By Sub-cluster · By Facility Type · By Tenant Sector · By Lab Classification

The Paris region holds only 2.9 million square feet of existing purpose-built lab and R&D space less than a single major Boston submarket yet its existing marketable area of 108,000 square metres is set to more than double by end-2026 to 250,000 square metres and exceed 300,000 square metres by 2030, driven by Kadans Science Partner, Biolabs, and EPA Paris-Saclay across four primary corridors, as The Hive oncology campus in Villejuif inaugurated in June 2026 and The Mix at Paris-Saclay targeting Q3 2026 delivery confirm that the chronic undersupply that has defined Paris life sciences real estate for a decade is finally being addressed at scale.

MARKET SYNOPSIS

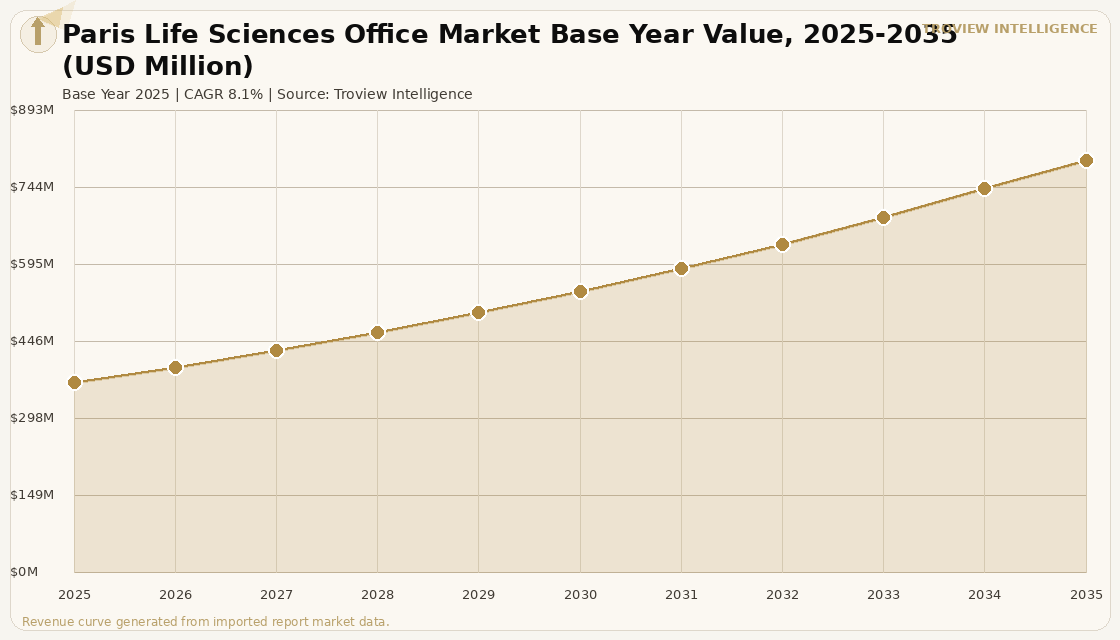

The Paris life sciences office market size was USD 368.2 Million in 2025 and is expected to register a revenue CAGR of 8.1% during the forecast period, reaching USD 797.1 Million by 2035. Market revenue growth is supported by the structural undersupply of purpose-built laboratory and R&D office space in the Paris region, where the Institut Paris Region documented existing marketable area of approximately 108,000 square metres across 42 inventoried sites in the Ile-de-France, set to more than double to 250,000 square metres by end-2026 and exceed 300,000 square metres by 2030, representing the most significant proportional supply expansion of any major European life sciences cluster in this planning cycle. Institut Paris Region and European real estate sector analysis confirms that the Paris region holds only 2.9 million square feet of existing purpose-built lab and R&D space, excluding owner-occupier premises, generating a structural shortage that has forced tenants to occupy converted light industrial buildings while awaiting purpose-built inventory from the development pipeline advancing across the Villejuif, Saclay, and Evry corridors. France's 864 biotechnology companies, which generated USD 1.7 billion in fundraising in 2024 a 39% increase from 2023 per EY and France Biotech data, represent the tenant pipeline that is pre-committing space in new developments before practical completion. The Paris Saclay Cancer Cluster received the first biocluster designation under the French government's France 2030 strategy, receiving EUR 7 billion committed to health innovation nationally and directing institutional capital into the Villejuif and Saclay corridors at a pace that will transform the Paris life sciences real estate market by 2028.

Paris's life sciences real estate market is defined by the convergence of academic excellence, hospital-adjacent research infrastructure, and an emerging institutional real estate development ecosystem. The Ile-de-France is home to Gustave Roussy, Europe's largest cancer treatment centre, the Institut Curie, the Institut Pasteur, and the Assistance Publique des Hopitaux de Paris, which collectively generate the clinical trial demand, spinout company formation, and technology transfer activity that sustains a growing ecosystem of laboratory-office tenant demand independent of the broader pharmaceutical investment cycle. AstraZeneca's USD 140 million investment in Paris-based Cellectis in 2024, following a cell therapy development collaboration established in 2023, demonstrates the in-licensing and co-investment dynamic that anchors global pharma to the Paris research ecosystem and generates on-site R&D office requirements within Ile-de-France clusters. For instance, in June 2026, Kadans Science Partner, Netherlands, officially inaugurated The Hive at Campus Grand Parc in Villejuif, France, delivering approximately 25,000 square metres of laboratory and office space as the first Kadans development in France and the first building within France's first dedicated oncology innovation hub, supported by a consortium of Paris-Saclay University, the Polytechnic Institute of Paris, Inserm, Gustave Roussy, and Sanofi, with the Ile-de-France Region awarding a EUR 1 million grant for the in-building innovation centre for early-stage startups, per Kadans Science Partner press release of June 5, 2026. These are some of the key factors driving revenue growth of the market.

However, the Paris life sciences office market faces structural constraints that moderate the pace of revenue growth despite the strength of underlying demand fundamentals. France's pharmaceutical reimbursement process, which averages 523 days between marketing authorisation and launch per the 2025 Patients W.A.I.T. Indicator by IQVIA and EFPIA, creates a commercial deterrent for global pharmaceutical companies whose French launch timelines lag Germany, Austria, and Switzerland by a significant margin, reducing the commercial motivation for large-footprint R&D office commitments in France relative to faster-access European markets. The risk that US drug price negotiations use France as a reference pricing country creates further uncertainty for global pharma companies considering major new research infrastructure commitments in the Paris region, as a low French launch price could depress global reference prices in markets that use France as a basket reference country. The venture capital base that drives early-stage lab space demand in the Paris region, while growing strongly in 2024, remains concentrated in early-stage companies requiring small-format incubator and co-working lab space rather than the 1,000 to 5,000 square metre floor plates that generate the highest revenue productivity for purpose-built campus developers. These factors substantially limit Paris life sciences office market growth over the forecast period.

Paris has the scientific infrastructure to support a world-class life sciences cluster. Gustave Roussy, Institut Curie, Institut Pasteur, and AP-HP in a single metropolitan area is an extraordinary clinical research asset base. What Paris has lacked, and is now finally acquiring, is the real estate infrastructure to translate that scientific capability into a commercially functioning cluster. The Hive inauguration in June 2026, The Mix delivering Q3 2026, and Biolabs at Hotel-Dieu targeting 2028 are not isolated projects. They are the first institutional-grade buildings in a supply pipeline that was previously non-existent. Investors who understand the Boston Kendall Square or San Francisco Mission Bay trajectories should recognise what the Paris market looks like at this stage of the cycle." Troview Intelligence Senior Analyst, Paris Life Sciences Real Estate

SEGMENT INSIGHTS

By Property Grade

Purpose-built Grade A laboratory and R&D office space is expected to account for a significantly large revenue share in the Paris life sciences office market during the forecast period.

Based on property grade, the Paris life sciences office market is segmented into Grade A purpose-built lab-office campuses, converted light industrial lab space, incubator and accelerator facilities, and owner-occupier research premises. Grade A purpose-built assets dominate revenue premium, commanding rents 30% to 45% above conventional office space in equivalent Paris locations, reflecting the BSL1 and BSL2 wet lab certification, enhanced HVAC and utilities infrastructure, biosafety compliance systems, and on-site scientific support services that purpose-built buildings provide. The converted light industrial segment is the fastest-growing supply typology in the near term, as the shortage of immediately available purpose-built space has driven tenants and developers to convert former industrial properties across the Essonne, Val-de-Marne, and southern Paris corridors into lab-enabled workspaces as a bridging solution documented by Institut Paris Region in its Ile-de-France life sciences supply analysis. Grade A assets delivered from 2025 onward, including The Hive in Villejuif and The Mix at Paris-Saclay, are establishing a new market rent benchmark that is differentiating certified sustainable lab buildings from earlier-generation converted stock.

By Sub-cluster

The Villejuif-Gustave Roussy and Paris-Saclay sub-clusters are expected to account for a significantly large revenue share in the Paris life sciences office market during the forecast period.

Based on sub-cluster, the Paris life sciences office market is segmented into Villejuif-Campus Grand Parc, Paris-Saclay plateau, Genopole-Evry, Paris south including the 13th arrondissement Biopark and Hotel-Dieu, Paris north including the Biopark area near Saint-Ouen, and other Ile-de-France locations. The Villejuif corridor anchored by Gustave Roussy is the fastest-growing sub-cluster by new supply delivery, with The Hive delivering 25,000 square metres in June 2026 and over 30,000 square metres of additional area planned by 2030 per Institut Paris Region data, benefiting from metro line 14 and Grand Paris Express line 15 connectivity providing 20-minute access to central Paris. The Paris-Saclay plateau accumulates the largest projected supply pipeline at over 50,000 square metres by 2030, with The Mix (15,000 square metres, Q3 2026), Le Central (16,000 square metres via EPA Paris-Saclay), and multiple smaller Kadans and Grow by GA buildings creating a multi-tenant research campus that serves the Servier, Danone, GSK, and Oracle corporate occupier base alongside Paris-Saclay University spinouts.

By Tenant Sector

Oncology and cell therapy research tenants are expected to account for a significantly large revenue share in the Paris life sciences office market during the forecast period.

Based on tenant sector, the Paris life sciences office market is segmented into oncology and immuno-oncology research, cell and gene therapy, genomics and bioinformatics, medical devices and diagnostics, contract research organisations, and digital health and AI-driven drug discovery. Oncology research tenants dominate the Paris-region market, anchored by the Gustave Roussy Institute's clinical research operations and the Paris Saclay Cancer Cluster's designation as France's national oncology innovation hub, which concentrates oncology-focused biotech companies, clinical stage programmes, and pharmaceutical company satellite research offices in the Villejuif corridor. Cell and gene therapy tenants are the fastest-growing segment by new lease transactions, driven by the proximity of Genopole's genomics expertise, the Institut Pasteur's gene therapy research, and Cellectis's established position in CAR-T cell therapy that has attracted AstraZeneca, Sanofi, and multiple global pharmaceutical companies as research collaborators requiring co-located Paris-region office and laboratory presence. BPI France's life sciences mandates and the French government's 42 active biotherapy production projects under the France 2030 strategy provide grant and concessional loan support that reduces the commercial risk for cell and gene therapy startups committing to Paris-region lab space.

SUB-CLUSTER ANALYSIS

Sub-cluster Deep-Dives

VILLEJUIF / CAMPUS GRAND PARC EUROPE'S PREMIER ONCOLOGY CAMPUS

| The Hive (Kadans) | 25,000 m² oncology labs + offices (Jun 2026) | Anchor Institution | Gustave Roussy (Europe's largest cancer centre) |

| Government Designation | France 2030 first bio-cluster | Transit Access | Metro 14 + Grand Paris Express Line 15 (20 min to Paris) |

Villejuif and Campus Grand Parc represent the most consequential new life sciences real estate development in continental Europe at the city level, designated as France's first bio-cluster under France 2030 and anchored by Gustave Roussy, Europe's largest cancer treatment centre. Kadans Science Partner inaugurated The Hive on June 5, 2026, delivering approximately 25,000 square metres of laboratory and office space in specialised BSL1 and BSL2 wet labs, dry labs, clean rooms, and collaborative office environments, with the Paris Saclay Cancer Cluster consortium comprising Paris-Saclay University, Polytechnic Institute of Paris, Inserm, Gustave Roussy, and Sanofi providing the academic, clinical, and industrial co-location that defines a globally competitive oncology research campus. Over 30,000 square metres of additional area is planned by 2030 in the Villejuif corridor per Institut Paris Region data, with the Sadev94 development agency, the City of Villejuif, and Grand Orly Seine Bièvre local authority developing an entirely new district around Campus Grand Parc. The metro line 14 and Grand Paris Express line 15 connectivity provides 20-minute access to central Paris per Kadans property documentation, ensuring that the campus can attract talent from across the Ile-de-France region.

| Kadans The Mix | 15,000 m² (Q3 2026 delivery) | EPA Le Central | 16,000 m² (EPA Paris-Saclay, pipeline) |

| Total Plateau Pipeline | >50,000 m² by 2030 | Anchor Corporates | Servier, Danone, Oracle, GSK |

The Paris-Saclay plateau is the largest life sciences real estate development territory in the Paris region by projected supply volume, with over 50,000 square metres of lab and R&D office area expected by 2030 per Institut Paris Region analysis, concentrated in multiple buildings from Kadans Science Partner, EPA Paris-Saclay, and Grow by GA. Kadans The Mix, a 15,000 square metre facility offering flexible BSL1 and BSL2 wet labs, dry labs, and clean rooms across four independent plots ranging from 2,000 to 3,500 square metres each, is targeting Q3 2026 delivery per Kadans property documentation, with the building designed for both startups and established corporations requiring customisable laboratory configurations. EPA Paris-Saclay is advancing Le Central, a 16,000 square metre purpose-built life sciences building under the public development agency's commercial programme, targeting corporate and institutional research tenants who require proximity to Paris-Saclay University's PhD and postdoctoral talent pipeline. Servier's primary R&D campus on the plateau, alongside Danone, Oracle, and GSK research facilities, provides the anchor corporate base that reduces leasing risk for new multi-tenant buildings entering the market at above-market rents for the Paris region.

| Established Since | Early 2000s redevelopment | Key Operator | Gecina (Biopark building owner) |

| Anchor Tenants | Cellectis, Parexel International | Character | Mixed biotech, CRO, digital health tenants |

The Biopark in Paris's 13th arrondissement is the most established inner-city life sciences hub in the Paris region, providing laboratory-enabled office space for biotechnology companies, contract research organisations, and digital health tenants within an urban setting accessible by multiple metro and RER lines from central Paris. Gecina, France's largest office REIT, pre-let the full Building E of the Biopark complex to a group of biotechnology, digital, and health companies on a nine-year lease, with existing tenants Cellectis and Parexel International anchoring the hub's identity as a combined biotech research and clinical services cluster. Cellectis, the Paris-based CAR-T cell therapy pioneer that received a USD 140 million investment from AstraZeneca in 2024, occupies Biopark space as its primary research address, demonstrating the hub's ability to retain globally significant biotech companies at inner-Paris locations rather than losing them to the suburban campus clusters. The proximity of the Biopark to the Paris Descartes medical school and Cochin Hospital creates a clinical translation environment that is particularly valuable for early-stage clinical stage companies requiring hospital site access for investigational medicinal product trials.

HOTEL-DIEU / CENTRAL PARIS EMERGING HOSPITAL-ADJACENT INNOVATION HUB

| Development | Biolabs + AP-HP + University of Paris JV | Target Capacity | ~100 startups at completion 2028 |

| Total Area | 10,000 m² healthcare innovation centre | Location | Ile de la Cité, heart of Paris |

The Hotel-Dieu life sciences innovation centre represents the most centrally located life sciences real estate development in the Paris region, developed by Biolabs in partnership with Assistance Publique-Hopitaux de Paris and the University of Paris as a 10,000 square metre healthcare innovation centre directly adjacent to the historic hospital campus on the Ile de la Cité in the heart of Paris. The centre targets approximately 100 startup companies at completion by 2028 per Choose Paris Region documentation, providing wet lab access, co-working space, and direct proximity to AP-HP's clinical research infrastructure, patient data systems, and physician-scientist community that represents an unmatched resource for early-stage companies developing diagnostics, digital therapeutics, and precision medicine applications. Google opened its first French laboratory dedicated to AI at the Institut Curie in 2024, targeting collaborations with CNRS and Institut Curie researchers, creating a model for technology company engagement with the Paris hospital research ecosystem that the Hotel-Dieu innovation centre is designed to replicate at greater scale with a diversified multi-company tenant base. The proximity to Sainte-Chapelle, the Palais de Justice, and central Paris transport connections ensures that the Hotel-Dieu centre will be able to attract talent from the full breadth of the Paris innovation economy.