By REIT Structure · By Asset Type · By Tenant Sector · By City

City Spotlights: Tokyo · Osaka

Japan's data centre market reached USD 12.76 billion in 2025 and is projected to grow at a CAGR of 20.42% to 2031, Keppel DC REIT completed the acquisition of Tokyo Data Centre 3 in Inzai City for JPY 82.1 billion approximately USD 530 million in December 2025 on a 15-year lease to a global hyperscaler, seven new data centres added over 200 MW of capacity across Japan in 2025 with a further 1.2 gigawatts announced or under construction, and NTT DATA completed its USD 16.4 billion buyout by parent NTT in July 2025, integrating nearly 1 gigawatt of planned capacity and cementing Japan as the second-largest data centre market among developed nations after the United States.

MARKET SYNOPSIS

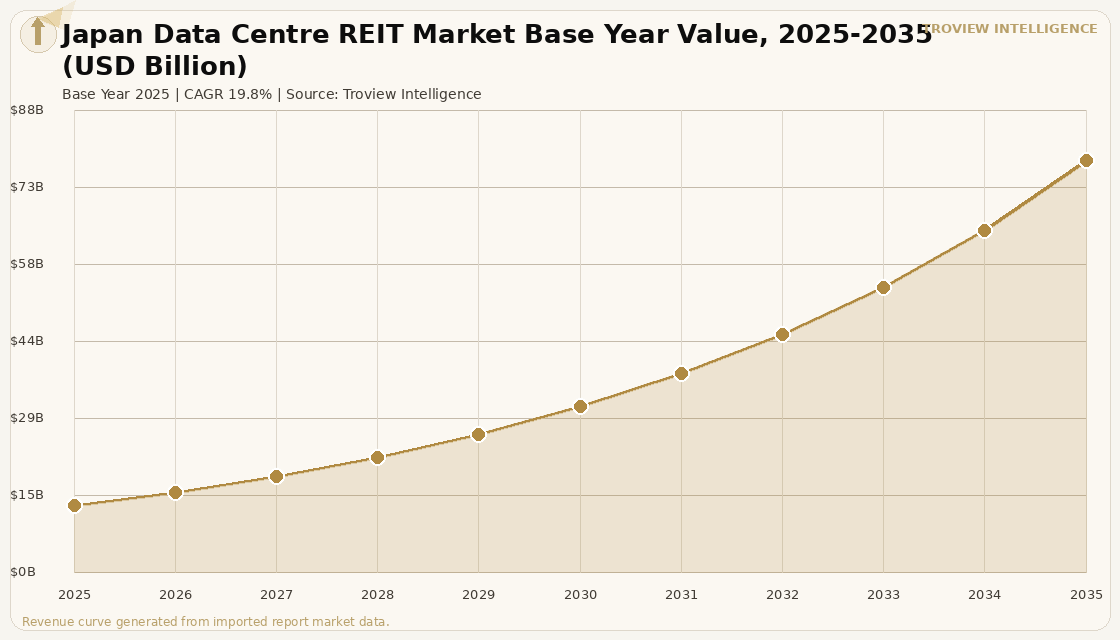

The Japan data centre REIT market size was USD 12.76 Billion in 2025 and is expected to register a revenue CAGR of 19.8% during the forecast period, reaching USD 78.14 Billion by 2035. Japan is the second-largest data centre market among developed countries after the United States, with the Japan Financial Services Agency's promotion of data centre REIT structures expected to generate a virtuous cycle of increased sector investment and improved transparency per JLL research, while the Ministry of Economy, Trade and Industry's energy efficiency standards are accelerating decarbonisation through liquid cooling and immersion cooling technology deployment. Japan recorded seven new data centres adding over 200 megawatts of capacity in 2025, with a further 1.2 gigawatts announced, planned, or under construction within the same year, and major operators including AT TOKYO, NTT Global Data Centers, Equinix, MC Digital Realty, AirTrunk, Colt Data Centre Services, and IDC Frontier collectively accounting for over 1 gigawatt of operational capacity. For instance, in December 2025, Keppel DC REIT, Singapore, completed the acquisition of a 98.47% effective interest in Tokyo Data Centre 3 in Inzai City, Greater Tokyo, for JPY 82.1 billion (approximately USD 530 million), a freehold hyperscale facility built in 2025 and fully leased to a leading global hyperscaler on a 15-year contract with annual rent escalations, immediately DPU-accretive by 2.8% and positioning Japan as the REIT's largest single-country exposure outside Singapore per SGX filing of December 2025. These are some of the key factors driving revenue growth of the market.

Japan's data centre investment landscape in 2025 is characterised by accelerating hyperscaler and cloud provider commitment across Tokyo and Osaka, with cloud giants including Amazon Web Services, Alibaba Cloud, Google, Microsoft, Oracle, and Tencent Cloud all maintaining dedicated cloud regions in Japan. In July 2025, NTT DATA completed its USD 16.4 billion buyout by parent NTT, integrating nearly 1 gigawatt of planned capacity including 100 megawatts in Tochigi, in a transaction that consolidates NTT's position as Japan's dominant data centre operator and creates a single-entity platform capable of competing for sovereign cloud mandates from the Japanese government's GovCloud programme. AirTrunk, Australia, opened its second Tokyo hyperscale data centre in May 2025, expanding domestic capacity toward a 300 megawatt TOK1 campus, while Gaw Capital Partners and GDS partnered in April 2025 to develop a 40 megawatt carrier-neutral campus in Fuchu Intelligent Park west of Tokyo targeting end-2026 operations, both transactions demonstrating sustained foreign institutional capital commitment to the Japanese market. Japan's data centre market in terms of IT load capacity is expected to grow from 3.34 thousand megawatts in 2025 to 6.46 thousand megawatts by 2030 at a CAGR of 14.12%.

However, the Japan data centre REIT market faces structural constraints that limit the pace of new supply delivery. The Iran-US geopolitical tensions and resulting Strait of Hormuz disruptions, confirmed by the IMF in March 2026 to affect approximately 20% of global seaborne oil and LNG flows, are generating energy cost inflation for Japanese data centre operators who depend on LNG imports for baseload electricity generation via TEPCO and KEPCO, Japan's two primary utility providers for data centre clients. Rising power and land constraints in Tokyo are pushing investors to view Osaka as a strategic alternative and to explore emerging locations including Hokkaido, Kyushu, Nagoya, and Yokohama that offer land availability, government support, and lower construction costs but require longer fibre backhaul routes to the primary demand centres. Rack power density requirements surpassing 70 kilowatts per rack for AI inference workloads are forcing a pivot from air cooling to immersion and direct-to-chip liquid cooling at capital costs 40 to 60% above those of air-cooled predecessors, requiring operators to fund expensive infrastructure upgrades at existing facilities or commit to higher-specification greenfield builds. These factors substantially limit Japan data centre REIT market growth over the forecast period.

TROVIEW ANALYST PERSPECTIVE "Japan's data centre REIT market in 2025 has three structural advantages that no other Asia Pacific market simultaneously possesses. First, yen-denominated acquisition financing allows foreign REITs including Keppel DC REIT to borrow in JPY at rates substantially below USD rates, mitigating currency risk while reducing cost of capital on Japanese assets. Second, Japan's sovereign cloud mandates and data residency regulations create a captive domestic cloud infrastructure demand that cannot be served from Singapore or Hong Kong, locking in hyperscaler commitment to local capacity. Third, the Japanese government's Financial Services Agency promotion of data centre REIT structures provides a policy framework that will likely produce domestically-listed J-REIT vehicles for data centre assets within the next three years, creating a new pool of domestic institutional capital for the sector. The constraint energy costs rising with LNG price volatility and the 70 kW-per-rack AI workload density that is making existing air-cooled facilities obsolete before they are fully depreciated is real. But it applies equally to every market globally. In Japan, the demand signal is more concentrated and the supply constraint is more structural than almost anywhere outside Northern Virginia." Troview Intelligence Head of Japan Data Centre REIT Research

SEGMENT INSIGHTS

Two Cities Shaping Japan's Data Centre REIT Market

| Operational DCs (Jun 2025) | Upcoming DCs | IT Load Capacity Growth (Japan) | Key REIT Asset |

| 74 in Tokyo | 26 under construction | 3.34K MW (2025) to 6.46K MW (2030) | Keppel DC REIT Tokyo DC 3 (USD 530M) |

Tokyo is Japan's primary data centre hub and the largest data centre market in Asia Pacific outside China, with 74 existing and 26 upcoming data centres as of June 2025 per verified operator data, hosting dedicated cloud regions for all six major global cloud providers and concentrated hyperscale demand that cannot be served from alternative locations due to enterprise and government proximity requirements. AirTrunk's TOK1 campus is expanding toward 300 megawatts with a 40 megawatt addition opened in May 2025, while Gaw Capital Partners and GDS are developing a 40 megawatt carrier-neutral campus in Fuchu Intelligent Park west of Tokyo for end-2026 operations, both reflecting the continued confidence of foreign institutional capital in Tokyo's data centre demand-supply dynamics. Rising power and land costs in central Tokyo are pushing developers to Inzai City in Greater Tokyo where Keppel DC REIT's Tokyo Data Centre 3 is located and to Fuchu, Sagamihara, and Tochigi for large-campus development where TEPCO grid connection timelines are more predictable and land costs lower than in the Tokyo metropolitan core.

| Osaka Share of Upcoming Capacity | Key Cloud Regions | KDDI-HPE AI Campus | Grid Utility |

| Over 60% with Tokyo combined | AWS, Microsoft, Google, Oracle, Alibaba | Launch FY2025, NVIDIA Blackwell chips | KEPCO competitive tariffs |

Osaka is Japan's second data centre market and is increasingly viewed as a strategic complement to Tokyo by operators facing power and land constraints in the capital. Tokyo and Osaka together account for over 60% of Japan's total upcoming data centre power capacity per verified operator data, with Osaka offering better capacity headroom while still serving major cloud and enterprise demand centres in the Kansai region. KDDI and Hewlett Packard Enterprise announced a new Osaka AI data centre incorporating NVIDIA Blackwell chips for launch in fiscal year 2025, demonstrating the willingness of Japanese telecommunications operators to deploy cutting-edge AI hardware in Osaka facilities that benefit from KEPCO's competitive electricity tariffs relative to TEPCO's Tokyo pricing. NTT DATA launched its Keihanna facility in Kyoto in 2025, a 30 megawatt AI-ready facility featuring advanced cooling and dual power infrastructure, strengthening the Kansai region as a data centre hub and attracting Osaka co-investment from REITs and institutional funds seeking geographic diversification within Japan beyond the Tokyo concentration.