By City · By Mall Format · By Developer · By Luxury Segment

City Spotlights: Mumbai · Delhi · Bengaluru · Hyderabad

India has only three genuine luxury malls DLF Emporio and DLF Chanakya in Delhi, and Jio World Plaza in Mumbai yet ranks fourth globally in individuals with net assets exceeding USD 100 million, with DLF's luxury mall management team confirming that international parent companies of LVMH, Kering, and Richemont brands are actively requesting additional space and more than a dozen prominent brands are prepared to enter India immediately if retail space became available making India the world's most supply-constrained luxury retail real estate market.

MARKET SYNOPSIS

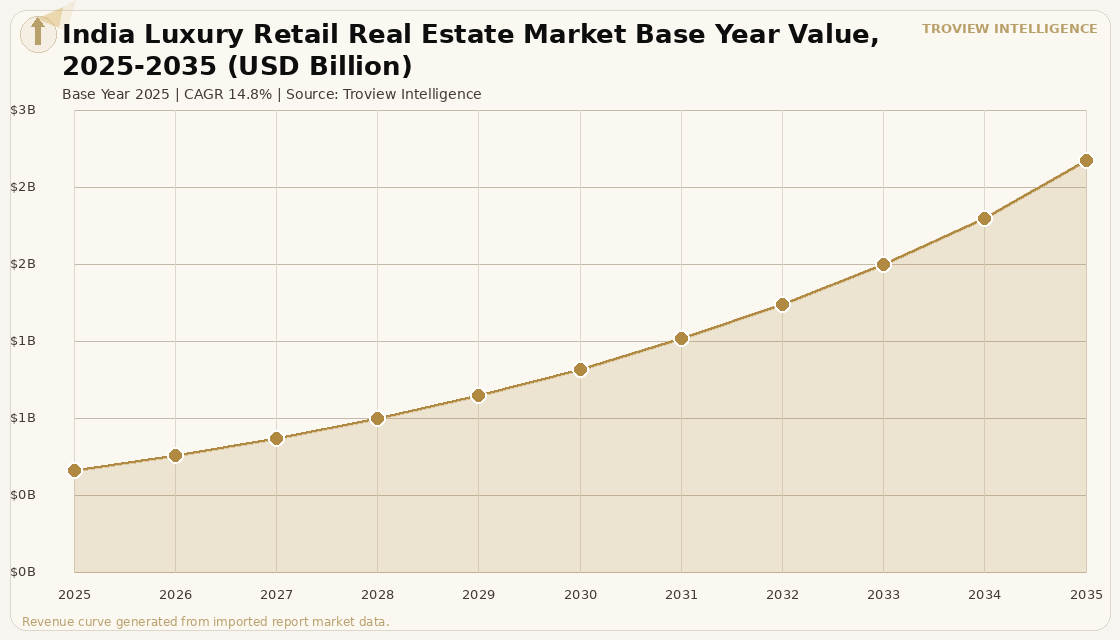

The India luxury retail real estate market size was USD 582.4 Million in 2025 and is expected to register a revenue CAGR of 14.8% during the forecast period, reaching USD 2.35 Billion by 2035. India's luxury retail real estate market is the world's most supply-constrained, with only three genuine luxury malls serving a country of 1.4 billion people that ranks fourth globally in individuals with net assets exceeding USD 100 million. DLF Emporio and DLF Chanakya in Delhi, and Jio World Plaza in Mumbai collectively represent India's entire institutional luxury mall inventory, all of which operate at full occupancy with no available space per DLF's luxury mall management disclosures. International parent companies representing brands under LVMH, Kering, and Richemont are actively requesting additional space in India, and more than a dozen prominent brands are prepared to enter the market immediately if retail space became available, per Saurabh Bharara, who oversees luxury malls at DLF, in public statements reported March 2026. India's luxury goods market was valued at USD 12.1 billion in 2024 and is projected to reach USD 85 billion by 2030 per market estimates cited by global luxury brand executives, making it one of the fastest-growing luxury markets in the world.

India's luxury retail real estate market is entering a structural inflection, with the November 2025 opening of Galeries Lafayette's first India flagship in Mumbai and the planned expansion of DLF Emporio to approximately 160,000 square feet signalling the beginning of a supply response to sustained demand that has outpaced the country's luxury real estate infrastructure for over a decade. New luxury mall projects are planned in Mumbai, Hyderabad, and Gurgaon, with four additional luxury malls expected to come online between 2026 and 2030, though each carries development timelines of three to five years that constrain the pace at which the supply-demand gap can be closed. Luxury brand entry into India is structurally linked to the availability of purpose-built luxury mall space, with the opening of DLF Chanakya in 2017 directly triggering a surge in brand entries that year per historical brand opening analysis, and the opening of Jio World Plaza in 2023 triggering a new wave of first-India entries including Balenciaga, Valentino, and Rimowa. For instance, in November 2025, Galeries Lafayette Group, France, opened India's first multi-brand luxury department store in Mumbai's historic Fort neighbourhood, a five-floor 90,000 square foot store housing over 250 luxury and designer brands in partnership with Aditya Birla Fashion and Retail Limited, per Reuters and AFP reporting of November 2025. These are some of the key factors driving revenue growth of the market.

However, the India luxury retail real estate market faces structural constraints. High import duties on luxury goods make India one of the most expensive markets to buy international luxury products, with import duties adding 25 to 100% to the consumer price of many luxury goods categories and pushing price-sensitive aspirational luxury buyers toward grey market imports or purchases during international travel rather than domestic retail. Infrastructure limitations including unpredictable power supply at older retail properties, congested access roads, and inconsistent air conditioning systems are inconsistent with the service standards that global luxury brands require per their global operations benchmarks. India's cultural and domestic luxury sector designer fashion houses including Sabyasachi, Tarun Tahiliani, Manish Malhotra, and Abu Jani Sandeep Khosla competes directly with international luxury brands for the premium wedding and occasion wear spending that represents the largest luxury expenditure occasion for Indian consumers. These factors substantially limit India luxury retail real estate market growth over the forecast period.

India's luxury retail real estate market is defined by a paradox that has no equivalent globally: a country that ranks fourth in the world for ultra-high-net-worth individuals, growing at 6% per year, where the world's leading luxury brands cannot find space to open stores. Only three luxury malls in the entire country. All at full occupancy. More than a dozen brands ready to sign leases if space existed. DLF Emporio's expansion to 160,000 square feet will not open until late 2028. This is not a demand problem. It is a real estate development problem that will take five to eight years to resolve, during which time India's luxury market will continue to grow and the pent-up supply will eventually deliver into one of the highest-demand-density luxury retail markets in the world." Troview Intelligence Head of India Luxury Retail Real Estate Research

SEGMENT INSIGHTS

By City

Mumbai and Delhi are expected to account for a significantly large revenue share in the India luxury retail real estate market during the forecast period.

Based on city, the India luxury retail real estate market is segmented into Mumbai, Delhi, Bengaluru, Hyderabad, and other emerging luxury retail cities. Mumbai and Delhi together account for the entirety of India's institutional luxury mall market Mumbai with Jio World Plaza and Galeries Lafayette Fort, and Delhi with DLF Emporio and DLF Chanakya. Delhi's luxury retail malls are fully occupied with no vacancy per DLF management disclosures. Bengaluru is the third-largest luxury retail market through UB City, India's first purpose-built luxury mall, and the Phoenix Palladium equivalent in the city, serving Bengaluru's large technology sector wealth base. Hyderabad is projected to have the highest CAGR in total retail sales of all Indian cities at 8.4% per year between 2024 and 2029 per Oxford Economics city-level analysis, making it the most significant emerging luxury retail real estate market outside the current three-city concentration.

By Mall Format

Dedicated luxury-only malls are expected to account for a significantly large revenue share in the India luxury retail real estate market during the forecast period.

Based on mall format, the India luxury retail real estate market is segmented into dedicated luxury-only malls, luxury floors within premium mixed-use malls, standalone luxury brand flagship stores, hotel boutique retail within five-star hotels, and luxury high street retail in affluent neighbourhoods. Dedicated luxury-only malls dominate India's institutional luxury retail real estate market, with DLF Emporio and DLF Chanakya in Delhi and Jio World Plaza in Mumbai collectively representing the entire purpose-built luxury mall inventory. All three are fully leased with no vacancy. Standalone luxury brand stores in five-star hotel retail arcades the Taj Mahal Hotel in Delhi, Taj Lands End and Four Seasons in Mumbai, Leela Palaces across India historically provided the only luxury brand access before the dedicated luxury mall format emerged in 2008 with DLF Emporio. Galeries Lafayette's Fort Mumbai location, at 90,000 square feet across five floors in a repurposed historic building, represents a new multi-brand luxury department store format that operates outside the dedicated luxury mall structure.

By Developer

DLF Limited and Reliance Industries are expected to account for a significantly large revenue share in the India luxury retail real estate market during the forecast period.

Based on developer, India's luxury retail real estate market is dominated by DLF Limited and Reliance Industries. DLF Limited operates DLF Emporio in Vasant Kunj, Delhi India's first luxury mall, opened 2008, spanning 320,000 square feet across four levels housing 65 international brands and 129 Indian designer brands and DLF Chanakya, a newer luxury retail and lifestyle destination in Chanakyapuri, Delhi. DLF plans to expand Emporio to approximately 160,000 square feet of new leasable area, though the expansion is not expected to open before late 2028. Reliance Industries owns and operates Jio World Plaza in Mumbai's Bandra Kurla Complex, India's largest luxury mall at 750,000 square feet housing 66 luxury brands. The Aditya Birla Group, through its retail arm Aditya Birla Fashion and Retail Limited, operates as a luxury distribution platform rather than a real estate developer, having partnered with Galeries Lafayette for the Fort Mumbai multi-brand luxury store.

Four Cities Shaping India's Luxury Retail Real Estate

| Jio World Plaza | 750,000 sq ft, 66 luxury brands, BKC, Reliance Industries | Galeries Lafayette Fort | 90,000 sq ft, 5 floors, 250+ brands, Aditya Birla, Nov 2025 |

| Palladium Rents | Base INR 433/sq ft/month; effective INR 600+ for top performers | Luxury Market Share | ~47% of India luxury retail real estate market |

Mumbai is India's largest luxury retail real estate market, home to Jio World Plaza at 750,000 square feet in Bandra Kurla Complex and the November 2025 launch of Galeries Lafayette's first India store in the historic Fort neighbourhood. Jio World Plaza hosts 66 luxury brands including India's largest Louis Vuitton store, Dior's first menswear outlet, and first-India entries including Balenciaga, Valentino, Rimowa, and Giorgio Armani Café, integrated with the Nita Mukesh Ambani Cultural Centre and Jio World Convention Centre to create India's most complete luxury lifestyle district. Galeries Lafayette's Fort Mumbai location, a five-floor 90,000 square foot space housing over 250 brands in partnership with Aditya Birla Fashion and Retail, represents a different format a multi-brand luxury department store in a repurposed historic building than the Reliance-owned purpose-built luxury mall. Palladium at High Street Phoenix, Lower Parel, operates as Mumbai's premium aspirational mall with base rents averaging INR 433 per square foot per month per market data.

| DLF Emporio | 320,000 sq ft, 65 international + 129 Indian designer brands, Vasant Kunj | DLF Chanakya | Luxury retail and lifestyle, Chanakyapuri, fully leased |

| Emporio Expansion | ~160,000 sq ft new GLA planned, expected not before late 2028 | LVMH/Kering/Richemont | Actively requesting additional India space; 12+ brands on waitlist |

Delhi is the origin city of Indian luxury retail real estate, home to DLF Emporio India's first luxury mall, opened 2008 in Vasant Kunj which houses Louis Vuitton, Cartier, Gucci, Christian Louboutin, Dior, Fendi, and over 60 international brands alongside 129 Indian designer labels across 320,000 square feet. DLF Chanakya, DLF's second luxury mall in the diplomatic Chanakyapuri district, provides a different profile serving the diplomatic community and South Delhi affluent resident catchment. Both Delhi luxury malls operate at full occupancy with no available space, per DLF management disclosures. DLF's planned Emporio expansion of approximately 160,000 square feet of new leasable area is expected not before late 2028, confirming that international brands requesting additional India space face at minimum a three-year wait before the country's most established luxury mall destination can accommodate them. The Mall at Worldmark in Aerocity, near Indira Gandhi International Airport, is developing as a globally benchmarked luxury retail environment that will provide the capital's next luxury retail infrastructure.

| UB City | India's first luxury mall, Bengaluru, UB City mixed-use complex | Technology Wealth | Largest concentration of USD millionaires from tech sector outside Mumbai/Delhi |

| Luxury Growth Rate | Strong demand from tech sector HNIs and startup ecosystem | New Supply | Phoenix Palladium Bengaluru and other premium destinations |

Bengaluru is India's third-largest luxury retail real estate market, anchored by UB City, the luxury-focused mixed-use development that houses the country's original luxury retail environment alongside premium offices and hospitality. The city's massive technology sector wealth base comprising senior executives, founders, and early employees of Infosys, Wipro, Flipkart, Swiggy, Zepto, and hundreds of funded startups generates the highest concentration of newly wealthy consumers under 45 outside Mumbai and Delhi, creating a structurally different luxury demand profile: younger, more globally exposed, and more willing to spend on international luxury fashion brands than the older generation of business family wealth that characterised Delhi and Mumbai luxury spending historically. Global luxury brands including Hermes, Cartier, Louis Vuitton, and Gucci have established Bengaluru presences at UB City and through hotel boutiques at the Taj West End and Leela Palace, but the city's luxury retail infrastructure remains undersized relative to its wealth base.

| Retail CAGR Forecast | 8.4% per year 2024-2029 (Oxford Economics, highest of all Indian cities) | Wealth Profile | Pharma, IT and BioTech sector HNI concentration |

| Key Asset | Hyderabad's luxury retail currently served through premium malls and hotels | Pipeline | New luxury mall planned as part of Hyderabad's luxury real estate development |

Hyderabad is projected to have the highest CAGR in total retail sales of all Indian cities at 8.4% per year between 2024 and 2029 per Oxford Economics city-level analysis, making it the most significant emerging luxury retail real estate opportunity in India outside the current Mumbai-Delhi duopoly. The city's wealth is anchored by the pharmaceutical sector concentrated in its Genome Valley biotech hub Dr. Reddy's Laboratories, Sun Pharma, Divi's Laboratories and a fast-growing information technology sector in the HITEC City and Gachibowli corridors that is generating a new generation of luxury consumers. Hyderabad's luxury retail market is currently underserved by its retail infrastructure, with luxury brands primarily operating through five-star hotel boutiques at the Taj Krishna, ITC Kakatiya, and Park Hyatt, or through the premium floor of larger malls that lack the dedicated luxury environment that international brands require. A purpose-built luxury mall project in Hyderabad is among the four new luxury destinations identified as being planned for India's next luxury retail development cycle.