By Submarket · By Property Grade · By Government Function · By Tenure

Seoul's prime office market recorded an average vacancy rate of 3.7% across the three major business districts in Q4 2025, with Grade A rents rising 4.3% for the full year and Yeouido reaching 5.0% rental growth, as Jongno-gu Office relocated 9,500 square metres into The K Twin Tower in the Gwanghwamun CBD and the Lee Jae Myung administration's Five Mega-Regions strategy commits to expediting the second phase of public institution relocation to Sejong City and provincial hubs creating a bifurcated Seoul government office market where prime CBD buildings are attracting relocated government agencies while ageing Gwacheon-era stock faces structural vacancy and repositioning.

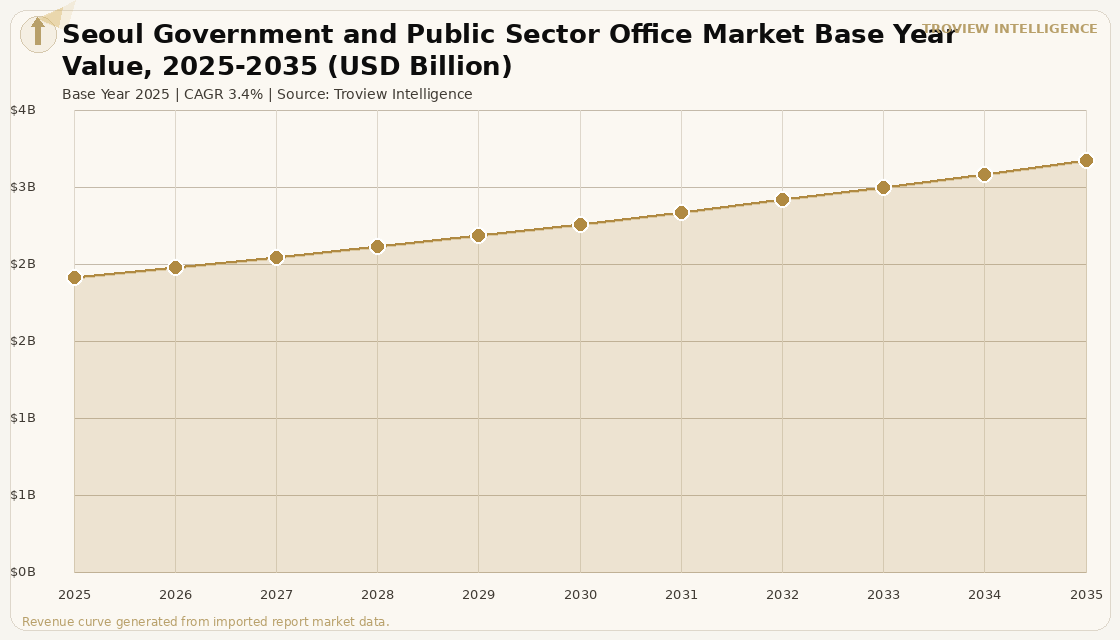

MARKET SYNOPSIS

The Seoul government and public sector office market size was USD 2.34 Billion in 2025 and is expected to register a revenue CAGR of 3.4% during the forecast period, reaching USD 3.27 Billion by 2035. Market revenue growth is supported by the sustained concentration of South Korea's executive, legislative, and diplomatic functions in Seoul, the active refurbishment and upgrading of government-occupied office buildings in the Gwanghwamun and Central Business District to meet mandatory zero-energy building standards, and the continued demand from quasi-government organisations, national policy research institutes, and international organisations that require proximity to the National Assembly, the presidential complex, and the foreign ministry cluster. Seoul contributed 56.1% of South Korea's total office market revenue in 2024 per Korea Real Estate Board data, and the city's Grade A office market recorded average rent growth of 4.3% in 2025 across the Central Business District, Gangnam Business District, and Yeouido Business District, with rents for prime offices in the three districts exceeding KRW 160,000 per 3.3 square metres per Seumter administrative platform data maintained by the Ministry of Land, Infrastructure and Transport. The average vacancy rate across Seoul's three prime business districts held at 3.7% in Q4 2025, confirming the structural tightness of the market despite corporate tenant consolidation by SK Group and planned downsizing by LG Chem, as incoming tenants including government agencies, law firms, and financial institutions absorbed vacated space at a rate that sustained positive net absorption.

Seoul's government office market is defined by the Gwanghwamun submarket, which anchors the Central Business District and concentrates the remaining Seoul-based functions of central ministries, the presidential office complex relocated from Cheong Wa Dae, diplomatic missions, and the permanent staffing of National Assembly liaison offices for each ministry. In Q4 2025, Jongno-gu Office moved 9,500 square metres into The K Twin Tower in the Gwanghwamun district, representing a direct government agency contribution to positive CBD net absorption, and Hanwha Claims Management relocated 4,300 square metres to the KCCI Building, both transactions confirming that government-affiliated organisations are actively consolidating into modernised Grade A space within the CBD. The Ministry of Land, Infrastructure and Transport's Seumter platform, which operates as South Korea's national building administration system, confirmed that only 9% of office buildings in Seoul's three major business districts are 10 years old or newer, confirming the ageing physical stock that government tenants occupy in the CBD and the capital refurbishment requirement this creates for property owners in the Gwanghwamun and Jongno areas. For instance, in December 2024, Mirae Asset Global Investments, South Korea, acquired Centropolis Tower B in Jongno-gu from Eugene Asset Management for USD 540 million, expanding its core office portfolio in central Seoul directly adjacent to the principal Gwanghwamun government cluster and confirming that top-tier Korean institutional investors are placing capital in the CBD buildings most proximate to government tenant concentration, per Korea real estate transaction records. These are some of the key factors driving revenue growth of the market.

However, the Seoul government and public sector office market faces structural constraints that limit revenue growth over the forecast period. The Lee Jae Myung administration's commitment to developing Sejong City as the undisputed administrative capital and expediting the second phase of public institution relocation to the provinces will progressively reduce the national ministry footprint in Seoul over the forecast period, removing structurally stable, long-tenure government tenants from the Gwanghwamun and surrounding CBD submarkets. The mandatory zero-energy building standard by 2030 under the Act on the Promotion of Green Buildings will require government-owned office buildings in Seoul, many of which are in the 30-to-40-year building age cohort identified by Seumter data, to undergo capital-intensive energy system refurbishments and building envelope upgrades that will temporarily displace tenants and create short-term vacancy in government-occupied CBD stock. The Yeouido Business District's government tenant profile, anchored by the National Assembly and financial regulatory bodies, faces disruption from the November 2024 government approval of the Yeouido Financial District Unit Plan enabling skyscraper developments over 200 metres that will trigger the redevelopment of older buildings currently housing government agencies and financial regulatory tenants. These factors substantially limit Seoul government and public sector office market growth over the forecast period.

Seoul's government office market tells the most precisely readable story of any government real estate market in Asia. Gwanghwamun is a landlord market 3.7% prime vacancy, 4.3% rent growth, and government agency relocations into The K Twin Tower demonstrating that what the CBD is losing in ministry headcount to Sejong it is gaining back in agency consolidation into premium space. The real tension is in the 47% of buildings that are over 30 years old. Government agencies will not sign 15-year leases in a building that cannot meet the 2030 zero-energy mandate. Owners of ageing CBD government buildings need to either refurbish to that standard or accept that their government tenants will leave for a building that has already done the upgrade. That is the defining investment question in Seoul government real estate for the rest of this decade." Troview Intelligence Senior Analyst, Seoul Government Office Markets

SEGMENT INSIGHTS

By Property Grade

Grade A and newly refurbished office buildings occupied by government and quasi-government tenants are expected to account for a significantly large revenue share in the Seoul government and public sector office market during the forecast period.

Based on property grade, the Seoul government and public sector office market is segmented into Grade A purpose-built or recently refurbished government-occupied buildings, Grade B government-tenanted buildings, legacy government-owned buildings requiring refurbishment, and purpose-built government complex buildings. Grade A assets dominate market revenue and rental income, with average vacancy of 3.7% across the three prime districts and Grade A rents exceeding KRW 160,000 per 3.3 square metres in prime locations per Seumter data published by the Ministry of Land, Infrastructure and Transport. The mandatory zero-energy building standard by 2030 under the Act on the Promotion of Green Buildings is creating a sustainability stratification within Grade A government-tenanted stock, as buildings that have completed or are committed to zero-energy upgrades command a greenery premium and retain government agency tenants that face internal sustainability procurement requirements under the Seoul Metropolitan Government's green public procurement policies. Grade B and legacy government-owned buildings are expected to register declining occupancy rates over the forecast period as government agencies consolidate into modernised Grade A space and older buildings face the dual pressure of non-compliance with the zero-energy standard and functional obsolescence relative to modern collaborative workspace requirements.

By Submarket

The Gwanghwamun Central Business District submarket is expected to account for a significantly large revenue share in the Seoul government and public sector office market during the forecast period.

Based on submarket, the Seoul government and public sector office market is segmented into Gwanghwamun and Jongno CBD, Yeouido Business District, Gangnam Business District, Mapo and City Hall area, Gasan and digital media city corridor, and the outer Seoul Metropolitan Area. The Gwanghwamun submarket dominates government office revenue as the primary address of presidential complex liaison offices, remaining central ministry Seoul functions, diplomatic missions, and the Jongno government administration cluster. The Yeouido Business District is the fastest-growing submarket for government-related office demand, driven by the National Assembly secretariat and the financial regulatory bodies including the Financial Services Commission and Financial Supervisory Service, with YBD recording 5.0% rent growth in 2025 the strongest of the three districts reflecting tight supply and active tenant demand from government-affiliated financial institutions. The November 2024 government approval of the Yeouido Financial District Unit Plan enabling towers over 200 metres will accelerate redevelopment of older Yeouido buildings that currently house government regulatory tenants, creating a near-term relocation cycle that will generate demand for transitional Grade A space within the YBD and adjacent CBD.

By Government Function

Executive and regulatory government functions concentrated in the Gwanghwamun and Yeouido submarkets are expected to account for a significantly large revenue share in the Seoul government and public sector office market during the forecast period.

Based on government function, the Seoul government and public sector office market is segmented into executive branch liaison offices and presidential complex support agencies, legislative branch and National Assembly operations, financial and economic regulatory bodies, diplomatic and international organisation offices, quasi-government research and policy institutes, and Seoul Metropolitan Government operations. Executive and regulatory functions dominate floor area and rental income in the Gwanghwamun CBD and Yeouido districts, generating the long-term, full-floor lease structures that produce the most valuable income streams for government-tenanted office buildings. Diplomatic and international organisation offices represent the fastest-growing segment by new lease transactions, with the Gwanghwamun, Jung-gu, and Yongsan districts attracting embassy expansions and United Nations system organisations that require proximity to the South Korean foreign ministry and presidential complex while obtaining International Organisation of Securities Commissions and related financial regulatory co-location in Yeouido. Quasi-government research institutes are the most stable segment by tenant tenure, with the Korea Development Institute, Korea Research Institute for Human Settlements, and Korea Institute for Industrial Economics and Trade maintaining long-term Seoul presences in the CBD and adjacent Mapo districts.

Submarket Deep-Dives

GWANGHWAMUN / JONGNO CBD PRIMARY GOVERNMENT OFFICE SUBMARKET

| CBD Vacancy Q4 2025 | 5.0% | CBD Rent Growth 2025 | +3.7% |

| Key Government Tenant Move Q4 2025 | Jongno-gu Office, 9,500 m² to The K Twin Tower | Mirae Asset CBD Acquisition 2024 | Centropolis Tower B, USD 540M |

Gwanghwamun and the Jongno CBD is Seoul's primary government office submarket, concentrating the residential liaison offices of central ministries that have relocated to Sejong, the Cheong Wa Dae successor complex functions of the presidential office, diplomatic missions, and the Jongno-gu government administration cluster. The CBD vacancy rate was 5.0% in Q4 2025, modestly elevated following SK C&C's relocation of 6,700 square metres from Centropolis to SK-U Tower, but offset by Jongno-gu Office's 9,500 square metre move into The K Twin Tower and Hanwha Claims Management's 4,300 square metre relocation to the KCCI Building, resulting in modest net positive absorption per Korea Real Estate Asia data. Mirae Asset Global Investments acquired Centropolis Tower B in Jongno-gu for USD 540 million in December 2024, directly adjacent to the Gwanghwamun government cluster, confirming that Korean institutional investors are placing the highest capital allocations in the buildings most proximate to the government tenant core. CBD rents grew 3.7% in 2025, the most modest of the three districts, reflecting the displacement effect of ministry departures to Sejong offset by active government agency consolidations into modernised buildings.

| YBD Rent Growth 2025 | +5.0% (strongest of 3 districts) | YBD Vacancy 2025 | 3.4% |

| YBD Effective NOC vs CBD | 94% of CBD levels (up from 89% in 2020) | Yeouido Unit Plan | Towers >200m approved, Nov 2024 |

Yeouido is Seoul's National Assembly and financial regulatory hub, hosting the legislative complex that anchors demand from ministerial liaison offices, parliamentary research services, political party headquarters, and the financial regulatory bodies including the Financial Services Commission and Financial Supervisory Service that co-locate in proximity to Korea's primary financial district and exchange infrastructure. Yeouido recorded the strongest rental growth of the three major Seoul business districts at 5.0% in 2025, with the effective net operating cost reaching 94% of CBD levels up from 89% in 2020 reflecting sustained leasing momentum from rent reversions at newly completed and refurbished prime assets including TP Tower and One Centinel per Korea Real Estate Board data. In Q4 2025, SAP Korea took 6,000 square metres at One IFC and Kakaopay Securities leased space, while Apple expanded 1,700 square metres at Parc.1 Tower 1, demonstrating that technology and financial sector private tenants are entering YBD at above-market rates that will exert upward pressure on rents for government and regulatory tenants at lease renewals. The November 2024 government approval of the Yeouido Financial District Unit Plan enabling skyscraper developments over 200 metres will trigger the phased redevelopment of older YBD buildings that currently house National Assembly support functions and regulatory office operations.

| GBD Rent Growth 2025 | +4.7% | GBD Vacancy | ~2.4% (tightest district) |

| Government Presence | Quasi-government, industry regulators, research institutes | Magok Expansion | Samsung C&T / Lendlease USD 1.1B tower (2025 MOU) |

Gangnam is Seoul's tightest major office submarket with vacancy at approximately 2.4% and Grade A rent growth of 4.7% in 2025, anchored by the technology and professional services tenant base that has driven sustained above-inflation rent increases over three consecutive years. The government presence in Gangnam is concentrated in quasi-government technology regulation bodies, industry research institutes, and technology sector associations that require proximity to the leading Korean technology companies headquartered in the Gangnam and Teheran-ro corridor. Samsung C&T's March 2025 memorandum of understanding with Lendlease Asia to co-develop a USD 1.1 billion Grade A tower in Seoul's Magok R&D cluster represents the expansion of the Gangnam-area premium office supply pipeline into the western Seoul technology corridor, targeting government-adjacent technology and institutional tenants. The Korea Real Estate Board data confirms that Gangnam and Yeouido saw on-year rent increases of 12.74% and 16.03% respectively in the period preceding 2025, representing the cumulative rent growth that has created tenant fatigue and prompted some government-affiliated tenants to consider secondary location moves.

MAPO / CITY HALL AREA SEOUL METROPOLITAN GOVERNMENT AND NGO CORRIDOR

| Key Tenant Type | Seoul Metropolitan Government, NGOs, quangos | Character | Mixed government, cultural, non-profit tenants |

| Development Pipeline | Songdo and Magok as relief markets | Connectivity | Metro lines 2, 5, 6 serving City Hall area |

The Mapo and City Hall area serves as Seoul's metropolitan government corridor, housing the Seoul Metropolitan Government's administrative complex, the offices of Seoul-chartered quangos, non-governmental organisations, and the cultural and educational institutions that require proximity to City Hall while operating at rent levels below the premium CBD. The Seoul Metropolitan Government's administrative buildings in the City Hall district provide anchor occupancy that stabilises the submarket despite the lower prestige positioning relative to Gwanghwamun and Yeouido. International organisations requiring Seoul presence without the premium rental obligations of the Gwanghwamun diplomatic cluster are increasingly considering Mapo and City Hall area buildings as cost-effective alternatives, particularly for regional offices of UN system agencies and international development finance institutions that have established Asia Pacific regional presences. The area benefits from metro line 2 connectivity that links City Hall directly to both Gangnam and the Gwanghwamun CBD, supporting the hybrid working patterns of civil servants and quasi-government employees who split their working week between Seoul and Sejong City.