| TROVIEW INTELLIGENCE | Global Colocation Data Centre Market | Q2 2026 |

| TROVIEW INTELLIGENCE · GLOBAL INTELLIGENCE REPORT |

By Geography · By Colocation Type · By Data Centre Tier · By End-User Sector

Equinix, Inc. posted 2025 revenues of USD 9.217 billion with Q4 2025 bookings increasing 42% year-on-year as 60% of its largest Q4 deals were driven by AI workloads, Digital Realty Trust reported 2025 operating revenues of USD 6.1 billion with its largest hyperscale lease in company history signed in Q1 2026, NTT Global Data Centers exceeded USD 1.80 billion in revenues in 2024 on a growth trajectory from USD 1.25 billion in 2020, and the Asia Pacific colocation market is expanding rapidly per JLL Global Data Center Market Outlook 2026 and Equinix Asia Pacific earnings a multi-year trajectory that reflects the combined pull of sovereign AI infrastructure programmes, hyperscale campus expansion, and the structural shift of enterprise workloads from owned data centres into third-party colocation facilities that provide power redundancy, carrier-neutral interconnection, and operational expertise that internal IT teams cannot replicate at equivalent cost.

| Standard License: USD 7,500 | Enterprise License: USD 10,500 |

MARKET SYNOPSIS

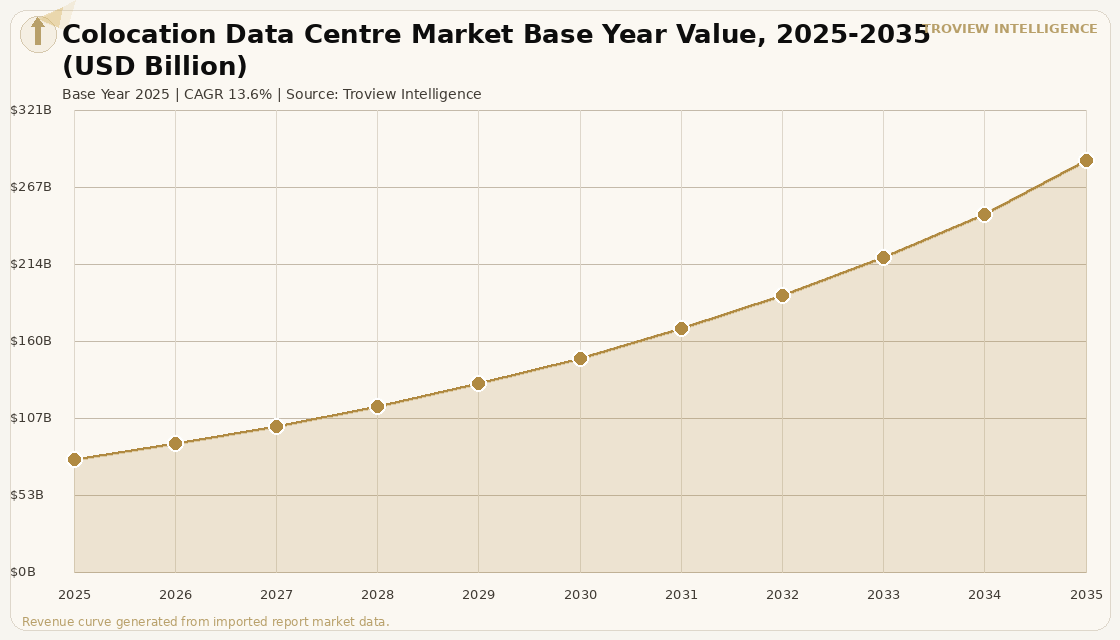

The global colocation data centre market size was USD 78.84 Billion in 2025 and is expected to register a revenue CAGR of 13.6% during the forecast period, reaching USD 286.17 Billion by 2035. Market revenue growth is supported by the accelerating conversion of enterprise IT infrastructure from owned and operated data centres to third-party colocation facilities, the expansion of hyperscale and wholesale colocation campuses driven by AI compute demand from cloud providers and AI-native operators, and the deepening of carrier-neutral interconnection ecosystems that make established colocation facilities structurally irreplaceable as tenants accumulate network relationships over time. Equinix, Inc., United States, surpassed 500,000 global interconnections in 2025, the most in the industry, and reported full-year 2025 revenues of USD 9.217 billion with operating income of USD 1.848 billion, a 39% year-on-year increase, as AI inference workloads generated 60% of its largest Q4 2025 deal volume per Equinix Q4 2025 earnings disclosures of February 2026. For instance, in January 2024, Equinix, Inc., United States, introduced its Private AI with NVIDIA offering, deploying GPU-accelerated infrastructure and liquid cooling support across more than 100 IBX colocation facilities globally, enabling AI-native enterprise tenants to access GPU compute within the interconnection density of the Equinix carrier-neutral ecosystem rather than building isolated AI infrastructure in owned facilities, per Equinix company announcement of January 2024. These are some of the key factors driving revenue growth of the market.

Digital Realty Trust, Inc., United States, reported 2025 operating revenues of USD 6.1 billion, a 10% year-on-year increase, with core funds from operations per share of USD 7.39 representing 10.1% growth year-on-year, and Q4 2025 total bookings expected to generate USD 400 million in annualised revenue covering 159.1 MW across its global colocation and hyperscale campus portfolio, with the company's PlatformDigital ecosystem spanning more than 300 data centres globally and serving over half of Fortune 500 companies per Digital Realty 2025 annual disclosures. NTT Global Data Centers, Japan, reported revenues of USD 1.80 billion in 2024, a 9.7% compound annual growth rate from USD 1.25 billion in 2020, with the company announcing new large-scale developments in India and Indonesia in June 2025 featuring direct-to-chip and immersion cooling capabilities per NTT company announcements of June 2025. Iron Mountain Inc., United States, reported full-year 2025 data centre revenues of USD 416.3 million, a year-on-year increase from its Q4 2024 quarterly data centre revenue run rate of USD 170 million, reflecting its active expansion into colocation-grade data centre real estate through new campus developments in Phoenix and Denver per Iron Mountain Q4 2025 earnings disclosures. Asia Pacific colocation is the fastest-growing colocation region globally per JLL Global Data Center Market Outlook 2026 and Equinix Asia Pacific operational disclosures, driven by Japan, Singapore, Australia, Malaysia, and Indonesia. These are some of the key factors driving revenue growth of the market.

However, the global colocation data centre market faces structural constraints that limit the pace of capacity delivery and the geographic distribution of revenue growth across the forecast period. Power availability is the binding constraint in the most demand-dense colocation markets: Northern Virginia's vacancy rate of 0.5% at year-end 2025 per CBRE H2 2025 reporting and Singapore's government-controlled capacity release under the Data Centre Call for Applications framework both reflect supply environments where operator demand cannot be accommodated regardless of capital availability. Construction costs for colocation-grade facilities reached a global average of USD 14.53 per watt in Singapore in 2025, the second highest globally after Tokyo, per Turner and Townsend 2025 data, creating a capital intensity that limits the pool of operators capable of developing new facilities at scale. Iran-US geopolitical tensions and LNG price volatility through the Strait of Hormuz, as confirmed by IMF March 2026 analysis, create upward pressure on power costs in LNG-dependent electricity markets including Japan, Singapore, and South Korea, directly affecting colocation operator margins in Asia Pacific's highest-revenue markets. The specialist technical workforce required for colocation operations power engineers, facility operators, and liquid cooling experts remains critically scarce globally, with the US data centre industry seeing a 60% increase in workforce since 2017 that has not kept pace with the acceleration of new facility delivery. These factors substantially limit global colocation data centre market growth over the forecast period.

The colocation market in 2025 is being split into two fundamentally different businesses that happen to share the same legal structure. The first is the interconnection business, where Equinix's 500,000 global connections and 11 internet exchanges in Singapore alone create a network effect that is as close to a natural monopoly as commercial real estate produces. The tenant who has 300 network relationships at Equinix SG1 is not going to move those relationships to a cheaper facility, ever. The second is the hyperscale wholesale business, where Digital Realty and QTS are competing for 50 MW to 500 MW commitments from Amazon, Microsoft, and Google on the basis of power cost, PUE, construction timeline, and substation access. These businesses require entirely different capital structures, risk profiles, and operating capabilities. Investors who treat them as the same market will systematically misprice both." Troview Intelligence Head of Global Colocation Data Centre Research

SEGMENT INSIGHTS

Four Regions Defining Global Colocation Revenue

| Market Share 2024 | Primary Markets | Vacancy H2 2025 | US Colo CAGR (est.) |

| ~39% of global colocation revenue | Northern Virginia, Chicago, Dallas, Phoenix | 1.4% primary market average (CBRE) | 12.8% to 2035 (Troview Intelligence) |

North America is the largest global colocation data centre market by revenue, capacity, and investment transaction volume, with the United States alone accounting for approximately 39% of total global colocation revenue in 2024 and with a US colocation market projected by Troview Intelligence to grow from USD 35.74 billion in 2025 at a 12.8% CAGR through 2035. The market is defined by the concentration of hyperscale campus infrastructure in Northern Virginia, which ended 2025 with 4,039.6 MW of total inventory and a 0.5% vacancy rate per CBRE H2 2025 reporting, and by the financial depth of the US data centre REIT sector, anchored by Equinix and Digital Realty's combined listed market capitalisation that provides pricing transparency and liquidity unavailable in any other global colocation market. Average monthly asking rates for 250 to 500 kW requirements across North American primary markets rose 6.5% year-on-year to USD 195.94 per kW per month in H2 2025, the fourth consecutive annual increase per CBRE, reflecting the structural supply deficit in the market's most productive zones.

| Europe Colo Market 2024 | Primary Cluster | Investment to 2030 | Growth Rate |

| USD 9.45 Billion (investment basis) | Frankfurt, London, Amsterdam, Paris, Dublin | USD 144.03 billion cumulative (W. Europe 70%) | Fastest major region by CAGR 2025 to 2030 |

Europe's colocation data centre market is concentrated in the FLAP-D cluster of Frankfurt, London, Amsterdam, Paris, and Dublin, which collectively attract the largest share of European institutional investment and hyperscale tenant demand. The European data centre colocation market attracted cumulative investment estimated at USD 144.03 billion through 2030, with Western Europe accounting for approximately 70% of regional investment and the Nordic region contributing around 20% through its competitive renewable energy access and low ambient cooling requirements per ResearchAndMarkets European colocation investment analysis. Amsterdam's moratorium on new data centre connections has permanently redirected development pressure toward Warsaw, Madrid, Zurich, and Milan, creating secondary colocation markets that are absorbing demand that the FLAP-D cluster can no longer accommodate within its existing power and planning constraints. Frankfurt's colocation market, anchored by Equinix's eight IBX facilities and Digital Realty's multi-building campus, remains the primary European financial services colocation hub and the continent's largest carrier-neutral internet exchange point by peering volume.

| APAC Colo Market 2025 | APAC Colo Market 2030 | Key Growth Markets | Constraint |

| USD 29.56 Billion | USD 68.47 Billion | Japan, Singapore, India, Malaysia, Indonesia | Power grid, land scarcity, Singapore CFA quota |

Asia Pacific is the fastest-growing colocation data centre region globally, expanding from USD 29.56 billion in 2025 toward USD 68.47 billion by 2030 per JLL Global Data Center Market Outlook 2026 and Equinix Asia Pacific earnings disclosures, driven by sovereign AI infrastructure mandates, hyperscale campus expansion in Japan and Australia, and the emergence of Malaysia and Indonesia as cost-competitive overflow markets for capacity constrained by Singapore's CFA framework. Japan's colocation market benefits from a combination of dense enterprise demand from domestic corporations, government-mandated data localisation requirements, and hyperscale investment from global cloud providers serving the broader North Asia region, with Digital Realty's NRT campus expansion in May 2024 incorporating higher-density racks and renewable power sources targeting AI-ready colocation demand. By June 2025, NTT Global Data Centers had announced new large-scale colocation developments in India and Indonesia featuring direct-to-chip and immersion cooling per NTT company announcements, reflecting the acceleration of high-density colocation supply in markets where data centre infrastructure is being built for the first time at hyperscale quality standards.