By Government Tier · By Geography · By Property Grade · By Occupier Function

The US General Services Administration manages over 8,100 owned and leased assets covering 377.9 million square feet of workspace for more than one million federal workers a portfolio carrying a USD 340 billion maintenance and repair backlog by fiscal 2024 per the Government Accountability Office while the DOGE-driven disposal programme shed 90 GSA-owned properties and 3 million square feet in fiscal 2025, and South Korea advances its second phase of public institution relocation from Seoul to Sejong City and provincial hubs as the Lee Jae Myung administration targets balanced national development through Five Mega-Regions infrastructure spending.

MARKET SYNOPSIS

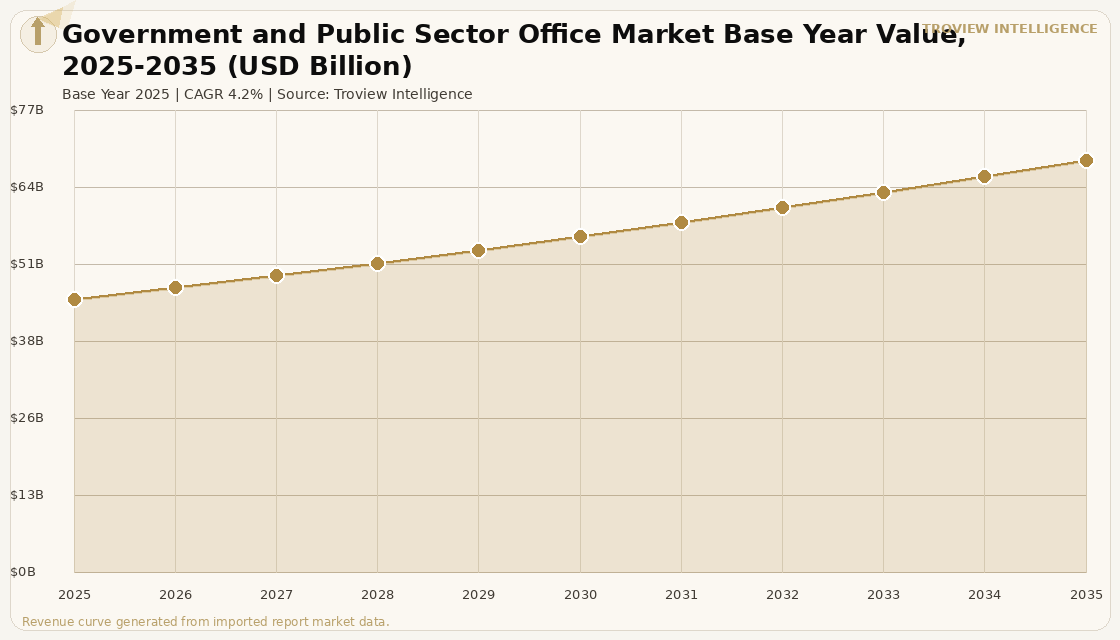

The global government and public sector office market size was USD 45.62 Billion in 2025 and is expected to register a revenue CAGR of 4.2% during the forecast period, reaching USD 68.70 Billion by 2035. Market revenue growth is supported by the sustained expansion of government office infrastructure in Asia Pacific, the modernisation of public sector workspace across Europe under national net-zero building mandates, and the construction of new administrative capitals in South Korea, Indonesia, and Egypt that are generating multi-billion-dollar government campus development programmes. The US General Services Administration manages the world's single largest government real estate portfolio, comprising over 8,100 owned and leased assets covering 377.9 million square feet of workspace for more than one million federal workers across more than 9,000 properties per the GSA's fiscal 2024 annual performance report. The Government Accountability Office placed federal real estate on its list of high-risk federal programmes, citing a maintenance and repair backlog that more than doubled between fiscal 2017 and fiscal 2024, from USD 170 billion to USD 340 billion, confirming the scale of reinvestment required across ageing federal office infrastructure even as the current US administration pursues footprint reduction. Asia Pacific governments are the primary growth engine for the global public sector office market, with South Korea's Ministry of Land, Infrastructure and Transport advancing the second phase of public institution relocation from Seoul to provincial hubs and new administrative centres under the Lee Jae Myung administration's Five Mega-Regions balanced development strategy.

Global government and public sector office demand is shaped by three competing forces: footprint consolidation and cost reduction in fiscally constrained Western governments, new capital construction and regional decentralisation in Asia Pacific, and mandatory green building upgrades driven by net-zero and energy performance legislation across the European Union. The US Congress passed new legislation in January 2025 requiring all government agencies to report occupancy data annually, with agencies occupying less than 60% of their space required to take corrective action or face reduced future footprint allocations, per the signed law reported by Federal News Network. The GSA disposed of 90 federal properties in fiscal 2025, eliminating 3 million square feet from the government portfolio, and identified 45 further properties for accelerated disposal, with the agency estimating potential savings of USD 60 billion over a decade by shedding up to 30% of its leased and owned office space. For instance, in fiscal 2025, the Court Services and Offender Supervision Agency in Washington DC executed a 20-year lease for 198,000 rentable square feet at 501 3rd Street NW, valued at USD 178 million, in one of the largest GSA transactions in the National Capital Region, per Lincoln Government Services Group documentation, demonstrating that even in a period of overall footprint reduction, major government tenants continue to commit to long-duration leases in modernised buildings. These are some of the key factors driving revenue growth of the market.

However, the global government and public sector office market faces structural constraints that moderate the pace of revenue growth. The US federal real estate portfolio carries a USD 340 billion maintenance and repair backlog per the GAO, and approximately 23 million square feet of office space have been officially designated as underutilised nationwide, creating disposal and consolidation pressure that will reduce total government-leased square footage and associated rental revenue in North America over the forecast period. The GSA's workforce was reduced by approximately 45% under the Trump administration, impairing the agency's ability to execute consolidation projects and lease negotiations at the pace required to realise the projected USD 60 billion in savings, per testimony by GSA's acting Public Buildings Service Commissioner to the House Transportation and Infrastructure Committee. The structural shift toward hybrid and remote work patterns within public sector workforces, codified by the January 2025 legislation requiring occupancy reporting, will reduce per-employee space allocations in government leases over the forecast period as agencies renegotiate expiring leases on terms reflecting post-pandemic utilisation data. Approximately 50% of all GSA leases are expiring within a five-year window, creating a concentration of lease renegotiation risk that may result in footprint reductions across multiple agencies simultaneously. These factors substantially limit global government and public sector office market growth over the forecast period.

The global government office market is simultaneously the most stable and the most structurally challenged segment of commercial real estate. Stable because sovereign tenants do not default, do not go bankrupt, and do not exit their leases without paying the credit quality of a government tenant is unmatched in the investment-grade market. Structurally challenged because Western governments, particularly the United States, are sitting on portfolios that were designed for a pre-hybrid, pre-digital workforce occupying 100% of their desks every day. The USD 340 billion GSA maintenance backlog and the 23 million square feet of officially designated underutilised space are not abstractions they are liabilities on the balance sheet of the world's largest office landlord. Meanwhile, South Korea's second phase of public institution relocation and Indonesia's Nusantara capital construction are building the government office campuses of the 2030s from the ground up." Troview Intelligence Head of Global Government Real Estate Research

SEGMENT INSIGHTS

By Government Tier

National and federal government office occupiers are expected to account for a significantly large revenue share in the global government and public sector office market during the forecast period.

Based on government tier, the global government and public sector office market is segmented into national and federal government occupiers, state and provincial government occupiers, municipal and local authority occupiers, and international and intergovernmental organisation occupiers. National and federal governments dominate market revenue, anchored by the US federal estate of 377.9 million square feet managed by the GSA, the UK Government Property Agency's central estate, France's Direction de l'Immobilier de l'Etat, and the consolidated government campuses of Singapore, South Korea, and Japan. State and provincial governments represent the fastest-growing segment in Asia Pacific, as decentralisation policies in Indonesia, India, and South Korea direct government employment and office construction to sub-national capitals and regional administrative hubs. The UK Government Property Agency has consolidated central government office holdings into an owned estate strategy focused on 22 Government Hubs across the United Kingdom, reducing private sector lease costs while delivering modern, energy-compliant workspace for civil servants.

By Geography

North America is expected to account for a significantly large revenue share in the global government and public sector office market, while Asia Pacific is expected to register the fastest revenue CAGR during the forecast period.

Based on geography, the global government and public sector office market is segmented into North America, Europe, Asia Pacific, and Middle East and Africa. North America retains the largest share of government office market revenue, underpinned by the scale and lease obligations of the US federal estate and Canadian federal property holdings. The US GSA manages a portfolio covering more than 377.9 million square feet, with agencies spending approximately USD 2 billion annually to operate and maintain federal office buildings exclusive of lease payments per GSA congressional testimony. Asia Pacific is expected to register the fastest revenue CAGR over the forecast period, driven by South Korea's second phase of public institution relocation to Sejong City and provincial hubs, Indonesia's Nusantara capital construction programme, and India's continued expansion of central secretariat and state government office infrastructure under the PM Gati Shakti National Master Plan.

By Property Grade

Owned and purpose-built government office buildings are expected to account for a significantly large revenue share in the global government and public sector office market during the forecast period.

Based on property grade, the global government and public sector office market is segmented into purpose-built government campuses and owned estate, Grade A leased commercial office buildings occupied by government agencies, and legacy government buildings requiring refurbishment or disposal. Purpose-built government campuses dominate market revenue and asset value, including Sejong City's Government Complex in South Korea which consolidated 42 central administrative agencies from Seoul and Washington DC's federal triangle of owned GSA-managed buildings anchoring the National Capital Region government estate. Grade A leased commercial office buildings occupied by government agencies represent the fastest-growing segment by new transaction volume, as governments in Australia, Canada, and the United Kingdom increasingly favour long-term leases in privately owned commercial buildings over owning and maintaining bespoke government facilities. Legacy government buildings represent the largest near-term disposal and conversion opportunity, with 47% of Seoul's major business district office buildings over 30 years old per the Ministry of Land, Infrastructure and Transport's Seumter administrative platform data.

REGIONAL ANALYSIS

NORTH AMERICA LARGEST

| GSA Portfolio Size | 377.9M sq ft, 8,100+ assets | Underutilised Space (US) | 23M sq ft designated |

| Maintenance Backlog (GAO) | USD 340 Billion (FY2024) | DOGE Disposal FY2025 | 90 properties, 3M sq ft eliminated |

North America is the largest government and public sector office market globally, dominated by the US federal real estate portfolio managed by the GSA, which provides workspace for more than one million federal workers across more than 9,000 properties covering 377.9 million square feet per the GSA's fiscal 2024 annual performance report. The US federal office portfolio is undergoing its most significant restructuring in decades, driven by the DOGE efficiency programme, the January 2025 occupancy reporting legislation, and the GSA's stated target of shedding up to 30% of leased and owned office space to generate an estimated USD 60 billion in savings over a decade. In fiscal 2025, GSA disposed of 90 owned properties eliminating 3 million square feet and identified 45 further properties for accelerated disposal per testimony to the House Transportation and Infrastructure Committee. The GAO's designation of federal real estate as a high-risk programme, citing a maintenance backlog that reached USD 340 billion in fiscal 2024, confirms the urgency of the consolidation and disposal agenda. Canada's federal government, managed through Public Services and Procurement Canada, is similarly rationalising its office footprint following pandemic-driven hybrid work adoption, with the Treasury Board of Canada Secretariat establishing the GCworkplace standard requiring agencies to demonstrate consistent occupancy justification for all retained leased space.

EUROPE NET-ZERO RETROFIT

| UK Government Hubs Strategy | 22 Government Hubs (Government Property Agency) | EU EPC Band B Requirement | All commercial buildings by 2030 |

| Key Markets | United Kingdom, France, Germany, Netherlands | French Central Estate Manager | Direction de l'Immobilier de l'Etat (DIE) |

Europe's government and public sector office market is entering a mandated investment cycle as EU Energy Performance of Buildings Directive requirements demand that all commercial properties reach EPC Band B by 2030, compelling governments holding legacy built estate to accelerate refurbishment or disposal. The United Kingdom's Government Property Agency has consolidated central government office holdings into a 22-hub strategy across England, Wales, and Scotland, with hubs providing modern, shared workspace that reduces per-agency private sector lease costs while delivering BREEAM-rated buildings meeting the net-zero transition requirements of the UK's Climate Change Act. France's Direction de l'Immobilier de l'Etat manages central government property and has implemented asset sales and lease rationalisation programmes that reduced the state office portfolio area while reinvesting proceeds into higher-specification retained buildings. Germany's federal government office portfolio, managed through the Federal Authority for Real Estate Tasks, includes the Berlin government district buildings and the distributed federal ministry estate across Bonn, and faces mandatory energy performance upgrades under the German Building Energy Act that will require significant capital investment over the forecast period.

ASIA PACIFIC FASTEST-GROWING

| South Korea 2nd Phase Relocation | 42+ agencies, Sejong City and provinces | Indonesia | Nusantara capital construction programme |

| South Korea Govt Infrastructure Plan | USD 190 Billion investment commitment | Key Markets | South Korea, Japan, Singapore, India, Indonesia |

Asia Pacific is the fastest-growing global government office market, driven by South Korea's second phase of public institution relocation from Seoul, Indonesia's Nusantara new capital construction, India's central secretariat expansion, and Singapore's sustained investment in smart government campus infrastructure. South Korea's Ministry of Land, Infrastructure and Transport, under the Lee Jae Myung administration, is pursuing a Five Mega-Regions balanced development strategy that includes developing Sejong as the undisputed administrative capital and accelerating the second phase of public institution relocation to the provinces, which will generate sustained demand for new government office construction outside Seoul through the forecast period. Indonesia's Nusantara capital construction programme, the most ambitious government office development project in Southeast Asia, is delivering presidential palace, ministries, and government department buildings on the island of Borneo, representing a multi-decade programme of public sector office construction. The South Korean government has committed to approximately USD 190 billion in infrastructure investment focused on transportation, utilities, and public facilities per industry analysis of Korean government capital programmes, with government office construction representing a component of this broader infrastructure commitment.