| TROVIEW INTELLIGENCE | Global Data Centre Real Estate Market | Q2 2026 |

| TROVIEW INTELLIGENCE · GLOBAL INTELLIGENCE REPORT |

By Geography · By Asset Type · By Data Centre Tier · By End-User Sector

Global data centre real estate investment surpassed USD 60 billion in 2024 per JLL reporting and is projected to grow by a further 20% in 2025, driven by an infrastructure investment supercycle that JLL estimates will require up to USD 3 trillion by 2030 as global data centre capacity doubles from 100 GW to 200 GW between 2025 and 2030, with Equinix posting 2025 revenues of USD 9.217 billion and record capacity delivery of 23,250 racks and more than 90 MW of xScale capacity, Digital Realty recording operating revenues of USD 6.1 billion for 2025 with core FFO per share growth of 10.1% year-on-year, and data centres accounting for nearly a third of total global real estate investment in 2025 per Colliers a share that did not exist as a category a decade ago.

| Standard License: USD 7,500 | Enterprise License: USD 10,500 |

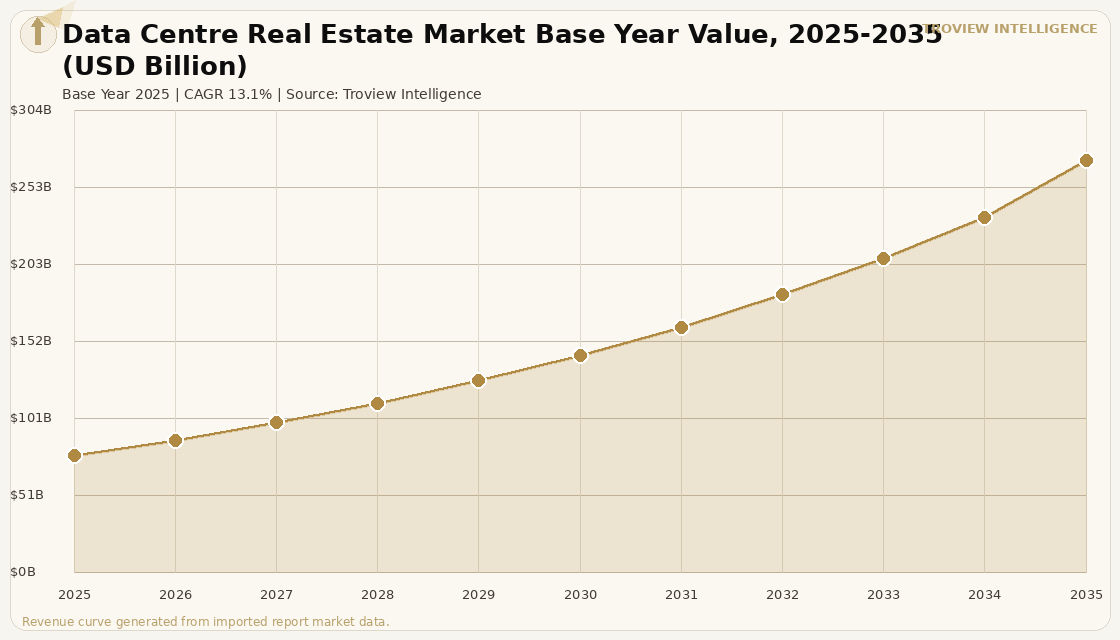

MARKET SYNOPSIS

The global data centre real estate market size was USD 77.32 Billion in 2025 and is expected to register a revenue CAGR of 13.1% during the forecast period, reaching USD 271.48 Billion by 2035. Market revenue growth is supported by the accelerating transition of global computing workloads toward AI inference, cloud hyperscale expansion, and sovereign digital infrastructure programmes that are collectively driving demand for purpose-built, power-dense real estate at a pace that utility grids, planning systems, and construction supply chains are struggling to match. JLL's 2026 Global Data Center Market Outlook projects that the sector will increase by 97 GW between 2025 and 2030, effectively doubling in size over a five-year period, requiring up to USD 3 trillion in cumulative investment across real estate, mechanical, electrical, and IT infrastructure. Equinix, Inc., United States, reported 2025 revenues of USD 9.217 billion, a 5% increase year-on-year, with record capacity delivery of 23,250 racks and more than 90 MW of xScale capacity, while its Q4 2025 bookings increased 42% year-on-year, with 60% of its largest deals in Q4 driven by AI workloads per Equinix earnings disclosures of February 2026. For instance, in April 2024, Equinix, Inc., United States, and PGIM Real Estate, United States, entered a USD 600 million joint venture to develop and operate SV12x, the first xScale data centre in the United States in Silicon Valley, providing over 28 MW of power capacity and targeting hyperscale and AI compute tenants requiring single-building deployments above the standard colocation format. These are some of the key factors driving revenue growth of the market.

Digital Realty Trust, Inc., United States, reported operating revenues of USD 6.1 billion for 2025, a 10% increase year-on-year, with core FFO per share of USD 7.39, a 10.1% increase year-on-year, and Q4 2025 total bookings expected to generate USD 400 million in revenue covering 159.1 MW, with the Manassas, Virginia location identified as the top contributor to above-1 MW signings in Q4 per Digital Realty earnings disclosures of February 2026. Data centres accounted for nearly a third of total global real estate investment in 2025 per Colliers research of January 2026, displacing traditional real estate pillars including industrial, logistics, and office sectors as the primary destination for institutional capital in commercial real estate. CBRE's North America Data Center Trends H2 2025 report records primary market net absorption of 2,497.6 MW in 2025, surpassing the prior record of 1,809.5 MW set in 2024, with average monthly asking rates for 250 to 500 kW requirements rising 6.5% year-on-year to USD 195.94 per kW per month the fourth consecutive annual increase. North America accounts for the largest share of global data centre real estate revenue, with Northern Virginia alone delivering more than 1 GW of new capacity in 2025 and reaching 4,039.6 MW of total inventory per CBRE H2 2025. These are some of the key factors driving revenue growth of the market.

However, the global data centre real estate market faces structural constraints that temper the pace and geographic distribution of growth even as demand signals remain at record levels. Power grid capacity is the binding constraint in the most active development markets: Dominion Energy's batching system in Northern Virginia has extended power delivery timelines for new data centre projects, limiting the conversion rate of permitted developments into operational capacity, while utility upgrade lead times of three to five years in constrained markets such as Silicon Valley, Amsterdam, and Singapore extend financial returns timelines for developers and investors. Iran-US geopolitical tensions and resulting energy price volatility through the Strait of Hormuz, which handles approximately 20% of global seaborne LNG per IMF March 2026 confirmation, create upward cost pressure on data centre power costs in markets with LNG-dependent electricity generation, including Japan, South Korea, and parts of Southeast Asia. Construction cost inflation for power-dense facilities capable of supporting high-density compute racks above 30 kW per rack remains elevated, as specialist mechanical, electrical, and cooling contractors face order backlogs extending to 12 to 18 months for liquid cooling system installations. These factors substantially limit global data centre real estate market growth over the forecast period.

The data centre sector has absorbed a larger share of global real estate investment capital faster than any prior asset class transition, including the shift to logistics in 2012 to 2018. The reason is structural, not cyclical. Every AI model deployed at scale creates permanent inference demand that grows with user adoption, and inference requires geographically distributed, low-latency, power-dense infrastructure that cannot be retrofitted from legacy office buildings or warehouse shells. Investors who understand this are not buying data centre real estate for the yield. They are buying it for the irreplaceability of the asset once it is powered and connected. A colocation campus in Ashburn with 100 MW of contracted hyperscale capacity and a 25-year Dominion Energy interconnection agreement is not a real estate asset. It is a piece of the AI economy's physical foundation, and the number of sites that can credibly claim that description is finite." Troview Intelligence Head of Global Data Centre Real Estate Research

SEGMENT INSIGHTS

Four Regions Defining Global Data Centre Real Estate

| Primary Market Supply H2 2025 | 2025 Net Absorption | Avg Asking Rate 250-500 kW | Primary Market Vacancy H2 2025 |

| 9,432 MW (+36% YoY) | 2,497.6 MW (record) | USD 195.94/kW/month | 1.4% (record low) |

North America is the largest data centre real estate market globally by every primary metric: total installed capacity, net absorption, investment transaction volume, and number of operational facilities. CBRE's H2 2025 North America Data Center Trends report records primary market supply at 9,432 MW across eight primary markets including Northern Virginia, Atlanta, Dallas, Chicago, Phoenix, Silicon Valley, Hillsboro, and the New York tri-state area, with a 36% year-on-year increase in inventory driven by hyperscale and AI demand. Northern Virginia alone delivered more than 1 GW of new capacity in 2025 and ended the year with 4,039.6 MW of total inventory, nearly 3.5 times the combined inventory of all secondary US data centre markets per CBRE research. The vacancy rate across primary North American markets fell to a record low of 1.4% at year-end 2025, with Northern Virginia recording 0.5% vacancy, reflecting a supply pipeline that cannot keep pace with contracted demand regardless of the pace of new construction.

| Primary Markets | EMEA Growth | Key Constraints | Investment Profile |

| Frankfurt, London, Amsterdam, Paris, Dublin | Fastest-growing sub-region for new supply | Power grid capacity, planning restrictions | Germany, Netherlands top EMEA volumes |

Europe's data centre real estate market is concentrated in the FLAP-D cluster of Frankfurt, London, Amsterdam, Paris, and Dublin, which collectively account for the majority of European institutional-grade data centre real estate investment. Colliers EMEA data centre capital markets analysis of January 2026 identifies Germany and the Netherlands as the top EMEA investment markets by volume in 2025, with the Frankfurt campus ecosystem anchored by Equinix's eight operational IBX facilities and Digital Realty's multi-building campus in the city's data centre corridor. Power grid access is the primary constraint on European data centre development, with Amsterdam imposing a moratorium on new data centre connections in 2023 that has permanently shifted development pressure to secondary EMEA markets including Warsaw, Madrid, Zurich, and Milan. Ireland's favourable corporate tax environment and renewable energy infrastructure continue to make Dublin the destination of choice for hyperscale European deployments by US cloud providers.

| Primary Hubs | Growth Markets | Hyperscaler Commitment | Sovereign AI Driver |

| Singapore, Tokyo, Sydney, Hong Kong | Malaysia, Indonesia, India, South Korea | USD 50B Amazon AWS US Gov AI, 2025 | National AI infrastructure mandates |

Asia Pacific is the fastest-growing data centre real estate region, driven by sovereign cloud mandates, hyperscale expansion in Japan and Australia, and the emergence of Malaysia and Indonesia as cost-competitive alternatives to capacity-constrained Singapore. In November 2025, Amazon Web Services, United States, announced a USD 50 billion data centre investment to power US government AI infrastructure, underscoring the scale of hyperscale capital commitments that are reshaping data centre real estate pipelines globally and producing secondary demand in Asia Pacific from government-linked cloud platforms that mirror US federal cloud procurement strategies. Singapore's data centre moratorium, partially lifted in 2022 with a managed approvals process, continues to restrict new supply in the city-state and is redirecting hyperscale demand to Johor Bahru in Malaysia, which has absorbed more than 3 GW of committed hyperscale capacity in 2024 and 2025 from Amazon, Microsoft, and Google per verified company announcements.