By Property Grade · By District · By Occupier Sector · By Lease Structure

City Spotlights: Riyadh · Jeddah · Dammam Metropolitan Area

Riyadh's Grade A headline rents climbed to SAR 2,750 per square metre in Q3 2025, up more than 15% year-on-year, at 98% occupancy a market running near structural capacity as 675 licensed multinational regional headquarters in the Kingdom by March 2025 absorb the Grade A pipeline faster than it delivers, while the Public Investment Fund's 385-metre PIF Tower at KAFD, a USD 2 billion Brookfield-PIF office venture, and the Saudi government's new foreign ownership law effective January 2026 are setting the conditions for the first major cycle of foreign institutional capital into Saudi commercial real estate.

MARKET SYNOPSIS

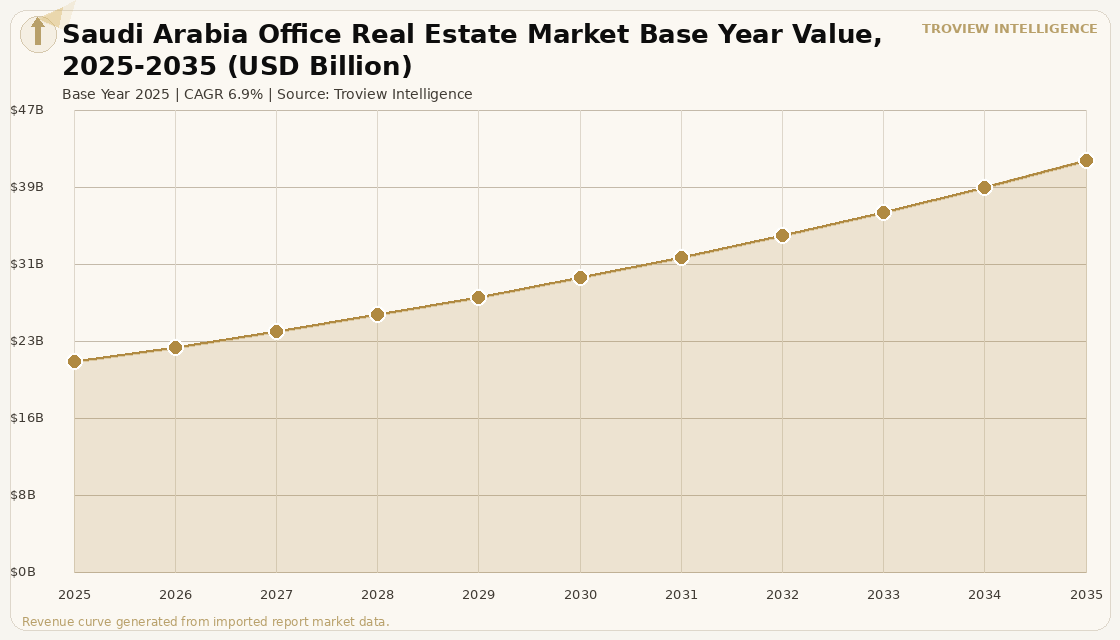

The Saudi Arabia office real estate market size was USD 21.46 Billion in 2025 and is expected to register a revenue CAGR of 6.9% during the forecast period, reaching USD 41.89 Billion by 2035. Market revenue growth is supported by the Saudi Vision 2030 programme, which mandated multinational corporations to locate their regional headquarters in the Kingdom and had licensed 675 international firms in Riyadh by March 2025 per Saudi government Regional Headquarters Program data, with each licence requiring a minimum of 15 senior employees and oversight of two MENA markets, generating sustained structural demand for large-format, high-specification Grade A office space. Grade A office supply in Riyadh reached 6.4 million square metres per the General Authority for Statistics property sector data, with Grade A rents climbing to SAR 2,750 per square metre in Q3 2025 a gain exceeding 15% year-on-year at occupancy rates of approximately 98% per market transaction records, confirming that the Kingdom's most important commercial district is operating at near-structural capacity. The King Abdullah Financial District, owned and managed by the KAFD Development and Management Company, a wholly-owned subsidiary of the Public Investment Fund, spans 1.6 million square metres across 95 towers designed by 25 world-leading architectural firms and achieved the designation of the world's largest LEED Platinum-certified mixed-use district, housing more than 140 office tenants and over 75 regional headquarters for multinational companies as of 2026. Foreign investment in Saudi Arabia's real estate sector reached SAR 3 trillion in 2025, with Riyadh capturing the largest share per Saudi Real Estate General Authority data, as property prices rose 10.6% year-on-year in September 2025.

Saudi Arabia's office market revenue growth is underpinned by the convergence of sovereign wealth capital deployment, Vision 2030 corporate attraction mandates, and infrastructure investment that is transforming the physical and digital quality of Saudi Grade A office stock. The Riyadh Metro, spanning 176 kilometres across six lines and 85 stations, became fully operational in early 2025, per the Arriyadh Development Authority, unlocking real estate value in districts along the network including King Abdullah Financial District, Al Malqa, Al Yasmin, and King Abdullah District. The Public Investment Fund is deploying capital directly into office real estate through the KAFD Development and Management Company and joint ventures including the USD 2 billion Brookfield-PIF venture that earmarks at least half its capital for domestic office assets. Saudi credit rose 16.26% year-on-year to USD 827.2 billion in March 2025, with real estate lending up 40.5% per Saudi Central Bank data, reflecting strong investment appetite in the sector. For instance, in September 2025, EY, United States, completed its 11,691 square metre MENA headquarters facility in King Abdullah Financial District, joining professional advisory firms including Deloitte, PwC, and KPMG in making long-term lease commitments to KAFD, confirming that global professional services firms are treating their Saudi headquarters presence as a permanent and expanding platform rather than a compliance-driven registration, per EY company announcements. These are some of the key factors driving revenue growth of the market.

However, the Saudi Arabia office real estate market faces structural constraints that moderate the growth trajectory. Total office stock across Riyadh, Jeddah, and the Dammam Metropolitan Area is projected to rise from approximately 9.7 million square metres in 2025 to approximately 15 million square metres by 2028 per Saudi Real Estate General Authority pipeline data, with Riyadh accounting for nearly half of this supply increase, creating near-term absorption risk as simultaneous delivery of New Murabba, expanded KAFD phases, and private towers could outpace organic tenant demand in late-decade periods if multinational headquarters expansion slows. The 5% Real Estate Transaction Tax introduced by the Saudi government in April 2025 adds financing friction for developers and acquisition investors, increasing transaction costs and creating a disincentive for speculative trading that may slow capital recycling in the secondary office investment market. Grade B office vacancy is rising in secondary locations as tenants execute a flight-to-quality consolidation, relocating from older southern Riyadh buildings to Grade A assets in the northern districts, creating bifurcated vacancy dynamics where Grade A remains near capacity while Grade B stock in peripheral locations faces extended absorption timelines. These factors substantially limit Saudi Arabia office real estate market growth over the forecast period.

Saudi Arabia's Grade A office market is operating in a regime that most markets never experience: 98% occupancy, 15% rent growth, and a government mandate that requires 675 international companies to maintain physical headquarters in the country. That is not a market cycle. That is policy-engineered structural demand meeting a supply pipeline that cannot deliver fast enough. The question for 2027 and 2028 is not whether demand exists it clearly does but whether the pipeline of New Murabba, KAFD Phase 2, and the northern Riyadh towers can be absorbed by multinational headquarters expansion without creating the oversupply dynamic that has historically followed every major Gulf construction cycle. The 2030 deadline for Vision 2030 delivery is a forcing function. After 2030, the institutional question becomes: what replaces the government mandate as the structural driver?" Troview Intelligence Head of Saudi Arabia Office Real Estate Research

SEGMENT INSIGHTS

By Property Grade

Grade A office assets are expected to account for a significantly large revenue share in the Saudi Arabia office real estate market during the forecast period.

Based on property grade, the Saudi Arabia office real estate market is segmented into Grade A, Grade B, and Grade C buildings. Grade A assets dominate market revenue and command a 47.9% share of Riyadh office demand per Saudi Real Estate General Authority data, with rents reaching SAR 2,750 per square metre in Q3 2025 at 98% occupancy as multinational regional headquarters mandates absorb supply ahead of delivery. KAFD's 95 towers, all achieving LEED Platinum certification as the world's largest LEED Platinum-certified mixed-use district per the US Green Building Council, represent the premium tier of Saudi Grade A stock and command the highest rents in the Kingdom. Grade B office assets are expected to register declining occupancy and flat rental growth over the forecast period as the flight-to-quality dynamic drives tenants from secondary Riyadh locations into modern Grade A buildings, with older southern Riyadh Grade B buildings facing structural vacancy and potential conversion or refurbishment requirements.

By City

Riyadh is expected to account for a significantly large revenue share in the Saudi Arabia office real estate market during the forecast period.

Based on city, the Saudi Arabia office real estate market is segmented into Riyadh, Jeddah, Dammam Metropolitan Area, and other cities including Makkah and Madinah. Riyadh captures 51.1% of national office demand per Saudi Real Estate General Authority data and leads the market by Grade A rent level, occupancy, and institutional investment activity. Jeddah is the fastest-growing secondary city by new Grade A supply and tenant base expansion, with Grade A occupancy at approximately 95% per Saudi Central Bank property sector data, and the city's USD 20 billion central regeneration project driving new office development in the Al-Balad historic centre and the Al-Corniche waterfront district. Dammam Metropolitan Area, encompassing Jubail and Dhahran, is expected to register the fastest CAGR of any Saudi city over the forecast period, driven by petrochemical joint venture expansions and the Kingdom's 59-hub logistics mandate requiring 5 million square metres of warehousing by 2030, which generates associated corporate office demand from energy and industrial companies.

By Occupier Sector

Financial services and professional services occupiers are expected to account for a significantly large revenue share in the Saudi Arabia office real estate market during the forecast period.

Based on occupier sector, the Saudi Arabia office real estate market is segmented into financial services and banking, professional services and advisory, energy and petrochemical, technology and fintech, government and quasi-government, and hospitality and entertainment sector corporate offices. Financial services and professional advisory firms dominate Grade A leasing at KAFD, with EY's 11,691 square metre MENA headquarters completed in September 2025 and the major global advisory firms committing to expanding Saudi Arabia presences. Technology and fintech companies are the fastest-growing occupier segment, with fintech companies thriving under Saudi Central Bank sandbox regulations and boosting demand for smaller, technology-ready office floor plates in the Riyadh Tech Quarter and adjacent northern districts. Saudi credit growing 16.26% year-on-year to USD 827.2 billion per Saudi Central Bank data, with real estate lending rising 40.5%, confirms the financial services expansion that is translating directly into Grade A office demand from both domestic Saudi financial institutions and international banks establishing or expanding regional treasury and investment banking operations.

Three Cities Shaping Saudi Arabia's Office Market

| Grade A Rent Q3 2025 | SAR 2,750/m² (+15% YoY) | Grade A Occupancy | ~98% |

| Regional HQ Licences | 675 (March 2025, Saudi RHQ Program) | KAFD Total Stock | 1.6M m², 95 buildings, 140+ office tenants |

Riyadh is Saudi Arabia's dominant office market, capturing 51.1% of national demand with Grade A rents at SAR 2,750 per square metre in Q3 2025 and occupancy at approximately 98%, confirming that the capital's premium office stock is operating at near-structural capacity. The King Abdullah Financial District, spanning 1.6 million square metres with 95 towers, hosts more than 140 office tenants and over 75 regional multinational headquarters as of 2026 per KAFD Development and Management Company records, and was awarded a Guinness World Record in July 2025 for the world's largest continuous pedestrian skyway network. The Riyadh Metro's full operational launch in early 2025, covering 176 kilometres across six lines and 85 stations per the Arriyadh Development Authority, has reinforced KAFD's 10-minute city appeal while unlocking value in northern districts including Al Malqa and Al Yasmin where property prices along metro lines recorded the strongest appreciation. Grade A supply in Riyadh is set to nearly double by 2028 with New Murabba, KAFD Phase 2, and private tower completions adding to the current 6.4 million square metre stock, creating near-term absorption risk that the Regional Headquarters Program mandate must sustain.

| Grade A Occupancy | ~95% | Office Rent Growth 2024 | 13.6% to USD 375/m² |

| Regeneration Investment | USD 20 Billion (Jeddah Central Project) | Jeddah Tower | 320-floor supertall, global landmark development |

Jeddah is Saudi Arabia's second-largest office market and the fastest-growing by new Grade A supply, driven by the USD 20 billion Jeddah Central regeneration project and the commercial demand generated by the city's position as Saudi Arabia's primary Red Sea port and Hajj and Umrah logistics gateway. Grade A occupancy in Jeddah stands at approximately 95% per Saudi Real Estate General Authority data, and office rents rose 13.6% in 2024 to USD 375 per square metre, reflecting strong financial services and logistics sector demand from companies clustering near Jeddah Islamic Port. The Jeddah Tower, designed to rise 320 floors as the world's tallest building, represents the most ambitious private sector construction commitment in Jeddah and will redefine the city's Grade A office and residential product upon delivery, attracting global occupier attention to the Al-Hamra and North Jeddah waterfront districts. The city's 29 investment prospects covering 1.4 million square metres per the Jeddah Economic Company's development pipeline will deliver diversified commercial real estate stock into a market that has historically been supply-constrained relative to multinational tenant demand.

| City CAGR Forecast | 8.41% (fastest of all Saudi cities) | Grade B Vacancy | 14% (secondary legacy stock) |

| Key Demand Driver | Petrochemical JVs, logistics, energy sector | Corporate Compound Value | USD 213,000 per unit (cost edge vs Riyadh) |

The Dammam Metropolitan Area, encompassing Dhahran, Khobar, and Jubail, is the Saudi office market with the strongest projected growth CAGR, driven by the concentration of Saudi Aramco's global headquarters in Dhahran, the SABIC and SABIC affiliate corporate campus cluster in Jubail, and the Kingdom's 59-hub logistics mandate requiring 5 million square metres of warehousing by 2030 that generates supporting corporate office demand. Saudi Aramco's annual report and earnings disclosures confirm the company maintains its global headquarters in Dhahran with supporting offices for finance, technology, and downstream operations in the broader Eastern Province, creating the largest single-employer anchor of office demand outside Riyadh. Grade B office vacancy in Dammam at 14% reflects the legacy oversupply from an earlier construction cycle, while prime assets hold steady in the high 80s occupancy per Saudi Real Estate General Authority data, confirming the flight-to-quality dynamic that characterises all three Saudi city office markets. Corporate compound acquisitions in Dammam at USD 213,000 per unit, compared to higher Riyadh equivalents, provide a cost advantage that attracts energy sector workforce relocations and sustains residential and supporting commercial demand.