By Geography · By Mall Format · By Tenant Mix · By Revenue Model

Simon Property Group accumulated USD 4.8 billion in real estate funds from operations in 2025, signed 4,600 leases for more than 17 million square feet, recorded retail sales per square foot growth of 8.1%, and held occupancy above 96.4% as Dubai Mall maintained its position as the most visited place on earth for two consecutive years with 111 million visitors in 2024 and Emaar committed AED 1.5 billion to expand it with 279 new luxury outlets, confirming that the regional mall format is not dying but bifurcating into irreplaceable destination assets that outperform and undifferentiated B-class stock that continues to structurally decline.

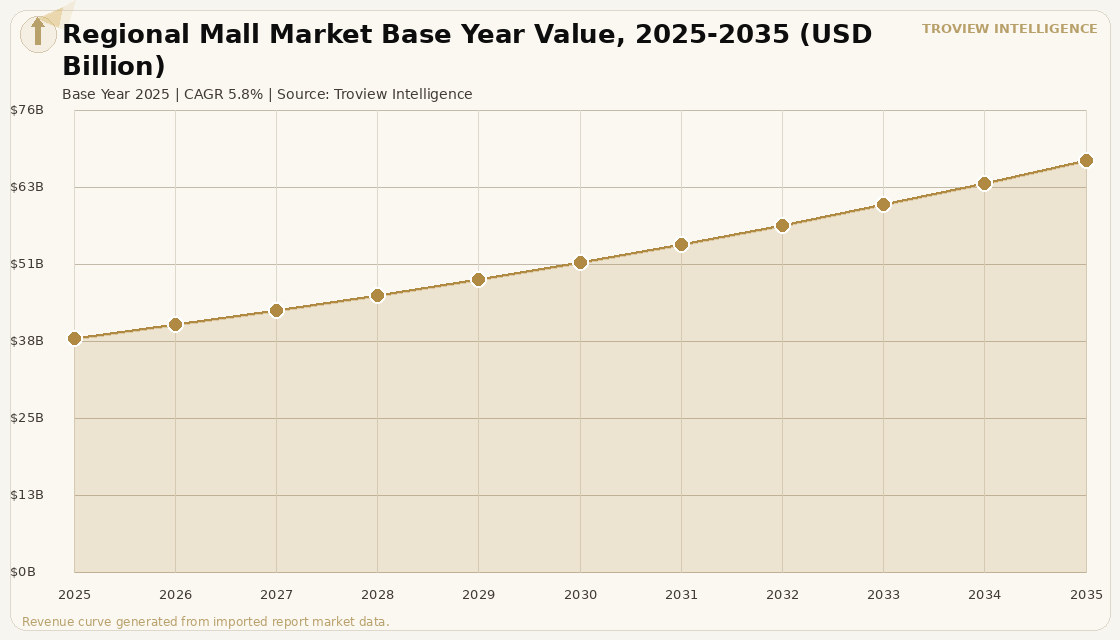

MARKET SYNOPSIS

The global regional mall market size was USD 38.48 Billion in 2025 and is expected to register a revenue CAGR of 5.8% during the forecast period, reaching USD 67.70 Billion by 2035. The global regional mall market encompasses the rental, operational, and ancillary revenues generated by large-format enclosed shopping centres typically exceeding 400,000 square feet of gross leasable area and anchored by department stores, hypermarkets, entertainment venues, or experiential attractions. Simon Property Group, the world's largest mall owner with ownership interests in more than 250 retail properties comprising 191 million square feet across North America, Europe, and Asia, accumulated USD 4.8 billion in real estate funds from operations in 2025 per Simon Property Group investor disclosures, signed 4,600 leases covering more than 17 million square feet, and achieved occupancy of 96.4% across its malls and outlet portfolio. Retail sales per square foot in Simon's portfolio grew 8.1% in 2025 versus 2024, confirming that the top tier of US regional mall assets is generating strong per-unit retail productivity even as the national class average is weighed down by lower-performing centres. Dubai Mall maintained its position as the most visited place on earth for two consecutive years with 111 million visitors in 2024, a 6% increase year-on-year, per Emaar Properties investor announcements.

The global regional mall market is bifurcating between irreplaceable destination assets that consistently outperform and undifferentiated secondary stock where structural vacancy is rising as e-commerce claims the routine purchase occasions that previously required a physical retail visit. Unibail-Rodamco-Westfield, the global mall operator positioned across 27 retail markets and cities worldwide with properties attracting 1.2 billion visits annually, has been pursuing a strategy of monetising its US portfolio while concentrating capital in European flagship assets, using a 10,300-square-foot ultra-luxury conference suite at Caesar's Palace Las Vegas for retailer meetings at the ICSC Las Vegas convention in 2025 rather than competing for floor space at the main convention hall, per CoStar reporting of June 2025. Majid Al Futtaim, the leading mall operator across the Middle East, Africa, and Asia, launched an AED 5 billion transformation of Mall of the Emirates in April 2025 to add 20,000 square metres of retail space, 100 new stores, a new wellness club, and a 600-seat theatre as part of its 20th anniversary redevelopment, per Majid Al Futtaim company press release. For instance, in May 2025, Emaar Properties, UAE, unveiled The District at Dubai Mall, the first phase of the AED 1.5 billion expansion introducing 279 new luxury outlets including 198 retail units and 81 food and beverage concepts, cementing Dubai Mall's position as the most visited place on earth and confirming the sustained institutional commitment to the largest regional mall formats that combine retail with destination entertainment, per Emaar Properties press release of May 2025. These are some of the key factors driving revenue growth of the market.

However, the global regional mall market faces structural constraints. E-commerce penetration of total retail sales, at 23.2% of US retail excluding autos and gasoline in Q3 2024, continues to expand, with Prologis projecting the share to reach 25% by year-end 2025 per US Census Bureau retail trade data, permanently reducing the addressable volume for physical retail in the categories most susceptible to online substitution. Secondary and tertiary regional malls, defined as those not in the top quartile of sales productivity, face accelerating vacancy as anchor department stores continue to close locations more than 1,500 US department stores have closed since 2017 per industry estimates leaving large anchor boxes vacant and reducing the co-tenancy that drives foot traffic to in-line retailers. The capital expenditure required to reposition regional malls from traditional retail formats to mixed-use destinations including residential, healthcare, hospitality, and entertainment has placed significant refinancing pressure on owners of lower-performing assets whose debt was underwritten on retail income that is no longer achievable. These factors substantially limit global regional mall market growth over the forecast period.

The regional mall market ended the 2020s as two completely different industries sharing one real estate classification. The top quartile Simon's Class A portfolio at 96% occupancy and 8% sales per square foot growth, Dubai Mall at 111 million visitors, Westfield London at 24 million annual visitors is not in the retail apocalypse. It never was. These are tourism destinations with retail attached. The bottom half of the global mall inventory is a different story: department store closures, rising vacancy, and capital structures built on rental incomes that e-commerce has permanently reduced. The investment thesis for regional malls requires being very explicit about which category you are buying." Troview Intelligence Head of Global Regional Mall Research

SEGMENT INSIGHTS

By Geography

North America and the Middle East are expected to account for a significantly large revenue share in the global regional mall market during the forecast period.

Based on geography, the global regional mall market is segmented into North America, Middle East, Asia Pacific, and Europe. North America is the largest revenue market, anchored by Simon Property Group's 191 million square foot portfolio and the Macerich and Brookfield Properties REIT platforms that collectively control the majority of US institutional regional mall income. The Middle East is expected to register the fastest revenue CAGR over the forecast period, driven by the Dubai and Riyadh mall markets where tourist-driven footfall, near-zero e-commerce substitution of experiential retail, and sustained expansion investment sustain occupancy rates of 97 to 98%. Asia Pacific's regional mall market is growing across Singapore, South Korea, Malaysia, and India, where rapid urbanisation and a growing middle class are driving new mall development. Europe's mall market is led by Unibail-Rodamco-Westfield's flagship portfolio and national REIT platforms in France, Germany, and the Netherlands, with the UK market navigating significant structural headwinds from e-commerce penetration.

By Mall Format

Super-regional malls above 800,000 square feet are expected to account for a significantly large revenue share in the global regional mall market during the forecast period.

Based on mall format, the global regional mall market is segmented into super-regional malls above 800,000 square feet, regional malls between 400,000 and 800,000 square feet, and specialist large-format retail destinations. Super-regional malls dominate institutional investment value and per-asset revenue, with Dubai Mall at 13 million square feet and 1.2 million square metres of gross area, Westfield London at 2.54 million square feet hosting 450 retail outlets and 24 million annual visitors, and King of Prussia in Philadelphia as Simon's largest US asset. Super-regional mall formats generate the highest experiential draw, combining traditional retail with destination entertainment including ice rinks, aquariums, ski slopes, cinemas, and luxury dining precincts that cannot be replicated online. Standard regional malls between 400,000 and 800,000 square feet are the most vulnerable format, lacking the experiential depth of super-regionals while facing the same anchor closures and e-commerce competition.

By Tenant Mix

Luxury and premium retail tenants are expected to account for a significantly large and growing revenue share in the global regional mall market during the forecast period.

Based on tenant mix, the global regional mall market is segmented by the proportion of luxury and premium, mid-market fashion, food and beverage, entertainment, health and wellness, and anchor department stores. Luxury and premium retail is the fastest-growing tenant segment, as global luxury brands continue to establish flagship stores in premium destinations and the structural insulation of luxury spending from e-commerce competition sustains rent-paying capacity above inflation. Dubai Mall's Fashion Avenue, Simon Property Group's luxury positioning in its top-tier centres, and Majid Al Futtaim's first-to-market luxury launches at Mall of the Emirates confirm the tenant mix shift toward luxury anchors that generate the footfall and per-square-foot productivity that justify premium mall rents. Food and beverage has grown from 15% to 25% of tenant mix in top-tier global malls over the past decade, as dining and social experience have replaced routine shopping as the primary reasons consumers visit destination retail centres.

REGIONAL ANALYSIS

NORTH AMERICA BIFURCATED

| Simon Property FFO 2025 | USD 4.8 billion (Simon Property Group investor disclosures) | Simon Occupancy | 96.4% (year-end 2025) |

| SPF Sales Growth | 8.1% retail sales per sq ft growth vs 2024 | URW US Strategy | Seeking residential redevelopment partners for US assets |

North America's regional mall market is defined by the widening gap between Class A destinations that are outperforming pre-pandemic benchmarks and secondary stock that continues to lose anchor tenants and footfall. Simon Property Group's USD 4.8 billion in FFO, 96.4% occupancy, and 4,600 new leases across 17 million square feet in 2025 confirm that America's premier mall portfolio is generating operating metrics that many other real estate sectors cannot match. Unibail-Rodamco-Westfield is on the other side of that strategy, seeking residential redevelopment partners for its Westfield Montgomery mall in Maryland and signalling a broader US divestment posture through its ICSC Las Vegas meeting format in 2025. The divergence between Simon doubling down on Class A retail and URW monetising its US position to concentrate in European flagships represents the clearest institutional expression of the global mall bifurcation thesis.

MIDDLE EAST

| Dubai Mall Footfall 2024 | 111 million visitors (Emaar, 6% YoY growth) | Mall of Emirates Occupancy | 98% (H1 2025, Majid Al Futtaim) |

| UAE Super-Regional Rents | AED 350-450/sq ft/year (+14.9% YoY in prime locations) | Dubai Retail Sales Q3 2025 | AED 1.1 billion transaction value (first time above AED 1B in a quarter) |

The Middle East is the global regional mall market's fastest-growing region, anchored by Dubai's two flagship super-regional malls Dubai Mall and Mall of the Emirates that together serve as the defining proof point for the destination mall model globally. Dubai Mall held its position as the most visited place on earth in 2024 for the second consecutive year with 111 million visitors, and Emaar committed AED 1.5 billion to expand it with 279 new outlets in The District precinct. Majid Al Futtaim simultaneously committed AED 5 billion to transform Mall of the Emirates, adding 20,000 square metres of retail, a 600-seat theatre, and a new wellness club. UAE super-regional mall rents rose 14.9% year-on-year to AED 350 to 450 per square foot per year in prime locations, and both Emaar and Majid Al Futtaim maintained 98% occupancy across their Dubai mall portfolios in Q3 2025.

ASIA PACIFIC GROWTH

| Malaysia Mid Valley Megamall | 1.82 million sq ft, 509 tenants, near 100% occupancy | Singapore | Occupancy rates 97-99% at prime Orchard Road centres |

| India | Large-format mall development accelerating in Tier 1 and New Tier 1 cities | Japan J-REIT | Retail REITs delivered 116% 5-year investor return per NAREIT data |

Asia Pacific's regional mall market is growing across multiple development cycles: Japan's mature J-REIT retail portfolio, South Korea and Singapore's high-occupancy prime urban malls, and India's first-generation large-format mall expansion in Mumbai, Delhi NCR, and Bengaluru. Malaysia's IGB REIT owns Mid Valley Megamall, the country's largest retail mall at 1.82 million square feet with 509 tenants and near-100% occupancy, attracting 3.5 million monthly visitors per REIT investor disclosures. Singapore's Orchard Road prime mall corridor maintains 97 to 99% occupancy at its top-tier centres including ION Orchard and Ngee Ann City, supported by Singapore's role as Southeast Asia's primary luxury retail and tourism destination. India's mall development pipeline is accelerating, with Phoenix Mills, DLF, and Prestige Group expanding large-format retail destinations in cities where the organised retail penetration is still below 10%.