem. The Choose France summit in May 2024 secured a record EUR 15 billion in international investment commitments, with Sanofi, Pfizer, and AstraZeneca collectively pledging EUR 1.87 billion in France investments, including Sanofi's commitment of more than EUR 1 billion across three French manufacturing sites and Pfizer's EUR 500 million five-year R&D investment pledge. Novo Nordisk, Sanofi, and Pfizer collectively committed over EUR 4 billion in new French investments since 2023, according to PharmaBoarroom's analysis of French pharmaceutical sector commitments, confirming France as the leading continental European destination for biopharma capital allocation.

The Paris region's life sciences real estate market is structurally undersupplied relative to the depth and growth of its tenant base. The Institut Paris Region documented existing marketable life sciences real estate of approximately 108,000 square metres in the Ile-de-France region, with the supply on course to more than double to 250,000 square metres by end-2026 and exceed 300,000 square metres by 2030 across 42 inventoried sites concentrated in Essonne, Val-de-Marne, and Paris departments. The four primary development territories the Paris-Saclay Cancer Cluster in Villejuif, the Saclay plateau, Genopole in Evry, and the southern half of Paris account for over 90% of projected supply by 2030, reflecting the government's deliberate concentration of life sciences infrastructure around the Gustave Roussy Institute, Paris-Saclay University, and the Polytechnic Institute of Paris. For instance, in June 2026, Kadans Science Partner, Netherlands, officially inaugurated The Hive at Campus Grand Parc in Villejuif, France, delivering approximately 25,000 square metres of laboratory and office space dedicated entirely to oncology research as the first building under France's first oncology innovation hub, with the Paris Saclay Cancer Cluster receiving the first biocluster designation under France 2030 and the Ile-de-France Region awarding a EUR 1 million grant for the internal innovation centre, per the Kadans Science Partner press release of June 5, 2026. These are some of the key factors driving revenue growth of the market.

However, the France life sciences office market faces structural constraints that moderate the pace of growth through the forecast period. France's reimbursement framework creates a challenging commercial environment for pharmaceutical companies, with an average time between marketing authorisation and reimbursement of 523 days, compared to 219 days in Austria and 52 days in Germany, per the 2025 Patients W.A.I.T. Indicator published by IQVIA and EFPIA, discouraging some companies from prioritising French launch timelines and dampening the commercial motivation for research office expansion relative to other European markets. The risk that France becomes a low-ceiling reference pricing country for US drug price negotiations may lead global pharmaceutical companies to delay or defer French market launches to avoid depressing their global pricing, creating uncertainty for R&D tenant commitments that would otherwise translate into life sciences office demand. Venture capital into French biotechs, while growing 39% in 2024, remains concentrated in early-stage companies that require incubator and small-scale lab space rather than the large floor plate R&D campuses that generate the highest revenue per square metre for life sciences real estate developers and institutional investors. These factors substantially limit France life sciences office market growth over the forecast period.

France's life sciences real estate story in 2025 and 2026 is being written at the cluster level, not the national level. The Paris Saclay Cancer Cluster designation under France 2030, the EUR 1.87 billion pharma investment pledge at Choose France, and Jeito Capital closing Europe's largest independent biopharma fund at EUR 1 billion are happening simultaneously with a life sciences real estate supply pipeline that is doubling from 108,000 to 250,000 square metres by end-2026. That is a structural supply-demand dynamic that has not been replicated in any other major European life sciences cluster at this pace. The question for real estate investors is not whether Paris has the demand. It is whether the development pipeline, currently dominated by Kadans, Biolabs, and EPA Paris-Saclay, can be institutionalised and securitised into investable structures before the window of undersupply closes." Troview Intelligence Senior Analyst, European Life Sciences Real Estate

SEGMENT INSIGHTS

By Facility Type

Purpose-built laboratory and R&D office campuses are expected to account for a significantly large revenue share in the France life sciences office market during the forecast period.

Based on facility type, the France life sciences office market is segmented into purpose-built laboratory and R&D campuses, incubator and accelerator facilities, converted light industrial lab space, biomanufacturing and GMP production buildings, and hospital-adjacent innovation centres. Purpose-built laboratory campuses dominate market revenue, led by developments from Kadans Science Partner, EPA Paris-Saclay, and Patriarche that are delivering BSL1 and BSL2 wet labs, dry labs, and clean rooms integrated with office space in the four primary Ile-de-France development corridors. Incubator and accelerator facilities are the fastest-growing segment by number of transactions, as early-stage French biotech companies, which represent the majority of France's 864 biotechnology companies, require flexible small-format lab access near academic medical centres before they reach the scale to commit to full building leases. Biolabs is developing a 10,000 square metre healthcare innovation centre at Hôtel-Dieu in central Paris in partnership with AP-HP and the University of Paris, targeting approximately 100 startups at completion by 2028, per Choose Paris Region documentation.

By Cluster

The Paris-Saclay and Villejuif-Gustave Roussy corridor is expected to account for a significantly large revenue share in the France life sciences office market during the forecast period.

Based on cluster, the France life sciences office market is segmented into Paris-Saclay including Saclay plateau, Villejuif and the Paris Saclay Cancer Cluster, Genopole in Evry-Courcouronnes, Lyon Biopole, Eurobiomed in Marseille, and Atlanpole Biotherapies in Nantes. The Paris-Saclay and Villejuif corridor is the largest and fastest-growing cluster by marketable life sciences real estate square metres, anchored by Paris-Saclay University, the Polytechnic Institute of Paris, and the Gustave Roussy Institute Europe's largest cancer treatment centre which together create the academic, clinical, and industrial co-location that defines a globally competitive life sciences cluster. Genopole in Evry is France's largest dedicated biotechnology cluster and specialises in genomics, cell and gene therapy, and rare disease research, hosting over 80 companies and receiving sustained state support as a designated competitiveness cluster under the French National Research Agency framework. Lyon Biopole is expected to register rapid revenue growth over the forecast period as the Lyon metropolitan area benefits from Sanofi's established manufacturing and research presence and a university medical centre complex that provides clinical trial infrastructure for Phase II and Phase III oncology and immunology studies.

By Tenant Sector

Large pharmaceutical and established biotech company tenants are expected to account for a significantly large revenue share in the France life sciences office market during the forecast period.

Based on tenant sector, the France life sciences office market is segmented into large pharmaceutical companies, established biotechnology firms, early-stage venture-backed biotechs, contract research organisations, medical device companies, and academic and hospital research institutions. Large pharmaceutical companies dominate leased floor area and revenue, with Sanofi's headquarters and multiple research facilities anchoring the Paris-region market, and Servier, a French-owned pharmaceutical company, maintaining its primary R&D campus at Paris-Saclay as an anchor tenant for the Saclay plateau cluster. Early-stage venture-backed biotechs are the fastest-growing tenant segment by company count, supported by French public investment bank BPI France's life sciences mandates and the EUR 1 billion Jeito II Fund closed in April 2026, which will fund companies requiring scale-up laboratory space across Paris-region clusters. AstraZeneca's USD 140 million investment in Paris-based Cellectis in 2024, following an earlier cell therapy development agreement, illustrates the in-licensing and co-investment dynamic between global pharma and French biotech that generates co-located R&D office demand within the Ile-de-France ecosystem.

Four Clusters Shaping France's Life Sciences Office Market

| Existing Lab/R&D Supply (Saclay Plateau) | >50,000 m² pipeline by 2030 | Key Development | Kadans The Mix, 15,000 m² (Q3 2026) |

| Anchor Institutions | Paris-Saclay University, Polytechnic Institute Paris | Key Corporate Tenants | Servier, Danone, Oracle, GSK |

Paris-Saclay is France's largest life sciences campus and one of the largest science and innovation clusters in Europe, centred on Paris-Saclay University and the Polytechnic Institute of Paris, which together constitute one of the highest concentrations of scientific and engineering talent in continental Europe. The accumulated potential lab and R&D supply on the Saclay plateau is estimated at more than 50,000 square metres by 2030 per Institut Paris Region, with Kadans Science Partner delivering The Mix, a 15,000 square metre research and development facility with flexible BSL1 and BSL2 wet labs, dry labs, and clean rooms, targeted for Q3 2026 completion per Kadans property documentation. Servier and Danone have established primary R&D operations on the Saclay campus, alongside multinational corporate research centres from Oracle and GSK that leverage proximity to the university's PhD and postdoctoral researcher pipeline. The EPA Paris-Saclay public development agency is advancing Le Central, a 16,000 square metre dedicated life sciences building, as part of the government-backed infrastructure programme that supports the cluster's transition from a science campus to a commercial life sciences cluster capable of attracting institutional real estate investment.

VILLEJUIF / PARIS SACLAY CANCER CLUSTER FASTEST-GROWING ONCOLOGY HUB

| The Hive (Kadans) | 25,000 m² oncology labs and offices (inaugurated Jun 2026) | Anchor Institution | Gustave Roussy Institute (Europe's largest cancer centre) |

| Development Pipeline | 30,000+ m² additional area by 2030 | Government Designation | France 2030 first bio-cluster |

Villejuif and the Paris Saclay Cancer Cluster represent the most consequential new life sciences real estate development territory in continental Europe, anchored by the Gustave Roussy Institute, Europe's largest cancer treatment centre, and designated as France's first bio-cluster under the France 2030 strategy. Kadans Science Partner officially inaugurated The Hive at Campus Grand Parc on June 5, 2026, delivering 25,000 square metres of laboratory and office space dedicated entirely to oncology research, with the Paris Saclay Cancer Cluster developed through a consortium comprising Paris-Saclay University, the Polytechnic Institute of Paris, Inserm, Gustave Roussy, and Sanofi per Campus Grand Parc documentation. The Ile-de-France Region awarded a EUR 1 million grant to support the innovation centre within The Hive for early-stage startups, and over 30,000 square metres of additional area are planned by 2030, per Institut Paris Region supply analysis. Connectivity to central Paris is provided by metro lines 7 and 14 and the Grand Paris Express line 15, with a 20-minute journey time to central Paris per Kadans property documentation, supporting the workforce commuting patterns required for a competitive research campus.

GENOPOLE (EVRY-COURCOURONNES) FRANCE'S LEADING BIOTECH CLUSTER

| Companies Hosted | >80 biotech and pharma companies | Specialisation | Genomics, cell and gene therapy, rare diseases |

| Operator | SEM Genopole (public-private structure) | Government Framework | French National Research Agency competitiveness cluster |

Genopole is France's largest dedicated biotechnology cluster, located in Evry-Courcouronnes in the Essonne department, approximately 30 kilometres south of Paris and served by the RER D suburban rail network. The cluster hosts over 80 biotechnology and pharmaceutical companies specialising in genomics, cell and gene therapy, rare disease research, and bioinformatics, representing the highest concentration of gene therapy and advanced biotherapy expertise in France. Genopole is operated through a public-private structure, SEM Genopole, with backing from the French National Research Agency and the Ile-de-France Region as a designated competitiveness cluster, providing below-market rental rates for early-stage companies and shared laboratory infrastructure that reduces the capital requirements for laboratory fit-out. The France Genomic Medicine 2025 national strategy and the National Health Data System, both supported by the French Ministry of Health, create a data-sharing infrastructure that makes Genopole-based companies particularly competitive in oncogenomics, rare disease biomarker research, and personalised medicine applications that require integration of clinical and molecular data at scale.

| Key Anchor | Sanofi manufacturing and R&D (Lyon operations) | Sector Focus | Infectious diseases, oncology, veterinary |

| University Anchor | University Claude Bernard Lyon 1, HCL hospital complex | Regional Support | Auvergne-Rhone-Alpes Region life sciences programme |

Lyon Biopole is France's second-largest metropolitan life sciences cluster, anchored by Sanofi's established manufacturing and research operations in the Lyon area, the University Claude Bernard Lyon 1, and the Hospices Civils de Lyon hospital complex that provides Phase I through Phase III clinical trial infrastructure for oncology, infectious disease, and immunology research. The cluster is expected to register rapid revenue growth over the forecast period as the Auvergne-Rhone-Alpes Region's life sciences investment programme, backed by the French National Research Agency's competitiveness cluster framework, channels capital into laboratory real estate development adjacent to the Gerland and Lyon-Part-Dieu science and innovation districts. Lyon's positioning as France's primary hub for veterinary life sciences research, through the Merieux Institute and BioMerieux's global headquarters and research operations, differentiates the cluster from Paris-centric oncology and genomics focus areas and provides a diversified tenant base for life sciences real estate developers entering the market.